| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Body Armor Market Size 2024 |

USD 2,405.1 Million |

| Body Armor Market, CAGR |

3.87 % |

| Body Armor Market Size 2032 |

USD 3,260.7 Million |

Market Overview

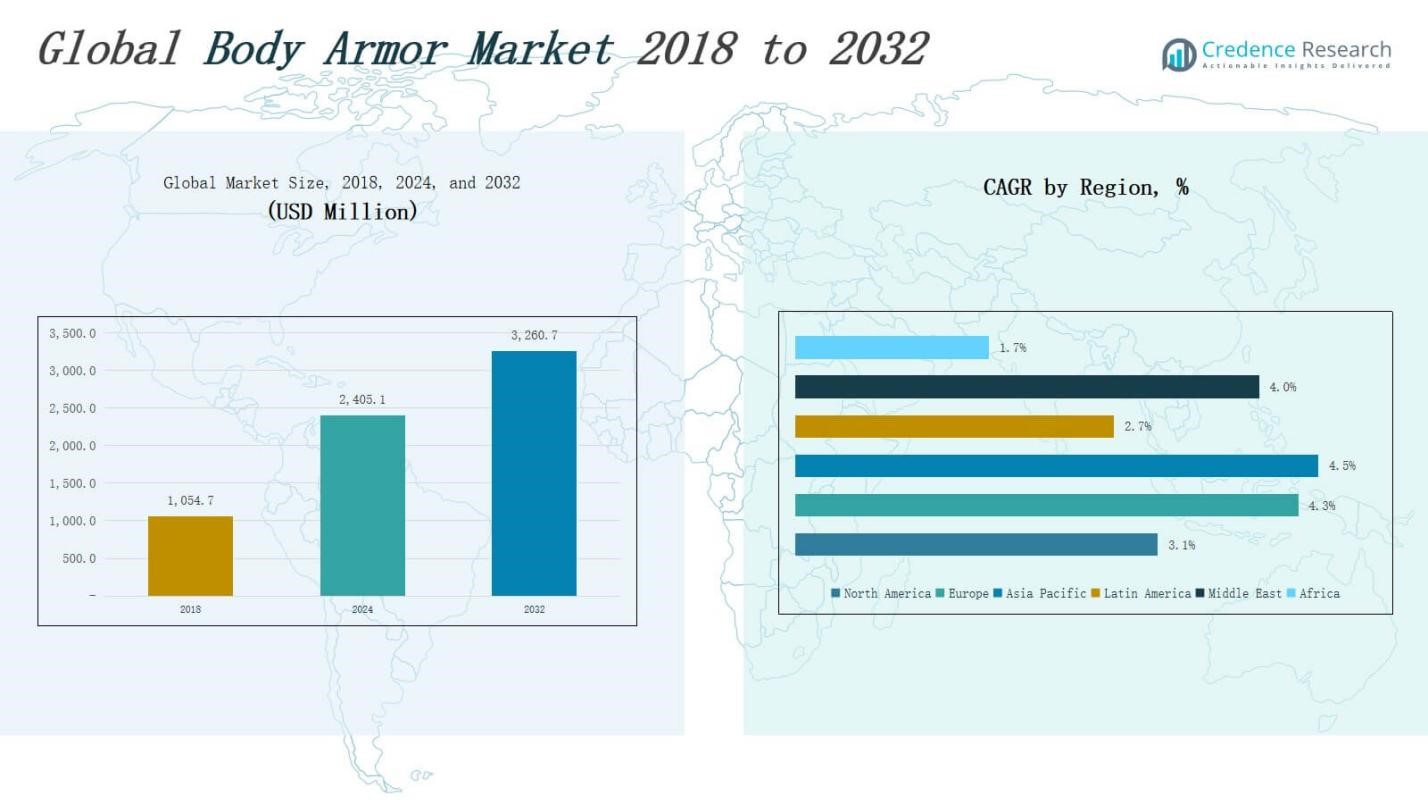

The Body Armor Market size was valued at USD 1,054.7 million in 2018 to USD 2,405.1 million in 2024 and is anticipated to reach USD 3,260.7 million by 2032, at a CAGR of 3.87 % during the forecast period.

