Artificial Disc Market Overview:

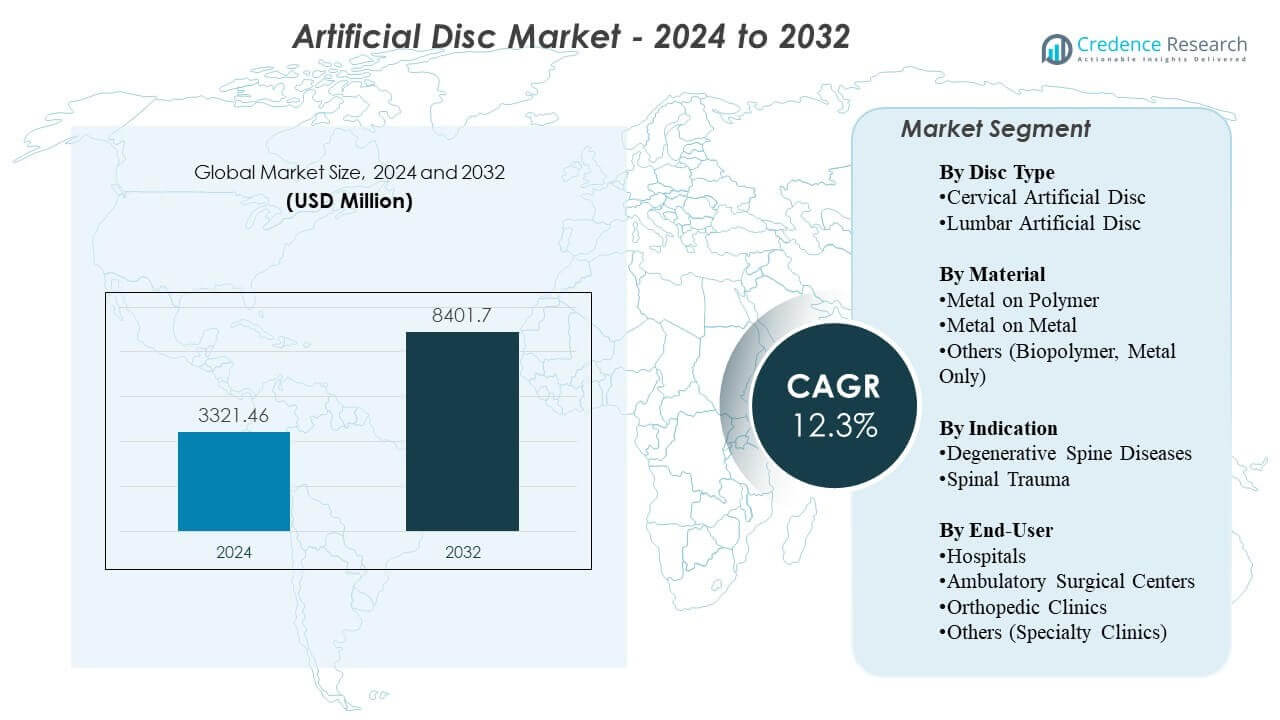

The Artificial Disc Market is projected to grow from USD 3321.46 million in 2024 to an estimated USD 8401.7 million by 2032, with a compound annual growth rate (CAGR) of 12.3% from 2024 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Artificial Disc Market Size 2024 |

USD 3321.46 million |

| Artificial Disc Market, CAGR |

12.3% |

| Artificial Disc Market Size 2032 |

USD 8401.7 million |

Market drivers include the rising prevalence of degenerative disc disease, driven by aging populations, sedentary habits, and increased ergonomic stress in younger workers. Surgeons adopt artificial disc replacement to maintain natural mobility and reduce adjacent segment degeneration, improving long-term outcomes. Hospitals invest in advanced imaging, robotics, and navigation systems to support higher surgical precision. New implant materials improve durability and reduce wear, while multi-level indications create new treatment opportunities. Patient preference for faster recovery and lower complication risk further enhances market uptake.

