Market Overview

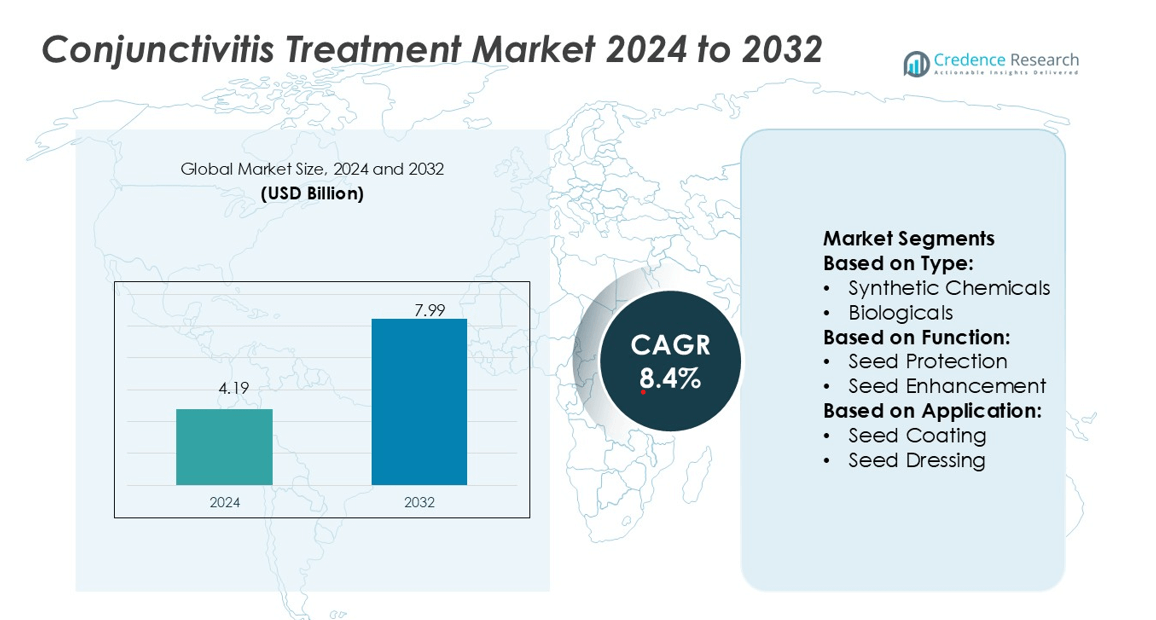

Conjunctivitis Treatment Market size was valued USD 4.19 billion in 2024 and is anticipated to reach USD 7.99 billion by 2032, at a CAGR of 8.4% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Conjunctivitis Treatment Market Size 2024 |

USD 4.19 billion |

| Conjunctivitis Treatment Market CAGR |

8.4% |

| Conjunctivitis Treatment Market Size 2032 |

USD 7.99 billion |

The conjunctivitis treatment market is characterized by strong competition among major players including Alcon, Allergan, Bausch + Lomb, Santen Pharmaceutical, Pfizer, Johnson & Johnson Vision, Novartis, Sun Pharmaceutical, Roche, and Teva Pharmaceuticals. These companies focus on innovative formulations, preservative-free products, and advanced combination therapies to enhance treatment effectiveness and patient adherence. Strategic alliances with healthcare providers and digital platforms strengthen their global reach and product availability. Asia Pacific leads the market with a 34% share, supported by rising urbanization, growing awareness, and improved healthcare infrastructure. This regional dominance is reinforced by expanding retail pharmacy networks, increasing R&D investments, and government-led eye health programs.

Market Insights

- The Conjunctivitis Treatment Market was valued at USD 4.19 billion in 2024 and is projected to reach USD 7.99 billion by 2032, growing at a CAGR of 8.4%.

- Rising allergy cases, pollution exposure, and increased awareness of eye health are driving strong demand across both developed and emerging economies.

- Companies are focusing on preservative-free drops, combination therapies, and teleophthalmology integration to strengthen market presence and patient access.

- Limited access to advanced formulations in low-income regions and rising antibiotic resistance continue to restrain faster market growth.

- Asia Pacific leads with a 34% regional share, supported by improved healthcare infrastructure, while OTC products remain the dominant segment, reflecting a growing preference for self-care solutions.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Type

Synthetic chemicals dominate the conjunctivitis treatment market, accounting for the largest market share. These products provide quick symptom relief and are widely used in both prescription and over-the-counter formulations. Broad availability, cost-effectiveness, and proven efficacy in treating bacterial conjunctivitis support strong demand. Antibiotic eye drops and anti-inflammatory agents are key contributors to growth. Biologicals are gaining momentum, but their higher cost limits adoption compared to synthetic drugs. Expanding awareness and clinical usage drive market penetration across hospitals, pharmacies, and clinics globally.

- For instance, Koppert developed its “Mirical” release system using corrugated cardboard strips that reduce plastic use by 99%, while improving insect delivery survival in transport.

By Function

Seed protection holds the largest market share in conjunctivitis treatment, focusing on preventing secondary infections and reducing inflammation. Antibacterial and antiviral properties help protect the ocular surface, ensuring faster recovery. These formulations lower recurrence rates, which makes them a preferred choice among physicians and patients. Seed enhancement, including lubricating and soothing formulations, is growing steadily. Rising cases of viral conjunctivitis and increased use of preservative-free drops support this segment. Continuous improvements in formulation stability and safety further strengthen its market position.

- For instance, Plant Health Care announced that sales of its PREtec peptides had increased by 153% to 2.0 million compared 18% of total group revenue: The same financial report for FY23 confirmed that PREtec sales accounted for 18% of the total group revenue for that year.

By Application

Seed coating is the dominant application technique, securing the largest market share in conjunctivitis treatment delivery. Eye drops and ointments are easy to administer, provide targeted relief, and support rapid patient compliance. Their wide availability across pharmacies and clinics strengthens market reach. Seed dressing methods, such as wipes and gels, are growing due to better comfort and hygiene benefits. Seed pelleting, including sustained-release inserts, remains a niche segment but is expanding with innovation in ocular drug delivery technologies.

Key Growth Drivers

Rising Prevalence of Allergic and Infectious Conjunctivitis

Increasing exposure to allergens, pollution, and seasonal triggers is driving higher infection rates. Urban populations are more prone to eye irritation and allergic reactions, boosting demand for fast-acting treatments. Healthcare systems are expanding screening programs to detect cases early. Pharmaceutical companies are investing in antihistamines, anti-inflammatory drugs, and antibiotic combinations. For example, Alcon’s Pataday Once Daily Relief has gained wider use due to its strong efficacy and quick relief. This rising burden of conjunctivitis cases strongly supports market expansion globally.

- For instance, Syngenta launched Cropwise AI / GenAI—a generative AI module added to enhance decision support for growers, integrating predictive analytics across more than 30 agronomic models.

Advancements in Drug Formulations and Delivery Systems

Innovations in drug delivery methods are improving treatment outcomes and patient compliance. Companies are developing preservative-free eye drops, sustained-release gels, and targeted antibiotics. These formulations reduce side effects, extend dosage intervals, and enhance comfort. For example, Novartis’ Ikervis uses cationic emulsion technology to ensure prolonged ocular surface coverage. Such developments increase product adoption among patients and clinicians. This shift toward innovative formulations boosts sales and encourages further R&D investment across the market.

- For instance, Bayer trials “ThryvOn Technology” across ≈ 60,000 acres to embed insect protection into crop tissues.Bayer’s precision digital farming tool, Climate FieldView, is active on > 250 million crop acres globally.

Expanding Access to Eye Care in Emerging Economies

Improved healthcare infrastructure and awareness campaigns are expanding access to eye care services in emerging regions. Governments and NGOs are supporting mass screening and subsidized treatment programs. The growth of retail pharmacies and e-commerce platforms enhances product availability. For instance, India’s National Programme for Control of Blindness is increasing early detection and treatment coverage. This rising accessibility accelerates diagnosis and drives strong demand for conjunctivitis medications in underserved areas.

Key Trends & Opportunities

Rising Demand for Over-the-Counter Eye Medications

Consumers are increasingly choosing OTC eye drops for quick relief from symptoms. Pharmacies and online platforms offer a wide range of antihistamines, lubricants, and decongestants. This trend reduces treatment delays and broadens the customer base. Major companies are focusing on branding, packaging, and patient education. For example, Bausch + Lomb’s OTC range has gained strong visibility in North American markets. This shift toward self-care creates growth opportunities for product diversification and retail expansion.

- For instance, BASF invests heavily in R&D to deliver breakthroughs that span many industries spent roughly 2,061 million on research and development.That same year, the company filed 1,159 new patents worldwide, with about 44.5% focused on sustainability innovations.

Growing Interest in Combination Therapies

Combination formulations that address multiple symptoms are gaining traction. These products help manage both allergic and bacterial infections efficiently. Physicians prefer such treatments for faster recovery and reduced prescription complexity. Companies are developing dual-action products that combine antihistamines and anti-inflammatories. For instance, Allergan’s dual-action drops offer relief from redness and itching in a single dose. This trend boosts product acceptance and supports strong revenue growth in developed and emerging markets.

- For instance, Croda’s Life Sciences arm is expanding its delivery systems for proteins, nucleic acids, and biologics: it holds a portfolio of over 2,000 lipids and polymers used as delivery agents.

Integration of Teleophthalmology and Digital Platforms

Teleophthalmology is expanding access to quick consultations and prescriptions. Digital platforms enable patients to receive care without visiting clinics. Many telehealth providers now offer conjunctivitis treatment with same-day delivery of eye drops. Companies are integrating AI-based diagnostic tools to speed up case evaluation. This digital shift lowers healthcare costs and improves patient convenience, creating new distribution and service opportunities in both urban and rural settings.

Key Challenges

Widespread Self-Medication and Misuse of Drugs

Many patients rely on OTC eye drops without proper diagnosis, which often leads to delayed treatment or complications. Misuse of steroid-based or antibiotic drops can worsen symptoms and promote resistance. Pharmacies often sell these products without prescriptions, increasing public health risks. This trend affects treatment effectiveness and slows the adoption of prescribed therapies. Regulatory bodies are tightening control, but the challenge remains widespread, especially in developing countries.

Rising Antibiotic Resistance in Bacterial Strains

Antibiotic resistance is becoming a critical challenge in treating bacterial conjunctivitis. Overuse and misuse of common antibiotics have reduced their effectiveness. Resistant strains demand more advanced and costly medications. This issue increases healthcare costs and complicates treatment protocols. Pharmaceutical companies are investing in next-generation antibiotics, but development is slow and expensive. Rising resistance pressures the market to adopt better stewardship programs and innovative treatment solutions.

Regional Analysis

North America

North America holds a 32% share of the conjunctivitis treatment market, supported by advanced healthcare infrastructure and strong product availability. High awareness of eye health and early diagnosis rates contribute to steady market growth. The U.S. leads the region with robust sales of OTC and prescription eye drops. Companies like Alcon, Allergan, and Bausch + Lomb dominate through product innovation and retail distribution. Digital health platforms and teleophthalmology adoption further enhance patient access. Rising allergy prevalence and aging populations continue to drive sustained treatment demand across urban and rural areas.

Europe

Europe accounts for a 27% share of the conjunctivitis treatment market, driven by strong regulatory standards and widespread healthcare coverage. Countries like Germany, France, and the U.K. lead in treatment adoption due to well-established ophthalmology services. National health systems support quick diagnosis and prescription access, boosting pharmaceutical uptake. The region shows high demand for preservative-free and combination eye drops. Companies are expanding their distribution networks through retail and hospital pharmacies. Rising cases of seasonal allergic conjunctivitis also strengthen product demand, especially during peak pollen seasons across Western and Central Europe.

Asia Pacific

Asia Pacific holds the largest 34% share of the conjunctivitis treatment market, driven by rising urbanization, pollution, and allergy exposure. Countries such as China, India, and Japan are major contributors due to their large populations and growing healthcare infrastructure. Governments and NGOs are actively promoting early eye care interventions, improving diagnosis rates. Expanding retail pharmacy networks and affordable generic drugs increase treatment accessibility. The region is witnessing growing investments from global and domestic pharmaceutical firms. High demand for OTC eye drops and combination therapies is further strengthening Asia Pacific’s dominant market position.

Latin America

Latin America represents a 4% share of the conjunctivitis treatment market, supported by improving access to eye care services and growing awareness campaigns. Brazil and Mexico lead the region, driven by expanding healthcare networks and rising patient awareness. Increasing prevalence of infectious conjunctivitis due to climatic conditions boosts medication demand. Many pharmaceutical companies are entering through retail pharmacy channels, improving availability. Government-led screening programs are gradually enhancing early diagnosis. While growth remains moderate, improving infrastructure and broader product access are expected to support steady regional expansion in the coming years.

Middle East & Africa

The Middle East & Africa region holds a 3% share of the conjunctivitis treatment market, driven by rising healthcare investments and increased patient awareness. Gulf countries like Saudi Arabia and the UAE are expanding ophthalmology services and pharmacy networks. Public health initiatives promote early detection of infectious and allergic conjunctivitis. However, limited access to advanced drug formulations in several African countries restrains faster growth. International companies are partnering with local distributors to strengthen market reach. Urban centers are showing rising demand for affordable OTC solutions, supporting gradual market penetration in the region.

Market Segmentations:

By Type:

- Synthetic Chemicals

- Biologicals

By Function:

- Seed Protection

- Seed Enhancement

By Application:

- Seed Coating

- Seed Dressing

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The conjunctivitis treatment market is shaped by strong competition among key players including Verdesian Life Sciences, Italpollina S.p.A., Koppert Biological Systems, Monsanto Company, Plant Health Care plc, Syngenta AG, Bayer CropScience, Precision Laboratories, LLC, Incotec, and BASF SE. The conjunctivitis treatment market is highly competitive, driven by rapid innovation and expanding product portfolios. Companies are investing in advanced formulations such as preservative-free drops and combination therapies to improve patient outcomes and comfort. Strategic collaborations with healthcare providers, pharmacies, and digital health platforms are enhancing product accessibility and distribution. Strong marketing efforts and patient education programs are increasing brand visibility and adoption rates. Firms are also focusing on regulatory approvals and fast-track product launches to gain a competitive edge. This intense competition encourages continuous R&D investments, ensuring broader treatment availability across global markets.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Verdesian Life Sciences

- Italpollina S.p.A.

- Koppert Biological Systems

- Monsanto Company

- Plant Health Care plc

- Syngenta AG

- Bayer CropScience

- Precision Laboratories, LLC

- Incotec

- BASF SE

Recent Developments

- In January 2025, UPL Corp announced the U.S. Environmental Protection Agency registration of ATROFORCE™ bionematicide, a new seed treatment for use in cotton to protect yield potential from a broad number of nematodes.

- In November 2024, Lallemand unveiled LalRise Shine DS Seed Treatment. This, a new seed treatment from Lallemand Plant Care for corn and dry bean growers. This is designed to improve root vigor and nutrient availability.

- In September 2024, Indigo Ag launched its ground-breaking CLIPS™ device. The device is an automatic hands-free system, which saves time, removes the hassle factor in the seed treatment process, and potentially upends standard biological seed treatment applications, offering customers a more efficient and reliable solution for applying biological seed treatment to reduce the opportunity for product exposure and eliminate manual steps, making it a must-have tool for us and our growers.

- In March 2023, Aquatech International partnered with Fluid Technology Solutions, Inc., a cutting-edge producer of sophisticated membranes and separation technologies. Together, they aim to develop next-generation solutions for enhanced brine concentration, advanced separation, and water reuse.

Report Coverage

The research report offers an in-depth analysis based on Type, Function, Application and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will see rising demand due to growing allergy and infection cases.

- Advanced drug delivery systems will improve treatment outcomes and patient comfort.

- Digital platforms and teleophthalmology will enhance access to timely care.

- OTC product expansion will boost self-care and retail sales.

- R&D investments will drive the launch of preservative-free and combination therapies.

- Regulatory support will accelerate approvals for innovative eye drop formulations.

- Pharmaceutical companies will expand distribution networks in emerging economies.

- Public health campaigns will increase awareness and early diagnosis rates.

- Market consolidation will strengthen the presence of leading brands.

- Technological integration will enhance personalized treatment approaches.