Brachytherapy Treatment Planning Systems Market Overview:

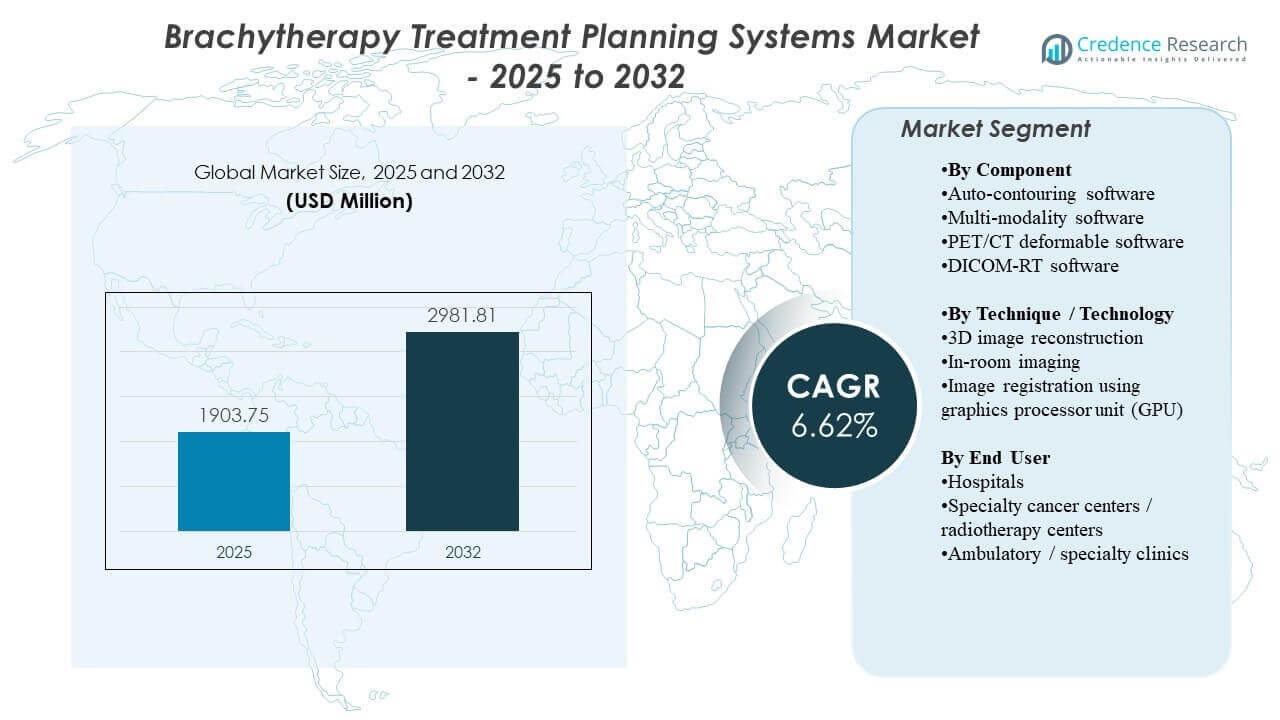

The global Brachytherapy Treatment Planning Systems Market size was estimated at USD 1903.75 million in 2025 and is expected to reach USD 2981.81 million by 2032, growing at a CAGR of 6.62% from 2025 to 2032. Growth is primarily supported by rising oncology procedure volumes and the need to improve treatment precision, consistency, and throughput in brachytherapy planning workflows. Increasing adoption of automation in contouring, stronger multi-modality image fusion needs, and broader digitization across radiotherapy departments are reinforcing demand for modern treatment planning capabilities across major care settings and regions.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Brachytherapy Treatment Planning Systems Market Size 2025 |

USD 1903.75 million |

| Brachytherapy Treatment Planning Systems Market, CAGR |

6.62% |

| Brachytherapy Treatment Planning Systems Market Size 2032 |

USD 2981.81 million |

Key Market Trends & Insights

- The market is projected to expand at a CAGR of 6.62% during 2025–2032.

- North America accounted for the largest share of 37.3% in 2025, supported by high adoption of advanced oncology software workflows.

