Market Overview

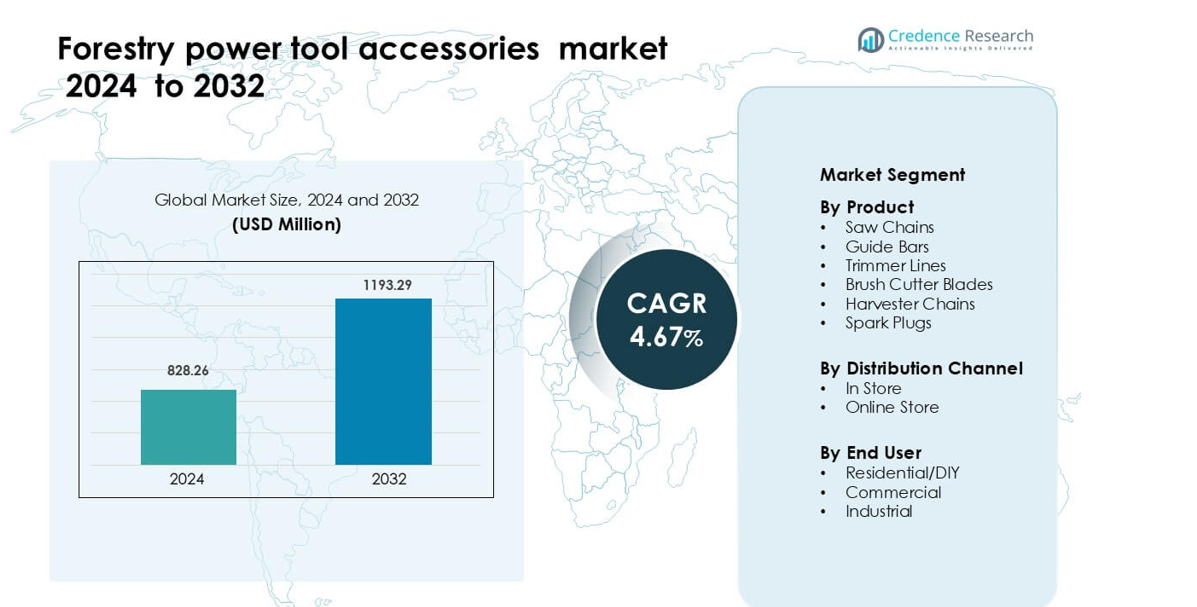

Forestry power tool accessories market was valued at USD 828.26 million in 2024 and is anticipated to reach USD 1193.29 million by 2032, growing at a CAGR of 4.67 % during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Forestry Power Tool Accessories Market Size 2024 |

USD 828.26 million |

| Forestry Power Tool Accessories Market, CAGR |

4.67% |

| Forestry Power Tool Accessories Market Size 2032 |

USD 1193.29 million |

The forestry power tool accessories market is shaped by strong competition from leading companies such as GB Forestry, Oregon, STIHL, Einhell, MTD Products, STIGA S.P.A, Husqvarna, Cannon Bar Works, Bahco, and Iggesund. These brands focus on durable saw chains, guide bars, trimmer lines, and brush cutter blades that support both commercial forestry operations and residential landscaping tasks. Product innovation centers on wear-resistant materials, low-kickback designs, and optimized accessories for battery-powered equipment. Asia Pacific stands as the leading region with a 36% share in 2024, driven by extensive forestry activities, rapid urban expansion, and rising adoption of outdoor power tools across major economies.

Market Insights

- Forestry power tool accessories market was valued at USD 828.26 million in 2024 and is anticipated to reach USD 1193.29 million by 2032, growing at a CAGR of 4.67 % during the forecast period.

- Strong market drivers include rising adoption of chainsaws, trimmers, and brush cutters across forestry, landscaping, and residential maintenance, with saw chains holding the largest share at 41% in 2024.

- Key trends include wider use of battery-powered outdoor tools, increasing demand for low-vibration and low-kickback accessories, and material innovations such as hardened alloys and friction-reduction coatings.

- Competitive intensity remains high as companies like Oregon, STIHL, Husqvarna, GB Forestry, and Cannon Bar Works focus on durability, compatibility, and premium-grade accessories to expand their customer base.

- Asia Pacific leads the market with a 36% regional share due to extensive forestry operations and rapid urban development, followed by North America at 33%, which benefits from strong commercial landscaping and wildfire-management activities.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Product

Saw chains hold the largest share in this segment with nearly 41% in 2024. Strong demand comes from chainsaws used in logging, firewood cutting, and tree maintenance across residential and commercial tasks. Buyers favor saw chains because they offer high cutting efficiency, long service life, and wide compatibility with major power tool brands. Trimmer lines and guide bars show steady adoption as landscaping and brush-clearing needs grow, while harvester chains and brush cutter blades gain traction in mechanized forestry operations.

