Market Overview

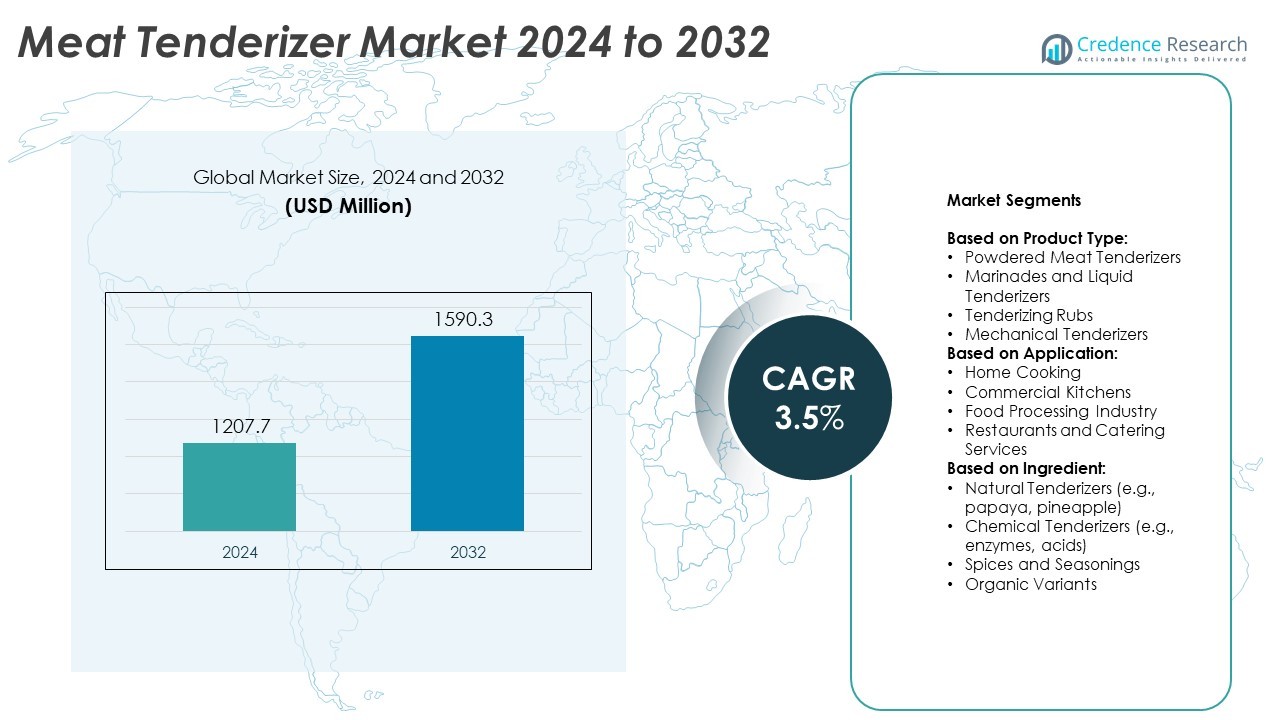

Meat Tenderizer Market size was valued at USD 1207.7 million in 2024 and is anticipated to reach USD 1590.3 million by 2032, at a CAGR of 3.5% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Meat Tenderizer Market Size 2024 |

USD 1207.7 Million |

| Meat Tenderizer Market, CAGR |

3.5% |

| Meat Tenderizer Market Size 2032 |

USD 1590.3 Million |

The Meat Tenderizer market is driven by rising consumer demand for processed, marinated, and convenience-based meat products supported by changing dietary preferences and expanding foodservice networks. It benefits from the growth of quick-service restaurants, frozen meals, and industrial meat processing where consistency and efficiency are critical. Clean-label trends push manufacturers toward natural enzyme-based solutions, while automation enhances throughput in commercial facilities. The market reflects evolving consumer interest in home cooking and premium textures, alongside the expansion of plant-based alternatives that require texture enhancement.

The Meat Tenderizer market demonstrates strong growth across key regions, with Asia-Pacific expanding rapidly due to rising meat consumption and growing foodservice industries. North America and Europe maintain steady demand supported by advanced processing infrastructures and consumer interest in natural tenderizers. Latin America shows increasing adoption through modern retail formats, while the Middle East and Africa gain traction with expanding urban foodservice. Leading players such as JBT Corporation, KitchenAid, Cuisinart, and Berkel strengthen their presence with innovation, broad distribution, and strong brand portfolios.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Meat Tenderizer market was valued at USD 1207.7 million in 2024 and is projected to reach USD 1590.3 million by 2032, at a CAGR of 3.5%.

- Demand for processed and marinated meat products is driving adoption across both retail and commercial channels, supported by evolving consumer lifestyles and rising preference for convenience.

- Clean-label trends and growing use of natural enzyme-based tenderizers such as papain and bromelain are reshaping product innovation, while automation strengthens efficiency in industrial applications.

- Competition is defined by established appliance brands and industrial system providers, with players focusing on product differentiation, ergonomic designs, and reliable tenderizing performance across home and commercial segments.

- Regulatory scrutiny on chemical additives and limitations in price-sensitive regions act as restraints, pushing manufacturers toward reformulation, natural ingredients, and cost-effective solutions.

- North America leads the market due to advanced processing infrastructure and consumer preference for premium meat textures, while Europe emphasizes clean-label adoption and sustainability.

- Asia-Pacific shows the fastest growth supported by urbanization, rising disposable incomes, and growing foodservice demand, while Latin America and the Middle East & Africa expand through modern retail and urban culinary adoption.

Market Drivers

Rising Demand for Processed and Ready-to-Cook Meat Products Across Urban Markets

The Meat Tenderizer market benefits from the increasing consumption of processed and convenience-based meat products, particularly in urban and semi-urban regions. Changing dietary habits and rising dual-income households are driving higher demand for pre-marinated, easy-to-cook meat cuts. This shift supports the need for tenderizers that reduce cooking time and improve meat texture. Quick-service restaurants, cloud kitchens, and frozen food manufacturers increasingly rely on tenderizing agents to deliver consistent meat quality. The market also finds growth opportunities in emerging economies where western-style diets are gaining popularity. It plays a pivotal role in enabling scalable, time-efficient meat preparation for high-volume commercial kitchens.

- For instance, Enzyme Solutions Ltd developed a bromelain-based powder that increases tenderness in chuck steak by 45% after a 20-minute marination at 4°C.

Expanding Foodservice Sector and Industrial Meat Processing Infrastructure

Rapid expansion in foodservice and institutional catering sectors accelerates the demand for commercial-grade meat tenderizers. Hotels, restaurants, and catering services prioritize tools and additives that improve the consistency and palatability of meat offerings. It supports quality control in industrial meat processing environments, where large-scale throughput requires mechanical or enzymatic solutions to standardize product output. Growth in hospitality and tourism increases the pressure on foodservice businesses to offer premium meat textures. Industrial tenderizing systems are integrated into production lines to maintain quality under high capacity. The Meat Tenderizer market aligns with this growth through equipment innovations and efficiency-driven solutions.

- For instance, JBT Corporation’s DSI Waterjet portioner integrates tenderizing functions and has shown a 30% improvement in marinade absorption uniformity across poultry breast fillets.

Growing Focus on Cost-Efficiency in Meat Processing Operations

The rising cost of premium meat cuts compels processors to improve the value of lower-grade meat through tenderization techniques. It enables food businesses to enhance profitability without compromising on consumer satisfaction. Enzymatic and mechanical tenderizers are deployed to convert tough cuts into market-ready products with improved chewability and flavor retention. This strategy reduces product wastage and improves margin control across the meat supply chain. The Meat Tenderizer market gains momentum by offering solutions that meet cost constraints while maintaining acceptable culinary standards. It remains a critical part of operational efficiency and value optimization.

Consumer Expectations for Enhanced Texture and Culinary Experience

Modern consumers increasingly demand premium taste and texture in meat products across retail and restaurant settings. Texture plays a central role in perceived quality, particularly in beef, pork, and poultry dishes. It enhances the sensory experience and supports brand loyalty for meat producers and culinary brands. Flavor-penetration and moisture retention also improve through effective tenderization, allowing marination processes to work more effectively. The Meat Tenderizer market evolves to meet these expectations by developing food-safe additives and precision mechanical tools. It helps ensure consistent satisfaction across product lines and meal formats.

Market Trends

Growing Adoption of Natural and Enzyme-Based Tenderizing Solutions in Clean-Label Meat Processing

The Meat Tenderizer market is witnessing a shift toward natural and plant-derived enzyme formulations in response to clean-label trends. Consumers increasingly avoid synthetic additives, encouraging manufacturers to explore papain, bromelain, and ficin-based alternatives. It supports product positioning around health, transparency, and minimal processing. Enzyme-based solutions provide effective protein breakdown without altering flavor profiles or requiring harsh chemicals. Food processors integrate these bio-based tenderizers to meet regulatory and consumer-driven clean-label standards. The trend reshapes innovation pipelines across both industrial and retail meat applications.

- For instance, The European Food Safety Authority (EFSA) set a group acceptable daily intake (ADI) of 40 mg/kg of body weight per day for phosphates, not a residue limit of 40 mg/kg in meat marinades. This ADI represents a safe daily intake level over a lifetime and applies to total phosphorus intake from all sources, not a specific limit for residual phosphates in food products.

Integration of Automated Tenderizing Equipment in Commercial Processing Facilities

Automated meat tenderizing machines are gaining traction across mid to large-scale processing plants to ensure speed and consistency. Equipment suppliers invest in stainless-steel designs with programmable settings for precise texture control. It helps reduce labor dependency and increases hygiene compliance in regulated meat production environments. Process automation supports consistent throughput while minimizing handling errors. The Meat Tenderizer market aligns with this trend by offering intelligent systems tailored for specific meat types and production scales. Manufacturers are also bundling tenderizing functions with cutting and marinating systems to streamline workflow.

- For instance, a survey by the Indian Council of Agricultural Research (ICAR) found that only 12 out of 145 small meat processors in central India used tenderization tools due to cost and training gaps

Expansion of Marinated Meat Segments Across Quick-Service and Packaged Food Channels

Pre-marinated meat products are rising in popularity across fast food chains and retail shelves due to convenience and flavor variety. Tenderization enhances marinade absorption and softens tougher muscle fibers, improving consumer appeal. It becomes essential in delivering uniform taste and texture across distributed foodservice channels. Manufacturers focus on developing tenderizer-infused marinade blends that simplify preparation and reduce cooking time. The Meat Tenderizer market supports this trend by introducing integrated formulations that work with standard marination processes. This synergy between texture optimization and flavor delivery increases demand in both chilled and frozen meat categories.

Increasing Use of Tenderizing Techniques for Alternative and Plant-Based Meat Products

The rise of plant-based meat alternatives creates new applications for tenderizing technologies. Manufacturers use mechanical shear and plant-derived enzymes to replicate the fibrous structure and mouthfeel of animal meat. It plays a role in addressing texture gaps commonly found in soy, pea, or wheat-based meat substitutes. Tenderizing steps also support flavor retention and protein uniformity in processed vegan meats. The Meat Tenderizer market evolves to serve this expanding segment with solutions designed for non-animal matrices. This trend highlights diversification beyond conventional meat applications.

Market Challenges Analysis

Regulatory Constraints on Chemical Additives and Growing Scrutiny of Ingredient Safety

The Meat Tenderizer market faces ongoing regulatory challenges linked to the safety and approval of chemical-based additives. Several countries impose strict limits on the use of phosphates, MSG, and synthetic enzymes due to health concerns. It compels manufacturers to reformulate or seek natural alternatives that meet food safety compliance. Ingredient transparency laws in regions such as North America and Europe increase the complexity of product development. Consumer watchdog groups and public health agencies continue to scrutinize labeling and additive declarations. This environment slows product launches and increases the cost of R&D in maintaining both effectiveness and regulatory alignment.

Limited Penetration in Price-Sensitive and Traditional Meat Processing Markets

Adoption of mechanical and enzymatic tenderizers remains relatively low in small-scale or traditional meat processing units. Cost barriers, limited awareness, and reliance on manual methods restrict market expansion in several developing regions. It hampers the scale of commercial deployment where margin control overrides investment in tenderization technologies. Resistance to change in local meat preparation practices further reduces uptake in artisanal and regional markets. The Meat Tenderizer market finds limited traction in segments that prioritize heritage techniques over industrial efficiency. Overcoming these barriers requires tailored education, low-cost solutions, and localized marketing strategies.

Market Opportunities

Rising Demand for Premium Meat Cuts in Emerging Economies with Expanding Middle-Class Consumers

Economic growth in Asia-Pacific, Latin America, and the Middle East is driving a surge in demand for high-quality meat products. Rising disposable income and urbanization support increased spending on premium meat cuts across both retail and foodservice channels. It creates strong demand for tenderizing solutions that enhance texture and improve cooking outcomes. Supermarkets and modern grocery chains are expanding their fresh meat offerings to meet evolving consumer expectations. The Meat Tenderizer market benefits from this shift by offering products that enable affordable access to upscale meat experiences. This opportunity encourages innovation in retail-ready tenderizing products and enzyme blends.

Product Development for E-commerce and Home Cooking Applications in Convenience-Driven Markets

Growth in online grocery platforms and at-home cooking trends opens new avenues for consumer-facing tenderizer products. Households seek tools and ingredients that replicate restaurant-quality meat texture without professional equipment. It prompts manufacturers to invest in user-friendly tenderizers suited for domestic kitchens. Powdered enzymatic blends, hand-held tenderizing tools, and pre-marinated kits gain popularity among home cooks seeking convenience and consistency. The Meat Tenderizer market can expand its footprint by targeting this segment through focused branding and distribution strategies. Companies that cater to convenience-focused consumers stand to gain early-mover advantages in untapped home-use categories.

Market Segmentation Analysis:

By Product Type:

Powdered meat tenderizers lead the segment due to their affordability, ease of application, and long shelf life. These products dominate in both retail and foodservice formats, particularly among home cooks and small kitchens. Marinades and liquid tenderizers follow, offering dual benefits of flavor enhancement and texture improvement. Tenderizing rubs gain momentum in specialty and regional markets where dry seasoning blends are preferred. Mechanical tenderizers serve industrial and high-volume users that require consistent results across large meat batches. The Meat Tenderizer market supports all four categories with differentiated formulations and tools tailored to usage scale and consumer habits.

- For instance, GEA Group’s MultiJector 2mm mechanical tenderizer is deployed in industrial poultry facilities and processes up to 6,000 kg of chicken breast per hour while maintaining a ±3% standard deviation in texture consistency.

By Application:

The food processing industry holds a prominent share due to its demand for scalable and standardized tenderizing methods. It supports high-volume operations that rely on both mechanical and enzymatic tenderization for quality control. Restaurants and catering services represent another critical application area, using both manual and automated systems to improve meat consistency and customer satisfaction. Commercial kitchens integrate tenderizers into their workflow to reduce preparation time while improving output quality. Home cooking continues to grow steadily, driven by increasing consumer interest in replicating restaurant-grade meals using accessible tenderizing products. The Meat Tenderizer market aligns with these diverse applications through targeted product offerings.

- For instance, Marel’s RevoPortioner forming line for poultry can produce up to 8,000 kilograms of formed raw material per hour, ensuring uniform product shape and minimizing waste.

By Ingredient:

Natural tenderizers such as papaya- and pineapple-derived enzymes are gaining preference among health-conscious and clean-label-focused consumers. These options meet demand for additive-free, plant-based solutions while maintaining functional effectiveness. Chemical tenderizers retain strong use in industrial and commercial applications where cost and consistency remain priorities. Spices and seasoning-based variants serve dual functions of tenderization and flavor enhancement, appealing to regional cuisines and specialty meat products. Organic variants, though niche, continue to expand across premium and wellness-focused consumer segments. It enables the Meat Tenderizer market to address evolving ingredient expectations across both mainstream and emerging demand profiles.

Segments:

Based on Product Type:

- Powdered Meat Tenderizers

- Marinades and Liquid Tenderizers

- Tenderizing Rubs

- Mechanical Tenderizers

Based on Application:

- Home Cooking

- Commercial Kitchens

- Food Processing Industry

- Restaurants and Catering Services

Based on Ingredient:

- Natural Tenderizers (e.g., papaya, pineapple)

- Chemical Tenderizers (e.g., enzymes, acids)

- Spices and Seasonings

- Organic Variants

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America holds the largest share of the Meat Tenderizer market, accounting for 34.2% of the global market in 2024. The region benefits from a strong presence of industrial meat processing facilities and well-established foodservice networks. Consumers in the United States and Canada show consistent demand for processed and marinated meat products, supporting high adoption of enzymatic and mechanical tenderizing methods. The widespread presence of quick-service restaurants, supermarket chains, and convenience-based food formats further drives demand for both commercial and home-use tenderizers. Leading manufacturers introduce tailored solutions that cater to barbecue culture, frozen meals, and retail seasoning blends. The market in North America continues to grow on the back of innovation, automation in meat processing, and clean-label trends that promote natural ingredient-based tenderizers.

Europe

Europe captures a market share of 26.7%, driven by its mature food processing industry and evolving consumer preferences for premium, sustainably processed meat. Countries such as Germany, France, the UK, and Italy lead demand due to their diverse culinary practices and preference for tender meat cuts in traditional dishes. The European Meat Tenderizer market emphasizes clean-label and organic tenderizers, with increased scrutiny on additives and synthetic enzymes. Food safety regulations and transparent labeling practices influence product innovation and drive the adoption of natural enzyme-based solutions such as bromelain and papain. Local meat producers also integrate automated tenderizing systems to improve consistency in product lines targeting export markets. The rise in plant-based alternatives further diversifies the tenderizer application space in this region.

Asia Pacific

Asia Pacific accounts for 21.4% of the global Meat Tenderizer market, supported by rapid urbanization, rising disposable incomes, and dietary shifts toward high-protein foods. Major economies including China, India, Japan, and South Korea experience growing demand for value-added meat products, especially in retail and foodservice segments. Local cuisines that involve marinated or grilled meat support strong adoption of powdered and liquid tenderizers. Manufacturers introduce affordable solutions targeting domestic kitchens and small restaurants to serve price-sensitive but quality-focused consumers. The market in Asia Pacific also benefits from government investment in modernizing food infrastructure and cold-chain logistics. With evolving lifestyle patterns and increasing western influence in diets, the region is poised for sustained growth in both traditional and convenience-driven tenderizing products.

Latin America

Latin America contributes 9.6% to the global Meat Tenderizer market, led by countries such as Brazil, Mexico, and Argentina. The region’s meat-centric food culture, particularly in grilled and smoked preparations, fuels demand for tenderizing agents that enhance flavor penetration and texture. Growth in modern retail formats and packaged meat categories creates new opportunities for pre-marinated and seasoned meat offerings. Local manufacturers and foodservice players adopt tenderizing solutions to improve competitiveness and reduce preparation time. While industrial adoption remains moderate, expanding urbanization and culinary modernization trends support long-term market potential. Traditional cooking methods still dominate rural areas, requiring awareness programs to promote broader adoption.

Middle East & Africa

The Middle East & Africa region holds a market share of 8.1%, supported by evolving foodservice infrastructure and increasing meat consumption in urban centers. In the Middle East, countries like Saudi Arabia and the UAE show growing demand for tender, flavorful meat suitable for grilling and kebab-style preparations. Africa’s developing markets rely on both traditional and semi-industrial meat handling systems, where adoption of tenderizers is gradually increasing. Religious dietary preferences and halal certification drive interest in natural and enzyme-based tenderizers. Retail chains and quick-service formats continue to expand, introducing packaged meat options that require consistent texture and flavor. The Meat Tenderizer market in this region is expected to grow with improvements in supply chains, food safety standards, and meat processing capabilities.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

Competitive Analysis

Key Players in the Meat Tenderizer market include JBT Corporation, Berkel, Cuisinart, Deni, Hamilton Beach, HIC (Harold Import Co.), Jaccard Corporation, KitchenAid, Maverick, and Oxo International, driving growth through specialized offerings, diversified product lines, and strategic channel penetration. The meat tenderizer market reflects a mix of strong consumer brands and specialized commercial players, each competing on product innovation, usability, and brand reach. Premium kitchenware brands emphasize ergonomics, durability, and distinctive design to appeal to households seeking both functionality and aesthetics. Companies with a broader appliance portfolio leverage brand recognition and retail networks to secure consistent shelf space, positioning themselves as household staples in both manual and electric categories.

Specialized firms that focus on blade-based tenderizers highlight stainless steel construction, food safety certifications, and replaceable components, which reinforce long-term reliability and recurring sales opportunities. Commercial-focused manufacturers differentiate through industrial-grade solutions, emphasizing processing efficiency, hygiene standards, and integration into large-scale food systems, where performance and service contracts build customer loyalty.

Mid-tier and value-driven competitors compete largely on affordability and distribution flexibility, often targeting online platforms and mass retailers. These companies secure market presence by offering cost-effective alternatives without compromising essential functionality, catering to cost-sensitive consumers and small businesses.

Recent Developments

- In 2024, Jaccard Corporation launched manual Model H and semi-automatic TSHY, the two new models that they worked on. Model H is suitable for both amateurs and professionals considering it’s designed to withstand wear and provide a hands-on experience to the user during the meat tenderizing process.

- In February 2023, JBT introduced the alco Tenderizer ASC at its Food Technology Centres. This system enhanced productivity and operational reliability by offering height-adjustable knife rollers and hygienic construction for high-throughput meat processors

- In 2023, McCormick and Company enhanced its lineup of enzyme-containing meat tenderizer with papain and bromelain. These natural enzymes are well known for their ability to break apart muscle fibers and increase the overall tenderness and texture of meat products. Utilizing these natural enzymes decreases the time spent cooking and improves the processing of meat products which makes it easier to achieve tender results both for private cooking and mass catering.

Market Concentration & Characteristics

The Meat Tenderizer market exhibits moderate concentration, with a blend of established kitchen appliance brands, industrial equipment manufacturers, and specialty tool providers contributing to its structure. It features both organized and fragmented segments, with large players dominating the industrial and premium consumer categories, while regional and private-label brands compete in price-sensitive markets. Product differentiation is largely based on application, ingredient composition, and ease of use across home, commercial, and industrial settings. It supports a dynamic competitive environment where innovation in safety, hygiene, and multi-functionality defines brand loyalty and shelf visibility. The market also reflects characteristics of seasonal demand variation, especially in retail segments tied to festive or grilling seasons. Regulatory compliance and food safety standards influence ingredient-based tenderizers, creating entry barriers for unverified products. It remains price-sensitive in emerging regions, yet sees strong brand-driven growth in developed economies where convenience, texture quality, and clean-label preferences shape buying behavior.

Report Coverage

The research report offers an in-depth analysis based on Product Type, Application, Ingredient and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand for clean-label and plant-based tenderizers will increase as consumers seek natural ingredient alternatives.

- Automated tenderizing equipment will gain traction in industrial meat processing to improve efficiency and consistency.

- Home-use tenderizers will grow in popularity due to rising interest in home cooking and premium meat preparation.

- Manufacturers will expand product lines to cater to both animal-based and plant-based meat applications.

- Retail demand for pre-marinated and ready-to-cook meats will drive innovation in integrated tenderizing solutions.

- Regulations on chemical additives will influence a shift toward enzyme-based and organic tenderizers.

- E-commerce will become a key sales channel for compact tenderizing tools and seasoning kits.

- Emerging markets will offer growth opportunities through rising disposable incomes and modernized food retail.

- Product differentiation will focus on multi-functionality, hygiene, and ergonomic design in consumer segments.

- Collaboration between food processors and ingredient companies will accelerate development of novel tenderizing blends.