- Asia Pacific held a 20.0% share in 2025, supported by expanding radiotherapy capacity and oncology infrastructure investments.

- Auto-contouring software accounted for the largest share of 34.0% in 2025, reflecting growing reliance on workflow automation.

- In-room imaging accounted for the largest share of 54.0% in 2025, reflecting the importance of image guidance in brachytherapy planning.

Segment Analysis

Brachytherapy treatment planning systems are increasingly purchased as part of broader radiotherapy workflow modernization, with buyers prioritizing planning accuracy, repeatability, and operational efficiency. Automation features such as contouring support faster plan creation and more consistent structure delineation, especially in high-volume centers managing diverse case mixes. Multi-modality planning needs are reinforcing demand for deformable workflows, particularly where cross-modality alignment is essential for delineation and target definition. Clinical teams also seek solutions that integrate cleanly with existing oncology information systems and quality assurance processes to reduce planning friction and improve throughput.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Technology selection is strongly influenced by the need to reduce uncertainty during planning and delivery. Imaging-driven planning remains central because reliable localization and verification contribute to tighter target margins and better normal-tissue sparing. Facilities also evaluate software based on usability, training requirements, and the strength of vendor support, particularly for advanced features such as deformable registration and adaptive workflows. Over time, procurement decisions are expected to weigh total workflow impact, including staffing efficiency, planning turnaround time, and interoperability with imaging and delivery ecosystems.

By Component Insights

Auto-contouring software accounted for the largest share of 34.0% in 2025. Automation is increasingly prioritized to reduce manual workload, standardize contouring output, and improve throughput in busy radiotherapy settings. The value proposition strengthens in multi-structure planning scenarios where consistent delineation reduces variability across clinicians and shifts. As AI models mature and become more integrated into routine workflows, decision-makers increasingly treat contouring automation as a core capability rather than an optional add-on.

By Technique / Technology Insights

In-room imaging accounted for the largest share of 54.0% in 2025. Real-time or near-real-time imaging supports higher confidence in target localization and reduces uncertainty that can impact dose coverage and organ-at-risk exposure. Imaging integration is also important for complex anatomy and cases that require tighter verification and documentation pathways. As clinical teams emphasize precision and toxicity reduction, in-room imaging remains a foundational requirement across many brachytherapy planning environments.

By End User Insights

Hospitals and specialty cancer centers represent the primary demand base due to higher procedure volumes, access to specialized staffing, and established quality assurance protocols. These settings typically adopt advanced planning capabilities to improve operational efficiency and support a wider range of brachytherapy case types. Ambulatory and specialty clinics participate where reimbursement, staffing capacity, and integration readiness support adoption. End-user purchasing decisions are commonly influenced by interoperability with existing radiotherapy ecosystems and the availability of vendor training and service support.

Brachytherapy Treatment Planning Systems Market Drivers

Rising cancer burden and brachytherapy procedure demand

Growth in oncology caseloads continues to increase the need for radiotherapy planning capacity and consistent clinical workflows. Brachytherapy planning tools support dose calculation, target definition, and documentation requirements that are critical for modern care delivery. Higher treatment volumes push providers to reduce planning turnaround time without compromising plan quality. These factors collectively sustain demand for robust and scalable treatment planning systems.

- For instance, RaySearch highlights that its RayStation brachytherapy workflows can reduce planning time from 45 to 15 minutes in the referenced RayBrachy context, directly addressing throughput pressure in busy departments.

Workflow efficiency and automation in planning

Providers seek productivity gains across planning steps, especially where staffing constraints and high patient throughput are persistent challenges. Automation, including contouring assistance and workflow standardization, reduces manual effort and helps improve consistency across clinicians and sites. Faster plan generation supports improved capacity utilization in radiotherapy departments. As a result, software capabilities that lower operational burden are increasingly tied to procurement decisions.

Demand for higher precision and image-guided planning

Planning accuracy is closely linked to outcomes and toxicity management, making image guidance a central requirement in brachytherapy workflows. Imaging integration supports target localization and verification, which improves confidence in dose placement relative to critical structures. Precision needs rise with complex anatomies, re-irradiation scenarios, and tighter margin philosophies. These trends sustain adoption of imaging-centric planning techniques and supporting software capabilities.

