Market Overview

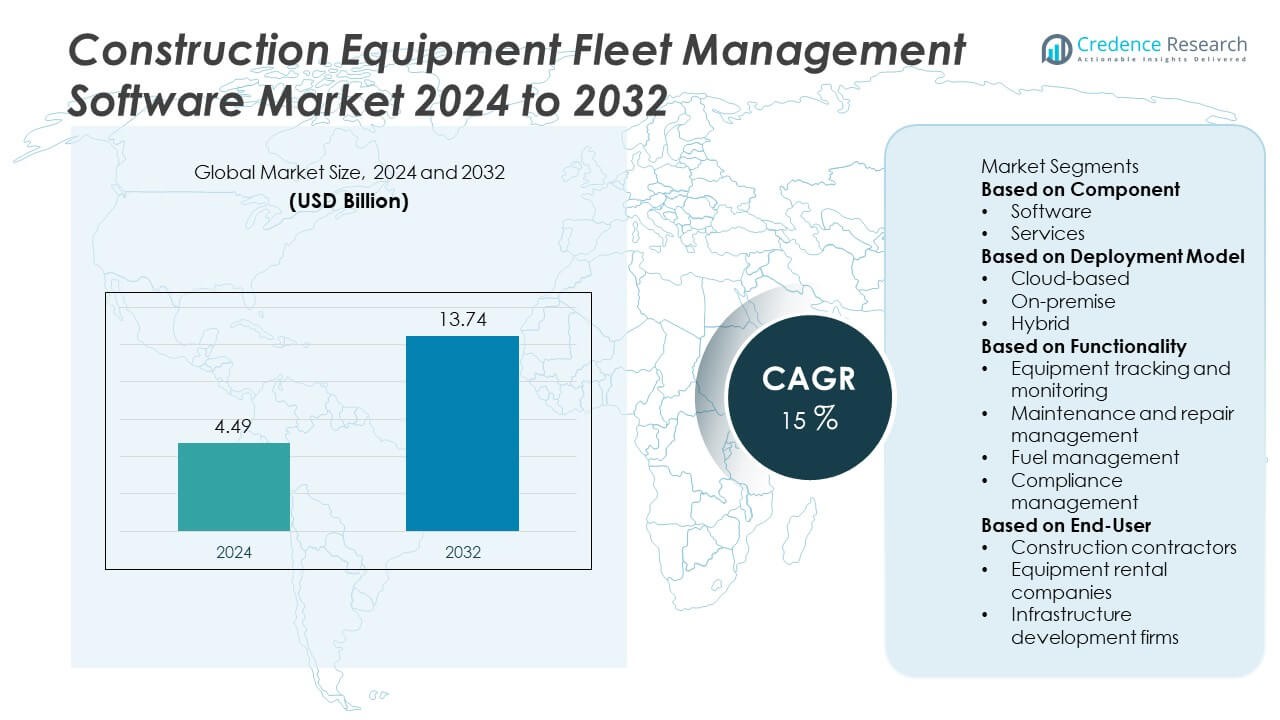

The Construction Equipment Fleet Management Software Market was valued at USD 4.49 billion in 2024 and is projected to reach USD 13.74 billion by 2032, expanding at a CAGR of 15% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Construction Equipment Fleet Management Software Market Size 2024 |

USD 4.49 Billion |

| Construction Equipment Fleet Management Software Market, CAGR |

15% |

| Construction Equipment Fleet Management Software Market Size 2032 |

USD 13.74 Billion |

The Construction Equipment Fleet Management Software market is led by prominent players such as Trimble, Caterpillar, Komatsu, John Deere, Hitachi Construction Machinery, Topcon Positioning Systems, Volvo Construction Equipment, Samsara, Teletrac Navman, and Zebra Technologies. These companies dominate through integrated telematics platforms, IoT-based analytics, and cloud-driven asset management solutions that enhance operational visibility and equipment utilization. North America led the market with a 36% share in 2024, supported by rapid adoption of digital construction technologies and strong investment in infrastructure modernization. Europe followed with 27%, driven by fleet optimization needs and sustainability goals, while Asia-Pacific, holding 30%, witnessed accelerated growth from large-scale construction and smart city projects.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The construction equipment fleet management software market was valued at USD 4.49 billion in 2024 and is projected to reach USD 13.74 billion by 2032, growing at a CAGR of 15% during the forecast period.

- Market growth is driven by rising demand for real-time fleet tracking, predictive maintenance, and automation to enhance productivity and minimize equipment downtime.

- Key trends include increasing adoption of IoT, AI, and cloud-based analytics platforms for remote monitoring, asset optimization, and sustainability compliance across construction fleets.

- The market is competitive, with major players such as Trimble, Caterpillar, Komatsu, and John Deere focusing on digital integration, data analytics, and telematics-based solutions to strengthen global presence.

- North America led the market with a 36% share in 2024, followed by Asia-Pacific with 30% and Europe with 27%, while the software segment dominated with a 64% share due to higher deployment in large-scale equipment management systems.

Market Segmentation Analysis:

By Component

The software segment dominated the construction equipment fleet management software market in 2024, accounting for a 65% share. This dominance stems from the rising integration of telematics, GPS tracking, and IoT-based analytics in fleet operations. Software solutions provide real-time visibility into asset location, fuel consumption, and equipment performance, enabling data-driven decision-making. Increasing adoption of AI and cloud technologies enhances predictive maintenance and reduces operational downtime. The demand for centralized fleet management platforms among construction companies continues to drive segment expansion, as they help optimize utilization and ensure higher productivity.

- For instance, Caterpillar Inc. integrated VisionLink across its fleet management ecosystem, processing machine data points for performance analytics. VisionLink provides key insights to maximize performance, monitor fleets, and optimize utilization.

By Deployment Model

The cloud-based segment led the market with a 59% share in 2024, driven by its scalability, cost efficiency, and easy accessibility across multiple job sites. Cloud deployment enables seamless data synchronization, remote monitoring, and real-time reporting for construction companies managing large fleets. Contractors increasingly prefer subscription-based cloud platforms to reduce IT overhead and improve data security. The growing use of mobile applications and remote operations management further strengthens this segment. Continuous advancements in cloud computing and SaaS-based fleet solutions are expected to fuel sustained adoption across global construction markets.

- For instance, Samsara Inc. connected more than 2.3 million IoT devices to its unified cloud fleet management platform, enabling real-time tracking and predictive diagnostics for construction equipment.

By Functionality

The equipment tracking and monitoring segment held the largest share of 42% in 2024, supported by increasing demand for real-time visibility and performance optimization. Advanced telematics and IoT sensors allow operators to track asset location, utilization rates, and operational health. This functionality minimizes idle time, prevents theft, and improves project scheduling accuracy. Construction firms are deploying intelligent tracking systems to manage dispersed fleets efficiently and reduce unplanned maintenance. Integration with AI-based analytics further enhances operational control, enabling proactive decision-making and extending equipment lifespan across large-scale infrastructure and commercial projects.

Key Growth Drivers

Rising Demand for Equipment Utilization and Cost Optimization

Construction companies are increasingly adopting fleet management software to enhance equipment utilization and reduce idle time. These platforms help track machine performance, fuel efficiency, and maintenance schedules in real time, lowering operational costs. The growing focus on maximizing return on assets (ROA) and minimizing downtime is driving adoption across infrastructure and heavy construction projects. Advanced analytics and telematics integration are further supporting efficient resource allocation, ensuring higher productivity and profitability in large-scale fleet operations.

- For instance, John Deere’s JDLink™ telematics platform monitors over 500,000 connected machines and offers tools and data to improve uptime and reduce maintenance costs.

Expansion of Smart Construction and IoT Integration

The integration of IoT and telematics technologies is a major growth driver in the construction equipment fleet management software market. Connected sensors enable real-time monitoring of equipment health, location, and environmental conditions. These data insights support predictive maintenance and help reduce mechanical failures. Construction firms are using IoT-driven platforms to streamline communication between operators and site managers. The ongoing shift toward smart construction ecosystems enhances safety, reliability, and operational transparency, strengthening market adoption globally.

- For instance, Trimble Inc. operates a connected ecosystem with over 1.3 million active devices, using GNSS and IoT sensors to deliver centimeter-level precision in fleet positioning and performance tracking.

Regulatory Push for Safety and Compliance

Increasing government regulations related to worker safety, emissions, and equipment maintenance are promoting the adoption of fleet management software. Compliance management modules help track certifications, inspections, and operational logs, ensuring adherence to safety standards. Construction companies rely on digital systems to automate compliance reporting and prevent violations. The need to meet evolving environmental and operational regulations across regions like North America and Europe continues to drive demand for integrated and compliant fleet management solutions.

Key Trends & Opportunities

Adoption of AI and Predictive Maintenance Solutions

AI-based predictive maintenance is transforming fleet management by enabling early detection of performance anomalies. Machine learning algorithms analyze sensor data to predict failures before they occur, reducing downtime and repair costs. This trend is gaining traction among large construction firms managing multiple heavy equipment fleets. Integration of predictive tools with telematics platforms enhances decision-making, boosts operational efficiency, and extends machinery lifespan. Companies investing in AI-driven solutions are improving fleet reliability while reducing total ownership costs.

- For instance, Komatsu Ltd.’s KOMTRAX system uses predictive analytics and real-time data to anticipate maintenance needs, aiming to reduce unscheduled maintenance across connected fleets. This strategy helps optimize maintenance schedules and improve machine uptime.

Cloud-Based and Mobile Fleet Management Expansion

The growing shift toward cloud-based and mobile-enabled fleet management platforms is creating new opportunities for remote operations. Cloud deployment allows real-time data sharing across construction sites and headquarters, improving collaboration. Mobile apps enhance accessibility by enabling field managers to monitor and control equipment from any location. This flexibility is particularly beneficial for multi-site contractors. As construction projects become more geographically dispersed, the demand for mobile-friendly and scalable fleet management software continues to accelerate globally.

- For instance, Topcon Positioning Systems developed its MAGNET Construct mobile application for Android and iOS handheld devices to enable remote site coordination, graphical-based layout, and asset mapping for construction projects.

Key Challenges

High Implementation and Integration Costs

The initial investment for advanced fleet management systems remains a major barrier, especially for small and medium-sized contractors. Costs include software licensing, IoT sensor installation, and integration with existing enterprise systems. In addition, ongoing maintenance and data analytics services increase total expenditure. While the long-term benefits are significant, the short-term financial burden slows adoption in cost-sensitive regions. Vendors are addressing this challenge by introducing modular and subscription-based models to improve affordability and accessibility.

Data Security and Connectivity Concerns

The reliance on cloud and IoT platforms increases vulnerability to cyber threats and data breaches. Construction firms store sensitive operational data, including equipment usage patterns and project timelines, which require secure transmission and storage. Weak network infrastructure in remote construction areas can also disrupt data flow and reduce system reliability. Addressing cybersecurity and connectivity challenges through advanced encryption, secured networks, and reliable connectivity solutions is essential for maintaining user trust and ensuring uninterrupted operations.

Regional Analysis

North America

North America held a 35% share of the construction equipment fleet management software market in 2024, driven by strong digital adoption across infrastructure and commercial construction projects. The United States leads the region due to widespread use of IoT, telematics, and AI-based asset management platforms. Government initiatives promoting smart construction and sustainable infrastructure further enhance demand. The presence of key players offering advanced analytics and compliance tools supports regional growth. Rising investments in predictive maintenance systems and cloud-based deployment models continue to strengthen North America’s leadership in technology-driven fleet operations.

Europe

Europe accounted for 27% of the global market in 2024, fueled by stringent regulations on equipment safety, emissions, and operational compliance. Countries such as Germany, France, and the U.K. are at the forefront of adopting digital fleet management platforms. The region’s focus on automation, sustainability, and operational transparency supports software adoption in large-scale infrastructure projects. Cloud-based solutions are gaining traction among equipment rental firms and contractors seeking real-time monitoring and regulatory alignment. The growing emphasis on lifecycle management and predictive analytics is accelerating the digital transformation of Europe’s construction ecosystem.

Asia-Pacific

Asia-Pacific dominated the construction equipment fleet management software market with a 30% share in 2024, driven by rapid urbanization, industrialization, and infrastructure expansion in China, India, and Japan. The region’s growing construction activities and government-led smart city initiatives are spurring adoption of digital fleet monitoring systems. Local contractors increasingly prefer cloud-based and mobile-enabled platforms to enhance equipment visibility and productivity. Investments in IoT-enabled machinery and data analytics tools are rising as firms aim to improve cost efficiency and reduce downtime. Expanding manufacturing bases and technology integration continue to position Asia-Pacific as the fastest-growing regional market.

Middle East & Africa

The Middle East & Africa region captured a 5% share in 2024, supported by growing infrastructure, oil and gas, and construction projects in Saudi Arabia, the UAE, and South Africa. Major government initiatives such as Saudi Vision 2030 are driving digital transformation and the integration of smart fleet management systems. Harsh working conditions and remote project locations are increasing reliance on predictive maintenance and equipment tracking solutions. Vendors are focusing on providing tailored cloud-based software to improve asset utilization. The region’s rising focus on operational efficiency and sustainability is gradually boosting adoption of advanced fleet management platforms.

South America

South America held a 3% share of the market in 2024, led by Brazil, Chile, and Argentina, where infrastructure development and mining activities are expanding. Construction companies in the region are increasingly adopting digital tools to monitor equipment performance and minimize downtime. Growing partnerships between global software vendors and local contractors are enhancing awareness and accessibility. Economic recovery and government investment in public infrastructure are further driving adoption. However, challenges such as limited internet connectivity and budget constraints persist, slowing widespread implementation of advanced fleet management systems across smaller enterprises.

Market Segmentations:

By Component

By Deployment Model

- Cloud-based

- On-premise

- Hybrid

By Functionality

- Equipment tracking and monitoring

- Maintenance and repair management

- Fuel management

- Compliance management

By End-User

- Construction contractors

- Equipment rental companies

- Infrastructure development firms

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The competitive landscape of the Construction Equipment Fleet Management Software market includes major players such as Trimble, Hitachi Construction Machinery, Caterpillar, Topcon Positioning Systems, Volvo Construction Equipment, Komatsu, Zebra Technologies, John Deere, Samsara, and Teletrac Navman. These companies are leading innovation through advanced telematics, IoT integration, and predictive analytics solutions that enhance equipment efficiency and reduce downtime. Market leaders are focusing on cloud-based platforms offering real-time tracking, maintenance alerts, and performance analytics. Strategic collaborations with construction firms and equipment OEMs are expanding product reach globally. Continuous investment in AI-driven analytics, remote diagnostics, and data-driven decision tools is strengthening competitive differentiation. Moreover, regional expansion, scalable SaaS offerings, and user-friendly interfaces are central to maintaining market dominance. The competition remains intense as vendors prioritize automation, cost optimization, and fleet visibility to cater to growing demands in large-scale infrastructure and smart construction projects worldwide.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Trimble

- Hitachi Construction Machinery

- Caterpillar

- Topcon Positioning Systems

- Volvo Construction Equipment

- Komatsu

- Zebra Technologies

- John Deere

- Samsara

- Teletrac Navman

Recent Developments

- In April 2025, Hitachi Construction Machinery launched LANDCROS Connect, a mixed-brand fleet platform that manages non-Hitachi machines from one dashboard.

- In February 2025, Trimble released FieldLink v2025.1.0 with new inspection and layout reporting to tighten field-to-office workflows used alongside connected machine control fleets.

- In September 2024, Continental Tire added onto their ContiConnect fleet management software by releasing two new versions, ContiConnect Lite and ContiConnect Pro. This modification intends to offer specific and customer-centric options for fleet managers to ensure efficient and sustainable practice in their tire maintenance.

- In August 2024, Align Technologies reported the acquisition of FleetWatcher, a significant company who specializes in fleet and material management software systems for heavy civil construction. This initiative is meant to strengthen the operating capabilities for Align’s customers by consolidating tools, equipment, fleet, and materials management in a single system.

Report Coverage

The research report offers an in-depth analysis based on Component, Deployment Model, Functionality, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will expand rapidly as construction firms prioritize digital fleet management solutions.

- Cloud-based platforms will dominate due to scalability, real-time access, and lower IT costs.

- Predictive analytics and AI will enhance maintenance scheduling and equipment performance.

- Integration with IoT and telematics will improve fleet visibility and operational efficiency.

- Data-driven insights will drive fuel optimization and emissions reduction initiatives.

- North America will remain a leading region supported by advanced digital infrastructure.

- Asia-Pacific will witness the fastest growth driven by urbanization and infrastructure investments.

- Partnerships between software developers and OEMs will boost integrated fleet ecosystems.

- Cybersecurity and data privacy measures will become key priorities for solution providers.

- Continuous innovation in automation and machine learning will define the market’s competitive edge