Arteriotomy Closure Devices Market Overview:

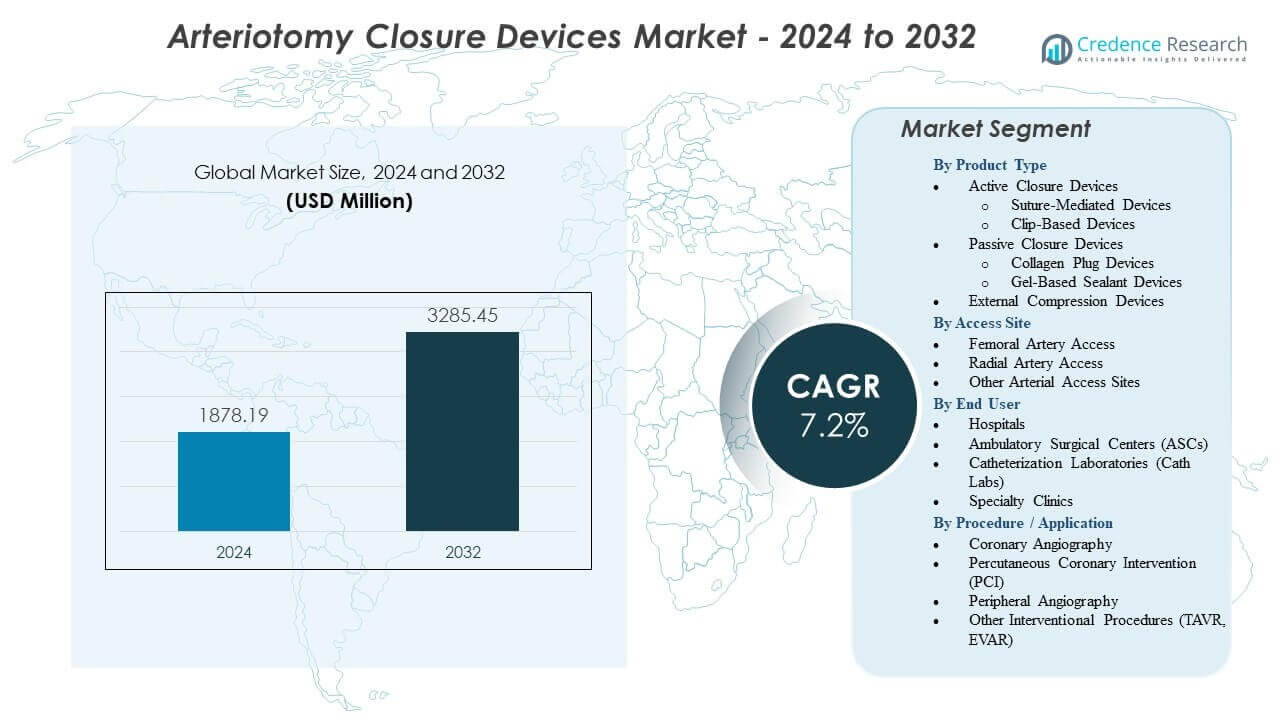

The Arteriotomy Closure Devices Market is projected to grow from USD 1878.19 million in 2024 to an estimated USD 3285.45 million by 2032, with a compound annual growth rate (CAGR) of 7.2% from 2024 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Arteriotomy Closure Devices Market Size 2024 |

USD 1878.19 million |

| Arteriotomy Closure Devices Market, CAGR |

7.2% |

| Arteriotomy Closure Devices Market Size 2032 |

USD 3285.45 million |

Market drivers include a rising preference for fast hemostasis and reduced dependency on manual compression. Clinicians adopt closure technologies that support quicker ambulation and shorter recovery room use. Increasing procedure volumes in angiography, PCI, electrophysiology and structural heart care expand the need for dependable closure systems. Advancements in suture-based, plug-based and bioresorbable platforms enhance clinical performance across varied patient profiles. Hospitals value solutions that ease staff workload and improve patient throughput. Broader training programs support greater operator confidence. These factors create strong momentum for innovation across the Arteriotomy Closure Devices Market.

North America leads due to strong interventional infrastructure and high adoption of minimally invasive cardiovascular procedures. Europe follows with structured care pathways that emphasize predictable recovery and access-site safety. Asia Pacific emerges rapidly as healthcare systems expand catheterization labs and improve access to modern vascular technologies. Growing procedure volumes in China and India strengthen long-term demand. Latin America shows steady progress supported by rising investment in cardiology services. The Middle East and Africa continue to develop capability for higher-acuity interventions. These regional dynamics shape broad global growth for the market.

Arteriotomy Closure Devices Market Insights:

- The Arteriotomy Closure Devices Market is projected to grow from USD 1878.19 million in 2024 to USD 3285.45 million by 2032, reflecting a 7.2% CAGR during the forecast period.

- Growth is driven by rising demand for rapid hemostasis, early ambulation, and efficient workflow support across high-volume interventional cardiology and vascular centers.

- Market restraints include variability in operator skill, high device costs for smaller facilities, and limited access to advanced closure technologies in developing regions.

- North America leads due to strong clinical adoption and advanced cardiac care infrastructure, while Europe maintains traction with standardized care pathways.

- Asia Pacific is expanding quickly as procedure volumes rise and catheterization capabilities strengthen across emerging countries.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Arteriotomy Closure Devices Market Drivers

Growing Demand for Rapid Hemostasis and Early Ambulation

The Arteriotomy Closure Devices Market grows due to the rising need for faster hemostasis across high-volume cardiac centers. Hospitals push for reduced manual compression to improve workflow and patient comfort. Clinicians prefer devices that support mobility within a short window after procedures. Early ambulation cuts the burden on nursing teams and improves bed turnover. The shift toward outpatient models increases the pressure to use efficient closure tools. Providers value predictable outcomes that lower the risk of access-site complications. New technologies improve hemostasis reliability during routine and complex cases. It strengthens adoption in interventional labs.

- For instance, Teleflex confirms that the MANTA large-bore device achieves full hemostasis in about 1 minute for 10–18 Fr access sites.

Expansion of Minimally Invasive Vascular and Cardiology Procedures

A global surge in minimally invasive procedures strengthens the Arteriotomy Closure Devices Market. More centers perform radial and femoral access interventions for diagnosis and therapy. Growth in structural heart procedures widens the pool of patients needing safe closure. Clinicians rely on closure tools to shorten procedure wraps and reduce patient monitoring time. New device options support varied access sizes and clinical needs. Hospitals invest in training that improves device handling and outcomes. High prevalence of cardiovascular disease raises procedure volumes each year. It pushes demand for faster and safer closure techniques.

Shift Toward Standardized Protocols and Enhanced Clinical Efficiency

Hospitals adopt strict access-site management protocols that increase usage of closure systems. Facilities aim to cut workflow variability and maintain predictable recovery timelines. Device makers offer tools that integrate well with these structured care pathways. Clinicians value reduced dependency on manual compression during peak workloads. Broader use of standardized techniques helps reduce complication rates across centers. Teams depend on closure solutions that shorten recovery room duration. Rising patient expectations for comfort and speed shapes purchasing decisions. It supports the steady momentum of the Arteriotomy Closure Devices Market.

- For instance, Perclose ProStyle’s IFU demonstrates >95% technical success in diverse anatomic conditions, supporting consistent outcomes in standardized programs.

Advancements in Automated, Suture-Based, and Plug-Based Closure Designs

Improved closure technologies enhance adoption and procedure confidence. Newer systems provide secure sealing across different anatomical conditions. Automation reduces operator fatigue and improves accuracy during peak procedure hours. Hospitals choose devices that support clean deployment and reliable tissue capture. Suture-based and plug-based platforms give clinicians more flexibility in challenging access conditions. Integration of ergonomic tools reduces technical errors. Vendors refine materials to improve bio-compatibility and post-procedural stability. It strengthens trust in advanced device portfolios.

Arteriotomy Closure Devices Market Trends

Growing Preference for Same-Day Discharge Pathways in Vascular Care

The Arteriotomy Closure Devices Market benefits from growing demand for same-day discharge programs. Hospitals shift toward efficient care pathways that remove unnecessary overnight stays. Closure devices support this model by reducing monitoring needs. Teams value predictable closure outcomes that cut waiting times in recovery bays. A larger share of elective interventions moves toward short-stay formats. Clinicians favor tools that improve patient comfort during rapid discharge cycles. Surgical centers refine workflow steps to streamline throughput. It aligns well with evolving patient expectations for quick recovery.

- For instance, Abbott’s Perclose ProStyle supports pre-close techniques that reduce post-procedure recovery time by over 40% in high-volume PCI centers.

Integration of Imaging and Access-Site Assessment Tools

Imaging-guided workflows influence new trends across the Arteriotomy Closure Devices Market. Centers use ultrasound and fluoroscopic assessment to improve deployment accuracy. The trend enhances safety during closure in high-risk patients. Clinicians track vessel condition before and after intervention to support cleaner outcomes. Vendors explore integration features that support decision-making during closure. Imaging data helps identify ideal positioning for closure components. Adoption grows in training programs to improve precision among new operators. It upgrades procedural confidence in tight operational windows.

Rising Interest in Biodegradable, Low-Profile, and Eco-Conscious Materials

Sustainability and material innovation shape new trends within the Arteriotomy Closure Devices Market. Vendors design low-profile components that reduce patient discomfort. Interest rises in biodegradable materials that dissolve after vessel healing. Hospitals seek products that create fewer waste issues during high-volume use. Material science improves reliability without raising procedural complexity. Patients value solutions that reduce long-term foreign-body presence. The industry tracks environmental impact across production stages. It encourages steady innovation across device portfolios.

Growing Training Ecosystem Supporting Skilled Deployment and Better Outcomes

Training programs expand to strengthen adoption across the Arteriotomy Closure Devices Market. Medical centers develop in-house modules to enhance operator skill. Vendors invest in simulation platforms for consistent practice. Structured learning reduces variability in closure outcomes among teams. Training improves confidence during complex or emergency procedures. Hospitals create competency criteria that guide purchasing decisions. Clinicians support peer-to-peer workshops for continuous improvement. It helps raise overall success rates across diverse settings.

- For instance, Haemonetics partners with electrophysiology labs offering hands-on VASCADE MVP workshops that demonstrate reductions of post-procedure hold time by up to 45%

Market Challenges Analysis

Technical Limitations and Deployment Errors Across Complex Anatomies

The Arteriotomy Closure Devices Market faces challenges linked to anatomical variation and technical difficulty. Some devices struggle in heavily calcified or tortuous vessels. Inconsistent deployment increases the risk of bleeding events. Clinicians face learning curves that slow early adoption in new centers. Device failure raises complication management costs for hospitals. Teams depend on precise placement, which remains difficult during emergency settings. Limited compatibility with large-bore access points restricts use in advanced structural procedures. It creates pressure on vendors to improve device reliability.

Cost Pressures, Limited Access in Developing Regions, and Regulatory Demands

Hospitals in developing regions struggle with budget constraints that slow adoption. Closure devices cost more than manual compression, which limits uptake in small facilities. Access barriers widen gaps in procedural quality across global markets. Regulatory pathways add time to device launches and increase compliance costs. Reimbursement uncertainty influences purchasing decisions in competitive healthcare systems. Hospitals evaluate cost-benefit ratios closely before introducing new tools. Maintenance and training requirements raise operational burdens on teams. It challenges the growth trajectory of the Arteriotomy Closure Devices Market.

Arteriotomy Closure Devices Market Opportunities

Expansion of Large-Bore and Structural Heart Procedures Creating New Demand Pools

The Arteriotomy Closure Devices Market gains new opportunities from rising structural heart and endovascular procedures. Growth in large-bore access interventions generates demand for stronger closure platforms. Hospitals need tools that reduce complications during these complex procedures. Vendors can develop targeted solutions for EVAR, TAVR, and advanced interventions. Clinicians support adoption of devices that reduce procedure wrap-up time. Next-generation systems can address unmet needs in multi-site access scenarios. Training programs create pathways for wider acceptance across centers. It opens long-term potential for specialized device lines.

Adoption of Digital Workflow Support, Data Feedback, and Smart Deployment Platforms

Digital guidance platforms create new opportunities across the Arteriotomy Closure Devices Market. Workflow tools help clinicians track deployment quality in real time. Data logs support performance audits and training improvement. Smart feedback systems can reduce operator error during critical steps. Hospitals value digital integration that aligns with broader surgical information systems. Predictive tools may optimize device choice for each patient profile. Vendors can use digital data to refine product upgrades. It improves clinical decision-making and encourages advanced technology adoption.

Arteriotomy Closure Devices Market Segmentation Analysis:

By Product Type

The Arteriotomy Closure Devices Market shows strong uptake of active closure devices due to their efficiency in reducing hemostasis time. Suture-mediated systems support reliable closure during high-volume procedures. Clip-based devices offer consistent outcomes in varied vessel conditions. Passive closure products hold steady demand in routine cases. Collagen plug devices attract users who prefer natural biomaterial sealing. Gel-based sealants gain traction in centers seeking quick deployment. External compression devices retain relevance in facilities with budget limits. It supports a wide product mix across regions.

- For instance, Terumo’s Angio-Seal achieves hemostasis in about 60 seconds with its bioabsorbable anchor-and-collagen design.

By Access Site

The Arteriotomy Closure Devices Market experiences higher adoption in femoral artery access due to the large share of complex cardiovascular procedures. Femoral access sites need dependable closure tools to reduce bleeding risks and improve recovery. Radial artery access grows quickly with expanding minimally invasive practices. Radial procedures need lower-profile devices that support fast mobilization. Other arterial access sites create demand for adaptable technologies. Hospitals rely on targeted tools for varied anatomical needs. It drives device development toward flexible access compatibility.

- For instance, Haemonetics’ Vascade LBL closes 12–21 Fr femoral access sites and reduces ambulation time compared with compression.

By End User

Hospitals dominate the Arteriotomy Closure Devices Market due to high procedure volumes and broad clinical capabilities. Large centers prefer closure systems that reduce workload and standardize outcomes. Ambulatory Surgical Centers use devices that support quick turnover and shorter stays. Cath Labs rely on dependable tools that reduce monitoring needs. Specialty clinics integrate closure products to streamline interventional workflows. Each end user group values predictable performance. It shapes diverse purchasing patterns across healthcare systems.

By Procedure / Application

Coronary angiography drives consistent demand within the Arteriotomy Closure Devices Market. PCI procedures increase reliance on advanced closure tools to reduce complications. Peripheral angiography expands adoption in vascular care settings. Other interventional procedures such as TAVR and EVAR need devices that secure large-bore access sites. Procedure growth increases pressure on teams to adopt efficient solutions. Clinicians choose devices that support shorter recovery windows. It strengthens the link between procedure expansion and product demand.

Segmentation:

By Product Type

- Active Closure Devices

- Suture-Mediated Devices

- Clip-Based Devices

- Passive Closure Devices

- Collagen Plug Devices

- Gel-Based Sealant Devices

- External Compression Devices

By Access Site

- Femoral Artery Access

- Radial Artery Access

- Other Arterial Access Sites

By End User

- Hospitals

- Ambulatory Surgical Centers (ASCs)

- Catheterization Laboratories (Cath Labs)

- Specialty Clinics

By Procedure / Application

- Coronary Angiography

- Percutaneous Coronary Intervention (PCI)

- Peripheral Angiography

- Other Interventional Procedures (TAVR, EVAR)

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America leads the Arteriotomy Closure Devices Market with an estimated 38% share, supported by strong interventional cardiology volumes and advanced clinical infrastructure. Hospitals in the United States adopt closure technologies that reduce workflow pressure and improve recovery timelines. Vendors launch new devices first in this region due to faster regulatory pathways. Training programs help improve procedural success across high-volume centers. Demand stays stable due to high rates of coronary artery disease. It remains the most mature regional market with a consistent technology upgrade cycle.

Europe follows with nearly 28% share, driven by widespread preference for minimally invasive cardiac and vascular procedures. Hospitals implement structured access-site management protocols that increase adoption of closure tools. Growth remains steady due to strong reimbursement support in leading countries. Clinicians favor devices that reduce post-procedure monitoring time. Regional guidelines encourage the use of closure systems to improve safety during elective and emergency care. It maintains strong demand due to continuous investment in cardiovascular services.

Asia Pacific holds about 22% share and shows the fastest expansion driven by rising cardiovascular disease prevalence. Countries increase investments in catheterization labs to meet growing patient loads. Hospitals adopt closure devices to shorten recovery and reduce bed occupancy. Emerging economies improve access to advanced vascular care, which strengthens long-term demand. Local manufacturing support reduces costs and improves product availability. It expands rapidly as clinical practices shift toward modern interventional workflows. Latin America and the Middle East & Africa together account for the remaining 12%, driven by growing hospital upgrades and rising procedure volumes.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Abbott Vascular

- Terumo Corporation

- Cardinal Health

- Medtronic

- Merit Medical Systems

- Teleflex Incorporated

- Cardiva Medical

- Vasorum Ltd.

- Morris Innovative

- Vivasure Medical

Competitive Analysis:

The Arteriotomy Closure Devices Market features strong competition among global and regional manufacturers that focus on product performance, reliability, and ease of use. Leaders such as Abbott Vascular, Terumo Corporation, Medtronic, and Teleflex maintain an advantage due to broad portfolios and established clinical trust. Firms invest in design improvements that reduce deployment errors and shorten hemostasis time. Competition increases in passive closure and compression devices where price sensitivity remains high. Smaller companies introduce niche innovations targeting large-bore access and complex anatomies. Distributors strengthen market reach through training programs and technical support. It encourages companies to refine materials, expand indication approvals, and secure long-term contracts with hospitals and ASC networks.

Recent Developments:

- In May 2025, Merit Medical Systems acquired Biolife Delaware for approximately $120 million, adding haemostatic devices like StatSeal and WoundSeal that support vascular closure applications in percutaneous procedures.

- In February 2025, Teleflex announced the acquisition of BIOTRONIK’s Vascular Intervention business for €760 million (completed June 30, 2025), incorporating vascular closure-related access products alongside stents and balloons for coronary and peripheral interventions.

- In August 2024, Haemonetics launched the Vascade MVP XL vascular closure system, which includes a resorbable collagen patch, collapsible disc technology, and proprietary features to support quick hemostasis in surgeries such as left atrial appendage closure and pulsed field ablation requiring 10-12 Fr sheaths.

- In June 2024, Haemonetics Corp expanded its VASCADE product line by introducing the VASCADE MVP XL mid-bore venous closure device, designed for larger sheaths (10-12F, up to 15F outer diameter) used in procedures like cryoablation, featuring 58% more collagen and a bigger collapsible disc for rapid hemostasis.

Report Coverage:

The research report offers an in-depth analysis based on Product Type, Access Site, End User, Procedure / Application, and Regions. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Growing procedure volumes in interventional cardiology strengthen the long-term demand outlook.

- Adoption of advanced closure technologies improves clinical efficiency and expands usage across high-volume centers.

- Rising preference for outpatient vascular procedures increases the need for reliable hemostasis solutions.

- Wider deployment of suture-based and clip-based devices enhances confidence in complex anatomical conditions.

- Expanding training programs elevate operator skills and improve consistency in procedural outcomes.

- New biodegradable materials support innovation and increase acceptance among clinicians seeking patient comfort.

- Integration of workflow support tools encourages digital transformation across catheterization labs.

- Growing adoption in developing regions broadens the global footprint of key suppliers.

- Product development targeting large-bore access strengthens opportunities in structural heart procedures.

- Increased focus on reducing recovery time supports stronger alignment with modern care models.