The Body Armor Market is driven by escalating global security threats, rising defense budgets, and growing demand for personal protection among military, law enforcement, and civilians. The proliferation of asymmetric warfare and increasing incidents of violent crime and terrorism have pushed governments and security agencies to invest in advanced protective gear. Technological advancements in ballistic materials such as ultra-high-molecular-weight polyethylene (UHMWPE) and aramid fibers are enabling lighter, more durable, and flexible armor solutions. At the same time, the market is witnessing a strong trend toward modular and ergonomic designs that enhance mobility without compromising protection. Manufacturers are focusing on integrating smart textiles and sensor-based technologies for real-time monitoring of impacts and wearer vitals. The surge in homeland security investments, modernization of military equipment, and adoption of multi-threat protection solutions are reshaping product innovation. Demand for concealable and gender-specific armor also reflects the broadening application scope across varied user groups and mission-specific needs.

The Body Armor Market spans six key regions: North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa. Asia Pacific leads in growth rate due to increasing defense investments and internal security demands, while North America holds the largest revenue share, driven by advanced procurement in the U.S. and Canada. Europe shows strong momentum from modernization programs in countries like Germany and the UK. Latin America and the Middle East experience steady demand due to rising law enforcement needs, while Africa remains nascent but gradually expanding. The market features key players such as MKU Pvt. Ltd, Honeywell International Inc., BAE Systems, Safariland, LLC, Point Blank Enterprises, ArmorSource LLC, Survitec Group Limited, KDH Defense Systems Inc., and Australian Defence Apparel Pty Ltd, all competing through innovation, lightweight solutions, and tailored offerings for regional requirements.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Body Armor Market was valued at USD 2,405.1 million in 2024 and is projected to reach USD 3,260.7 million by 2032, growing at a CAGR of 3.87%.

- Demand is fueled by rising global threats, military modernization, and increased need for ballistic protection among law enforcement, civilians, and private security.

- Technological advancements in materials like UHMWPE and aramid fibers are enabling lightweight, durable, and modular armor systems tailored for varied threats.

- Integration of smart textiles and sensors is transforming body armor into intelligent systems capable of real-time impact detection and biometric monitoring.

- High material costs and fragmented regulatory standards challenge market expansion, particularly for budget-constrained buyers and small-scale manufacturers.

- Asia Pacific leads in growth rate, while North America holds the largest market share; Europe, Latin America, Middle East, and Africa show steady to emerging demand.

- Key players such as MKU Pvt. Ltd, Honeywell International Inc., BAE Systems, Safariland, and Point Blank Enterprises are focusing on innovation, exports, and mission-specific product lines.

Market Drivers

Heightened Threat Landscape and Rising Security Concerns

The Body Armor Market is propelled by the growing incidence of violent crimes, terrorism, and civil unrest worldwide. Governments and security agencies are increasing procurement of personal protective equipment to safeguard military personnel, law enforcement officers, and critical infrastructure security staff. It responds to an urgent need for enhanced survivability in both combat and non-combat environments. The prevalence of asymmetrical warfare and insurgent tactics has forced defense forces to prioritize body armor modernization. Civil unrest and urban conflicts have increased demand for riot-control gear and non-lethal protection equipment. The expanding private security sector, especially in volatile regions, contributes significantly to the market’s growth trajectory.

- For instance, BAE Systems plc supplied its Osprey body armor to the UK Ministry of Defence as part of ongoing modernization programs to protect British soldiers deployed in conflict areas; the Osprey system is recognized for its enhanced ballistic protection and modular design.

Military Modernization Programs and Budget Allocations

Military modernization initiatives across North America, Europe, and Asia Pacific are reinforcing procurement of advanced protective gear, significantly boosting the Body Armor Market. National defense budgets continue to rise, supporting large-scale body armor deployment and research programs focused on next-generation materials. It benefits from strategic partnerships between defense agencies and private manufacturers to streamline supply chains and improve equipment quality. Governments are prioritizing soldier lethality programs that include high-performance ballistic vests and modular armor components. The shift toward lightweight, high-durability armor systems aligns with battlefield mobility and survivability requirements. These initiatives are expected to remain consistent, backed by long-term defense spending plans and threat mitigation strategies.