- For instance, Husqvarna’s X‑CUT® saw chain uses a low‑vibration pixel design and pre-stretched chrome and steel, which helps the chain maintain its sharpness over prolonged use and reduces the need for frequent re‑tensioning.

By Distribution Channel

In-store sales dominate this segment with about 64% share in 2024, driven by consumer preference for hands-on inspection and expert guidance before purchase. Hardware stores, specialty dealers, and equipment retailers offer quick availability and service support, which strengthens offline demand. Online stores continue to grow due to better price transparency and wide product selection. E-commerce gains momentum among DIY users and small contractors, but physical stores retain leadership because they provide immediate replacement parts for urgent forestry tasks.

- For instance, Husqvarna Group serves customers in over 100 countries through a network of direct sales, dealers, and retailers. These authorized dealers do offer service andsupport, including maintenance and genuine parts replacement.

By End User

Commercial users lead this segment with nearly 48% share in 2024 as forestry contractors, tree-care firms, and landscaping companies rely heavily on durable accessories for frequent and high-load operations. Demand grows because professional crews prioritize performance, reliability, and compatibility with heavy-duty equipment. Residential/DIY users follow, supported by rising home gardening and small-scale tree-maintenance activities. Industrial users show steady adoption in mechanized logging sites where advanced harvester chains and guide bars support continuous, high-capacity workloads.

Key Growth Drivers

Rising Demand for Efficient Woodcutting and Landscaping Tasks

Demand for forestry power tool accessories grows as households, contractors, and commercial users increase their use of chainsaws, trimmers, cutters, and harvesters for routine land clearing and precision cutting. Expanding urban landscaping projects, wildfire prevention programs, and tree-health maintenance activities boost the need for reliable accessories that improve cutting efficiency and reduce downtime. Saw chains and guide bars benefit the most because they support high-frequency cutting tasks across forestry and residential applications. Growing replacement cycles also lift demand since accessories wear faster under heavy loads. Manufacturers focus on improved durability, sharper cutting edges, and low-kickback designs to support safer and faster operations across skill levels.

- For instance, Oregon’s LubriTec system, integrated into its guide bars and chains, uses specially designed oil flow features to reduce friction, thereby extending the service life of the chain under high-stress cutting.

Expansion of Mechanized Forestry and Professional Tree-Care Services

Mechanized forestry continues to expand as countries adopt advanced logging machines, brush cutters, harvesters, and high-torque chainsaws that depend on performance-grade accessories. Harvester chains, guide bars, and brush cutter blades see higher adoption as commercial operators shift from manual tools to mechanized solutions that increase productivity and reduce labor strain. Tree-care companies and landscaping services also drive growth because they require frequent accessory replacements to maintain operational safety and service quality. Increased spending on arboriculture services in cities and infrastructure corridors adds to demand. Continuous innovation in wear-resistant coatings, vibration-reduction designs, and high-strength materials helps professional users achieve better fuel efficiency and cleaner cuts, strengthening accessory sales across commercial and industrial end users.

- For instance, Oregon’s 18HX harvester chain is built on patented OCS‑01 steel and has a pitch of 0.404″ with a gauge of 0.080″, and is chrome‑plated to retain edge even under high‑speed, cold logging conditions.

Rising Adoption of Battery-Powered Outdoor Equipment

The shift toward battery-powered chainsaws, trimmers, and brush cutters stimulates strong demand for compatible accessories designed to enhance run time and cutting precision. Governments encourage battery equipment adoption through emission-reduction policies, and users favor these tools for lower noise and easier handling. This shift boosts sales of lightweight saw chains, optimized guide bars, and low-resistance trimmer lines tailored for cordless platforms. Manufacturers develop accessories with reduced friction, improved balance, and extended wear life to match the performance needs of high-power lithium-ion tools. Growth in residential DIY gardening and small-scale forestry work further supports battery-equipment penetration, increasing replacement frequency and long-term demand for durable accessories across global markets.

Key Trends & Opportunities

Rising Integration of Advanced Materials and Coatings

Manufacturers increasingly apply hardened alloys, carbide-tipped blades, nano-coatings, and corrosion-resistant metals to improve durability and cutting precision. This trend creates opportunities for accessories that last longer under high-load forestry operations, reducing downtime and enhancing operational safety. Demand rises for low-kickback saw chains, heat-treated guide bars, and reinforced trimmer lines as professional users seek performance consistency. Innovations in friction-reduction coatings help boost run time in battery-powered tools, creating a strong market for premium accessories. Companies focusing on advanced metallurgy and precision engineering gain a competitive edge as end users shift toward high-efficiency tools that support both productivity and cost savings.

- For instance, Husqvarna’s X‑CUT saw chain is manufactured from pre‑stretched chrome and steel that undergoes a proprietary heat‑treatment process to strengthen its molecular structure, while its links have arrow-shaped oil channels that improve lubrication contributing to smoother cuts and extended service life.

Growing Digital and Smart Forestry Solutions

Digital forestry tools, including sensor-based equipment monitoring, connected power tools, and automated sharpening systems, open new opportunities for accessory optimization. Smart guide bars, chain-wear indicators, and auto-lubrication systems improve accuracy and reduce manual adjustments, making forestry operations safer and more efficient. Professional logging firms adopt telematics-supported equipment to track usage cycles and schedule predictive maintenance, boosting recurring demand for accessories. These advancements support stronger adoption of premium parts engineered for precision and compatibility with digital platforms. As data-driven forestry operations expand, suppliers can create value-added accessories that integrate with smart tool ecosystems and enhance long-term operational performance.

- For instance, Oregon’s Power Sharp™ system allows on‑saw sharpening in just 3–5 seconds by pulling a lever, reducing downtime and ensuring the chain is routinely resharpened.

Growing Focus on Safety and Ergonomic Designs

Rising awareness of operator safety drives demand for accessories engineered to reduce risk during cutting, trimming, and harvesting. Low-vibration guide bars, anti-kickback saw chains, and balanced trimmer lines gain traction among both professional and residential users. Manufacturers innovate with lightweight materials and ergonomic designs to reduce fatigue and improve tool handling, particularly in battery-powered equipment. Training programs in commercial forestry and arboriculture highlight the role of safer accessories, increasing replacement frequency for compliant products. This creates strong opportunities for companies offering certified, safety-enhanced accessories that meet evolving regulatory and workplace safety standards.

Key Challenges

High Wear Rates and Frequent Replacement Costs

Forestry power tool accessories face high wear and tear due to intense cutting loads, abrasive materials, and continuous exposure to harsh outdoor environments. Frequent replacements increase operational expenses for professional users, making cost-sensitive buyers hesitant to adopt premium accessories. Consistent performance also becomes harder to maintain as accessory quality deteriorates, especially in budget-grade products. Manufacturers must balance durability and affordability, but rising material costs challenge competitive pricing. Users in remote forestry locations also struggle with limited access to replacement parts, which can slow operations and reduce productivity, reinforcing the challenge of maintaining steady supply and cost control.

Stringent Safety and Environmental Regulations

Regulations governing noise levels, emissions, vibration exposure, and workplace safety affect how accessories are designed and used across forestry applications. Manufacturers must meet strict standards for low-kickback chains, reduced-vibration guide bars, and safe-handling designs, increasing development and compliance costs. Environmental policies push users toward battery-powered tools, requiring accessories optimized for lower friction and higher energy efficiency. Smaller manufacturers often struggle to keep pace with regulatory updates, causing market fragmentation. Compliance failures can lead to product recalls or restricted market access, making regulatory complexity a major challenge for both established and emerging accessory suppliers.

Regional Analysis

North America

North America holds about 33% share of the forestry power tool accessories market in 2024, supported by strong demand from commercial forestry, landscaping contractors, and DIY homeowners. The United States leads due to extensive woodcutting operations, wildfire management programs, and widespread adoption of battery-powered outdoor tools. Replacement demand for saw chains, guide bars, and trimmer lines stays high because professional users operate large fleets of power tools. Rising urban landscaping and tree-care services further lift consumption. Canada contributes steady growth as harvesting activities and mechanized forestry expand, driving continued uptake of durable, high-efficiency accessories.

Europe

Europe accounts for nearly 27% share in 2024, driven by well-established forestry industries in Germany, Sweden, Finland, and France. High adoption of professional-grade chainsaws, brush cutters, and harvesters supports steady demand for premium accessories with strict compliance to EU safety and sustainability standards. Users prioritize low-emission and low-vibration tools, boosting accessory upgrades that enhance efficiency in regulated work environments. Landscaping services and municipal maintenance programs contribute to consistent replacement cycles. Growing interest in battery-powered garden equipment among homeowners also strengthens sales of lightweight saw chains, trimmer lines, and ergonomic guide bars.

