Antithrombotic Drugs Market Overview:

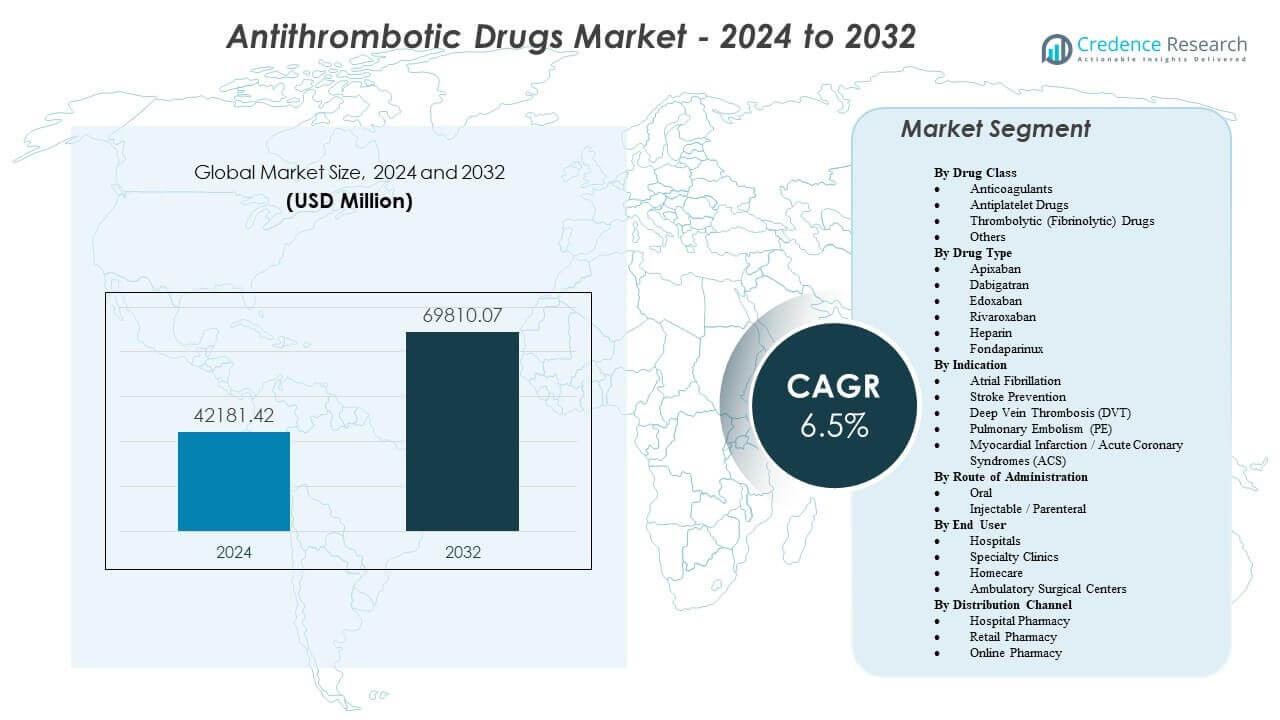

The Antithrombotic Drugs Market is projected to grow from USD 42181.42 million in 2024 to an estimated USD 69810.07 million by 2032, with a compound annual growth rate (CAGR) of 6.5% from 2024 to 2032

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Antithrombotic Drugs Market Size 2024 |

USD 42181.42 million |

| Antithrombotic Drugs Market, CAGR |

6.5% |

| Antithrombotic Drugs Market Size 2032 |

USD 69810.07 million |

Rising cases of atrial fibrillation, venous thromboembolism, and ischemic heart disease continue to expand the treated patient pool. Clinicians increase adoption of direct oral anticoagulants because fixed dosing supports outpatient care and reduces routine monitoring needs. Hospitals also use antithrombotic protocols for orthopedic surgery, cancer-associated thrombosis, and post-intervention prevention. Companies support growth through real-world evidence, safety management tools, and bleed-risk mitigation strategies. Retail and online channels strengthen refill continuity, which improves persistence in long-duration therapy.

North America leads due to high diagnosis rates, strong reimbursement, and early adoption of newer anticoagulants across the United States and Canada. Europe follows with guideline-driven prescribing and broad access across Germany, the UK, France, Italy, and Spain. Asia Pacific is the key emerging region, led by China, Japan, and India, where aging populations and expanding hospital capacity raise treatment rates. Latin America and the Middle East & Africa also advance as awareness improves, cardiology infrastructure expands, and access to generics increases in cost-sensitive markets.

Antithrombotic Drugs Market Insights:

- Rising atrial fibrillation, venous thromboembolism, and ischemic heart disease cases drive sustained demand, supported by wider use of fixed-dose oral anticoagulants in outpatient care.

- Strong hospital protocols for surgery prophylaxis, acute coronary care, and cancer-associated thrombosis continue to expand therapy adoption across high-risk patient groups.

- Bleeding risk concerns, complex dosing in comorbid patients, and uneven reimbursement in cost-sensitive markets restrain faster uptake and limit uniform access to newer agents.

- North America leads due to reimbursement and early adoption, Europe follows with guideline-led prescribing, and Asia Pacific grows fastest as China, Japan, and India expand diagnosis rates and hospital capacity.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Antithrombotic Drugs Market Drivers

Rising Burden Of Atrial Fibrillation And Thromboembolic Disorders Worldwide

Atrial fibrillation prevalence rises with age and metabolic risk factors. Stroke prevention remains a top priority for clinicians and payers. VTE incidence grows due to sedentary lifestyles and complex comorbidities. Cancer care protocols increase anticoagulant use during high-risk periods. Hospital pathways standardize prophylaxis after major surgeries and trauma. Physicians apply risk scoring to identify patients who need therapy sooner. Better imaging and lab access improve clot detection and treatment initiation. Health systems also track readmissions, which supports preventive prescribing.

- For instance, Janssen confirmed XARELTO approval for NVAF stroke risk reduction with a 20 mg once-daily dose, or 15 mg once daily for moderate to severe renal impairment.

Expanding Use Of Direct Oral Anticoagulants In Routine Clinical Practice

DOACs offer predictable dosing and reduce reliance on frequent INR tests. Clinicians prefer simpler regimens when adherence risk remains high. Fewer food and drug interactions support stable real-world outcomes. Hospital discharge planning improves when dosing remains straightforward. Primary care adopts more anticoagulant management within standard workflows. Patients accept therapy when monitoring needs decline and travel reduces. Clinical guidelines support DOAC use across major indications in many regions. Competitor investment in education also improves prescriber confidence over time.

Protocol Driven Antiplatelet Therapy In Coronary And Peripheral Interventions

PCI volumes support continued use of antiplatelet therapy after stent placement. Dual antiplatelet therapy remains central for many ACS care pathways. Peripheral artery disease diagnosis improves and raises treatment adoption. Secondary prevention programs expand within cardiology clinics and networks. Hospitals apply discharge bundles that include antiplatelet adherence support. Pharmacy-led reviews reduce therapy gaps after acute cardiac events. Revascularization procedures create recurring need for tailored antiplatelet plans. Clinicians also refine duration based on bleeding risk and ischemic risk.

Broader Access Through Reimbursement Coverage And Generic Price Competition

Payer coverage improves when evidence supports cost avoidance from stroke and VTE. Generic options increase affordability for long-term therapy in large populations. Tender systems in public hospitals expand access to standard anticoagulants. Retail pharmacy reach supports refill continuity outside major cities. Patient assistance programs reduce drop-off during early months of therapy. Telehealth follow-up supports dose checks and refill planning in remote areas. Care pathways for chronic disease improve adherence and persistence. This access expansion supports sustained prescription growth year after year.

- For instance, Sandoz announced a Germany launch of rivaroxaban film-coated tablets in 10 mg, 15 mg, and 20 mg strengths.

Antithrombotic Drugs Market Trends

Growth Of Real World Evidence And Outcomes Based Contracting In Antithrombotic Care

Payers seek data that reflects everyday patients, not only trial populations. Providers use registries to compare safety outcomes across therapy classes. Health systems track bleed events, stroke rates, and VTE recurrence. Manufacturers sponsor observational studies to support label confidence. Contracts shift toward outcomes where systems share risk with suppliers. Clinical decision tools use local outcomes data to refine therapy selection. Pharmacy analytics identify gaps and prompt interventions for high-risk patients. This trend reshapes evidence needs across product lifecycles and market access.

- For instance, Janssen reported two-year real-world outcomes in frail NVAF patients where rivaroxaban reduced stroke/systemic embolism risk by 32% (HR 0.68) and ischemic stroke by 31% (HR 0.69) versus warfarin.

Patient Focused Adherence Programs And Digital Support For Long Duration Therapy

Chronic therapy needs higher persistence to deliver full preventive benefit. Pharmacies deploy reminders, refill synchronization, and counseling services. Clinics use remote check-ins to address side effects and missed doses. Digital apps support education on bleed signs and drug interactions. Home delivery improves refill reliability for older and mobility-limited patients. Care teams coordinate transitions from hospital to outpatient follow-up. Employers and insurers add adherence incentives for high-risk members. These programs strengthen continuity and reduce avoidable interruptions in care.

Expanded Use Of Reversal Agents And Bleed Management Pathways In Acute Settings

Hospitals build standardized protocols for major bleed events and urgent surgery. Reversal agent availability influences formulary choices in some systems. Emergency departments align anticoagulant plans with imaging and lab workflows. Clinicians train teams to manage bleed risk while preserving clot protection. Multidisciplinary committees review safety signals and update hospital pathways. This focus increases confidence in broader anticoagulant use for complex patients. Quality metrics track bleed outcomes and protocol compliance at scale. The trend supports safer adoption and better risk communication with patients.

- For instance, the PRAXBIND FDA label reports a 5 g idarucizumab dose delivered a median maximum reversal of 100%, with >89% of evaluable patients reaching complete reversal within 4 hours.

Greater Personalization Of Therapy Duration And Intensity Across Patient Segments

Clinicians tailor DAPT duration based on ischemic risk and bleed risk scores. Care teams adjust anticoagulant dose for renal function and frailty profiles. Cancer-associated thrombosis care uses individualized plans across treatment cycles. Post-surgery prophylaxis duration changes by procedure type and mobility level. Guidelines encourage patient-specific choices rather than uniform protocols. Shared decision discussions improve acceptance for long-term preventive therapy. Specialist collaboration supports optimized regimens in complex comorbidity cases. This personalization increases differentiation between brands and care pathways.

Antithrombotic Drugs Market Challenges Analysis

Persistent Bleeding Risk Concerns And Complex Risk Benefit Decisions In Practice

Bleeding remains the primary safety concern across therapy classes. Clinicians face hard choices in elderly patients with multiple comorbidities. Renal impairment and drug interactions complicate dose selection and monitoring. Some patients stop therapy after minor bleeds or fear of complications. Emergency bleed protocols vary across hospitals and resource levels. Under-treatment occurs when providers avoid anticoagulation despite high stroke risk. Over-treatment can occur when therapy duration exceeds patient risk needs. This safety balance limits uniform adoption across settings and regions.

Pricing Pressure, Generic Competition, And Uneven Access Across Health Systems

Generic entry increases price pressure and reduces brand pricing power. Payers tighten prior authorization in cost-sensitive segments. Public systems may limit access to newer agents in lower-income regions. Supply constraints can disrupt continuity in certain markets. Patients face out-of-pocket burden where insurance coverage remains limited. Provider education gaps can reduce appropriate switching and dosing accuracy. Regulatory differences across countries slow harmonized market expansion. These factors create uneven growth across regions and care settings.

Antithrombotic Drugs Market Opportunities

Therapy Expansion In High Risk Populations Through Better Screening And Earlier Intervention

Earlier detection of atrial fibrillation expands the eligible treatment pool. Wearable ECG tools support faster referral and confirmation in primary care. VTE risk assessment tools improve prophylaxis use in hospitals and clinics. Cancer centers adopt structured thrombosis pathways for high-risk regimens. Post-discharge follow-up reduces gaps after surgery and acute cardiac events. Community health programs raise awareness about stroke prevention needs. Pharmacy-led anticoagulation services improve persistence and dose appropriateness. These actions expand volume while improving outcomes in high-risk cohorts.

Innovation In Safer Regimens, Combination Strategies, And Evidence For New Indications

Companies can develop regimens that lower bleed risk without losing efficacy. New trials can support use in complex groups such as frail elderly patients. Combination strategies may target PAD and high-risk cardiovascular populations. Better reversal options can increase clinician confidence in broader prescribing. Long-acting formulations could reduce missed doses and improve persistence. Regional partnerships can expand access and local manufacturing capacity. Health economics evidence can strengthen reimbursement in emerging markets. These opportunities support product differentiation and long-term market value.

Antithrombotic Drugs Market Segmentation Analysis:

By Drug Class

Anticoagulants lead due to broad use in atrial fibrillation and VTE prevention, supported by long-term therapy needs. Antiplatelet drugs sustain demand in coronary disease care, especially after stent procedures and secondary prevention. Thrombolytic (fibrinolytic) drugs hold a smaller share because hospitals reserve them for acute events under strict protocols. Others include niche agents and supportive therapies that serve specific risk profiles and clinical settings.

By Drug Type

Apixaban and rivaroxaban drive strong uptake due to convenient oral dosing and wide guideline support across key indications. Dabigatran and edoxaban serve targeted patient groups based on physician preference and patient risk profiles. Heparin remains essential in inpatient care, perioperative prophylaxis, and acute settings where rapid onset matters. Fondaparinux supports selective use where clinicians want predictable anticoagulation and specific safety considerations. Others cover legacy drugs and new entrants that compete on access, dosing, and safety.

- For example, Edoxaban shows a major bleeding advantage versus warfarin, with HR 80 (p<0.001) reported in ENGAGE AF-TIMI 48 in the FDA label.

By Indication

Atrial fibrillation and stroke prevention form the core demand base due to long-duration use and aging populations. Deep vein thrombosis and pulmonary embolism support strong acute-to-chronic therapy pathways with structured follow-up. Myocardial infarction and acute coronary syndromes rely on protocol-led regimens that often combine antiplatelet therapy with anticoagulation when needed. Others include post-surgical prophylaxis, cancer-associated thrombosis, and high-risk prophylaxis in complex patients.

- For example, Acute ischemic stroke pathways also rely on thrombolysis dosing precision, with alteplase specified at 0.9 mg/kg (max 90 mg) within a defined treatment window in the FDA label.

By Route of Administration

Oral therapies expand fastest because fixed dosing supports outpatient care and better persistence. Injectable or parenteral drugs remain vital in hospitals, perioperative care, and acute thrombosis management. Others include short-term or procedure-based delivery routes that serve limited clinical use cases.

By End User

Hospitals dominate due to acute event management, surgery volume, and complex patient monitoring needs. Specialty clinics support sustained therapy management for cardiac and vascular patients and improve adherence through follow-up. Homecare grows where chronic patients prefer convenient access and remote monitoring. Ambulatory surgical centers use standardized prophylaxis pathways for elective procedures. Others include long-term care settings and emergency networks.

By Distribution Channel

Hospital pharmacy leads due to inpatient initiation and protocol-based dispensing. Retail pharmacy supports chronic refills and adherence services for long-term prevention therapy. Online pharmacy grows with home delivery, refill automation, and better access in urban markets. Others include institutional supply channels and tender-based procurement routes.

Segmentation:

By Drug Class

- Anticoagulants

- Antiplatelet Drugs

- Thrombolytic (Fibrinolytic) Drugs

- Others

By Drug Type

- Apixaban

- Dabigatran

- Edoxaban

- Rivaroxaban

- Heparin

- Fondaparinux

- Others

By Indication

- Atrial Fibrillation

- Stroke Prevention

- Deep Vein Thrombosis (DVT)

- Pulmonary Embolism (PE)

- Myocardial Infarction / Acute Coronary Syndromes (ACS)

- Others

By Route of Administration

- Oral

- Injectable / Parenteral

- Others

By End User

- Hospitals

- Specialty Clinics

- Homecare

- Ambulatory Surgical Centers

- Others

By Distribution Channel

- Hospital Pharmacy

- Retail Pharmacy

- Online Pharmacy

- Others

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America leads the Antithrombotic Drugs Market with 39% share, supported by high diagnosis rates and strong reimbursement in the U.S. and Canada. Europe holds 23% share, driven by guideline-led use and broad access across Germany, France, the UK, and other EU markets. Providers in both regions favor DOAC adoption where monitoring burdens must stay low and outpatient care expands. Hospitals also sustain demand for parenteral anticoagulants during acute episodes and peri-procedure care.Large branded portfolios and strong hospital procurement systems keep therapy use stable across care settings.

Asia Pacific accounts for 25% share and shows strong momentum due to large patient pools in China, India, and Japan. Urban hospital expansion and wider insurance coverage increase access to modern anticoagulants and antiplatelets. Japan supports DOAC use through national guidance and mature cardiology pathways, which lifts volumes. China and India benefit from scale, improving diagnosis, and stronger distribution networks. Local manufacturing and generics improve affordability, which helps long-term adherence in cost-sensitive groups.

Latin America holds 5% share, led by Brazil and Mexico where awareness and hospital access continue to improve. Middle East & Africa holds 8% share, with growth tied to infrastructure upgrades in GCC markets and South Africa. Public procurement programs and cardiac care investments increase use in tertiary hospitals. Access gaps and uneven reimbursement still limit the shift to newer agents in several countries.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Bristol-Myers Squibb Company

- AstraZeneca plc

- Eli Lilly and Company

- Aspen Holdings

- Boehringer Ingelheim International GmbH

- Pfizer Inc.

- Sanofi S.A.

- Bayer AG

- Novartis AG

- Johnson & Johnson

- F. Hoffmann-La Roche Ltd.

- Daiichi Sankyo Company, Limited

- GlaxoSmithKline plc

- Merck & Co., Inc.

Competitive Analysis:

The Antithrombotic Drugs Market shows intense competition across anticoagulants, antiplatelets, and thrombolytics, with strong brand loyalty in chronic indications. Large firms defend share through deep clinical evidence, broad labels, and payer access strategies. Key portfolios center on DOACs and established antiplatelet brands that physicians trust for long-term prevention. Several players also compete in hospital channels where heparins and acute-care protocols drive volume. Product differentiation depends on safety reputation, dosing simplicity, and real-world outcomes that support formulary wins. Companies invest in life-cycle actions such as new dosage forms, patient support services, and expanded indications. Competitive pressure rises from generic erosion in legacy classes, which shifts value toward differentiated brands and newer mechanisms. Partnerships and selective acquisitions strengthen pipelines in next-generation targets and reversal options. Market concentration stays meaningful, since a limited group of multinationals controls many top-selling therapies

Recent Developments:

- In February 2025, Novartis agreed to acquire Anthos Therapeutics for $925 million upfront (up to $3.1 billion total) to advance abelacimab, a Factor XI inhibitor for stroke prevention in atrial fibrillation and cancer-associated thrombosis.

- In August 2025, Sandoz launched generic rivaroxaban (Rivaroxaban – 1 A Pharma) in new strengths of 10 mg, 15 mg, and 20 mg in Germany expanding access to affordable high-quality antithrombotic treatment options for patients.

Report Coverage:

The research report offers an in-depth analysis based on Drug Class, Drug Type, Indication, Route of Administration, End User, Distribution Channel, and region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Expanding diagnosis of atrial fibrillation and VTE will raise long-term prescription volume across care settings.

- Wider DOAC adoption will support outpatient therapy and simplify follow-up for clinicians and patients.

- Hospitals will keep strong demand for parenteral anticoagulants in acute care, surgery pathways, and complex cases.

- Personalized therapy duration and dose selection will strengthen outcomes and reduce avoidable bleeding events.

- Reversal protocols and bleed-management pathways will improve confidence for use in high-risk patients.

- Real-world evidence will shape formulary access, guideline refinement, and payer negotiations for therapy value.

- Adherence programs, home delivery, and digital reminders will reduce therapy gaps in chronic prevention regimens.

- Generic pressure will reshape pricing, while brands compete through safety profiles, labels, and service support.

- Emerging markets will gain scale as access expands through hospital build-out and broader pharmacy reach.

- Pipeline progress will focus on safer regimens, better combinations, and clearer use in complex comorbidity groups.