Global Inhaled Nitric Oxide (iNO) Delivery Systems Market Overview:

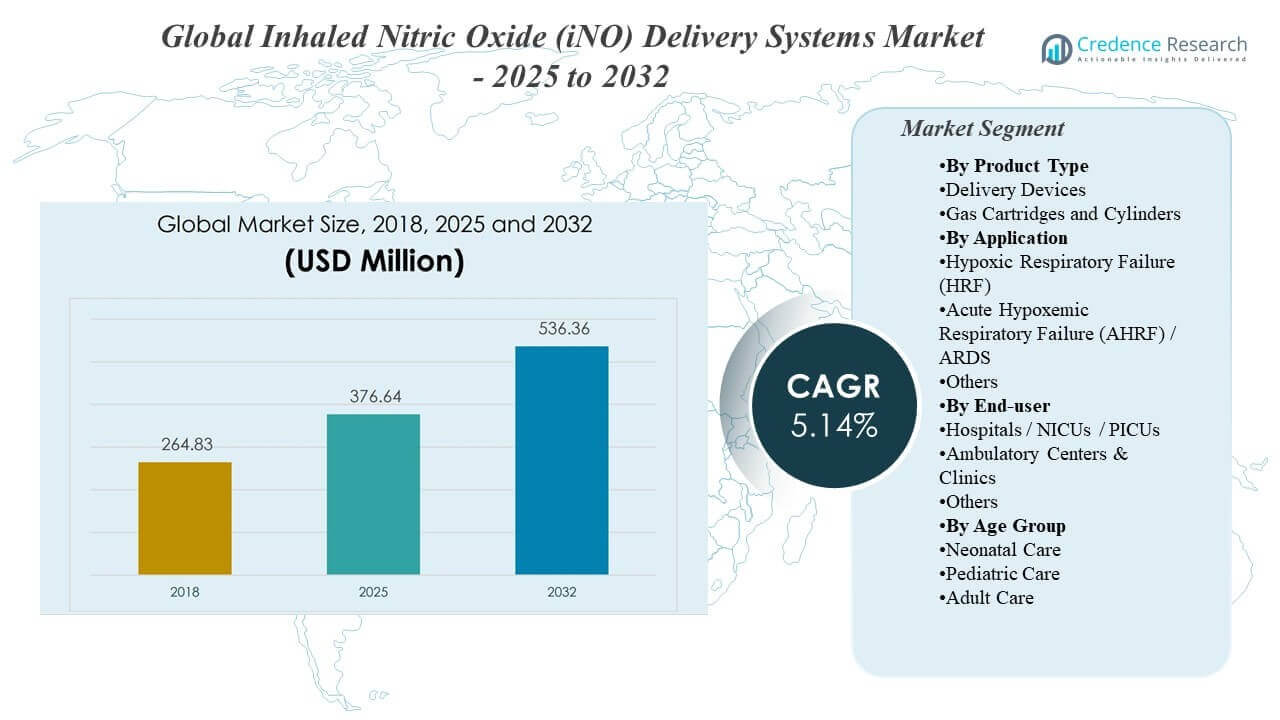

The Global Inhaled Nitric Oxide (iNO) Delivery Systems Market was valued at USD 264.83 million in 2018, reached USD 376.64 million in 2025, and is projected to grow to USD 536.36 million by 2032, expanding at a 5.14% CAGR during 2025–2032. Hospital-based critical care usage remains the strongest demand anchor because inhaled nitric oxide therapy is typically initiated, titrated, and monitored in controlled ICU and NICU environments that require compatible delivery hardware, trained respiratory teams, and continuous gas monitoring. Growth momentum is also supported by rising utilization outside neonatal-only pathways as intensive care protocols, device portability, and workflow integration improve across more sites.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Inhaled Nitric Oxide (iNO) Delivery Systems Market Size 2025 |

USD 376.64 million |

| Inhaled Nitric Oxide (iNO) Delivery Systems Market, CAGR |

5.14% |

| Inhaled Nitric Oxide (iNO) Delivery Systems Market Size 2032 |

USD 536.36 million |

Key Market Trends & Insights

- The market is projected to expand from USD 376.64 million (2025) to USD 536.36 million (2032), reflecting a 5.14% CAGR (2025–2032).