Asia Pacific

Asia Pacific leads the market with about 36% share in 2024, supported by large forestry operations, rapid urban development, and rising landscaping activities across China, India, Japan, and Southeast Asia. China drives the majority of demand due to extensive timber harvesting, strong domestic manufacturing, and expanding outdoor equipment use in both commercial and residential settings. Growth in small-scale farming, plantation management, and rural land-clearing boosts accessory consumption. Japan and Australia contribute significant demand for high-quality chains, bars, and trimmer lines, while increasing adoption of battery tools accelerates uptake of lightweight, high-efficiency accessories.

Latin America

Latin America holds nearly 8% share in 2024, influenced by expanding forestry activities in Brazil, Chile, and Argentina. Demand for saw chains, harvester chains, and brush cutter blades grows as mechanized logging and plantation forestry become more common. Rising investment in agriculture and land-clearing projects supports broader adoption of trimmers and cutters, boosting accessory use across rural markets. While economic fluctuations affect purchasing capacity, consistent replacement needs sustain demand. Local distributors and retail networks play a key role in market expansion, particularly as safety-focused and durable products gain preference among professional users.

Middle East & Africa

The Middle East & Africa region accounts for about 6% share in 2024, driven by growing landscaping, agriculture, and municipal maintenance activities. Countries such as South Africa, Kenya, and the UAE show rising demand for trimming and cutting tools used in estate management, roadway maintenance, and green-area development. Forestry-related usage remains smaller but gains traction where commercial timber operations exist. Sales are led by trimmer lines, brush cutter blades, and guide bars, supported by increasing urban development. Limited local manufacturing creates opportunities for international brands offering durable, cost-effective accessories suited to varied climatic conditions.

Market Segmentations:

By Product

- Saw Chains

- Guide Bars

- Trimmer Lines

- Brush Cutter Blades

- Harvester Chains

- Spark Plugs

By Distribution Channel

By End User

- Residential/DIY

- Commercial

- Industrial

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The forestry power tool accessories market shows strong competition among established global brands and specialized manufacturers offering saw chains, guide bars, trimmer lines, brush cutter blades, and harvester chains. Key players such as GB Forestry, Oregon, STIHL, Einhell, MTD Products, STIGA S.P.A, Husqvarna, Cannon Bar Works, Bahco, and Iggesund focus on durability, precision engineering, and compatibility with a wide range of power tools. Companies strengthen market presence through product upgrades, heat-treated materials, low-kickback designs, and friction-reduction technologies tailored for both fuel-powered and battery-powered outdoor equipment. Many brands expand digital support services, dealer networks, and aftersales programs to secure recurring demand from commercial and residential users. Growing emphasis on sustainability encourages manufacturers to adopt eco-friendly coatings and energy-efficient designs. Competitive intensity increases as suppliers target professional forestry operators, landscapers, and DIY users with performance-grade accessories that improve cutting efficiency, reduce wear, and support safer field operations across global markets.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- GB Forestry

- Oregon

- STIHL

- Einhell

- MTD Products

- STIGA S.P.A

- Husqvarna

- Cannon Bar Works

- Bahco

- Iggesund

Recent Developments

- In March 2025, Oregon Tool introduced its TerraMax™ trimmer line for harsh, rocky terrain. The high-grade copolymer blend increases strength and stiffness for dense vegetation cutting. Company tests report less line flutter, more stability, and faster cutting versus prior lines.

- In September 2023, STIHL released a technology article on its forestry saw chains and guide bars. .325″ Pro chains deliver about 20% faster cutting with 20% less vibration than earlier lines. The Light 04 guide bar is up to 200 g lighter and reduces kickback while improving balance in felling and pruning work.

Report Coverage

The research report offers an in-depth analysis based on Product, Distribution Channel, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will see rising demand for high-durability accessories as mechanized forestry expands.

- Battery-powered outdoor tools will drive development of lightweight, low-resistance chains and guide bars.

- Premium accessories with advanced coatings will gain higher adoption among commercial users.

- Digital tool integration will support growth in smart accessories with wear indicators and optimized lubrication.

- Replacement cycles will increase as professional forestry operations intensify across developing regions.

- Sustainability goals will push manufacturers to adopt eco-friendly materials and production methods.

- Growth in landscaping and municipal maintenance will lift demand for trimmer lines and brush cutter blades.

- Global brands will expand service networks to strengthen aftersales support and customer retention.

- Adoption of ergonomic and low-vibration designs will rise as safety regulations tighten.

- Asia Pacific will remain the fastest-expanding market due to strong forestry activity and rapid urbanization.