Brachytherapy Devices Market Overview

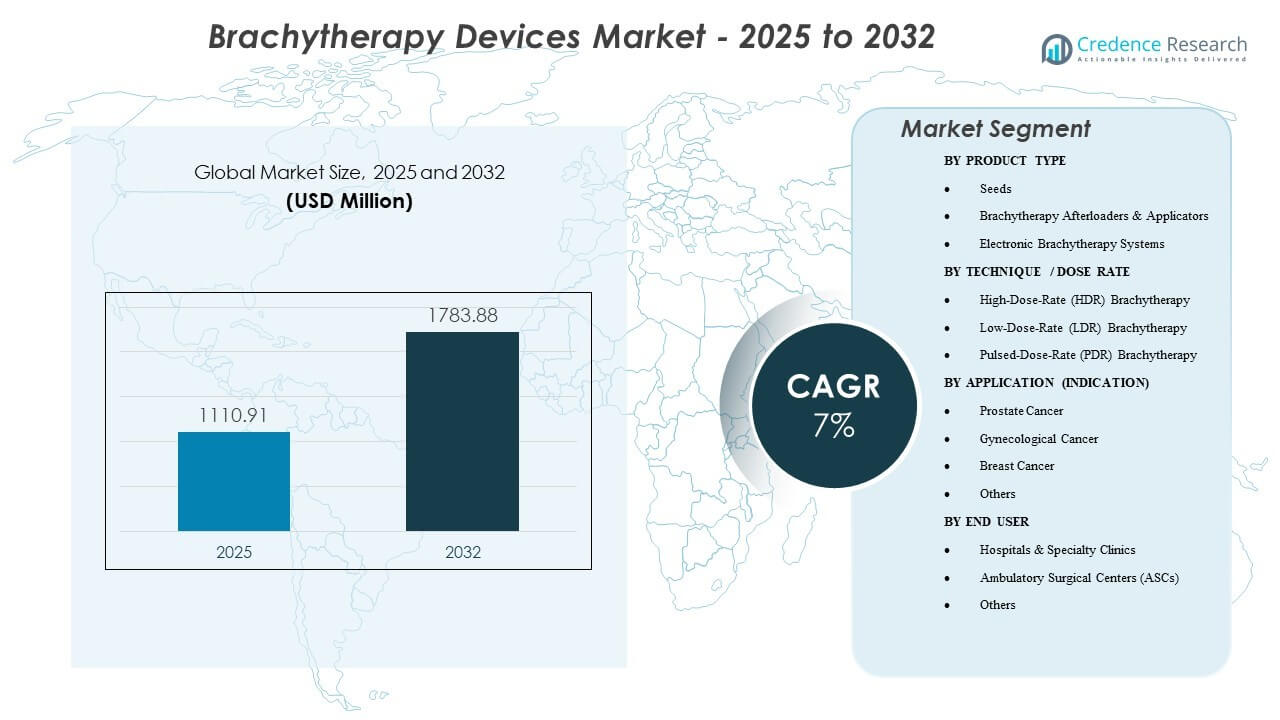

The global brachytherapy devices market size was valued at USD 1,110.91 million in 2025 and is expected to reach USD 1,783.88 million by 2032, growing at a CAGR of 7% from 2025 to 2032. Demand is supported by the shift toward localized, organ-sparing radiation treatments and rising cancer case volumes, along with wider adoption of image-guided planning that improves placement accuracy and dose conformity. In addition, high-throughput clinical workflows are reinforcing the use of HDR platforms and related consumables, as providers prioritize treatment time and scheduling efficiency. North America accounted for 45% of revenue in 2025, supported by a strong installed base, higher procedure volumes, and favorable reimbursement.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Brachytherapy Devices Market Size 2025 |

USD 1,110.91 million |

| Brachytherapy Devices Market, CAGR |

7% |

| Brachytherapy Devices Market Size 2032 |

USD 1,783.88 million |

Key Market Trends & Insights

- North America held 45% of global revenue in 2025, supported by higher procedure penetration and a large installed base of radiation oncology systems.

- HDR brachytherapy accounted for 72% share in 2025, reflecting preference for shorter, fractionated workflows and better scheduling efficiency.