North America leads the Artificial Disc Market due to high procedural volumes, strong clinical adoption, and widespread availability of advanced spine care. Europe follows with structured spine programs and a high concentration of skilled surgeons supporting consistent procedure growth. Asia Pacific emerges as the fastest-expanding region, driven by growing healthcare investment, rising awareness, and improved access to specialized surgical centers. Latin America and the Middle East show gradual adoption as infrastructure improves and training programs expand. This geographic spread supports steady global market momentum.

Artificial Disc Market Insights:

- The Artificial Disc Market is valued at USD 3321.46 million in 2024 and is projected to reach USD 8401.7 million by 2032, growing at a CAGR of 12.3%.

- Rising cases of degenerative disc disease, increased ergonomic strain, and stronger demand for motion-preserving procedures are driving market expansion.

- Limited reimbursement in some regions, high implant costs, and the need for specialized surgical expertise continue to restrain broader adoption.

- North America leads due to advanced spine care systems, while Europe maintains strong uptake supported by skilled surgeons and structured clinical pathways.

- Asia Pacific shows the fastest growth as investments in healthcare infrastructure rise and awareness of motion-preserving spine solutions increases.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Artificial Disc Market Drivers

Growing Demand for Motion-Preserving Spine Procedures

Growing demand for motion-preserving spine procedures strengthens the adoption of next-generation implants in the Artificial Disc Market. Surgeons prefer disc replacement because the technique maintains natural spine movement and reduces adjacent segment degeneration. Rising awareness among patients increases procedure acceptance across major healthcare systems. Strong technical advances in implant kinematics build confidence among clinical specialists. Many hospitals expand spine programs to support higher procedure volumes. Product upgrades with improved materials support better long-term outcomes. Regulatory approvals for multi-level replacements expand the eligible patient pool. Market players focus on wider availability through training programs.

Rising Incidence of Degenerative Disc Disease and Lifestyle-Linked Disorders

Rising incidence of degenerative disc disease drives steady growth across global markets. Sedentary routines, reduced physical activity, and ergonomic strain contribute to early disc deterioration in younger adults. Surgeons see more cases that require motion-preserving solutions rather than fusion. Many patients seek quicker recovery and lower complication risk. Market growth benefits from rising clinical evidence supporting durable outcomes. Hospitals upgrade surgical suites to support advanced spinal implants. New devices improve biomechanical performance and reduce revision rates. The shift toward outpatient procedures increases treatment accessibility.

Rapid Technological Advancements in Biomaterials and Disc Design

Rapid innovation in biomaterials leads to stronger clinical adoption across surgical centers. Manufacturers introduce viscoelastic materials that mimic natural disc function. Many systems feature optimized endplate coatings that improve osseointegration. New designs enable improved flexibility and natural motion during daily activity. Robotics and navigation systems enhance surgical precision and reduce operative risks. Clinical studies highlight improved pain relief and functional recovery in implant recipients. Hospitals evaluate new systems to reduce long-term complications. This steady upgrade cycle supports strong demand.

- For instance, titanium plasma-spray coatings used in the prodisc portfolio improve fixation strength by up to 40% in mechanical evaluations.

Expanding Reimbursement Coverage and Improved Clinical Guidelines

Expanding reimbursement coverage supports higher adoption among eligible patients. Updated clinical guidelines encourage motion-preserving interventions where possible. Insurers approve more indications based on stronger long-term data. Hospitals expand training workshops to support surgeon proficiency. Many regions invest in specialized spine centers to improve access. Coverage expansion reduces financial burden for patients. Manufacturers work closely with regulatory bodies to maintain compliance. This environment strengthens growth opportunities across the spine care ecosystem.

- For instance, U.S. insurers expanded coverage for two-level cervical disc replacement after long-term Mobi-C data showed superior outcomes to ACDF, increasing patient access.

Market Trends

Growing Use of Multi-Level Disc Replacement for Complex Degenerative Conditions

Growing acceptance of multi-level disc replacement shapes a strong trend within the Artificial Disc Market. Surgeons select multi-level procedures for patients who need broader mobility restoration. Clinical research supports improved long-term function in multi-level cases. Hospitals develop advanced protocols to manage patient selection. Robotic systems support precise implant alignment across multiple segments. Manufacturers refine disc geometry to support stability in complex cases. Training programs support surgeon adoption across major centers. Multi-level procedures expand the overall market potential.

- For instance, robotic systems such as Globus Medical’s ExcelsiusGPS deliver ≤1.2 mm placement accuracy across multiple segments, improving placement reliability.

Increasing Adoption of Minimally Invasive and Outpatient Spine Procedures

Rising preference for minimally invasive surgery influences product development strategies. Many procedures shift toward outpatient settings due to shorter recovery timelines. Device makers design implants suited for smaller incisions and reduced tissue disruption. Hospitals adopt navigation systems that support reduced complication risk. Patients request procedures with faster return-to-work expectations. Outpatient care models lower treatment cost and expand accessibility. Clinical teams invest in enhanced imaging and intraoperative tools. This shift supports broader adoption across community hospitals.

Advances in 3D Printing and Patient-Specific Implant Engineering

Advances in 3D-printing technology create new possibilities for customized implants. Many manufacturers explore personalized disc designs to match anatomical variations. Customized implants may improve surgical fit and reduce postoperative discomfort. Hospitals evaluate early outcomes to determine patient suitability. Engineers refine lattice structures to support natural load distribution. Surgeons gain more flexibility in planning complex interventions. Imaging advancements improve preoperative measurement accuracy. Personalized systems may create new revenue streams for suppliers.

- For instance, 4WEB Medical reports that its 3D-printed titanium lattice design improves load distribution by up to 40% compared with machined implants.

Stronger Integration of Digital Planning, Simulation, and Data-Driven Surgery

Stronger integration of digital platforms transforms the future direction of the Artificial Disc Market. Preoperative simulation tools allow surgeons to review patient anatomy and plan implant size. Data-driven planning helps reduce intraoperative uncertainty. Robotics improve alignment precision and reduce human error. Hospitals value digital tracking for long-term patient monitoring. Clinical software helps predict postoperative mobility levels. Digital systems support faster learning curves. Vendors invest in AI-based assessment for decision support. Technology convergence drives better outcomes.

Artificial Disc Market Challenges Analysis

High Cost of Disc Replacement Procedures and Limitations in Reimbursement Coverage

High procedure cost remains a major challenge across the Artificial Disc Market, limiting access for many patients. Reimbursement inconsistencies create uncertainty for hospitals and surgeons. Many insurers restrict coverage to single-level procedures. Surgeons face challenges in managing patients who cannot afford the treatment. Some healthcare systems lack standardized payment pathways. High device cost makes adoption difficult in developing regions. Hospitals evaluate cost-benefit factors before expanding disc replacement programs. Market players need stronger economic data to support broader approvals. This environment slows penetration in cost-sensitive markets.

Clinical Complications, Implant Failures, and Limited Long-Term Data in Some Regions

Clinical complications create hesitation among certain surgeons despite strong technology advances. Implant migration, wear issues, and reoperation risk remain concerns. Long-term performance data vary across regions and device categories. Some centers lack skilled surgeons trained for disc replacement. Hospitals need consistent training programs to reduce variability in outcomes. Postoperative imaging requirements increase operational burden. Regulatory approval timelines slow new product introductions. Complex patient anatomy presents challenges during implant placement. These factors limit large-scale adoption in certain markets.

Artificial Disc Market Opportunities

Rising Demand for Advanced Spine Care in Emerging Economies with Growing Surgical Capacity

Rising demand for advanced spine care creates large expansion opportunities across the Artificial Disc Market. Emerging countries invest in modern surgical infrastructure. Hospitals upgrade operating suites to support motion-preserving procedures. Surgeons receive training through international partnerships. Patients seek treatments that help maintain mobility and reduce long-term disability. Wider adoption of insurance coverage expands the eligible patient pool. Manufacturers strengthen distribution channels across high-growth regions. Market expansion accelerates as awareness increases.

Innovation in Biomimetic Disc Technologies and Integration of Digital Surgery Platforms

Innovation in biomimetic materials shapes major growth opportunities across clinical settings. Next-generation discs replicate natural biomechanics more effectively. Hospitals evaluate new devices to reduce revision risk and improve patient satisfaction. Digital surgery platforms enhance accuracy during implantation. AI-based analytics support better decision-making for surgeons. Robotics help standardize procedural quality across institutions. Personalized planning tools drive improved patient-matched outcomes. These advancements help expand market potential in high-demand spine centers.

Artificial Disc Market Segmentation Analysis:

By Disc Type

Cervical artificial discs lead adoption in the Artificial Disc Market because surgeons prefer motion-preserving solutions for patients with neck pain linked to degenerative disorders. Cervical procedures show strong clinical outcomes and shorter recovery timelines. Lumbar artificial discs gain interest where mobility restoration matters for younger and active patients. Many hospitals evaluate newer lumbar systems that improve stability and reduce revision needs. Clinical evidence continues to strengthen confidence in both segments. Product innovation supports wider use across multiple care settings.

By Material

Metal-on-polymer implants remain widely used due to strong wear resistance and proven long-term performance across varied patient groups. Many surgeons select these systems for their reliable articulation and reduced complication rates. Metal-on-metal discs maintain a smaller share because some centers prefer alternatives with lower wear-debris concerns. The others category, including biopolymer and metal-only designs, expands through biomimetic technologies that aim to mimic natural disc movement. Each material group evolves with new designs that improve flexibility and load distribution across the spine.

- For example, Synthes’ Prestige LP system reports less than 0.04 mm/year wear, reinforcing material reliability across diverse patient groups. Metal-on-metal discs hold a smaller share because many centers monitor metal-ion release, despite designs like Medtronic’s Prestige ST demonstrating over 90% success rates in long-term follow-ups.

By Indication

Degenerative spine diseases account for the highest procedure volume, driven by rising cases linked to aging populations and sedentary lifestyles. Surgeons recommend disc replacement in cases where mobility preservation supports quality of life. Spinal trauma represents a smaller but important segment where artificial discs help restore functionality in suitable candidates. Many trauma centers consider disc replacement when anatomical alignment and stability allow safe implantation. Broader awareness improves adoption across both indications.

- For example, Mobi-C clinical data show 85–90% patient-reported functional improvement, making it a preferred option for symptomatic cervical degeneration.

By End-User

Hospitals remain the primary treatment centers because they offer advanced imaging, skilled surgical teams, and comprehensive postoperative care. Ambulatory surgical centers gain share due to shorter stays and reduced procedure costs. Orthopedic clinics strengthen demand through increased patient referrals and specialized spine programs. The others segment, including specialty clinics, expands where surgeons adopt modern implants and outpatient workflows. Each end-user category contributes to the broader growth of the market by supporting diverse patient pathways.

Segmentation:

By Disc Type

- Cervical Artificial Disc

- Lumbar Artificial Disc

By Material

- Metal on Polymer

- Metal on Metal

- Others (Biopolymer, Metal Only)

By Indication

- Degenerative Spine Diseases

- Spinal Trauma

By End-User

- Hospitals

- Ambulatory Surgical Centers

- Orthopedic Clinics

- Others (Specialty Clinics)

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America holds the largest share of the Artificial Disc Market, supported by strong surgical volumes, advanced healthcare infrastructure, and high adoption of motion-preserving technologies. The region accounts for roughly 40–45% of the global share due to early approval pathways and strong reimbursement support. Surgeons in the United States prefer cervical and lumbar disc replacements for suitable candidates, which increases procedure penetration. Hospitals invest in robotics and navigation to improve precision and outcomes. Patient preference for quicker recovery strengthens demand. It continues to benefit from ongoing clinical studies that validate long-term performance.

Europe represents the second-largest regional share, with an estimated 30–32% of the global market. The region benefits from structured spine care pathways, strong surgeon expertise, and broad procedural acceptance across Germany, France, and the UK. Many European centers adopt next-generation biomimetic discs to improve postoperative mobility. Regulatory harmonization supports consistent product availability across key markets. Hospitals focus on reducing revision rates through advanced material technologies. It maintains steady growth through expanding multi-level replacement eligibility.

Asia-Pacific emerges as the fastest-growing region and holds roughly 20–22% of the global share. Growing investments in spine surgery infrastructure in China, India, Japan, and South Korea support wider adoption. Rising awareness of motion-preserving procedures increases interest among younger patient groups. Hospitals upgrade operating platforms to support precise implantation and improved safety outcomes. Regional manufacturers expand product pipelines to meet rising demand. It benefits from improving insurance coverage and expanding private healthcare sectors across major cities.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Medtronic plc

- Zimmer Biomet Holdings Inc.

- DePuy Synthes Inc. (Johnson & Johnson)

- Globus Medical Inc.

- NuVasive Inc.

- Stryker Corporation

- Orthofix Medical Inc.

- Braun Melsungen AG (Aesculap)

- Smith & Nephew Plc

- Centinel Spine LLC

- Alphatec Spine Inc.

- Paradigm Spine LLC

- Spineart SA

Competitive Analysis:

The Artificial Disc Market features strong competition among global orthopedic leaders that invest heavily in product innovation and clinical validation. Medtronic, Zimmer Biomet, DePuy Synthes, Globus Medical, and Stryker maintain leadership positions through broad implant portfolios and global distribution strength. Many companies focus on enhanced biomimetic materials and multi-level replacement systems to differentiate performance. Smaller players such as Centinel Spine, Spineart, and Orthofix expand their presence through targeted launches and surgeon training programs. Competitors invest in digital surgery platforms to improve precision and reduce variability in outcomes. Strategic collaborations with hospitals support wider procedural adoption. It continues to evolve as companies strengthen regulatory approvals and pursue expansion into high-growth regions.

Recent Developments:

- In July 2025, Dymicron was granted FDA IDE approval for the Triadyme-C artificial disc. This approval enables the start of a pivotal U.S. clinical trial comparing the next-generation cervical disc, made with proprietary Adymite polycrystalline diamond material for reduced wear, against ACDF surgery, with first implants planned for Q4 2025.

- In July 14, 2025. Synergy Spine Solutions extended its strategic sales agency collaboration with Johnson & Johnson MedTech into Switzerland, effective April 1, 2025. The partnership builds on prior agreements in the UK and Ireland to broaden access to the Synergy Disc, the only artificial cervical disc with a 6° lordotic core for improved alignment and motion.

- In March 2025, NGMedical received Australian TGA approval for its MOVE-C cervical artificial disc In this regulatory milestone, the company announced the approval for its innovative cervical disc arthroplasty product featuring unique articulating viscoelastic properties, marking a key step in expanding motion-preserving spinal care in Australia.

Report Coverage:

The research report offers an in-depth analysis based on Disc Type, Material, Indication, and End-User. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Growing adoption of motion-preserving procedures will strengthen global demand as patients seek improved mobility and faster rehabilitation outcomes.

- Rising preference for minimally invasive techniques will support broader use of next-generation cervical and lumbar disc systems.

- Biomimetic and viscoelastic implant technologies will gain traction due to their ability to mimic natural disc behavior and reduce long-term complications.

- Digital surgery platforms, including navigation and robotics, will enhance precision and improve surgical consistency across high-volume centers.

- Multi-level disc replacement will expand with stronger clinical evidence supporting sustained functional improvement and reduced adjacent segment stress.

- Emerging markets will accelerate growth with expanding surgical infrastructure and greater access to specialized spine care.

- Outpatient and ambulatory centers will perform more disc procedures due to shorter recovery timelines and reduced overall costs.

- Personalized implants created through advanced imaging and 3D engineering will improve procedural accuracy and patient satisfaction.

- Regulatory approvals for new materials and device designs will facilitate faster market penetration for innovative technologies.

- Strategic partnerships between manufacturers and spine centers will enhance training, product uptake, and long-term clinical adoption.