- For instance, Elekta’s Oncentra Brachy brochure highlights contouring/navigation in arbitrary planes across modalities including CT, PET/CT, ultrasound, and MRI, enabling multi-modality visualization for target/OAR definition.

Digitalization and system integration across oncology care

Radiotherapy departments continue to invest in integrated digital ecosystems that connect imaging, planning, delivery, and oncology information systems. Interoperability and smooth data exchange reduce planning friction and improve documentation and compliance readiness. Standardized workflows across multi-site health networks also increase the value of unified planning platforms. This digital shift supports continued upgrades and replacements across installed bases.

Brachytherapy Treatment Planning Systems Market Challenges

Clinical adoption can be constrained by training requirements, workflow change management, and variability in user readiness across sites. Advanced tools such as deformable workflows and high-end imaging integration may require additional validation and quality assurance oversight, which can slow deployment. Integration complexity across heterogeneous IT environments can also delay implementation timelines. These issues are particularly important in multi-site systems where standardization and governance requirements are stringent.

- For instance, GE HealthCare’s AIR Recon DL (deep-learning MR reconstruction) is associated with reported scan-time reductions “up to 50%,” a magnitude that often triggers protocol re-validation and governance review when sites standardize sequences across departments.

Cost pressure remains a barrier in settings with limited capital budgets or constrained reimbursement environments. Facilities may prioritize essential upgrades over advanced functionality, especially where existing systems remain functional. Vendor selection can also be influenced by long-term service commitments, upgrade pathways, and interoperability risk. These factors can extend purchase cycles and increase emphasis on total cost of ownership.

Brachytherapy Treatment Planning Systems Market Trends and Opportunities

AI-enabled workflow features are increasingly embedded into radiotherapy planning environments, supporting faster planning and more standardized outputs. Automation is expected to expand beyond contouring into broader planning assistance, documentation support, and workflow orchestration. This creates opportunities for vendors to differentiate on clinical usability, model performance, and seamless integration into routine planning processes. Buyers are also expected to value transparent QA pathways that support confident clinical deployment.

- For instance, Elekta ONE Planning states “zero-click” automated contouring completed in under 45 seconds and positions GPU-based Monte Carlo dose computation as up to 49× faster than CPU on average (with site examples like up to 35× for prostate), which are concrete integration/throughput claims used to differentiate planning usability and performance.

Emerging markets are expanding oncology infrastructure and radiotherapy capacity, creating opportunities for scalable, service-supported planning deployments. Adoption can accelerate where vendors provide strong training, remote support, and flexible implementation approaches aligned to local infrastructure. Multi-modality planning demand continues to grow as imaging approaches diversify and clinical protocols evolve. These trends increase opportunities for solutions that simplify image fusion, registration, and planning workflows without adding operational burden.

Regional Insights

North America

North America held a 37.3% revenue share in 2025, supported by advanced radiotherapy infrastructure and high adoption of modern oncology software workflows. Providers emphasize planning accuracy, documentation readiness, and workflow efficiency to support high patient volumes. Integrated ecosystems that connect imaging, planning, and oncology information systems remain a key purchasing factor. Competitive differentiation often centers on automation, usability, and vendor support capabilities.

Europe

Europe accounted for 29.3% of revenue in 2025, supported by structured radiotherapy networks and steady modernization of planning environments. Clinical adoption is influenced by quality-focused protocols, governance standards, and workflow standardization across care networks. Buyers often prioritize interoperability and long-term upgrade pathways to protect installed-base investments. Demand is reinforced by ongoing investments in oncology care delivery and radiotherapy capacity upgrades.

Asia Pacific

Asia Pacific represented 20.0% of revenue in 2025, supported by expanding oncology infrastructure and increasing adoption of modern planning tools. Growth is reinforced by rising cancer incidence, capacity expansion in radiotherapy centers, and investment in imaging and digital oncology workflows. Facilities prioritize scalable deployment, training support, and robust clinical usability to manage diverse case mixes. Vendor success is often tied to service coverage and implementation flexibility across varied hospital environments.

Latin America

Latin America held an 8.8% revenue share in 2025, supported by gradual expansion of radiotherapy services and targeted modernization in larger urban care centers. Adoption is influenced by budget constraints and procurement cycles, which increase emphasis on total cost of ownership and vendor support. Implementation is supported when platforms integrate cleanly with existing imaging and delivery infrastructure. Growth opportunities remain tied to capacity expansion and broader digitalization of oncology services.

Middle East & Africa

Middle East & Africa accounted for 4.6% of revenue in 2025, supported by incremental expansion of oncology infrastructure and increasing investment in specialized cancer centers. Adoption is concentrated in higher-resource markets and flagship institutions building comprehensive radiotherapy capabilities. Buyers often prioritize vendor-led training, service reliability, and integration readiness to support safe deployment. Longer procurement cycles and infrastructure variability can shape near-term adoption patterns.

Competitive Landscape

Competition focuses on workflow automation, image-guided planning performance, interoperability, and clinical usability, with vendors differentiating through planning accuracy, QA features, and service support. Product roadmaps increasingly emphasize AI-enabled contouring and workflow improvements that reduce planning time and standardize outputs across clinicians. Partnerships and ecosystem alignment with imaging and delivery platforms remain important to reduce integration friction. Vendors also compete on upgrade pathways and deployment support that accelerate adoption across multi-site networks.

Elekta AB emphasizes integrated oncology workflows through planning platforms and broader digital radiotherapy ecosystems that support standardization and operational efficiency. The company’s approach typically aligns planning capabilities with data management and clinical workflow needs to support repeatable delivery across varied treatment environments. Focus areas include interoperability, usability, and support models that enable broader adoption across health networks. Continued platform enhancements and deployment expansion reinforce Elekta AB’s positioning in digital radiotherapy planning environments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Elekta AB

- Varian Medical Systems

- MIM Software

- RaySearch Laboratories

- Prowess Inc.

- C4 Imaging

- Mirada Medical

- Mobius Medical Systems

- DOSIsoft

- RayStation (RaySearch)

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In June 2025, Elekta announced the acquisition of assets from its distributor in Croatia, a move intended to strengthen Elekta’s direct presence (office in Zagreb, service engineers, added staff) and improve service/upgrade support for installed radiotherapy and brachytherapy customers in the country.

- In January 2025, a research team at CHU de Québec–Université Laval disclosed that its gMCO-GUI multi-criterion optimization software entered a strategic partnership with Elekta, with integration underway and the algorithm expected to join the Elekta ecosystem in the coming years to help modernize brachytherapy planning.

- In January 2024, MIM Software expanded regulatory-cleared capabilities for AI-based contouring models, supporting broader clinical adoption of automated structure delineation in radiotherapy planning workflows.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 1903.75 million |

| Revenue forecast in 2032 |

USD 2981.81 million |

| Growth rate (CAGR) |

6.62% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026-2032 |

| Quantitative units |

USD million |

| Segments covered |

By Component Outlook: Auto-contouring software, Multi-modality software, PET/CT deformable software, DICOM-RT software; By Technique / Technology Outlook: 3D image reconstruction, In-room imaging, Image registration using graphics processor unit (GPU); By End User Outlook: Hospitals, Specialty cancer centers / radiotherapy centers, Ambulatory / specialty clinics |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Elekta AB, Varian Medical Systems, MIM Software, RaySearch Laboratories, Prowess Inc., C4 Imaging, Mirada Medical, Mobius Medical Systems, DOSIsoft, RayStation (RaySearch) |

| No. of Pages |

338 |

Segmentation

BY COMPONENT

- Auto-contouring software

- Multi-modality software

- PET/CT deformable software

- DICOM-RT software

BY TECHNIQUE / TECHNOLOGY

- 3D image reconstruction

- In-room imaging

- Image registration using graphics processor unit (GPU)

BY END USER

- Hospitals

- Specialty cancer centers / radiotherapy centers

- Ambulatory / specialty clinics

BY REGION

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa