Market Overview:

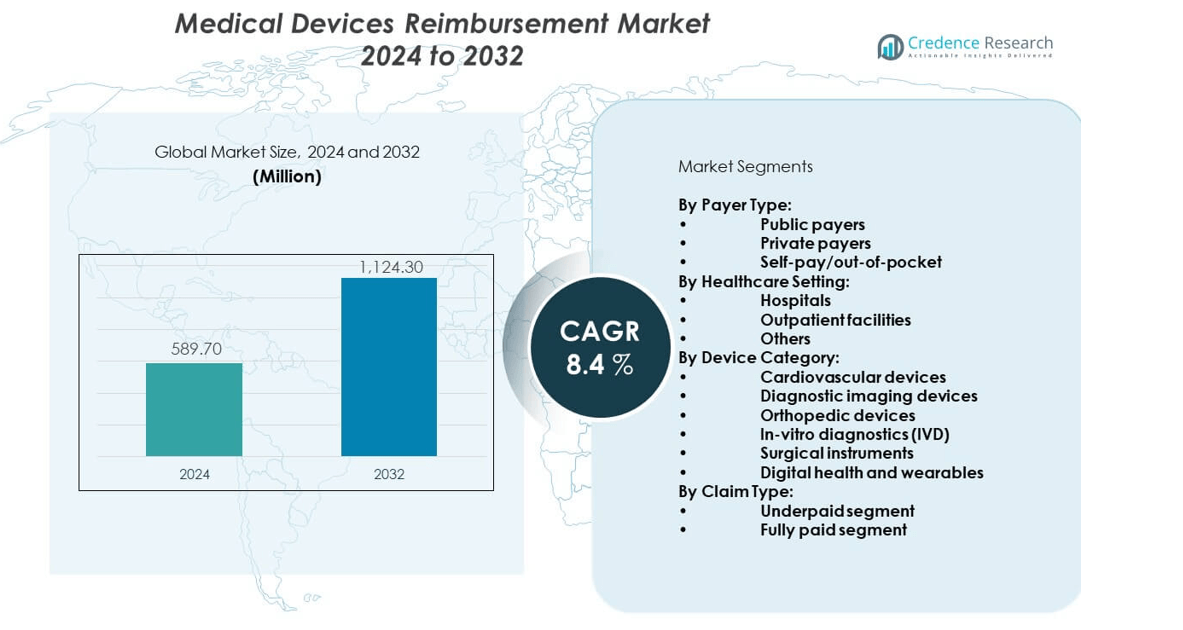

The medical devices reimbursement market was valued at USD 589.7 million in 2024 and is projected to reach USD 1,124.3 million by 2032, growing at a CAGR of 8.4% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Medical Devices Reimbursement Market Size 2024 |

USD 589.7 million |

| Medical Devices Reimbursement Market, CAGR |

8.4% |

| Medical Devices Reimbursement Market Size 2032 |

USD 1,124.3 million |

The market is driven by the rising prevalence of chronic diseases, which heightens demand for costly medical devices such as diagnostic imaging equipment, implants, and monitoring systems. Governments and private insurers are under pressure to enhance affordability while ensuring timely access to innovative treatments. The growing elderly population and the shift toward value-based healthcare models further push reimbursement frameworks to evolve, enabling better patient outcomes and wider adoption of advanced technologies.

Geographically, North America leads the medical devices reimbursement market due to strong healthcare infrastructure, widespread insurance coverage, and supportive reimbursement policies. Europe follows closely, supported by universal healthcare systems and government-led reforms. Asia-Pacific is emerging as the fastest-growing region, with rising healthcare investments, expanding insurance penetration, and growing awareness of medical device reimbursement. Meanwhile, Latin America and the Middle East & Africa are gradually adopting structured reimbursement models as part of broader healthcare modernization efforts.

Market Insights:

- The medical devices reimbursement market was valued at USD 589.7 million in 2024 and is expected to reach USD 1,124.3 million by 2032, growing at a CAGR of 8.4%.

- Rising prevalence of chronic diseases increases the demand for costly medical devices and creates a need for reimbursement systems.

- Strong government support and policy reforms are boosting the adoption of structured reimbursement frameworks across healthcare systems.