- For instance, Protection Group Danmark introduced the LW+ SA lightweight hard armor NIJ Level III+ plate, weighing only 1.5 kg and designed for both military and law enforcement personnel seeking extended wear and reduced fatigue.

Technological Advancements in Ballistic Materials and Design

Continuous advancements in armor materials such as aramid fibers, UHMWPE, and ceramic composites are transforming the Body Armor Market. It is moving toward lightweight, multi-functional armor systems that provide superior protection without compromising mobility. Manufacturers are developing hybrid designs that integrate soft and hard armor elements tailored for different operational needs. Smart textiles embedded with sensors are entering the market, offering biometric monitoring and impact detection capabilities. These innovations enable dynamic threat response and enhance situational awareness. The shift toward ergonomic, mission-specific armor reflects rising user expectations for functionality, durability, and comfort during prolonged wear.

Growing Civil and Law Enforcement Demand for Protective Gear

The Body Armor Market is expanding beyond military use due to rising adoption in law enforcement and civilian sectors. Police departments face increasing risks from firearms and edged weapons, prompting upgrades in ballistic and stab-resistant vests. It also sees demand from journalists, private security professionals, and first responders working in high-risk areas. The proliferation of concealed carry permits and personal protection needs among civilians contributes to soft armor sales. Body armor manufacturers are offering gender-specific and modular designs that cater to a wider range of body types and operational roles. Public safety agencies and non-military users continue to drive bulk purchases supported by government funding and safety regulations.

Market Trends

Integration of Smart Technologies and Wearable Sensors

The Body Armor Market is witnessing a strong trend toward integrating wearable technologies that improve situational awareness and personal safety. Manufacturers are embedding sensors into vests to monitor vital signs, impact force, and ballistic trauma. It supports real-time data transmission to command centers, enabling faster medical intervention and tactical decisions. Smart textiles and wireless communication modules are also gaining attention for their ability to enhance coordination among personnel. These features are becoming standard in next-generation armor systems for military and law enforcement applications. Investment in research for energy-efficient, sensor-compatible materials is accelerating innovation in this segment.

- For instance, Vuzix offers smart glasses equipped with sensors that provide law enforcement and military personnel with hands-free access to real-time data, improving on-site safety and coordination by integrating location tracking and communication directly into the visor.

Rising Demand for Lightweight and Flexible Armor Solutions

There is a growing shift in the Body Armor Market toward lightweight and ergonomic armor solutions that enhance user mobility without sacrificing protection. Military forces and law enforcement units increasingly seek gear that reduces fatigue during extended missions. It drives innovation in composite materials, including ultra-high-molecular-weight polyethylene and advanced ceramics. Manufacturers are designing modular systems that allow users to adapt protection levels based on mission requirements. Weight reduction is becoming a critical performance metric across both hard and soft armor categories. This trend also supports increased adoption among civilians and private security personnel who prioritize comfort and concealability.

- For instance, Armor Express has introduced the RZR-XT-IIIA soft armor, combining aramid and ultra-high-molecular-weight polyethylene (UHMWPE) to achieve a thickness of just 0.20 inches (5.1 mm) and a weight of 0.84 lbs/ft²—making it highly flexible and suitable for prolonged use.

Customization and Gender-Specific Armor Development

The Body Armor Market is embracing user-specific customization, including gender-tailored designs and size adaptability. Law enforcement agencies and defense organizations are demanding armor that fits diverse body types without compromising protection. It encourages manufacturers to offer product lines specifically engineered for female personnel. Adjustable straps, flexible panels, and improved fit-and-finish standards are becoming essential features. The need for inclusive designs reflects a broader move toward user-centered development. Customization also enables better performance in active scenarios, improving wearability and reducing injury risks. This trend supports both tactical efficiency and wearer compliance across operational environments.

