Market Overview

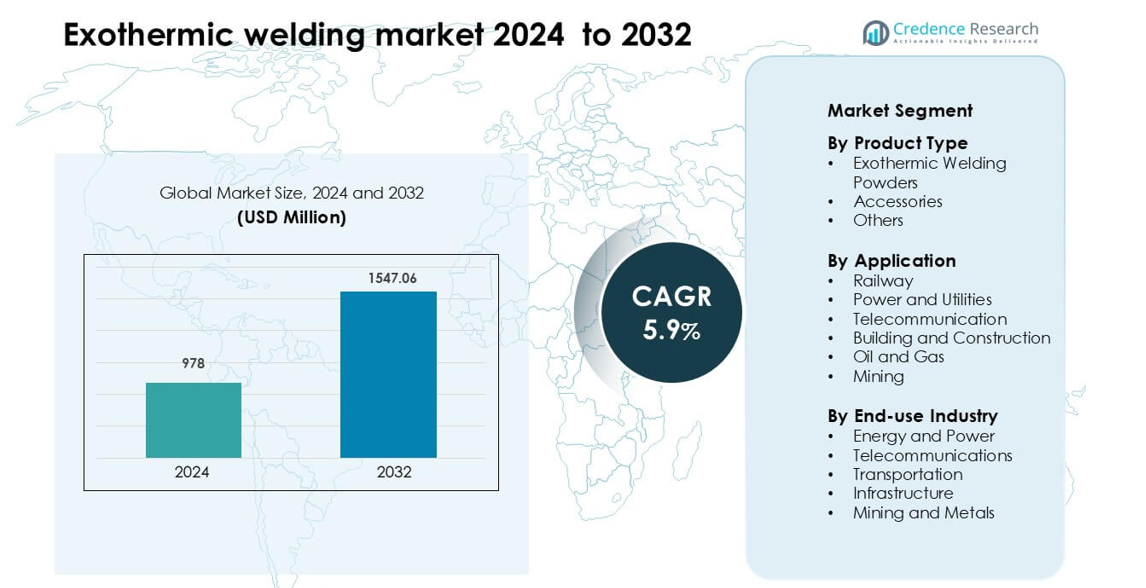

Exothermic welding market was valued at USD 978 million in 2024 and is anticipated to reach USD 1547.06 million by 2032, growing at a CAGR of 5.9 % during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Exothermic Welding Market Size 2024 |

USD 978 million |

| Exothermic Welding Market, CAGR |

5.9% |

| Exothermic Welding Market Size 2032 |

USD 1547.06 million |

The exothermic welding market features several prominent players, including nVent, Hubbell, Harger, EXOWELD, Tectoweld, Aplicaciones Tecnológicas S.A., ALLTEC, ESTWELD, Amiable Impex, Huadian Lightning Protection, Kumwell, Ningbo Banghe New Materials, A. N. Wallis and Co., and Shandong Fullworld. These companies compete through innovations in welding powders, mold design, and safety-enhanced ignition systems while expanding their distribution networks to strengthen global reach. North America leads the market with a commanding 35% share, driven by strong utility infrastructure, widespread renewable energy deployment, and strict grounding standards that accelerate adoption across industrial, telecom, and transportation applications.

Market Insights

- The global exothermic welding market is valued at USD 978 million and is projected to grow at a CAGR of 5.9% driven by rising infrastructure modernization and safety-critical bonding requirements.

- Strong demand comes from utilities, railways, telecom, and construction sectors, with exothermic welding powders holding the largest segment share at 55% due to their reliability and long-life conductivity.

- Key trends include the adoption of smokeless powders, portable ignition systems, reusable molds, and growing use in renewable energy, 5G rollout, metro expansion, and smart-grid projects.

- The market remains moderately competitive with players such as nVent, Hubbell, Harger, Tectoweld, and A. N. Wallis investing in material innovation, safety enhancements, and technician-training programs; however, availability of mechanical connectors and skilled labor shortages act as restraints.

- North America leads with 35% regional share, followed by Europe at 25% and Asia-Pacific at 28%, supported by large-scale grid upgrades, railway electrification, telecom expansion, and industrial development.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Product Type

Exothermic welding powders dominate the product type segment with an estimated over 55% market share, driven by their critical role in forming high-strength, corrosion-resistant permanent connections across grounding and bonding applications. Their reliability in harsh environmental conditions and compatibility with diverse metals accelerates adoption across industries that demand long-life electrical joints. Accessories, including molds, clamps, and ignition systems, support recurring demand but represent a smaller share. The Others category grows steadily as manufacturers introduce advanced refill kits and eco-efficient ignition tools to enhance operational efficiency and safety.

- For instance, nVent’s ERICO Cadweld process has been used to make more than 150 million exothermic welded connections since its invention.

By Application

Railway applications hold the dominant share at around 30%, fueled by extensive use of exothermic welding for rail track bonding, signal grounding, and traction power connections. The method’s ability to deliver vibration-resistant and maintenance-free joints strengthens its role in large-scale rail modernization and electrification projects. Power and utilities, telecommunications, and building and construction segments show steady growth as utilities upgrade earthing networks to meet grid-stability requirements. Oil and gas and mining industries contribute additional demand as operators prioritize durable bonding solutions for high-temperature and corrosive environments.

- For instance, KLK Weld’s ELPA procedure achieves electrical resistance of less than 10⁻⁵ Ω when welding copper cables (10 mm² to 240 mm²) to the rail foot, and its molds endure at least 70 welds per graphite mold.

By End-use Industry

The energy and power sector leads with nearly 35% market share, supported by continuous upgrades of transmission, distribution, and substation grounding systems. Exothermic welding’s superior conductivity and long service life make it the preferred method for fault-current management and grid safety, driving its widespread adoption. Telecommunications follows closely as network expansion and 5G infrastructure intensify the need for robust grounding. Transportation and infrastructure sectors generate sustained demand, particularly in rail, metro, and smart-city installations, while mining and metals rely on the technology for reliable bonding in high-load, high-corrosion sites.

Key Growth Drivers

Growing Emphasis on Electrical Safety and Reliable Grounding Systems

The exothermic welding market expands rapidly as industries intensify their focus on electrical safety, grounding reliability, and long-term conductivity. Modern power distribution networks, renewable energy sites, and industrial facilities increasingly rely on exothermic welding to create permanent molecular bonds with superior resistance to corrosion, thermal shocks, and mechanical stresses. Standards issued by regulatory bodies and safety agencies promote the use of exothermic welding over mechanical connectors, especially in environments exposed to lightning, fault currents, and high soil resistivity. Utilities and critical infrastructure operators prefer exothermic joints because they eliminate loosening or failure risks, lowering maintenance costs over a system’s life cycle. As electrification accelerates across transportation, industrial automation, and urban infrastructure, demand for dependable grounding and bonding solutions continues to drive the adoption of exothermic welding globally.

- For instance, HEXWELD exothermic welds from HEX Worldwide are certified to IEEE 837 and deliver the lowest possible earth path resistance, maintaining stable resistance even after repeated fault current cycles.

Rapid Expansion of Railway, Metro, and Transportation Infrastructure

Railway modernization and the global expansion of metro networks significantly propel the exothermic welding market. Rail operators use exothermic welding extensively for track bonding, signal grounding, traction power distribution, and return current continuity—areas where joint reliability is crucial for operational safety. Governments across emerging economies increase investments in high-speed rail, urban transit, and freight corridors, creating large-scale, recurring demand for high-strength electrical connections. Exothermic welding eliminates risks associated with vibration loosening, making it ideal for rail environments subjected to frequent shock loads. Electrification initiatives in Asia, Europe, and the Middle East also boost the need for superior grounding networks. Additionally, digital signaling and automation (CBTC, ETCS) intensify requirements for interference-free bonding, further accelerating the adoption of exothermic welding solutions in transportation ecosystems.

- For instance, The CADWELD system, specifically the nVent ERICO Cadweld One Shot product line, is widely used in railway applications globally for permanent, high-quality exothermic connections for cable-to-rail and cable-to-rebar connections.

Expansion of Renewable Energy and Utility Grid Modernization Projects

The shift toward renewable energy, distributed power generation, and utility grid upgrades acts as a major growth catalyst for the exothermic welding market. Solar farms, wind parks, substations, and battery energy storage systems require robust earthing networks to protect equipment from surge events, lightning, and ground faults. Exothermic welding offers long-term stability in remote, corrosive, or high-moisture environments where mechanical connectors commonly degrade. Utilities increasingly replace aging grounding systems in transmission and distribution infrastructure, reinforcing the need for permanent, maintenance-free bonding. As smart grids integrate advanced monitoring systems, grounding reliability becomes even more critical to maintaining power flow continuity. The rising installation of EV charging stations, microgrids, and hybrid renewable systems further strengthens demand for exothermic welding as a preferred method for ensuring electrical continuity and safety.

Key Trends & Opportunities

Increased Automation and Portable Welding Innovations

Technology advancements create significant opportunities as manufacturers introduce automated molds, portable ignition systems, and safer handling mechanisms for exothermic welding. Compact and reusable molds reduce operational time and improve consistency, especially for field technicians working in remote or constrained environments. Innovations in smokeless or reduced-emission welding powders support compliance with occupational safety standards. Digital monitoring tools enabling real-time quality checks are emerging as value-added solutions for utilities and rail operators seeking traceable, error-free installations. These advancements allow companies to train technicians more efficiently, reduce operational risks, and expand adoption in industries that previously relied heavily on mechanical connectors.

- For instance, Amiable Impex’s XMold powder is engineered for clean combustion and is certified under ISO 9001 quality standards, with reaction temperatures reaching above 1,400 °C to ensure complete molecular bonding without excess fumes.

Expansion into Telecom, Smart City, and 5G Infrastructure Projects

The accelerating rollout of 5G networks, fiber-optic expansions, and smart-city infrastructure presents significant growth opportunities for exothermic welding providers. Telecom towers, data centers, IoT hubs, and underground fiber networks require reliable grounding to protect sensitive electronic equipment from surges and electromagnetic interference. Exothermic connections offer superior conductivity and longevity compared to bolted or crimped joints, making them preferred for high-density digital infrastructure. As governments invest in resilient urban networks and digital connectivity, demand rises for grounding solutions that ensure uninterrupted service performance. Increasing deployments of edge computing nodes and distributed small-cell sites further expand adoption across the telecom ecosystem.

- For instance, nVent ERICO grounding systems used in telecom installations across over 100 countries feature CADWELD bonds tested to carry fault currents exceeding 30 kA, ensuring protection for 5G and fiber-optic installations.

Key Challenges

Safety Risks and Skilled Labor Requirements

Despite its advantages, exothermic welding poses operational challenges due to safety risks associated with high-temperature reactions and handling of reactive metal powders. The process requires trained personnel capable of managing molds, ignition systems, and on-site environmental conditions. Inadequate training increases the likelihood of burns, misfires, or substandard bonding, deterring some operators from adopting the technology. Many developing regions face shortages of certified technicians, slowing market penetration. The need for specialized safety gear and training programs also increases operational costs. Addressing these issues through automated solutions, improved packaging, and enhanced training remains essential to broadening market acceptance.

Availability of Alternative Bonding Technologies

The availability of mechanical connectors, compression lugs, and advanced crimping technologies poses a competitive challenge to exothermic welding. These alternatives attract buyers seeking faster installation, minimal training requirements, and reduced safety concerns. In industries with rapid deployment needs such as temporary installations or small-scale grounding mechanical connectors may be preferred due to their simplicity. Additionally, advancements in corrosion-resistant materials and coated connectors increase competition. Some operators hesitate to adopt exothermic welding due to the need for consumables and mold maintenance. Overcoming this challenge requires continuous product innovation, education on long-term performance benefits, and targeted marketing highlighting lifecycle cost advantages.

Regional Analysis

North America

North America accounts for the largest share of the exothermic welding market, holding around 35%, supported by strong utility infrastructure, extensive rail networks, and stringent grounding safety regulations. Utilities continue upgrading transmission and distribution grids, driving consistent demand for long-life bonding solutions. The U.S. leads adoption due to expanding renewable energy installations, substation modernization, and rapid deployment of EV charging infrastructure. High awareness of electrical safety standards and widespread use of exothermic welding in telecommunications and industrial facilities strengthen regional dominance, while ongoing smart-grid and metro expansion projects further reinforce market growth.

Europe

Europe captures approximately 25% of the global market, driven by large-scale railway electrification, metro expansions, and strict regulatory frameworks for grounding and bonding. Countries such as Germany, France, and the U.K. adopt exothermic welding extensively in transportation, renewable energy, and industrial automation sectors. The region’s aggressive transition toward renewable energy—particularly wind and solar—supports increased installation of durable grounding systems. Upgrades to aging power grids and adoption of digital substations accelerate demand. Additionally, growing 5G deployment and smart-city initiatives across Western and Northern Europe create new opportunities for high-performance exothermic bonding solutions.

Asia-Pacific (APAC)

Asia-Pacific represents the fastest-growing region, holding around 28% market share, fueled by rapid urbanization, extensive railway development, and massive investments in power and telecom infrastructure. Countries such as China, India, and Japan expand metro networks, high-speed rail, and industrial zones, significantly increasing demand for reliable grounding systems. Large-scale renewable energy projects—including solar parks and offshore wind farms—further strengthen adoption. Growing 5G rollouts and expansion of data centers intensify requirements for corrosion-resistant, maintenance-free joints. Favorable government programs promoting infrastructure modernization position APAC as a key future growth engine for the exothermic welding market.

Middle East & Africa (MEA)

MEA accounts for around 7–8% of the global market, supported by expanding oil and gas operations, utility upgrades, and large infrastructure developments. The region’s harsh climatic conditions—high salinity, temperature extremes, and corrosion—drive preference for exothermic welding due to its long-term durability. GCC nations invest heavily in smart-grid technologies, renewable energy clusters, and rail projects such as the GCC Railway, increasing adoption. In Africa, growth is driven by electrification initiatives and telecom network expansion. Although market penetration remains lower than in other regions, rising industrial investments are strengthening long-term demand.

Latin America

Latin America holds around 6–7% market share, with growth supported by upgrades in power distribution, mining expansion, and telecom modernization. Countries such as Brazil, Mexico, and Chile invest in renewable energy, grid stabilization, and digital connectivity projects, driving the need for reliable grounding and bonding solutions. The mining industry, particularly in Chile and Peru, relies on exothermic welding for corrosion-resistant electrical joints in high-load environments. Infrastructure expansion, including metro systems and industrial parks, further supports adoption. While budget constraints and slow regulatory alignment influence growth, rising investment in utilities and telecom accelerates market opportunities.

Market Segmentations:

By Product Type

- Exothermic Welding Powders

- Accessories

- Others

By Application

- Railway

- Power and Utilities

- Telecommunication

- Building and Construction

- Oil and Gas

- Mining

By End-use Industry

- Energy and Power

- Telecommunications

- Transportation

- Infrastructure

- Mining and Metals

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The competitive landscape of the exothermic welding market features a mix of global leaders and specialized regional manufacturers competing on product quality, safety, customization, and material innovation. Companies such as nVent, Hubbell, Harger, and A. N. Wallis and Co. maintain strong market positions through extensive distribution networks, broad product portfolios, and established credibility in grounding and bonding applications. Mid-sized players like EXOWELD, Tectoweld, ESTWELD, and Kumwell compete by offering cost-effective solutions, localized support, and industry-specific product variants. Innovation focuses on smokeless powders, portable ignition tools, reusable molds, and enhanced safety mechanisms to meet evolving regulatory and utility standards. Strategic partnerships with utilities, telecom operators, and railway authorities strengthen market presence, while manufacturers increasingly invest in training programs to address skilled labor shortages. Overall, competition intensifies as companies prioritize durability, ease of installation, and lifecycle reliability to differentiate their offerings in a performance-driven market.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Tectoweld

- Kumwell

- N. Wallis and Co

- Amiable Impex

- Shangdong Fullworld

- Huadian Lightning Protection

- nVent

- EXOWELD

- ESTWELD

- ALLTEC

- Aplicaciones Tecnológicas S.A.

- Ningbo Banghe New Materials

- Hubbell

- Harger

Recent Developments

- In September 2025, A. N. Wallis & Co Ltd exhibited at Solar & Storage Live UK 2025 at NEC Birmingham, promoting its Cu-nnect exothermic welding range alongside earthing, lightning protection, and surge protection solutions, reinforcing its role as a key exothermic welding supplier to the renewables and power sectors.

- In January 2024, Kumwell released its Exothermic Welding Product Catalog EXO01/2024, a refreshed technical catalog detailing graphite moulds, weld metal powders, tools, and one-time welding kits, aligned with UL 467 and IEEE 837 testing requirements; access is promoted through a dedicated registration form titled Catalogue Exothermic Welding 2024.

Report Coverage

The research report offers an in-depth analysis based on Product Type, Application, End-Use Industry and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will see rising adoption as utilities modernize grids and strengthen grounding systems for higher reliability.

- Railway electrification, metro expansion, and high-speed rail projects will continue driving long-term exothermic welding demand.

- Renewable energy installations will increasingly rely on exothermic bonding for durable grounding in solar, wind, and storage projects.

- Telecom networks and 5G infrastructure will accelerate usage due to the need for stable, corrosion-resistant earthing.

- Manufacturers will introduce safer, smokeless powders and advanced ignition tools to improve on-site efficiency.

- Automation and portable welding solutions will enhance consistency and reduce dependency on skilled labor.

- Demand will grow in harsh environments such as oil and gas, mining, and coastal regions where corrosion resistance is essential.

- Training programs and digital guidance tools will expand to support workforce readiness.

- Competition will intensify as more players develop modular, reusable mold systems.

- Asia-Pacific will emerge as the fastest-growing region due to infrastructure megaprojects and large-scale industrial expansion.