- Pediatric care represented the leading age-group demand with 74.3% share in 2025, reflecting the strong clinical reliance on iNO therapy in neonatal and pediatric respiratory pathways.

- Hospitals / NICUs / PICUs accounted for the largest end-user share at 78.9% in 2025, supported by monitoring requirements and ventilator-integrated administration workflows.

- Hypoxic Respiratory Failure (HRF) led application demand with 47.1% share in 2025, reinforced by established care protocols and dosing weaning practices in acute settings.

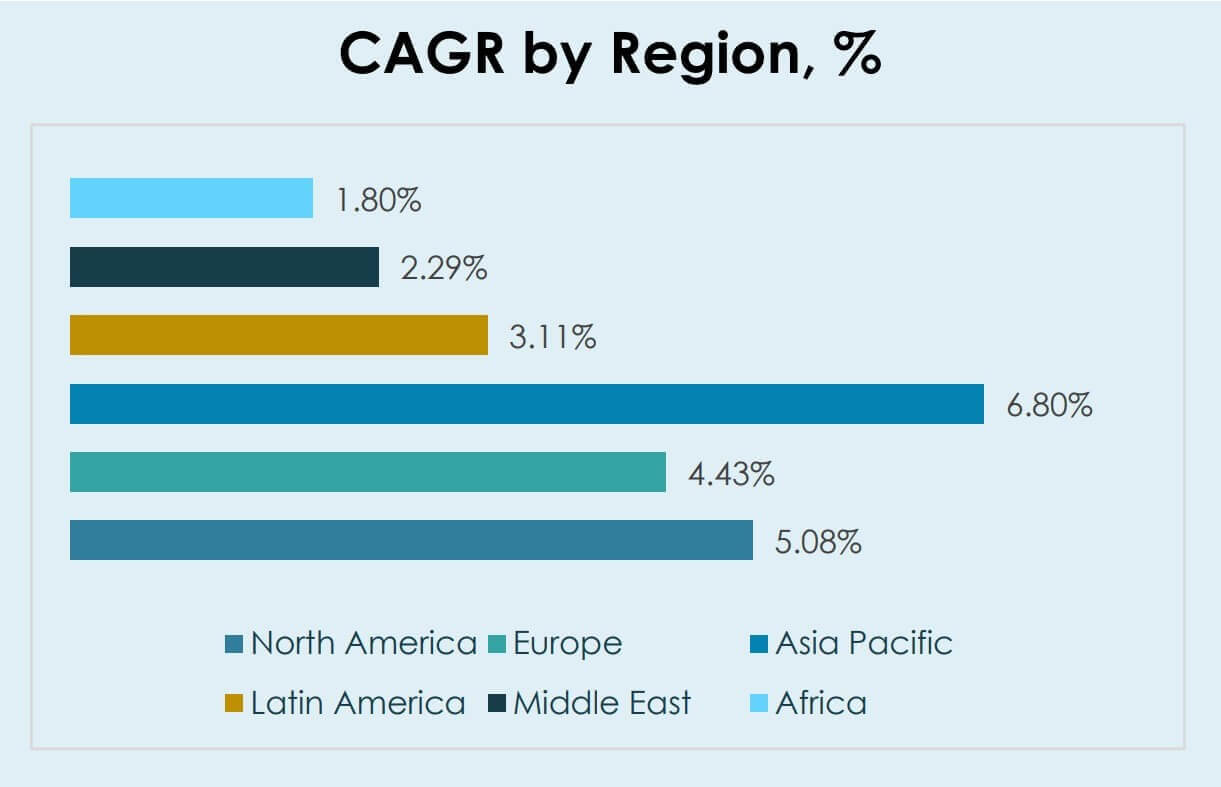

- Asia Pacific is positioned as the fastest-growing region with 6.80% CAGR (2025–2032), outpacing North America (5.08%) and Europe (4.43%) over the same period.

Segment Analysis

Demand for Global Inhaled Nitric Oxide (iNO) Delivery Systems Market solutions remains concentrated in high-acuity respiratory care settings where continuous dosing control, gas monitoring, and ventilator compatibility are essential. Clinical pathways in neonatal and pediatric respiratory failure keep utilization structurally supported, and procurement decisions often prioritize safety interlocks, reliability of dose delivery, and ease of integration into existing respiratory circuits. Recurrent consumable usage and service needs also influence total cost of ownership considerations, particularly for high-volume centers.

Product configuration preferences often reflect a balance between installed workflow familiarity and operational efficiency requirements. Facilities with established ICU and NICU protocols tend to value standardized delivery approaches that reduce setup time and simplify staff training. Adoption of improved delivery designs is also tied to portability needs, maintenance burden, and the ability to support consistent dosing across different ventilator modes and patient profiles.

By Product Type Insights

Gas Cartridges and Cylinders held the leading position in 2025 due to widespread legacy workflows that rely on standardized gas supply and familiar handling procedures in ICU environments. Gas supply formats support recurring purchasing patterns because therapy setup and replenishment requirements create consistent demand across high-volume centers. Infection-control and standardization priorities also encourage the use of compatible consumables that align with established respiratory circuits. Delivery Devices benefit from ongoing innovation tied to workflow simplification and portability, especially for sites seeking easier deployment and monitoring integration.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Application Insights

Hypoxic Respiratory Failure (HRF) accounted for the largest share of 47.1% in 2025. HRF pathways in neonatal and pediatric care support sustained utilization because therapy initiation and titration are closely protocolized and monitored in NICU settings. HRF management often involves continuous observation and structured weaning, which increases delivery-system utilization per case. Acute Hypoxemic Respiratory Failure (AHRF) / ARDS demand is supported by broader critical-care caseloads and evaluation of iNO use in severe hypoxemia management where monitoring and dosing control remain central.

By End-user Insights

Hospitals / NICUs / PICUs accounted for the largest share of 78.9% in 2025. Hospital settings remain dominant because iNO therapy requires ventilator integration, real-time monitoring, and rapid escalation capability that aligns with ICU infrastructure and staffing. Concentration of eligible neonatal and pediatric cases in NICUs and PICUs also increases utilization intensity in hospital environments. Ambulatory Centers & Clinics remain smaller but continue to gain relevance where simplified delivery workflows and care decentralization expand the feasible settings for therapy initiation and monitoring.

By Age Group Insights

Pediatric Care accounted for the largest share of 74.3% in 2025. Pediatric and neonatal pathways continue to anchor demand because clinical value is well-established in specific respiratory failure and pulmonary hypertension-related management workflows that are tightly monitored. High-acuity pediatric care settings support adherence to dosing, monitoring, and safety requirements that shape device selection and replacement cycles. Adult Care growth is influenced by critical-care adoption dynamics and the expansion of severe respiratory management protocols that require consistent dose delivery and compatibility with ICU respiratory equipment.

Inhaled Nitric Oxide Delivery Systems Market Drivers

Expansion of NICU/PICU respiratory care capacity and protocolized therapy use

Growth in neonatal and pediatric critical care capacity increases the number of sites capable of administering and monitoring iNO therapy. Clinical pathways for severe hypoxemia and related conditions often require controlled dosing and continuous monitoring, supporting steady utilization of delivery systems. Standardized protocols encourage repeatable workflows that increase device use per eligible patient episode. Procurement also favors systems that reduce setup errors and support consistent dosing performance across different ventilator configurations.

- For instance, Mallinckrodt’s INOmax EVOLVE DS combines the primary delivery system, monitoring system, 2 cylinder bays, an electronic blender, and backup systems in a single enclosure, while each 0.4-L mini-cylinder weighs 1.43 lb, contains 4,880 ppm INOmax, and is filled to 3,000 psig, supporting standardized setup and controlled dosing in neonatal critical-care workflows.

Installed base replacement and workflow modernization in hospitals

Hospitals maintain mixed fleets of respiratory equipment and often pursue modernization to improve safety features, monitoring integration, and operational reliability. Replacement cycles are shaped by lifecycle economics, service support, and the need to maintain uptime in high-acuity units. Standardization across ICU rooms and multi-site networks also increases demand for consistent delivery platforms that simplify training and reduce variability. Modern delivery features can reduce clinician burden and improve consistency across care teams.

- For instance, VERO Biotech’s GENOSYL DS uses a 16.0-lb console and a 1.0-lb single-use cassette, supports dose settings from 1 to 80 ppm, and is configured with two fully redundant delivery consoles, features that directly support portability, system standardization, and uptime in high-acuity environments.