Increased Use of Sustainable and Recyclable Materials

Sustainability considerations are gaining traction in the Body Armor Market as manufacturers explore environmentally friendly production methods. Companies are adopting recyclable fibers and reducing reliance on hazardous chemicals in armor fabrication. It aligns with global regulatory pressure and corporate ESG commitments. Defense procurement programs are beginning to prioritize vendors offering greener solutions. Biodegradable or low-impact packaging, energy-efficient manufacturing, and sustainable sourcing practices are entering standard procurement criteria. These developments foster responsible innovation and create competitive differentiation. The shift toward circular economy principles is expected to influence future material selection and design protocols across the industry.

Market Challenges Analysis

High Costs of Advanced Materials and Production Constraints

The Body Armor Market faces significant challenges from the high cost of raw materials and advanced manufacturing processes. Aramid fibers, ceramics, and composite materials used in modern armor systems are expensive and require specialized fabrication techniques. It creates pricing pressure, particularly for budget-constrained defense and law enforcement agencies. Small-scale manufacturers often struggle to compete with larger players due to limited access to advanced technologies and economies of scale. Lead times for customized or high-spec products can also delay procurement cycles. These cost-related barriers restrict market penetration in developing countries and among civilian users.

Regulatory Compliance and Certification Complexities

Stringent regulatory standards and lengthy certification procedures present another major challenge for the Body Armor Market. Each region enforces different ballistic protection benchmarks, testing methods, and quality protocols. It complicates international distribution and increases compliance costs for manufacturers. Delays in testing and approval can hinder time-to-market for new product launches. Frequent changes in defense procurement requirements demand continuous adaptation, stretching R&D budgets and development cycles. This regulatory fragmentation limits operational flexibility and slows innovation across the global supply chain.

Market Opportunities

Expansion into Civilian and Commercial Security Segments

The Body Armor Market holds strong growth potential through expansion into civilian and private security sectors. Rising personal safety concerns and increased firearm ownership are driving demand for concealable, lightweight armor among civilians, journalists, and VIP protection services. It opens new revenue channels beyond traditional military and police procurement. Companies offering discreet, comfortable, and certified protection solutions can capture this emerging customer base. The growth of private security services, particularly in urban centers and high-risk zones, further supports commercial adoption. These non-government segments offer scalability through direct sales, e-commerce, and tactical retail networks.

Innovation in Modular and Multi-Threat Protection Systems

Opportunities exist in the Body Armor Market through the development of modular systems that address multiple threat scenarios. End users seek adaptable gear that allows integration of plates, trauma pads, and sensor modules based on mission profiles. It encourages manufacturers to design scalable solutions that combine ballistic, stab, and blast resistance in a single platform. Investments in R&D for multi-threat fabrics and hybrid armor composites can differentiate offerings in a competitive landscape. Government and defense agencies continue to prioritize flexible, next-generation gear for specialized forces and urban operations. This modular trend aligns with operational needs and boosts long-term product relevance.

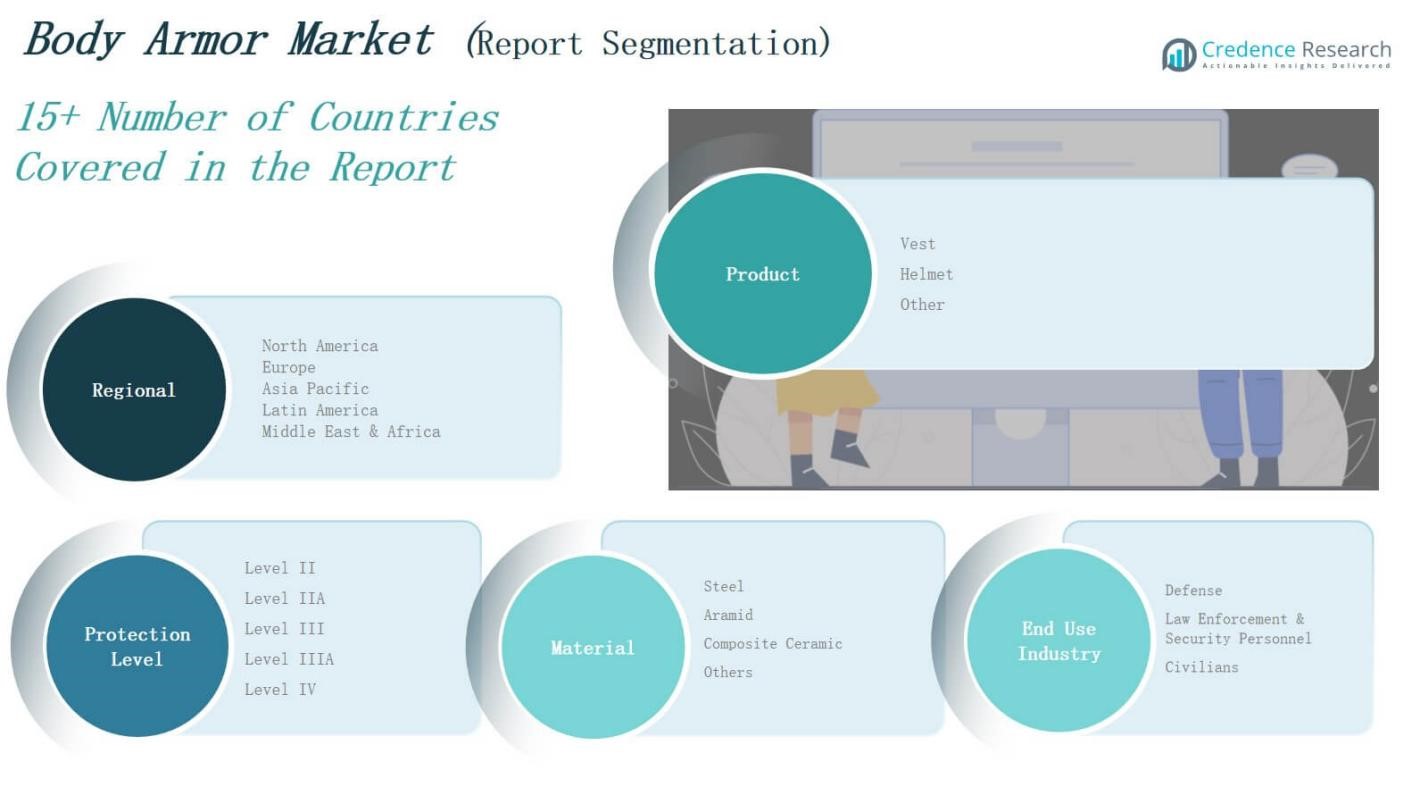

Market Segmentation Analysis:

By Product

The Body Armor Market is segmented by product into vests, helmets, and others. Vests hold the largest share due to their widespread use among military and law enforcement personnel for torso protection. Helmets are gaining traction for head protection in active combat and riot control situations. The “others” category includes shields and protective pads used in specialized scenarios. It continues to expand with evolving operational needs and non-lethal engagement requirements.

- For instance, Honeywell International provides lightweight bulletproof vests designed for law enforcement and military applications, leveraging advanced materials like Spectra fiber to increase comfort and protection.

By Protection Level

The Body Armor Market includes Level II, Level IIA, Level III, Level IIIA, and Level IV armor types. Level II and IIA offer lightweight protection against handgun threats and are widely used by law enforcement. Level III and IIIA provide greater ballistic resistance and are favored in tactical operations. Level IV offers the highest protection, capable of stopping armor-piercing rounds, and is primarily used by military personnel. Each level supports specific mission profiles based on threat environments.

- For instance, BAE Systems PLC supplies Level IV ceramic plates for military applications, engineered to defeat armor-piercing rifle rounds and adopted by several armed forces for high-risk conflict environments.

By Material

The Body Armor Market categorizes materials into steel, aramid, composite ceramic, and others. Aramid dominates due to its lightweight, flexible, and high-strength properties, making it suitable for soft body armor. Steel offers durability but adds significant weight, limiting mobility. Composite ceramics deliver high ballistic resistance while maintaining lighter weight, ideal for hard armor plates. The “others” category includes emerging materials like UHMWPE, which enhance comfort and multi-threat protection while reducing fatigue during extended use.

Segments

Based on Product:

Based on Protection Level:

- Level II

- Level IIA

- Level III

- Level IIIA

- Level IV

Based on Material:

- Steel

- Aramid

- Composite Ceramic

- Others

Based on End User Industry:

- Defense

- Law Enforcement & Security Personnel

- Civilians

Based on Region

North America

Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

Latin America

- Brazil

- Argentina

- Rest of Latin America

Middle East

- GCC Countries

- Israel

- Turkey

- Rest of Middle East

Africa

- South Africa

- Egypt

- Rest of Africa

Regional Analysis

North America

The North America Body Armor Market size was valued at USD 237.95 million in 2018 to USD 520.84 million in 2024 and is anticipated to reach USD 666.82 million by 2032, at a CAGR of 3.1% during the forecast period. North America holds the largest market share in the Body Armor Market, driven by robust defense budgets, advanced law enforcement infrastructure, and frequent procurement of next-generation armor solutions. The U.S. Department of Defense and homeland security agencies continue to invest heavily in modular and smart armor systems. It benefits from the presence of leading manufacturers such as Point Blank Enterprises and BAE Systems. Demand for concealable and lightweight armor is also growing among private security and civilian users. Strict regulatory standards and high awareness of ballistic protection further support regional growth.

Europe

The Europe Body Armor Market size was valued at USD 275.39 million in 2018 to USD 645.60 million in 2024 and is anticipated to reach USD 907.14 million by 2032, at a CAGR of 4.3% during the forecast period. Europe accounts for a significant share of the Body Armor Market due to rising investments in military modernization and counter-terrorism efforts. Countries like Germany, the UK, and France are actively upgrading soldier protection gear and riot-control equipment. It also benefits from NATO mandates that require member nations to improve combat readiness. Ongoing civil security concerns and migration-related unrest are fueling demand for body armor in border and law enforcement agencies. The region is seeing a strong trend toward eco-friendly and gender-specific armor products.

Asia Pacific

The Asia Pacific Body Armor Market size was valued at USD 318.85 million in 2018 to USD 755.62 million in 2024 and is anticipated to reach USD 1,076.04 million by 2032, at a CAGR of 4.5% during the forecast period. Asia Pacific is the fastest-growing region in the Body Armor Market, supported by rising defense expenditures in China, India, Japan, and South Korea. Geopolitical tensions, territorial disputes, and internal security threats are driving large-scale procurement of body armor across armed forces and paramilitary units. It also benefits from domestic production initiatives and technology collaborations. Growing law enforcement needs in urban areas and increasing civilian demand for personal protection gear further contribute to market growth. Regional manufacturers like MKU Ltd. are expanding their global footprint through exports.

Latin America

The Latin America Body Armor Market size was valued at USD 109.90 million in 2018 to USD 235.98 million in 2024 and is anticipated to reach USD 293.47 million by 2032, at a CAGR of 2.7% during the forecast period. Latin America holds a moderate share in the Body Armor Market, primarily driven by crime control efforts and law enforcement upgrades in countries like Brazil, Mexico, and Colombia. It sees growing demand for ballistic vests and helmets among police forces, private security firms, and correctional institutions. Limited defense budgets restrict high-end procurement, but governments are focusing on locally manufactured cost-effective armor solutions. The region faces challenges related to regulatory compliance and product standardization. Civilian interest in personal armor is also emerging in high-risk urban zones.

Middle East

The Middle East Body Armor Market size was valued at USD 66.87 million in 2018 to USD 153.62 million in 2024 and is anticipated to reach USD 210.32 million by 2032, at a CAGR of 4.0% during the forecast period. The Middle East Body Armor Market is shaped by ongoing military operations, counterinsurgency programs, and border security initiatives. Countries such as Saudi Arabia, Israel, and the UAE are key contributors to regional growth through large-scale defense procurement. It benefits from demand across both armed forces and internal security units. Regional conflicts and cross-border tensions increase the need for multi-threat protection systems. Local production capabilities and international collaborations are expanding the availability of advanced armor solutions. Demand for lightweight, high-mobility gear continues to rise.

Africa

The Africa Body Armor Market size was valued at USD 45.78 million in 2018 to USD 93.46 million in 2024 and is anticipated to reach USD 106.95 million by 2032, at a CAGR of 1.7% during the forecast period. Africa holds the smallest share in the Body Armor Market due to limited defense spending and procurement capacity. However, internal conflicts, anti-terrorism efforts, and peacekeeping missions are gradually increasing the need for protective gear across military and paramilitary units. It shows demand for basic ballistic protection, especially in countries like South Africa, Egypt, and Nigeria. External aid and international military support programs often fund armor procurement. The market faces infrastructure challenges and lacks uniform certification standards, slowing widespread adoption. Domestic production remains minimal, creating reliance on imports.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- MKU Pvt. Ltd

- KDH Defense Systems Inc.

- Survitec Group Limited

- Honeywell International Inc.

- BAE Systems

- Australian Defence Apparel Pty Ltd

- Safariland, LLC

- ArmorSource LLC

- Point Blank Enterprises, Inc.

- Other Key Players

Competitive Analysis

The Body Armor Market features a competitive landscape led by global defense contractors and specialized armor manufacturers. Key players include MKU Pvt. Ltd, Honeywell International Inc., BAE Systems, Safariland, LLC, and Point Blank Enterprises, Inc. Companies compete on innovation, material strength, weight reduction, and modularity. It favors firms that offer certified, mission-specific solutions for military, law enforcement, and civilian use. Strategic partnerships with defense agencies and expansion into emerging markets strengthen market positioning. Vendors focus on integrating smart technologies and sustainable materials to differentiate offerings. Continuous R&D investment and product customization are essential to meet evolving protection requirements. Competitive intensity remains high as firms strive to align with regional regulations and secure multi-year defense contracts.

Recent Developments

- In June 2025, BAE Systems signed an MoU with Helios Global Technologies to co-develop liquid armor solutions aimed at advancing ballistic protection using next-generation liquid-based materials.

- In January 2025, Safariland introduced two new ballistic panels—SX HP and Hardwire 57—at the SHOT Show, offering law enforcement personnel lighter weight and enhanced ballistic performance.

- In April 2025, BAE Systems selected Integris Composites to supply advanced ballistic protection systems for CV90 infantry fighting vehicles operated by European armed forces.

- In February 2025, EnGarde launched its MT‑PRO‑GEN7™ and COMFORT‑GEN7™ soft armor panels, featuring reduced weight, thinner profiles, and NIJ Level IIIA certification for improved mobility and protection.

Market Concentration & Characteristics

The Body Armor Market shows moderate to high market concentration, with a few dominant players holding significant global shares. It is characterized by a mix of large defense contractors and specialized manufacturers that focus on innovation, advanced materials, and product customization. Companies compete on the basis of lightweight design, multi-threat protection capabilities, and integration of smart technologies. The market is shaped by stringent procurement standards, long certification cycles, and high dependence on government contracts, particularly in North America and Europe. It features high entry barriers due to material costs, complex testing protocols, and regulatory compliance requirements. Regional demand variations drive the need for localized production and adaptive product strategies. The Body Armor Market also supports long-term supply contracts, which give established players an advantage in pricing and capacity planning. Product differentiation, R&D investment, and technological partnerships are central to maintaining competitive positioning and addressing evolving protection needs across defense, security, and civilian sectors.

Report Coverage

The research report offers an in-depth analysis based on Product, Protection Level, Material, End-User Indusrty and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Rising geopolitical tensions will continue to drive demand for advanced personal protection gear across military and paramilitary forces.

- Law enforcement agencies will increasingly adopt lightweight, modular body armor systems for urban and tactical operations.

- Civilian and private security segments will see higher demand for concealable and gender-specific protective solutions.

- Manufacturers will focus on integrating sensor-based technologies for impact detection and health monitoring.

- Hybrid armor designs using soft and hard materials will gain traction for mission-specific adaptability.

- Governments will prioritize domestic production and technology transfer agreements to ensure supply chain resilience.

- Regulatory frameworks will become more standardized, encouraging smoother product certification and global distribution.

- Investments in sustainable materials and eco-friendly production processes will influence procurement decisions.

- Procurement in emerging economies will grow, supported by rising internal security concerns and international aid.

- Key players will expand their presence through exports, partnerships, and localized manufacturing strategies.