| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Asia Textile Chemicals Market Size 2024 |

USD 16,706.29 million |

| Asia Textile Chemicals Market, CAGR |

5.34% |

| Asia Textile Chemicals Market Size 2032 |

USD 26,111.36 million |

Market Overview

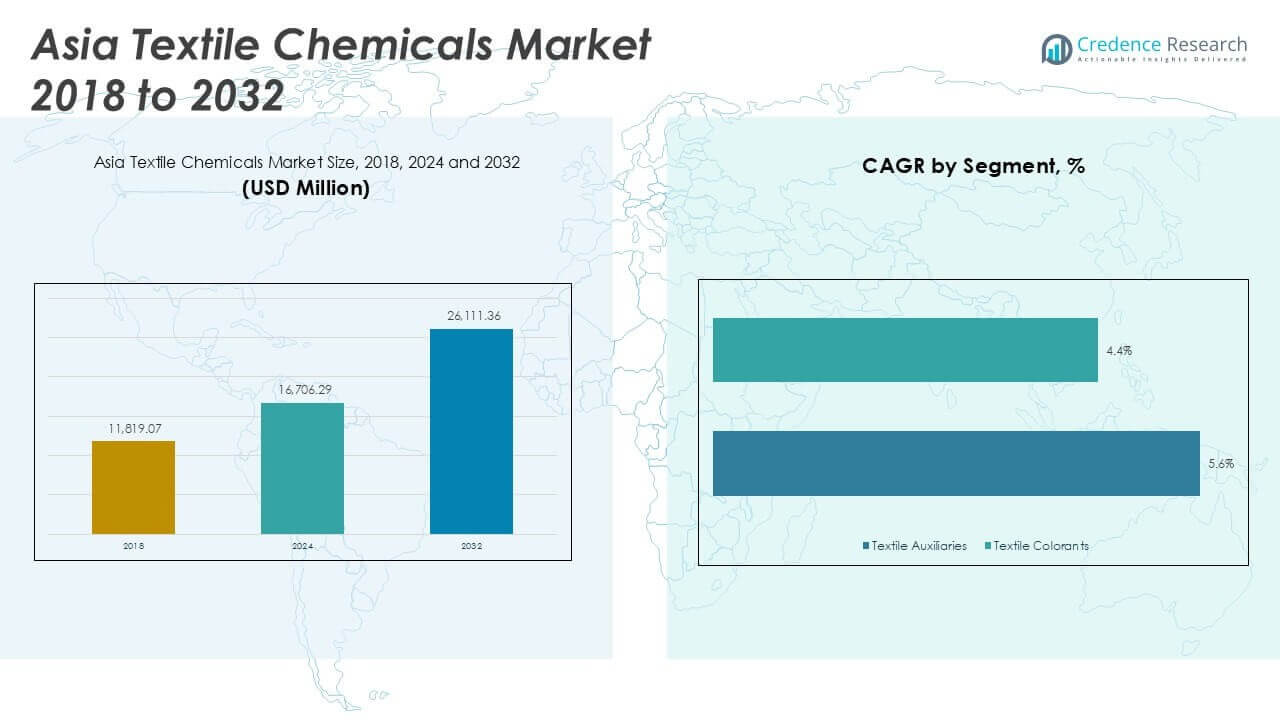

The Asia Textile Chemicals market size was valued at USD 11,819.07 million in 2018, increased to USD 16,706.29 million in 2024, and is anticipated to reach USD 26,111.36 million by 2032, at a CAGR of 5.34% during the forecast period.

The Asia Textile Chemicals market is dominated by key players such as BASF SE, Arvind Ltd, Bombay Dyeing and Manufacturing Company Ltd, Shenzhou International Group, Texhong Textile Group, Weiqiao Textile, Huntsman Corporation, Archroma Management LLC, DyStar Group, and DIC Corporation. These companies maintain competitive strength through diverse product portfolios, technological advancements, and a strong focus on sustainable solutions. China leads the regional market, holding the largest share of 38.5% in 2024, driven by its expansive textile manufacturing base and export dominance. India follows with a 25.7% market share, supported by rising domestic consumption and government initiatives promoting textile industry growth.

Market Insights

- The Asia Textile Chemicals market was valued at USD 16,706.29 million in 2024 and is expected to reach USD 26,111.36 million by 2032, growing at a CAGR of 5.34% during the forecast period.