- High device costs and complex regulatory requirements remain key restraints, limiting faster market penetration.

- North America leads due to advanced healthcare infrastructure and widespread insurance coverage supporting device reimbursement.

- Europe maintains steady growth, backed by universal healthcare systems and evolving reimbursement regulations.

- Asia-Pacific is the fastest-growing region, driven by expanding insurance penetration, healthcare investments, and rising awareness of reimbursement benefits.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Rising Chronic Disease Burden and Demand for Advanced Medical Devices:

The medical devices reimbursement market is strongly driven by the increasing prevalence of chronic diseases. Conditions such as cardiovascular disorders, diabetes, and respiratory illnesses require continuous monitoring and specialized devices. Patients depend on expensive diagnostic equipment and implants, creating demand for structured reimbursement systems. Governments and insurers face pressure to make these devices more affordable and accessible. It reflects a clear push for reimbursement policies that support both innovation and patient affordability. Healthcare providers also prefer advanced devices when costs are covered through insurance. This alignment between demand and affordability accelerates adoption rates. It builds a cycle where improved reimbursement strengthens access and boosts overall market growth.

- For instance, Medtronic’s Micra leadless pacemaker demonstrated a remarkable implant success rate of 99.1% with a low major complication rate of 2.7% through 12 months, exemplifying advanced cardiac device technology gaining reimbursement support and patient trust.

Growing Government Support and Healthcare Policy Initiatives:

Government agencies across regions are implementing reforms to ease financial strain on patients. They focus on strengthening reimbursement structures that ensure coverage for critical medical devices. National health authorities are linking reimbursement frameworks with quality and efficiency in healthcare delivery. This integration promotes faster adoption of innovative technologies across public hospitals and clinics. The medical devices reimbursement market benefits from these coordinated initiatives that balance cost with quality. Reimbursement also encourages local manufacturers to expand production capacities for high-demand devices. The integration of cost-sharing models reduces patient out-of-pocket expenses. It creates confidence in healthcare systems and increases demand for advanced medical solutions.

- For instance, Abbott’s partnership with mAbxience to broaden access to biosimilars in emerging markets reflects how strategic agreements supported by reimbursement policy enhance availability of affordable advanced therapeutics.

Expansion of Private Insurance Coverage and Patient-Centric Plans:

Private insurance companies are broadening their coverage plans to include more medical devices. They aim to strengthen customer retention by providing financial relief for costly equipment. Insurers view medical devices as vital for preventive care and long-term health management. The expansion of patient-focused policies supports higher reimbursement for implants, imaging systems, and monitoring devices. It allows patients to make quicker treatment decisions without fearing high costs. The medical devices reimbursement market benefits when private players integrate digital claim processing systems. The adoption of AI-based claim verification also reduces fraud and improves policyholder confidence. It encourages patients to use advanced devices, fueling overall growth momentum.

Integration of Value-Based Healthcare and Patient Outcome Metrics:

Healthcare systems are transitioning toward value-based models where patient outcomes drive reimbursement. Governments and private insurers adopt outcome-based frameworks to align payments with treatment success. Hospitals must show measurable improvements in patient health to secure higher reimbursements. This trend encourages the use of advanced devices with proven clinical benefits. The medical devices reimbursement market gains traction as outcome-based policies enhance trust among stakeholders. The focus on efficiency reduces unnecessary device usage while rewarding proven technologies. Value-based systems ensure cost control without limiting patient access to quality care. It motivates manufacturers to develop evidence-backed devices, strengthening long-term sustainability.

Market Trends:

Increasing Adoption of Digital Platforms for Claims and Processing Efficiency:

Healthcare providers are embracing digital tools to speed up reimbursement cycles. Digital claims systems allow faster validation, reducing delays in device adoption. Blockchain platforms enhance transparency by securing patient data and payment histories. Insurers use AI algorithms to detect errors and prevent fraudulent claims. The medical devices reimbursement market is shifting toward automated workflows that cut administrative costs. Hospitals also integrate cloud-based reimbursement systems for real-time claim tracking. Patients benefit from quicker approvals, which increases confidence in adopting devices. It highlights a trend where digital adoption strengthens efficiency and market reliability.

- For instance, Boston Scientific’s acquisition of Bolt Medical enhances the cardiovascular portfolio with intravascular lithotripsy technology, which is expected to benefit from streamlined reimbursement processes enabled by digital claims management.

Rising Role of Telemedicine and Remote Device Monitoring in Reimbursement Models:

The adoption of telemedicine has expanded the scope of device reimbursement. Remote monitoring tools and wearable devices are being included under insurance plans. This reflects recognition of the role of digital health in preventive care. Insurers link reimbursement rates with real-time data provided by connected devices. The medical devices reimbursement market evolves as remote healthcare adoption grows. Hospitals view telehealth-linked devices as cost-effective in reducing hospital readmissions. Reimbursement models that integrate telehealth strengthen access for rural and underserved populations. It positions digital monitoring as a permanent component of reimbursement frameworks.

- For instance, Smith+Nephew’s partnership with Standard Health to establish an Orthopaedic Ambulatory Surgery Centre demonstrates how integration of digital health and remote monitoring supports reimbursement models expanding outpatient orthopedic care.

Expansion of Public-Private Collaborations to Standardize Reimbursement Policies:

Governments and private insurers are forming partnerships to unify reimbursement approaches. Collaborative frameworks reduce policy gaps and ensure equal access to medical devices. Healthcare systems benefit when standardized rules prevent regional inequalities in reimbursement. The medical devices reimbursement market gains stability through consistent global practices. Partnerships also promote integration of quality metrics across reimbursement programs. International organizations are influencing governments to adopt aligned reimbursement standards. This reduces complexity for manufacturers that operate across multiple regions. It strengthens a predictable environment that supports innovation and global device distribution.

Growing Patient Awareness and Transparency in Reimbursement Policies:

Patients are becoming more informed about their reimbursement rights and options. Awareness campaigns highlight insurance coverage for devices and the process of claim approvals. Transparency in policy communication reduces patient hesitation in adopting advanced medical solutions. The medical devices reimbursement market adapts to rising demand for clarity and fairness. Insurers are publishing clear guidelines for device eligibility and approval. Hospitals also share structured information with patients to ensure smooth reimbursement. This shift increases trust between healthcare stakeholders and consumers. It builds momentum for higher adoption of both insurance plans and medical devices.

Market Challenges Analysis:

Complex Regulatory Frameworks and Slow Policy Adaptation Across Regions:

The medical devices reimbursement market faces significant challenges due to fragmented regulations. Each country maintains its own reimbursement rules, creating barriers for manufacturers. The lack of global standardization increases compliance costs and slows device availability. Insurers also struggle with aligning reimbursement models to rapidly evolving medical technologies. It creates uncertainty for manufacturers planning cross-border expansions. Regulatory delays often lead to uneven access for patients across regions. Hospitals and providers must navigate multiple policies, causing inefficiencies. It makes policy harmonization critical for sustaining market growth and global accessibility.

Rising Cost Pressures, Fraud Risks, and Limited Awareness Among Patients:

Healthcare systems face financial strain due to increasing device costs and patient volumes. Insurers must balance coverage expansion with risk of financial losses. Fraudulent claims also create distrust within the reimbursement ecosystem. The medical devices reimbursement market encounters challenges when awareness about policies remains limited. Many patients are unaware of device eligibility or claim processes. Hospitals face additional administrative burdens while educating patients on reimbursement. Limited financial literacy prevents widespread use of available benefits. It highlights the urgent need for streamlined claim systems and awareness programs.

Market Opportunities:

Expansion of Emerging Healthcare Systems and Insurance Penetration in Developing Regions:

Developing countries are expanding healthcare access through national insurance programs and public-private partnerships. Governments are integrating device reimbursement policies into broader healthcare modernization plans. The medical devices reimbursement market gains opportunities from rising insurance penetration in Asia-Pacific and Latin America. Growing middle-class populations demand affordable access to advanced medical technologies. Private insurers are targeting these regions with low-cost policies that include device coverage. This creates favorable conditions for device manufacturers to expand. It strengthens adoption rates while building long-term trust in insurance-based care models.

Innovation in AI, Big Data, and Personalized Reimbursement Models for Medical Devices:

Technological innovation creates opportunities for personalized reimbursement frameworks. AI-driven analytics can predict device usage patterns and adjust coverage accordingly. Big data allows insurers to design flexible reimbursement based on patient profiles. The medical devices reimbursement market evolves when policies reward preventive and precision healthcare devices. Insurers can link coverage directly with predictive outcomes to minimize risks. Hospitals also benefit from reduced claim rejections and faster approvals. Patients experience tailored benefits that align with individual treatment needs. It sets a foundation for personalized healthcare financing and sustainable market expansion.

Market Segmentation Analysis:

By Payer Type

The medical devices reimbursement market is segmented into public, private, and self-pay categories. Public payers, including government programs such as Medicare and Medicaid, dominate due to broad coverage and strong policy support. Private payers hold significant share with expanding commercial insurance plans that cover advanced devices. Self-pay remains smaller but relevant in regions with limited insurance penetration. Each payer category reflects different levels of affordability and access to medical devices. It highlights how payer diversity directly impacts patient access and market growth.

- For instance, Medtronic’s Micra leadless pacemaker achieved a 99.2% implant success rate with a low major complication rate of 2.7% through 12 months in a study involving 725 patients across 19 countries, demonstrating both technological reliability and acceptance supported by diverse reimbursement policies.

By Healthcare Setting

Hospitals account for the largest share, driven by high-acuity inpatient procedures and reliance on complex medical devices. Outpatient facilities, including ambulatory surgery centers and specialty clinics, are growing rapidly due to cost-efficient treatment models. Other settings such as home healthcare providers and physician offices are emerging contributors. Remote monitoring devices and home-based care support this growth. The segment structure demonstrates a clear shift toward diversified care settings. It emphasizes the importance of flexible reimbursement models tailored to each environment.

- For instance, the Micra AV post-approval registry showed a 99.4% implant success rate in 801 patients with a 1.5% system revision rate at one year, highlighting the device’s adaptability and reliability in diverse care settings including outpatient environments.

By Device Category

Cardiovascular devices and diagnostic imaging hold substantial shares due to their critical role in chronic care. Orthopedic devices, in-vitro diagnostics, and surgical instruments add further reimbursement demand. Digital health and wearables are the fastest-growing segment, reflecting the adoption of connected healthcare solutions. These technologies align with preventive care models and patient-centered approaches. The medical devices reimbursement market benefits when such categories gain broader coverage. It indicates an ongoing shift toward technology-driven reimbursement frameworks.

By Claim Type

The underpaid segment dominates due to partial reimbursements that are common across multiple regions. Fully paid claims are expanding as policies improve and insurers strengthen affordability initiatives. It reflects a positive shift toward reducing patient financial burdens. The balance between underpaid and fully paid claims shapes patient confidence in healthcare systems. Insurers are focusing on reducing delays and denials. This evolution strengthens the role of reimbursement as a driver of device adoption. It ensures broader alignment between policy reforms and healthcare accessibility.

Segmentation:

By Payer Type:

- Public payers (government programs such as Medicare and Medicaid)

- Private payers (commercial health insurance companies)

- Self-pay/out-of-pocket

By Healthcare Setting:

- Hospitals (hold the majority share due to high-acuity inpatient procedures)

- Outpatient facilities (ambulatory surgery centers, specialty clinics)

- Others (home healthcare providers, physician offices)

By Device Category:

- Cardiovascular devices (pacemakers, ICDs)

- Diagnostic imaging devices (including AI-supported systems)

- Orthopedic devices

- In-vitro diagnostics (IVD)

- Surgical instruments

- Digital health and wearables (fastest-growing segment)

By Claim Type:

- Underpaid segment (leading due to partial reimbursements)

- Fully paid segment (gaining traction with policy improvements)

By Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis:

North America

North America holds the largest share of the medical devices reimbursement market, accounting for around 38%. Strong healthcare infrastructure, extensive insurance coverage, and government programs such as Medicare and Medicaid drive this dominance. Private insurers also play a vital role by expanding reimbursement for advanced devices, including digital health and wearables. Hospitals and outpatient facilities benefit from clear reimbursement frameworks that encourage device adoption. It continues to attract innovation due to supportive regulatory policies and high per capita healthcare spending. The region’s focus on value-based care and outcome-driven reimbursement sustains market leadership.

Europe

Europe represents nearly 29% of the global market, supported by universal healthcare systems and government-backed reimbursement models. Countries like Germany, France, and the United Kingdom lead with structured policies that reduce patient out-of-pocket costs. The region’s aging population further increases demand for cardiovascular and orthopedic devices under reimbursement programs. Insurers are emphasizing patient access and cost control while maintaining quality standards. The medical devices reimbursement market in Europe reflects stability through well-established healthcare funding mechanisms. It also benefits from harmonized policy frameworks across member states, promoting predictable adoption trends.

Asia-Pacific and Other Regions

Asia-Pacific accounts for about 23% of the global market and is the fastest-growing region. Rising healthcare investments, expanding insurance coverage, and the adoption of digital health solutions fuel strong growth. Countries such as China, India, and Japan are leading with reforms that strengthen reimbursement frameworks. The region’s large population base creates strong demand for affordable access to advanced medical devices. Latin America holds around 6% share, supported by gradual improvements in public and private insurance penetration. The Middle East and Africa contribute nearly 4% share, driven by healthcare modernization and expanding medical infrastructure. It positions emerging regions as future growth hubs for medical device reimbursement.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Medtronic

- Boston Scientific

- Abbott

- Hologic

- Smith and Nephew

- Terumo Corporation

Competitive Analysis:

The medical devices reimbursement market is shaped by a mix of global insurers, healthcare providers, and device manufacturers. Leading payers such as UnitedHealthcare, Allianz, and CVS Health maintain strong positions by leveraging broad customer bases and diverse policy structures. Prominent device manufacturers including Medtronic, Abbott, and Boston Scientific influence reimbursement policies through innovative technologies that demand coverage alignment. It is highly competitive, with private payers competing against government programs and device makers seeking favorable reimbursement pathways. Market players focus on partnerships, product expansion, and policy engagement to strengthen their positions and address evolving reimbursement frameworks.

Recent Developments:

- In August 2024, Abbott and Medtronic announced a partnership to develop an integrated continuous glucose monitoring system combining Abbott’s FreeStyle Libre technology with Medtronic’s automated insulin delivery system and smart insulin pens. This collaboration aims to create a device that automatically adjusts insulin based on glucose levels, simplifying diabetes management for users.

- In January 2025, Boston Scientific announced the acquisition of Bolt Medical, a company specializing in intravascular lithotripsy technology for treating calcified arterial disease. The deal valued up to $664 million expands Boston Scientific’s cardiovascular portfolio with a minimally invasive technology that addresses a significant unmet medical need.

- In October 2023, Abbott signed a strategic agreement with mAbxience to commercialize biosimilars focusing on oncology and women’s health in emerging markets, aiming to increase access to affordable biosimilar medicines globally.

- In January 2025, Hologic completed a $350 million acquisition of Gynesonics, a medical device company that developed the Sonata System, a novel ultrasound-guided, incision-free treatment for symptomatic fibroids. This acquisition complements Hologic’s women’s health portfolio and expands minimally invasive treatment options.

Market Concentration & Characteristics:

The medical devices reimbursement market is moderately concentrated, with a few dominant insurers and multinational device manufacturers shaping the competitive landscape. It is defined by strong regulatory oversight, evolving policy frameworks, and growing emphasis on value-based healthcare models. Large companies maintain market leadership through extensive networks, while smaller players differentiate through niche coverage solutions and specialized reimbursement support. Continuous innovation in digital health, wearables, and AI-driven diagnostics creates new dynamics, increasing the need for adaptive reimbursement strategies.

Report Coverage:

The research report offers an in-depth analysis based on payer type, healthcare setting, device category, claim type, and geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Expansion of value-based healthcare will reshape reimbursement structures.

- Digital health and wearables will drive faster reimbursement adoption.

- AI-supported diagnostics will gain broader insurance coverage.

- Policy reforms will strengthen fully paid claim segments.

- Partnerships between insurers and device firms will increase.

- Emerging markets will witness faster adoption of reimbursement frameworks.

- Hospitals will retain dominance as primary reimbursement centers.

- Outpatient facilities will gain more coverage due to cost efficiency.

- Data-driven claim processing will improve payer transparency.

- Global standardization efforts will harmonize reimbursement policies.