- The market is forecast to grow at a 7% CAGR during 2025–2032, driven by modernization of oncology infrastructure and protocol-based adoption.

- Brachytherapy afterloaders & applicators captured 43% share in 2025, supported by mandatory platform use in HDR/PDR delivery and recurring applicator demand.

- Ambulatory Surgical Centers (ASCs) are expected to see steady growth f as outpatient pathways expand for eligible procedures.

Segment Analysis

Market demand is shaped by a balance between capital equipment (afterloaders, planning integration) and recurring procedure-linked components (applicators, accessories, and, in selected indications, seeds). Centers prioritize systems that improve throughput, standardize dose delivery, and reduce variability across operators, which supports consistent replacement cycles and service contract attachment. Workflow fit and clinical team capacity play a major role in purchase decisions, because brachytherapy requires coordinated scheduling across physicians, physicists, and imaging resources.

Indication mix remains a key determinant of device utilization patterns. Prostate and gynecological care continue to anchor a large share of clinical use due to established protocols, while breast applications benefit from localized approaches in selected patient groups. Adoption is also influenced by the availability of trained teams and the ability to integrate applicators with imaging and treatment planning to improve confidence in placement and dose coverage.

Site-of-care dynamics increasingly matter as providers seek efficient outpatient delivery where clinically appropriate. Hospitals remain the main installation environment due to infrastructure, staffing, and multi-disciplinary oncology pathways, while ASC growth is supported when streamlined HDR workflows and scheduling efficiency improve feasibility.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Product Type Insights

Brachytherapy Afterloaders & Applicators accounted for the largest share of 43% in 2025. This leadership reflects the central role of afterloaders in HDR/PDR treatment delivery, making them a core capital requirement for brachytherapy-capable centers. Applicators also contribute to repeat demand through procedure-specific designs and replacement cycles driven by utilization intensity and clinical standardization. Procurement often favors vendors offering integrated planning compatibility, service coverage, and a broad applicator portfolio that supports multiple indications.

By Technique / Dose Rate Insights

High-Dose-Rate (HDR) Brachytherapy accounted for the largest share of 72% in 2025. HDR dominance is reinforced by shorter treatment times, outpatient-friendly scheduling, and operational efficiency for high-volume oncology departments. Clinical adoption also benefits from established protocols and strong alignment with image-guided planning that supports consistent placement and dose delivery. Centers tend to prioritize platforms that support predictable fractionation workflows and reduce variability across procedures.

By Application (Indication) Insights

Prostate Cancer accounted for the largest share of 32% in 2025. The segment is supported by established clinical pathways and sustained procedure volumes in centers equipped for seed-based implants and HDR approaches in selected cases. Providers value predictable workflow integration with imaging and planning tools, which strengthens demand for compatible applicators and delivery systems. Replacement and upgrade decisions are often driven by throughput needs and the desire to improve placement accuracy and dose conformity.

By End User Insights

Hospitals & Specialty Clinics accounted for the largest share of 60% in 2025. This leadership reflects concentration of radiation oncology infrastructure, physicist coverage, and multi-disciplinary care teams required for planning and delivery. Hospitals also dominate capital procurement due to budget structures that support afterloader installations, service contracts, and standardized accessory portfolios. Specialty clinics reinforce demand where high procedure volumes justify dedicated brachytherapy workflows and frequent equipment utilization.

Market Drivers

Expanding Demand For Localized, Organ-Sparing Radiation

Brachytherapy supports high-dose delivery to a defined target while limiting exposure to surrounding tissue, which aligns with clinical goals for localized disease management. Demand grows when providers seek approaches that can fit into shorter treatment pathways for eligible patients. Increasing use of image-guided workflows improves confidence in placement and dose conformity, supporting broader adoption. These factors reinforce purchasing of systems and accessory portfolios that enable standardized delivery across teams.

- For instance, an MRI‑guided HDR prostate brachytherapy trial at a U.S. academic center achieved a median prostate V100 of 94% while keeping rectal V75 below 3.1%, demonstrating high target coverage with limited organ-at-risk dose.

Installed-Base Modernization And Workflow Standardization

Replacement cycles and upgrades contribute materially to market momentum as centers modernize planning, delivery, and safety features. Hospitals and high-throughput clinics increasingly emphasize consistent protocols, predictable scheduling, and improved utilization efficiency. This environment supports demand for afterloader platforms with integrated planning compatibility and robust service coverage. Standardization also increases accessory utilization, including procedure-specific applicators and related consumables.

Cancer Care Capacity Expansion In Emerging Systems

Expansion of oncology capacity in developing care systems supports new installations, especially where radiotherapy infrastructure is being strengthened across tertiary and regional centers. New site development increases demand for capital equipment, commissioning support, and training, which can accelerate installed base growth. Procurement decisions often favor vendors that offer end-to-end implementation, maintenance support, and staff training pathways. Over time, these installations create recurring demand via service and accessory replacement.

- For instance, Japan reports 129 Ir‑192 remote afterloaders installed nationwide for brachytherapy, indicating significant penetration of modern HDR capacity in a single Asia‑Pacific market.

Shift Toward Outpatient-Feasible Care Where Appropriate

When clinical protocols and operational capability allow, providers increasingly adopt outpatient-friendly brachytherapy delivery models. HDR’s scheduling advantages support this shift and can improve throughput for facilities managing high patient volumes. ASC growth is enabled where staffing and safety requirements are addressed and where workflow efficiency supports economic feasibility. This trend reinforces demand for platforms that reduce operational friction while maintaining delivery accuracy.

Market Challenges

Brachytherapy adoption remains sensitive to staffing availability and training depth because delivery requires coordinated teams and specialized planning workflows. Facilities without consistent physicist coverage and procedural expertise may limit utilization even after installing capital equipment. Operational constraints such as scheduling, imaging access, and procedure room availability can also reduce throughput, which affects ROI decisions and slows expansion.

- For instance, AAPM practice guidelines specify that an authorized medical physicist and an authorized user must be on site for treatment initiation and immediately available throughout delivery, meaning that any gap in this staffing model can force postponement or cancellation of scheduled HDR cases, reducing realized utilization relative to installed capacity.

Procurement complexity and lifecycle costs create additional friction for new installations. Capital budgets, service contracts, regulatory compliance, and commissioning requirements can lengthen purchasing cycles, especially in cost-sensitive markets. Standardization across applicator portfolios and compatibility with existing planning workflows also influences vendor selection, which can delay decision-making and reduce switching rates.

Market Trends and Opportunities

Electronic brachytherapy systems represent a key opportunity where providers seek simplified logistics and flexible deployment pathways in suitable use cases. Growth is supported by interest in solutions that reduce operational barriers and fit outpatient delivery models, particularly when implementation and workflow integration are streamlined. Vendors that package hardware, training, and service into scalable deployment models are better positioned to convert new sites.

- For instance, the Elekta Xoft Axxent electronic brachytherapy system delivers 50 kV low‑energy X‑rays from a mobile, shielded unit that can operate in standard procedure rooms without a dedicated bunker, and dosimetric comparisons in cervical cancer planning have shown a roughly 45% reduction in Point B dose to pelvic organs at risk versus traditional 192Ir or 60Co HDR sources (111 cGy vs about 210 cGy and 203 cGy, respectively) while maintaining target coverage.

Demand is also rising for applicator ecosystems optimized for image guidance and reproducible placement. Product differentiation increasingly depends on workflow fit, compatibility with planning systems, and accessory breadth across indications. Opportunities expand when vendors support clinical standardization with procedure kits, planning support tools, and service coverage that reduces downtime and improves utilization.

Regional Insights

North America

North America led the market with a 45% revenue share in 2025, supported by higher procedure penetration, established reimbursement pathways, and a large installed base across hospitals and specialty oncology networks. Demand remains strong for HDR workflows and broad applicator portfolios used across multiple indications. Replacement cycles and workflow modernization continue to support system upgrades and service contract growth.

Europe

Europe accounted for 25% of global revenue in 2025, supported by structured oncology care pathways and continued investment in radiotherapy infrastructure. Adoption is influenced by national procurement models, training availability, and standardization of brachytherapy protocols across major centers. Demand typically emphasizes compatibility, service reliability, and procedure standardization.

Asia Pacific

Asia Pacific captured 23% share in 2025 and is supported by expanding oncology capacity, increasing access to radiotherapy services, and growing installation activity across larger hospital systems. Market growth is reinforced by investments in modern planning and delivery workflows, along with rising adoption of standardized protocols in major urban centers. Implementation support and training remain key to sustained utilization expansion.

Latin America

Latin America represented 4% of global revenue in 2025. Growth is shaped by selective expansion of oncology capacity, procurement constraints, and uneven access to specialized staffing. Demand strengthens where hospitals pursue modernization and where vendor support improves commissioning and service continuity.

Middle East & Africa

Middle East & Africa accounted for 3.5% share in 2025. Adoption trends track investments in tertiary care infrastructure and radiotherapy modernization programs, with utilization depending on workforce depth and equipment availability. Demand is stronger in countries expanding national cancer care capacity and building specialist centers.

Competitive Landscape

Competition centers on afterloader platform performance, applicator ecosystem breadth, treatment planning compatibility, and service reliability. Vendors differentiate through workflow integration, uptime support, training capability, and the ability to support multiple indications with standardized accessory portfolios. Commercial strategy increasingly emphasizes installed-base retention via service contracts, upgrades, and procedure-linked accessory pull-through.

Varian Medical Systems (Siemens Healthineers) competes through integrated oncology workflows that connect planning, delivery, and service support, which can improve standardization and operational efficiency for high-volume centers. Its approach typically emphasizes clinical workflow alignment, broad system integration, and lifecycle support that reduces downtime and improves utilization across the installed base.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Varian Medical Systems (Siemens Healthineers)

- Elekta AB

- Eckert & Ziegler BEBIG

- Best Medical International (TeamBest)

- Theragenics Corporation

- IsoAid, LLC

- GT Medical Technologies

- iCAD, Inc. (XOFT)

- CIVCO Medical Solutions

- C4 Imaging LLC

- Merit Medical Systems

- Boston Scientific Corporation

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In January 2026, GT Medical Technologies reported that the first patients had been enrolled and treated with its GammaTile brachytherapy therapy in the BRIDGES randomized trial for newly diagnosed glioblastoma, marking the clinical start of a study designed to test whether immediate, surgically targeted GammaTile radiation at the time of tumor resection can improve survival compared with the standard delayed‑radiation approach.

- In June 2025, Elekta announced the acquisition of assets from its Croatian distributor to establish direct operations in Zagreb. This move followed a significant 2024 order from the Croatian Ministry of Health for 12 linear accelerators and four brachytherapy systems to address national equipment shortages.

- In March 2025, BEBIG Medical’s SagiNova® HDR Afterloader became operational at Father Muller Medical College Hospital in Mangalore, India. This launch was part of a major healthcare wing inauguration, supporting the company’s expansion in the Indian high-growth oncology market.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 1110.91 million |

| Revenue forecast in 2032 |

USD 1783.88 million |

| Growth rate (CAGR) |

7% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026–2032 |

| Quantitative units |

USD million |

| Segments covered |

By Product Type; By Technique / Dose Rate; By Application (Indication); By End User; By Region |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Varian Medical Systems (Siemens Healthineers), Elekta AB, Eckert & Ziegler BEBIG, Best Medical International (TeamBest), Theragenics Corporation, IsoAid, LLC, GT Medical Technologies, iCAD, Inc. (XOFT), CIVCO Medical Solutions, C4 Imaging LLC, Merit Medical Systems, and Boston Scientific Corporation. |

Segmentation

BY PRODUCT TYPE

- Seeds

- Brachytherapy Afterloaders & Applicators

- Electronic Brachytherapy Systems

BY TECHNIQUE / DOSE RATE

- High-Dose-Rate (HDR) Brachytherapy

- Low-Dose-Rate (LDR) Brachytherapy

- Pulsed-Dose-Rate (PDR) Brachytherapy

BY APPLICATION (INDICATION)

- Prostate Cancer

- Gynecological Cancer

- Breast Cancer

- Others

BY END USER

- Hospitals & Specialty Clinics

- Ambulatory Surgical Centers (ASCs)

- Others

BY REGION

- North America

- Europe

- Asia-Pacific

- South America

- Middle East and Africa