- The market is driven by the growing textile manufacturing base in countries like China, India, Bangladesh, and Vietnam, along with increasing demand for technical and high-performance textiles across various industries.

- A key trend is the rising adoption of eco-friendly and sustainable textile chemicals, driven by stringent environmental regulations and the growing preference for low-impact dyeing and digital printing technologies.

- The market is highly competitive with major players including BASF SE, Huntsman Corporation, DyStar Group, and Archroma Management LLC focusing on product innovation, sustainability, and regional expansion to maintain market leadership.

- China holds the largest regional share at 38.5%, followed by India at 25.7%, while the dyeing process and textile auxiliaries lead the segment shares across the market.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Product Type

In the Asia Textile Chemicals market, textile auxiliaries dominate the product type segment, accounting for the largest market share in 2024. Textile auxiliaries are widely used across various stages of textile processing, including pre-treatment, dyeing, printing, and finishing, to enhance fabric properties and improve processing efficiency. The growing demand for high-quality, functional textiles with properties such as wrinkle resistance, water repellency, and flame retardancy drives the adoption of textile auxiliaries. Additionally, the rise in production of technical textiles and increasing consumer preferences for premium fabrics further support segment growth.

- For instance, Huntsman Textile Effects developed the PHOBOTEX® R-ACE durable water repellent finishing chemical, which has been applied to over 200 million garments globally without the use of fluorocarbons.

By Process Type

Within the process type segment, the dyeing sub-segment holds the dominant market share in the Asia Textile Chemicals market. The substantial consumption of dyes in both natural and synthetic textile applications fuels this dominance. Increasing fashion consciousness and the rapid expansion of the apparel industry in countries like China and India have significantly boosted the demand for vibrant and diverse fabric colors. Technological advancements in eco-friendly dyeing processes and the push for sustainable production further encourage the adoption of innovative chemicals in this segment, supporting the overall market expansion.

- For instance, Archroma’s AVITERA® SE dyeing technology has reduced water consumption by up to 50 liters per kilogram of fabric dyed and shortened dyeing cycle times by up to 25 minutes per batch, as adopted by several mills across Asia.

By Application

In the application segment, apparels represent the leading sub-segment, commanding the highest market share in 2024. The consistent growth of the fashion and clothing industry, coupled with rising disposable incomes and shifting consumer preferences towards branded and high-quality garments, is a primary driver. The increasing urban population and demand for sportswear, casualwear, and formal attire continue to propel the consumption of textile chemicals in this segment. Additionally, manufacturers are focusing on using advanced chemicals to meet the rising need for durable, comfortable, and performance-enhancing apparel.

Market Overview

Expanding Textile Manufacturing Base

The rapid expansion of textile manufacturing in Asia, particularly in China, India, Bangladesh, and Vietnam, serves as a major growth driver for the textile chemicals market. Increasing demand for textiles from both domestic and international markets, supported by cost-effective labor and favorable government policies, is encouraging production scale-up. This growth fuels the need for textile chemicals used across processes like pre-treatment, dyeing, and finishing, thereby boosting market demand. The region’s position as a global textile hub significantly contributes to sustained market expansion.

- For instance, Shenzhou International Group has scaled its production to over 580 million pieces of knitwear annually, significantly increasing its textile chemical consumption in recent years to support growing orders from global brands like Nike and Adidas.

Rising Demand for Technical Textiles

The growing application of technical textiles in industries such as automotive, healthcare, construction, and sportswear is driving the demand for specialized textile chemicals in Asia. Technical textiles require enhanced performance properties like flame retardancy, water resistance, and antimicrobial effects, which depend heavily on chemical treatments. This shift towards value-added and functional textiles supports the increasing consumption of textile auxiliaries and finishing agents. The focus on producing high-performance textiles presents significant growth potential for chemical manufacturers in the region.

- For instance, BASF’s PROBAN® flame retardant technology is applied to more than 400 million square meters of fabric annually, primarily used in protective clothing and technical textiles worldwide.

Shift Towards Sustainable and Eco-Friendly Products

Stringent environmental regulations and rising consumer awareness about sustainable fashion are pushing manufacturers toward the adoption of eco-friendly textile chemicals. Brands and producers in Asia are increasingly using low-impact dyes, water-based coatings, and biodegradable auxiliaries to reduce their environmental footprint. This transition is creating strong market opportunities for green chemistry innovations. Investments in sustainable manufacturing practices and the development of less toxic chemicals are not only regulatory necessities but also emerging as competitive advantages for industry players.

Key Trends & Opportunities

Growth in Smart and Functional Textiles

The rising popularity of smart textiles and garments with functional features such as UV protection, odor resistance, and temperature regulation is shaping new opportunities in the Asia textile chemicals market. These innovative products require advanced chemical treatments to achieve desired functionalities. With increasing consumer interest in wearable technology and performance-enhancing apparel, manufacturers are focusing on developing chemicals that can impart such advanced properties, creating a niche but rapidly expanding market segment.

- For instance, DyStar’s SERA® Smart process control technology has enabled precise chemical dosing in smart textile production, optimizing over 3,000 dyeing processes globally to enhance functional textile properties while reducing resource consumption.

Digital Printing and Low-Impact Dyeing

The growing adoption of digital textile printing is transforming the industry by enabling precision dyeing with reduced water and energy consumption. This trend aligns with the increasing demand for sustainable production methods. Textile chemicals compatible with digital printing processes, including specialized inks and pre-treatment agents, are gaining traction. Additionally, low-impact dyeing techniques that minimize environmental damage are becoming essential in Asia’s competitive textile markets, presenting opportunities for manufacturers to innovate and differentiate their chemical offerings.

- For instance, DIC Corporation’s high-performance pigment inks have been used in over 500 industrial digital textile printers worldwide, contributing to significantly lower wastewater generation compared to conventional dyeing processes.

Key Challenges

Environmental Regulations and Compliance

Stringent environmental regulations across Asia, particularly concerning wastewater management and chemical toxicity, pose a significant challenge for textile chemical manufacturers. Meeting regulatory standards requires substantial investment in cleaner production technologies and effluent treatment facilities. Non-compliance can result in fines, production halts, or even shutdowns, especially in countries like China where environmental audits have intensified. These regulatory pressures increase operational costs and can limit the competitiveness of smaller players in the market.

Volatility in Raw Material Prices

Fluctuations in the prices of raw materials, especially petrochemical-based inputs, present a persistent challenge for the Asia textile chemicals market. Unpredictable crude oil prices, supply chain disruptions, and dependency on imports for certain chemical components can significantly impact production costs. These price variations often squeeze profit margins for manufacturers and create pricing instability for end users. Managing cost fluctuations while maintaining product quality remains a key operational hurdle.

Rising Competition and Price Pressure

The Asia textile chemicals market is highly competitive, with numerous local and international players vying for market share. This competitive intensity often leads to price wars and shrinking margins, especially in commodity chemical segments. Additionally, customers increasingly demand cost-effective yet high-performance solutions, putting further pressure on manufacturers to deliver value while controlling expenses. Sustaining profitability and differentiation in such a price-sensitive environment is a continuing challenge for market participants.

Regional Analysis

China

China dominated the Asia Textile Chemicals market in 2024, holding a substantial market share of 38.5%. The market size in China reached USD 6,429.92 million in 2024, up from USD 4,552.35 million in 2018, and is projected to grow at a CAGR of 5.6% during the forecast period. China’s leadership in global textile production and export, coupled with strong domestic consumption, drives this growth. Continuous investments in advanced chemical processing and a rising focus on sustainable textile production further support the expanding demand for textile chemicals across the country’s manufacturing hubs.

India

India accounted for a market share of 25.7% in the Asia Textile Chemicals market in 2024, with the market size reaching USD 4,291.92 million, up from USD 2,943.30 million in 2018. The market is expected to grow at a CAGR of 5.9% through 2032. India’s expanding textile and apparel industry, driven by rising exports and increasing domestic demand, significantly boosts the consumption of textile chemicals. Government support for the textile sector through favorable policies and investments in infrastructure, such as textile parks, further enhances the country’s position as a key growth market in Asia.

Bangladesh

Bangladesh captured 14.8% of the Asia Textile Chemicals market share in 2024, with a market size of USD 2,468.53 million, up from USD 1,694.42 million in 2018, and is anticipated to register a CAGR of 5.5% during the forecast period. The country’s strong dependence on its textile and garment export industry, particularly to European and North American markets, fuels robust demand for textile chemicals. Continuous investments in modernizing textile manufacturing facilities and the increasing adoption of eco-friendly chemicals to meet international compliance standards support the steady growth of the textile chemicals sector in Bangladesh.

Vietnam

Vietnam represented 11.0% of the Asia Textile Chemicals market share in 2024, with the market valued at USD 1,834.69 million, increasing from USD 1,260.46 million in 2018. The market is projected to grow at a CAGR of 5.2% over the forecast period. Vietnam’s rapid emergence as a competitive textile manufacturing hub, supported by favorable trade agreements and growing foreign investments, drives the rising demand for textile chemicals. The country’s increasing focus on sustainable production practices and advanced processing technologies further contribute to the consistent expansion of the textile chemicals market in this region.

Rest of Asia

The Rest of Asia segment, covering countries like Indonesia, Pakistan, and Sri Lanka, accounted for 10.0% of the Asia Textile Chemicals market share in 2024, with a market size of USD 1,681.23 million, up from USD 1,368.54 million in 2018. The region is expected to grow at a CAGR of 4.9% through 2032. Growing textile production, increasing exports, and the gradual shift of manufacturing bases from China to lower-cost regions underpin market growth. Additionally, rising domestic consumption of textiles and efforts to upgrade manufacturing facilities are boosting the demand for advanced textile chemicals across these emerging markets.

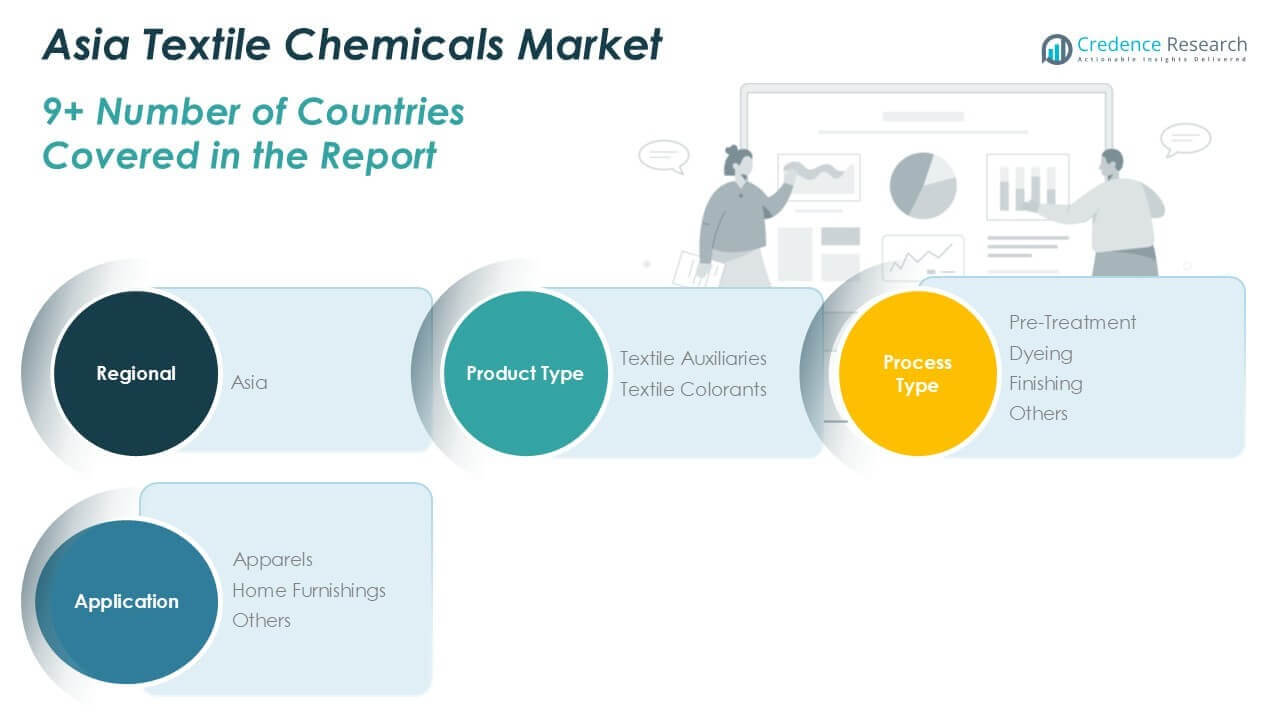

Market Segmentations:

By Product Type

- Textile Auxiliaries

- Textile Colorants

By Process Type

- Pre-Treatment

- Dyeing

- Finishing

- Others

By Application

- Apparels

- Home Furnishings

- Others

By Geography:

- China

- India

- Bangladesh

- Vietnam

- Rest of Asia

Competitive Landscape

The Asia Textile Chemicals market is highly competitive, characterized by the presence of both global and regional players striving to strengthen their market positions. Major companies such as BASF SE, Huntsman Corporation, DyStar Group, and Archroma Management LLC lead the market with extensive product portfolios, advanced technologies, and strong regional distribution networks. These key players focus on strategic initiatives including mergers, acquisitions, partnerships, and continuous product innovation to meet the growing demand for sustainable and high-performance textile chemicals. Local manufacturers like Arvind Ltd, Bombay Dyeing and Manufacturing Company Ltd, Shenzhou International Group, Texhong Textile Group, and Weiqiao Textile hold significant market shares by offering cost-effective solutions and maintaining long-standing relationships with regional textile producers. The competition is further intensified by increasing consumer expectations for eco-friendly products, which is pushing companies to invest in green chemistry and sustainable processing technologies. Overall, product differentiation, sustainability, and regional expansion remain the core competitive strategies in this dynamic market.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- BASF SE

- Arvind Ltd

- Bombay Dyeing and Manufacturing Company Ltd

- Shenzhou International Group

- Texhong Textile Group

- Weiqiao Textile

- Huntsman Corporation

- Archroma Management LLC

- DyStar Group

- DIC Corporation

Recent Developments

- In January 2024, Devan Chemicals, a provider of sustainable textile finishes, is excited to announce its upcoming participation in Heimtextil 2024. Devan invites attendees to visit their booth in Hall 11.0, booth A21, to experience firsthand the latest sustainable textile finishes they have developed.

- In April 2024, BASF SE announced its portfolio of polyamides for the textile industry. The company’s sustainable polyamide PA6 and PA6.6 product range have been certified under the Recycled Claim Standard (RCS) for textile applications. This certification allows BASF SE to market textiles produced using recycled raw materials.

- In November 2023, Solvay introduced a textile fiber that decomposes rapidly in the oceans, minimizing the environmental impact of microplastics. The new textile polyamide, set to be manufactured at the company’s industrial facility in Brazil, will decrease oceanic impact by roughly 40 times compared to traditional fibers. This product development aligns with the global trend of rising demand and market shifts toward more sustainable textile solutions.

- In May 2023, Dystar announced its eco-advanced indigo dyeing, which aims to reduce energy consumption by up to 30% and water usage by up to 90% during the production process.

- In August 2022, Archroma entered into a definitive agreement with Huntsman Corporation to acquire the latter’s Textile Effect business. The transaction, awaiting regulatory approvals, is expected to close in the first half of 2023. The acquisition is expected to benefit Archroma in building a comprehensive portfolio of chemical solutions to cater to the textile market.

- In February 2022, Archroma rolled out a new vegan textile softener, EARTH SOFT system based on Siligen EH1, with one-third plant-based active content. The new product line offers an alternative to textile manufacturers seeking to reduce fossil fuel-based ingredients in their end products.

Market Concentration & Characteristics

The Asia Textile Chemicals Market is moderately fragmented, with both global and regional players competing to secure significant market shares. It shows a balanced mix of established multinational corporations and strong local manufacturers. Companies focus on product innovation, cost efficiency, and sustainability to differentiate their offerings. The market demands high-performance chemicals that meet evolving environmental standards and consumer expectations for quality textiles. Growth is supported by the rising textile production across China, India, Bangladesh, and Vietnam. Intense price competition, strict regulatory frameworks, and shifting consumer preferences shape the competitive dynamics. It requires continuous technological advancement and strong supply chain capabilities to sustain growth.

Report Coverage

The research report offers an in-depth analysis based on Product Type, Process Type, Application and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The Asia Textile Chemicals market is expected to witness steady growth driven by increasing textile production across major countries.

- Demand for eco-friendly and sustainable textile chemicals will continue to rise due to stricter environmental regulations.

- Technological advancements in low-impact dyeing and water-efficient processes will shape future chemical innovations.

- The growing popularity of technical textiles will boost the need for specialized chemical treatments.

- Expansion in the fashion, sportswear, and home furnishing industries will support consistent market growth.

- Digital textile printing will gain more adoption, increasing the demand for compatible chemical formulations.

- Manufacturers will focus on developing biodegradable and non-toxic chemical solutions to meet global sustainability goals.

- Strategic partnerships and regional expansion by key players will intensify competitive dynamics in the market.

- Emerging economies like Vietnam, Bangladesh, and Indonesia will attract significant investments in textile chemical production.

- Supply chain optimization and raw material cost management will remain critical for maintaining profitability in the market.