Market Overview:

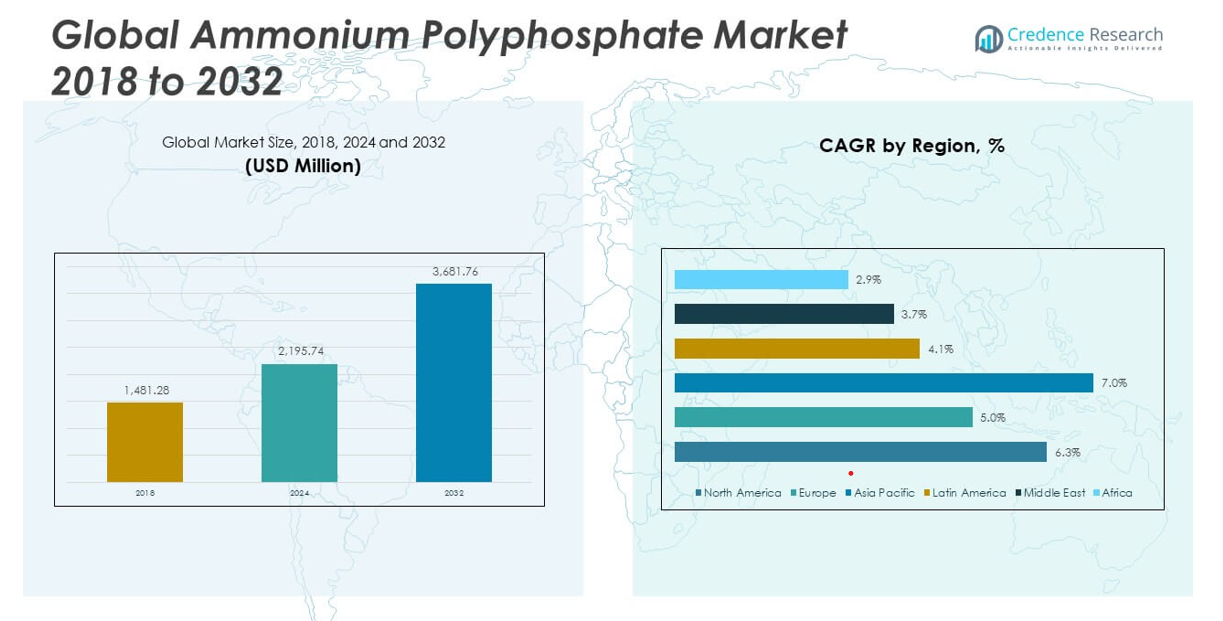

The Global Ammonium Polyphosphate Market size was valued at USD 1,481.28 million in 2018 to USD 2,195.74 million in 2024 and is anticipated to reach USD 3,681.76 million by 2032, at a CAGR of 6.21% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Ammonium Polyphosphate Market Size 2024 |

USD 2,195.74 million |

| Ammonium Polyphosphate Market, CAGR |

6.21% |

| Ammonium Polyphosphate Market Size 2032 |

USD 3,681.76 million |

The growth of the global ammonium polyphosphate market is primarily driven by increasing demand from the agriculture and fire safety sectors. In agriculture, the need for high-efficiency fertilizers to support crop yield amid rising global food demand has led to increased adoption of APP, especially its water-soluble APP-I form. Its compatibility with modern irrigation systems and precision farming practices makes it an ideal nutrient source. Simultaneously, the industrial sector is experiencing growing demand for halogen-free flame retardants, where APP-II is widely utilized in plastics, coatings, electronics, and construction materials. Stringent global fire safety regulations are accelerating the replacement of traditional halogen-based chemicals with APP due to its low toxicity and thermal stability. Additionally, environmental sustainability is becoming a central focus for manufacturers and consumers alike, pushing the adoption of non-toxic, biodegradable chemical solutions.

The Asia-Pacific region leads the global ammonium polyphosphate market, accounting for a substantial share due to robust growth in agriculture, construction, and manufacturing sectors. China dominates regional demand with its vast fertilizer production capacity and rising consumption of flame-retardant materials in electronics and infrastructure. India’s agricultural reforms and government support for sustainable fertilizers are enhancing the use of APP-I. North America holds the second-largest market share, driven by widespread adoption of precision farming techniques, advanced agricultural infrastructure, and stringent fire safety regulations that promote APP-II in building materials and industrial applications. Europe shows steady growth supported by environmental regulations that favor halogen-free, eco-friendly flame retardants. Countries like Germany, France, and the UK are leading in demand for non-toxic additives. Meanwhile, Latin America and the Middle East & Africa are emerging markets, with increasing agricultural investments, expanding construction projects, and rising awareness of fire safety measures contributing to long-term growth potential in these regions.

Market Insights:

- The Global Ammonium Polyphosphate Market reached USD 2,195.74 million in 2024 and is projected to hit USD 3,681.76 million by 2032, expanding at a CAGR of 6.21%.

- Demand from agriculture is rising due to APP-I’s compatibility with modern irrigation systems and its role in improving crop yield through balanced nutrient delivery.

- The flame retardant industry increasingly adopts APP-II in plastics, coatings, and construction materials to comply with stricter fire safety standards.

- Sustainability efforts are driving the shift toward non-toxic and biodegradable chemical alternatives, positioning APP as a preferred green solution.

- Product innovations, including slow-release and encapsulated APP, are expanding its application in both agriculture and fire safety.

- Lack of awareness in developing regions and preference for conventional materials continue to slow market penetration in rural and semi-urban zones.

- Asia Pacific leads the market with a strong base in China and India, while North America and Europe follow due to advanced regulations and infrastructure.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Rising Demand for High-Efficiency Fertilizers in Modern Agriculture

The increasing global population and growing food demand have intensified the need for high-efficiency fertilizers that enhance crop productivity. Ammonium polyphosphate (APP), especially the APP-I grade, offers a concentrated source of nitrogen and phosphorus that supports precision farming. Farmers and agribusinesses prefer it for its high water solubility, ease of handling, and compatibility with modern irrigation systems. Government policies promoting sustainable agricultural practices and balanced nutrient use are also encouraging the use of APP-based formulations. The Global Ammonium Polyphosphate Market benefits from these trends as countries seek to improve yields and reduce environmental impact. Fertilizer manufacturers are incorporating APP in liquid and granular blends to cater to evolving agronomic needs. Demand remains strong in both developed and emerging markets, supporting steady growth in agricultural applications.

- For example, companies like Mosaic and Simplot highlight that their 10-34-0 and 11-37-0 polyphosphate fertilizersremain stable in a wide temperature range and can be stored for extended periods without crystallization, supporting large-scale, efficient farming operations.

Strengthening Fire Safety Regulations Boosting Industrial Demand

Governments worldwide are enforcing stricter fire safety regulations across construction, automotive, electrical, and textile industries. Ammonium polyphosphate functions effectively as a halogen-free flame retardant, especially in the APP-II form, which is less soluble and thermally stable. It reduces flammability in plastics, paints, intumescent coatings, and other materials, supporting compliance with fire protection standards. The Global Ammonium Polyphosphate Market is responding to this regulatory push through higher production of flame-retardant additives for construction and industrial sectors. Increased construction of high-rise buildings, data centers, and public infrastructure demands reliable fire-resistant materials. Industries are moving away from halogenated compounds due to their toxic emissions, strengthening the case for safer alternatives like APP.

Rising Focus on Environmental Sustainability in Chemical Applications

Environmental concerns are influencing material choices across multiple industries, prompting a shift toward safer, more sustainable chemical solutions. Ammonium polyphosphate, being non-toxic and low in environmental impact, is gaining preference over traditional halogenated flame retardants and synthetic fertilizers. It decomposes into ammonia and polyphosphoric acid, both of which pose minimal ecological risk. The Global Ammonium Polyphosphate Market is aligned with the demand for green chemistry and circular economy initiatives. Industries adopting eco-friendly production practices are increasingly integrating APP in product lines to meet regulatory and consumer expectations. Growing awareness of soil health and air quality is also increasing interest in biodegradable and low-emission compounds.

- For example, recent product innovations include nano-scale APP particlesthat enhance dispersion and reactivity, with specialty grades growing by 7% since 2021 to reach 35,000 metric tons annually.

Continuous Innovation in Product Formulations Enhancing Market Penetration

Product development remains a core focus for manufacturers seeking to expand the utility of ammonium polyphosphate across sectors. Advances in formulation techniques, such as encapsulation and slow-release technologies, are making APP-based fertilizers more efficient and crop-specific. In fire safety applications, manufacturers are combining APP with synergistic additives to improve flame resistance and moisture stability. These innovations help the Global Ammonium Polyphosphate Market penetrate new industrial segments and meet specialized requirements. Companies are also improving compatibility with bio-based polymers and sustainable coatings. Strategic collaborations between chemical producers and end-use industries are accelerating the adoption of customized APP solutions.

Market Trends:

Expansion of Flame-Retardant Applications Beyond Traditional Sectors

Manufacturers are exploring new application areas for ammonium polyphosphate in response to growing safety concerns and material innovations. The product is now being used in textiles, adhesives, paper coatings, and electronic casings, extending its role beyond conventional plastic and construction markets. This diversification is expanding the customer base and prompting material scientists to test compatibility with various substrates. The Global Ammonium Polyphosphate Market is adapting to these changing needs by supporting customized formulations for niche industrial uses. It helps reduce flammability in non-thermoplastic materials, where traditional halogenated agents are unsuitable. Market participants are investing in pilot projects to validate APP’s performance in emerging flame-retardant applications. Regulatory changes in fire safety standards across these new sectors further support its adoption.

- For example, Tecnosintesi reports that their Phase II APP, with a polymerization degree greater than 1000, delivers thermal decomposition onset at ≥285°Cand water solubility below 0.5 g/100 mL at 25°C, making it suitable for high-humidity and specialty applications.

Growing Investment in Research Focused on Water Insolubility Enhancement

Improving the water resistance of APP, particularly in flame-retardant coatings, has become a major research focus. Developers are seeking to enhance APP’s performance in outdoor environments where exposure to moisture limits its effectiveness. Research centers and specialty chemical companies are working on advanced coating techniques and microencapsulation to reduce solubility without compromising thermal behavior. The Global Ammonium Polyphosphate Market benefits from this effort by enabling product use in demanding applications such as exterior panels, insulation boards, and marine equipment. It allows APP-based coatings to compete with more expensive fire-retardant materials. Product trials across weather-resistant construction systems are generating new opportunities in the architectural and engineering sectors. Technical innovations in surface treatments are gradually overcoming historical application barriers.

Increasing Use of Ammonium Polyphosphate in 3D Printing and Composite Materials

The adoption of APP in 3D printing materials and polymer composites is gaining momentum as manufacturers search for lightweight, fire-resistant solutions. It is being integrated into filaments, resins, and composite structures for use in aerospace, automotive, and electronics. The Global Ammonium Polyphosphate Market is witnessing interest from additive manufacturing firms that require customizable fire-retardant compounds. It supports lightweight material development without compromising fire safety, which is critical for advanced manufacturing. End users are evaluating APP-enhanced composites for both structural and non-structural parts. Partnerships between chemical companies and 3D printing innovators are helping bring these new materials to market faster. This trend is likely to redefine the competitive landscape of fire-retardant applications in high-performance materials.

Shift Toward Transparent and Color-Stable Flame Retardant Formulations

End users are increasingly requesting flame retardants that do not compromise the visual or aesthetic properties of finished products. In response, chemical developers are introducing transparent and color-stable APP formulations for use in consumer goods, electronics, and furniture. The Global Ammonium Polyphosphate Market is supporting this trend through the supply of high-purity variants and low-residue formulations. It allows manufacturers to meet both safety and design requirements in products where visual appeal is critical. These developments address a long-standing industry challenge of balancing fire performance with material appearance. Applications in decorative laminates, LED housings, and coated furniture are driving demand for visually neutral flame-retardant systems. Companies are optimizing production processes to eliminate impurities that cause discoloration.

- For example, companies like Evonik have developed transparent and color-stable systems. Their VISIOMER® HEMA-P, when combined with a specific grade of APP, enables clear, flame-retardant waterborne acrylic coatingsfor wood, maintaining both high transparency and excellent flame-retardancy.

Market Challenges Analysis:

Limited Awareness and Application Knowledge in Emerging Markets

Despite the product’s versatility, ammonium polyphosphate remains underutilized in several developing regions due to limited technical awareness and application knowledge. End users in agriculture and construction often lack the information required to adopt APP effectively in their operations. The Global Ammonium Polyphosphate Market faces challenges in expanding to rural and semi-urban areas where traditional materials dominate due to familiarity and availability. Distributors and manufacturers must invest in training, product demonstrations, and tailored outreach to overcome resistance to change. Small-scale farmers and manufacturers tend to prioritize short-term costs over long-term efficiency, slowing the adoption of APP-based solutions. It requires targeted marketing and collaboration with local stakeholders to address knowledge gaps. Without increased technical support, market penetration in these areas will remain slow.

Complex Manufacturing Processes and Raw Material Dependencies

The production of ammonium polyphosphate involves controlled chemical reactions, quality consistency, and precise formulation—factors that demand significant technical expertise. Manufacturers depend heavily on reliable supplies of ammonia and phosphoric acid, both of which are sensitive to fluctuations in global pricing and trade regulations. The Global Ammonium Polyphosphate Market faces cost-related challenges when raw material prices surge or when supply chains become disrupted. It increases production costs, reduces profit margins, and restricts the flexibility to scale operations. Environmental regulations around emissions and chemical waste further complicate the manufacturing process. Companies must invest in process optimization and sustainability measures to maintain compliance and competitiveness. These technical and economic constraints limit the entry of new players and slow down capacity expansion.

Market Opportunities:

Rising Demand for Sustainable Alternatives in Flame Retardancy

The increasing push for environmentally safe and halogen-free flame retardants presents a strong opportunity for ammonium polyphosphate adoption across multiple industries. Manufacturers in construction, automotive, and electronics are shifting toward non-toxic solutions that comply with evolving fire safety and sustainability regulations. The Global Ammonium Polyphosphate Market is well-positioned to capture this demand by offering a reliable alternative to traditional halogenated compounds. It meets performance requirements without producing harmful byproducts, making it suitable for green building materials and eco-labeled consumer products. Companies that develop advanced APP-based formulations tailored to specific end-use requirements can gain competitive advantage. Expansion into bio-based polymers and recyclable composites further strengthens market potential.

Expansion into High-Growth Agricultural Regions and Specialty Fertilizers

Emerging economies with growing agricultural activity present strong growth prospects for ammonium polyphosphate as a nutrient-rich, water-soluble fertilizer. Governments are investing in modern farming techniques, encouraging the use of efficient nutrient systems that improve yield and soil health. The Global Ammonium Polyphosphate Market can tap into this momentum by supplying APP-I for precision agriculture and fertigation applications. It aligns with global efforts to reduce nutrient runoff and improve sustainability in food production. Customized solutions for different crops and soil conditions can accelerate adoption. Collaborations with local agritech firms and cooperatives will help improve reach and market penetration.

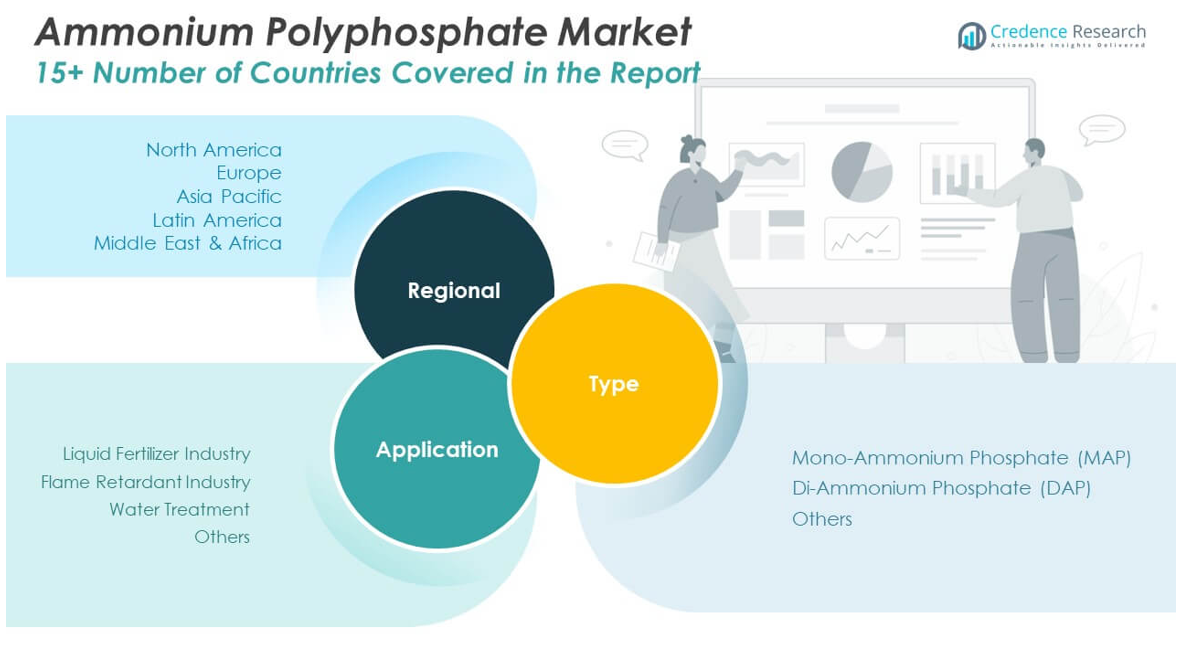

Market Segmentation Analysis:

The Global Ammonium Polyphosphate Market is segmented

By type into Mono-Ammonium Phosphate (MAP), Di-Ammonium Phosphate (DAP), and Others. DAP holds a significant share due to its high phosphorus content and widespread use in agriculture as a nitrogen-phosphorus fertilizer. It supports early plant development and is compatible with various crops, making it a preferred choice in both developed and emerging economies. MAP is also widely used, particularly where lower nitrogen concentrations are required. The “Others” segment includes specialty formulations used in niche industrial or environmental applications.

- For example, the Mosaic Company produces MAP (12-61-0) primarily for crops requiring lower nitrogen but high phosphorus. Mosaic’s MAP is favored in horticulture and specialty crops.

By application, the market is divided into Liquid Fertilizer Industry, Flame Retardant Industry, Water Treatment, and Others. The liquid fertilizer industry represents a major share due to the increasing adoption of precision farming and fertigation techniques. The flame retardant industry is experiencing strong demand for APP-II in non-halogenated fire protection systems across construction, electronics, and automotive sectors. Water treatment uses are expanding slowly, driven by environmental compliance needs. The “Others” segment includes minor applications in adhesives, coatings, and specialty chemicals. Each segment reflects distinct regulatory, environmental, and performance requirements that shape purchasing decisions and product innovation.

- For example, Simplot reports that their liquid APP fertilizers are fully water-soluble, compatible with drip and sprinkler irrigation, and improve nutrient use efficiency by up to 20%, supporting sustainable farming.

Segmentation:

By Type

- Mono-Ammonium Phosphate (MAP)

- Di-Ammonium Phosphate (DAP)

- Others

By Application

- Liquid Fertilizer Industry

- Flame Retardant Industry

- Water Treatment

- Others

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

The North America Ammonium Polyphosphate Market size was valued at USD 468.59 million in 2018 to USD 684.64 million in 2024 and is anticipated to reach USD 1,152.41 million by 2032, at a CAGR of 6.3% during the forecast period. North America accounts for approximately 24% of the global ammonium polyphosphate market share, supported by strong demand across agriculture and industrial applications. It benefits from widespread adoption of precision farming practices and the presence of advanced fertilizer infrastructure. Fire safety regulations in the U.S. and Canada drive consistent use of APP-II in coatings, electronics, and polymer compounds. The construction sector’s preference for halogen-free flame retardants further increases regional consumption. The Global Ammonium Polyphosphate Market in North America also sees innovation in slow-release and customized fertilizer solutions tailored to local soil and crop conditions. Key industry players are expanding R&D and distribution channels to strengthen market reach.

The Europe Ammonium Polyphosphate Market size was valued at USD 287.87 million in 2018 to USD 404.26 million in 2024 and is anticipated to reach USD 618.95 million by 2032, at a CAGR of 5.0% during the forecast period. Europe contributes 14% to the global market, driven by environmental regulations and growing use of non-toxic flame retardants. Countries such as Germany, France, and the UK emphasize sustainable materials in construction and consumer goods. It supports demand for APP-II in fire-resistant panels, coatings, and polymer additives. The Global Ammonium Polyphosphate Market in Europe also gains traction from its integration into circular economy practices and organic fertilizer formulations. Regional manufacturers focus on product quality and regulatory compliance, strengthening their position in export markets. Collaborative efforts between academia and industry fuel innovation and process improvements.

The Asia Pacific Ammonium Polyphosphate Market size was valued at USD 610.79 million in 2018 to USD 940.82 million in 2024 and is anticipated to reach USD 1,679.31 million by 2032, at a CAGR of 7.0% during the forecast period. Asia Pacific holds the largest share in the Global Ammonium Polyphosphate Market at 39%, driven by expanding agricultural output and rapid industrialization. China and India lead regional consumption due to large-scale farming and rising construction activities. It benefits from government subsidies on fertilizers and national initiatives promoting flame-retardant building materials. The region shows strong uptake in both APP-I and APP-II grades, supported by local manufacturing capabilities and cost advantages. Demand continues to rise in electronics and infrastructure sectors. Regional players are scaling up production to meet domestic needs and export demand.

The Latin America Ammonium Polyphosphate Market size was valued at USD 55.32 million in 2018 to USD 80.71 million in 2024 and is anticipated to reach USD 115.60 million by 2032, at a CAGR of 4.1% during the forecast period. Latin America represents 3% of the global market, with growth led by agricultural expansion in Brazil, Argentina, and Chile. It sees steady adoption of APP-based fertilizers for large-scale crop farming. The Global Ammonium Polyphosphate Market in the region benefits from public and private investment in modern farming practices. Fire safety regulations are less stringent compared to developed regions, limiting current use of APP-II in industrial applications. Opportunities exist for growth through targeted awareness programs and technology transfers. Regional distributors are partnering with international suppliers to broaden access.

The Middle East Ammonium Polyphosphate Market size was valued at USD 37.70 million in 2018 to USD 50.60 million in 2024 and is anticipated to reach USD 70.11 million by 2032, at a CAGR of 3.7% during the forecast period. The Middle East accounts for nearly 2% of the global market, driven primarily by demand from controlled irrigation agriculture and infrastructural growth. It utilizes APP-I in greenhouse and fertigation systems suited for arid conditions. The Global Ammonium Polyphosphate Market in this region shows limited penetration of APP-II due to modest enforcement of fire safety norms. Urban development projects in the UAE and Saudi Arabia are slowly increasing demand for non-halogenated flame retardants. Growth remains gradual but consistent with broader economic diversification efforts. Imports dominate supply, with few local producers currently active.

The Africa Ammonium Polyphosphate Market size was valued at USD 21.01 million in 2018 to USD 34.71 million in 2024 and is anticipated to reach USD 45.38 million by 2032, at a CAGR of 2.9% during the forecast period. Africa holds a 1% share in the global market, with growth driven by rising agricultural productivity and food security initiatives. Countries such as South Africa, Kenya, and Nigeria are investing in fertilizer infrastructure and modern crop management techniques. The Global Ammonium Polyphosphate Market in Africa remains underdeveloped due to limited access, distribution challenges, and low awareness. Use of APP-I is gradually increasing where irrigation networks and commercial farming exist. Fire retardant applications are minimal due to weak regulatory frameworks. Long-term growth depends on international collaboration, knowledge transfer, and policy support.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Innophos Inc.

- Parchem

- Noah Chemicals

- CJ Chemicals

- CREMER ERZKONTOR

- ChemCeed

- SAE Manufacturing Specialties Corp

- Barentz

Competitive Analysis:

The Global Ammonium Polyphosphate Market features moderate to high competition, with key players focusing on product innovation, capacity expansion, and strategic partnerships to strengthen their market presence. Major companies include Clariant, Nutrien Ltd., JLS Chemical, Sichuan Chuanhong Phosphorus Chemical, and Innophos Holdings. These firms compete based on product purity, flame-retardant performance, solubility grades, and cost efficiency. It remains a technology-driven market, where advanced manufacturing processes and compliance with environmental standards give companies a competitive edge. Regional players, particularly in Asia Pacific, are expanding their production to meet rising domestic and export demand. Multinational firms are targeting agricultural and industrial customers through distributor networks and customized product offerings. The competitive landscape continues to evolve, shaped by regulatory shifts, supply chain stability, and raw material availability. It offers growth opportunities for both established companies and new entrants capable of delivering specialized formulations and maintaining consistent quality.

Recent Developments:

- In July 2025, Innophos Inc. launched VersaCal, a clean-label whitening alternative to titanium dioxide, marking a significant innovation in specialty phosphates with potential applications in food and other industries.

- In April 2025, Clariantcelebrated 50 years of its Exolit™ AP flame retardants, highlighting the company’s ongoing leadership in sustainable ammonium polyphosphate (APP) solutions. While the announcement primarily marked a milestone, it also underscored Clariant’s commitment to innovation in encapsulated APP technology, which remains central to new product development and market expansion in flame retardants and related applications

- In February 2025, CREMER ERZKONTOR entered a strategic partnership with The Alumina Industrial Company LLC (TAC) in the United Arab Emirates, securing a long-term exclusive contract to supply high-quality alumina products. This move strengthens CREMER ERZKONTOR’s supply chain and global market presence in processed industrial minerals, supporting key industries worldwide.

Market Concentration & Characteristics:

The Global Ammonium Polyphosphate Market shows moderate concentration, with a mix of multinational corporations and regional manufacturers driving production and distribution. It is characterized by strong vertical integration among leading players who manage raw material sourcing, processing, and distribution. The market relies heavily on consistent quality, technical expertise, and regulatory compliance, especially in flame-retardant and agricultural applications. Entry barriers remain moderate due to complex manufacturing processes and dependency on specific chemical feedstocks. Product differentiation is based on solubility, purity, and formulation type, catering to varied industrial and agricultural needs. It exhibits steady demand cycles, with seasonality impacting fertilizer applications and regulatory cycles influencing industrial demand. Long-term supply contracts and distributor networks play a key role in market competitiveness.

Report Coverage:

The research report offers an in-depth analysis based on type and application. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Demand for APP-based flame retardants will grow in construction, electronics, and automotive sectors due to tightening global fire safety standards.

- Adoption in precision agriculture will rise with increased use of water-soluble fertilizers in drip and sprinkler irrigation systems.

- Manufacturers will invest in advanced formulations, including slow-release and microencapsulated APP products for targeted nutrient delivery.

- Asia Pacific will maintain its lead in both consumption and production, driven by China and India’s industrial and agricultural expansion.

- Regulatory bans on halogenated flame retardants will boost global preference for environmentally safe alternatives like APP.

- Collaborations between chemical producers and agritech companies will support innovation and product customization.

- Market players will face pressure to reduce production costs amid fluctuating raw material prices and energy inputs.

- North America and Europe will remain key consumers due to high safety compliance and demand for non-toxic materials.

- Entry of regional manufacturers in Latin America and Africa will increase competition and improve local supply chains.

- R&D in composite materials and 3D printing will open new application areas for APP-based flame-retardant compounds.