Recurring demand for consumables, cartridges, and supply-chain continuity

Consumable and supply components are repeatedly required for therapy setup, ongoing administration, and maintenance of consistent workflows. High-volume centers generate recurring purchasing patterns that support stable revenue streams across gas and accessory categories. Supply reliability becomes a key decision factor because any interruption can disrupt ICU protocols and patient management. As a result, vendor selection often emphasizes availability, support response, and compatibility with existing respiratory circuits.

Broader critical-care use cases and monitoring-led adoption in severe hypoxemia care

Critical-care teams continue to evaluate iNO delivery in severe hypoxemia management where rapid response and continuous monitoring are required. Adoption is supported by improved monitoring capabilities, safety interlocks, and workflow integration that reduce variability in dose delivery. As severe respiratory caseloads remain structurally present across hospitals, demand for reliable delivery systems stays supported in many regions. Clinical familiarity and staff training investments also help sustain utilization where protocols are established.

Inhaled Nitric Oxide Delivery Systems Market Challenges

Cost sensitivity and procurement constraints remain a limiting factor, particularly in regions where ICU budgets are tight and therapy adoption depends on reimbursement and hospital funding cycles. Delivery systems must compete for capital budgets alongside ventilators, monitoring systems, and other respiratory equipment, which can lengthen purchase timelines and slow upgrades. In addition, hospitals often prioritize multi-purpose critical-care equipment first, delaying dedicated iNO delivery investments unless clinical volumes clearly justify the spend.

- For instance, Beyond Air’s LungFit PH generates nitric oxide from room air instead of cylinders, delivers 0.1–80 ppm across a 0.5–100 L/min flow range, and includes an independent backup flow of 1 L/min at 220 ppm.

Operational complexity also creates barriers to broader adoption because safe administration requires trained staff, ventilator compatibility, and reliable monitoring of delivered dose. Variability across respiratory equipment and site-specific protocols can increase integration effort, which can limit expansion into lower-acuity settings. Supply continuity for gas and consumables can further influence adoption decisions, especially for multi-site networks that prioritize predictable logistics. These factors raise total cost of ownership concerns and can lead to preference for simpler systems with stronger service and supply assurances.

Market Trends and Opportunities

Portability and workflow simplification are becoming more important as care delivery shifts across distributed networks and hospitals seek standardization with lower training burden. Systems that reduce setup steps, improve monitoring clarity, and integrate smoothly into existing respiratory workflows are increasingly favored. These priorities support opportunities for device upgrades and broader penetration within hospital groups that want consistent performance across sites. Vendors that reduce setup time and enable faster clinician adoption can gain share in upgrade-driven tenders.

- For instance, Hamilton Medical’s HAMILTON‑T1 transport ventilator weighs 6.5 kg, provides up to 8 hours of battery operation with two batteries, and is built around the company’s common user-interface approach across ventilator settings, which supports easier standardization from bedside care to transport use cases.

Digital integration and data capture are strengthening purchasing criteria as hospitals increase focus on monitoring, auditability, and protocol compliance. Devices that support reliable tracking of delivered dose, alarms, and therapy history align with safety and quality initiatives in critical care. These trends expand opportunities for vendors that can provide integrated service models and workflow-aligned device ecosystems. Interoperability with hospital IT systems and remote service diagnostics can further differentiate suppliers as hospitals scale connected care infrastructure.

Regional Insights

North America

North America is expected to grow at a 5.08% CAGR during 2025–2032, supported by established ICU and NICU therapy protocols and higher penetration of advanced respiratory monitoring practices. Hospital procurement in North America often prioritizes dosing reliability, workflow integration, and service support, which sustains replacement and upgrade activity. Continued emphasis on standardization across hospital systems supports demand for compatible delivery platforms and accessories.

Europe

Europe is projected to expand at a 4.43% CAGR from 2025 to 2032, reflecting steady adoption supported by hospital modernization initiatives and protocol-driven critical care pathways. Procurement in Europe tends to be more price-sensitive, increasing emphasis on lifecycle value, uptime, and maintenance efficiency. Standardization across public and private hospital networks also supports demand for consistent delivery workflows.

Asia Pacific

Asia Pacific is forecast to register the fastest growth with a 6.80% CAGR over 2025–2032, driven by expansion of critical care capacity, increasing access to advanced respiratory management, and broader availability of specialized neonatal and pediatric services. Hospital infrastructure buildout and rising clinical capabilities support adoption of iNO delivery systems where eligible patient volumes rise. Growth also benefits from modernization of respiratory care workflows in expanding hospital networks.

Latin America

Latin America is expected to grow at a 3.11% CAGR between 2025 and 2032, with adoption influenced by unequal ICU infrastructure distribution and budget constraints across healthcare systems. Demand remains concentrated in tertiary hospitals and leading neonatal centers where monitoring and specialist staffing are available. Supply continuity and affordability continue to shape procurement decisions, limiting rapid expansion in lower-resourced settings.

Middle East & Africa

Middle East growth is projected at a 2.29% CAGR (2025–2032) and Africa growth is projected at a 1.80% CAGR (2025–2032), reflecting slower expansion tied to uneven ICU capacity, constrained budgets, and variable access to specialized respiratory care. Demand is largely concentrated in higher-capability centers that can support safe administration and monitoring. Procurement decisions often emphasize reliability of supply, service availability, and compatibility with existing ICU respiratory equipment.

Competitive Landscape

Competition in the Global Inhaled Nitric Oxide (iNO) Delivery Systems Market is shaped by system reliability, dosing precision, safety interlocks, and compatibility with ICU ventilator environments. Vendors differentiate through workflow integration, portability, monitoring interfaces, and service responsiveness that supports uptime in high-acuity care. Hospital buyers commonly evaluate total cost of ownership across consumables, maintenance, and training burden, which elevates the importance of scalable service models and supply reliability.

Mallinckrodt Pharmaceuticals is positioned around established clinical presence and the ability to support hospital workflows that require consistent dosing performance and strong customer support. Portfolio evolution and delivery-system enhancements support continuity across installed base environments and help address hospital priorities around standardization and safety. Commercial positioning also benefits from relationships across critical care stakeholders and the ability to align delivery systems with protocol-driven ICU and NICU use.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Mallinckrodt Pharmaceuticals

- VERO Biotech

- Linde plc.

- Beyond Air Inc.

- Air Liquide Healthcare

- International Biomedical, Inc.

- Messer Medical (Messer Group GmbH)

- Matheson Tri-Gas

- Novlead Biotechnology Co., Ltd.

- SOL Spa

- Others

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In February 2025, Linde Gas & Equipment, part of Linde plc, announced the submission of a 510(k) application to the U.S. FDA for NOXBOX I PLUS, a nitric oxide delivery and monitoring system for NOXIVENT, positioning it as a new product advancement in this market.

- In March 2025, Beyond Air Inc. also announced a partnership with Vanderbilt University Medical Center, which became the first luminary site for LungFit PH to help evaluate and showcase the clinical and operational benefits of its tankless inhaled nitric oxide technology.

- In June 2025, Beyond Air announced the submission of an FDA PMA supplement for LungFit PH II, a next-generation version of its nitric oxide delivery system. The company said LungFit PH II is smaller, lighter, transport-ready, and designed using feedback from respiratory therapists, with the goal of expanding use across more care settings.

- In Nov 2025, Linde plc. addressed performance-related correction actions associated with a nitric oxide delivery system under specific operating conditions. This development matters because ventilator compatibility and dose stability remain core safety requirements that directly influence hospital purchasing decisions and protocol confidence.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 376.64 million |

| Revenue forecast in 2032 |

USD 536.36 million |

| Growth rate (CAGR) |

5.14% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026–2032 |

| Quantitative units |

USD million |

| Segments covered |

By Product Type, By Application, By End-user, By Age Group |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Mallinckrodt Pharmaceuticals; VERO Biotech; Linde plc.; Beyond Air Inc.; Air Liquide Healthcare; International Biomedical, Inc.; Messer Medical (Messer Group GmbH); Matheson Tri-Gas; Novlead Biotechnology Co., Ltd.; SOL Spa; Others companies |

| No. of Pages |

328 |

Segmentation

By Product Type

- Delivery Devices

- Gas Cartridges and Cylinders

By Application

- Hypoxic Respiratory Failure (HRF)

- Acute Hypoxemic Respiratory Failure (AHRF) / ARDS

- Others

By End-user

- Hospitals / NICUs / PICUs

- Ambulatory Centers & Clinics

- Others

By Age Group

- Neonatal Care

- Pediatric Care

- Adult Care

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa