Market Overview:

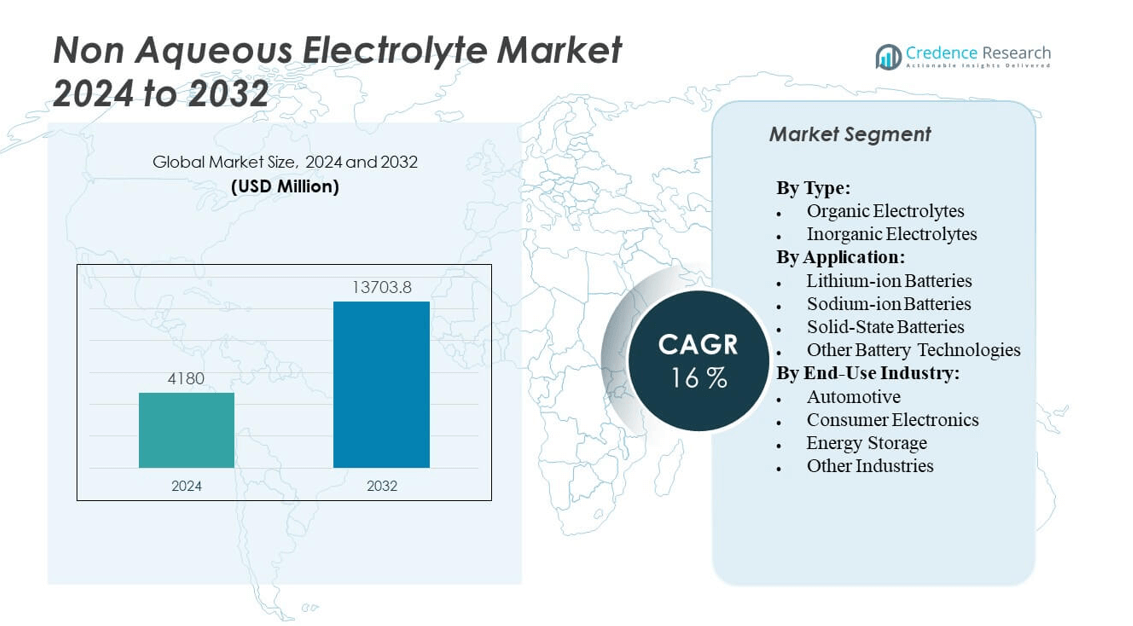

The Non Aqueous Electrolyte Market is projected to grow from USD 4,180 million in 2024 to an estimated USD 13,703.8 million by 2032, with a compound annual growth rate (CAGR) of 16% from 2024 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Non Aqueous Electrolyte Market Size 2024 |

USD 4,180 million |

| Non Aqueous Electrolyte Market, CAGR |

16% |

| Non Aqueous Electrolyte Market Size 2032 |

USD 13,703.8 million |

The market growth is driven by the rising adoption of lithium-ion batteries across electric vehicles, energy storage systems, and portable electronics. Expanding renewable energy integration further fuels demand for efficient storage technologies, where non-aqueous electrolytes provide higher voltage stability and superior electrochemical performance. Growing emphasis on sustainable energy and government incentives for EV adoption are accelerating innovations, with manufacturers focusing on electrolyte formulations that enhance safety, improve thermal stability, and deliver higher energy density to meet performance needs.

Geographically, Asia Pacific leads the market due to strong EV production in China, Japan, and South Korea, supported by large-scale battery manufacturing facilities. North America is emerging rapidly, with growing investments in energy storage and EV infrastructure, while Europe shows steady growth, driven by strict environmental regulations and sustainability mandates. Developing regions in Latin America and the Middle East are beginning to explore opportunities, particularly in renewable energy projects, indicating expanding adoption in future years.

Market Insights:

- The Non Aqueous Electrolyte Market is projected to grow from USD 4,180 million in 2024 to USD 13,703.8 million by 2032, at a CAGR of 16%.

- Strong EV adoption and demand for high-capacity lithium-ion batteries are driving significant market growth.

- Expansion of renewable energy projects is fueling the need for grid-scale storage using advanced electrolytes.

- Safety concerns and flammability issues continue to act as restraints on widespread adoption.

- High production costs and supply chain disruptions create challenges for scaling manufacturing globally.

- Asia Pacific leads the market with 46% share in 2024, supported by strong battery production in China, Japan, and South Korea.

- North America and Europe follow with 27% and 21% shares respectively, while Latin America and the Middle East & Africa together account for 6%.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising adoption of electric vehicles and high-capacity batteries drives strong demand for advanced electrolytes

The global push toward sustainable transportation is increasing the need for high-performance lithium-ion batteries, which rely on advanced electrolytes for stable operation. Government policies that encourage electric vehicle adoption are strengthening supply chains for battery production. Automotive manufacturers are focusing on developing long-range EVs, creating consistent demand for electrolytes with higher energy density and thermal stability. It is driving innovation in electrolyte chemistry to support next-generation EV batteries. The Non Aqueous Electrolyte Market benefits directly from these shifts. Stringent emission norms across Europe, Asia, and North America strengthen the need for efficient energy storage solutions. Companies are collaborating to scale manufacturing capacities and ensure consistent supply. Continuous funding in R&D supports safer and more sustainable electrolytes that improve performance standards globally.

- For instance, CATL introduced a lithium-metal battery prototype using an advanced lithium salt electrolyte (LiFSI), which doubled cycle life while maintaining high energy density, supporting the development of long-range EVs capable of exceeding 600 kilometers per charge.

Expanding renewable energy projects accelerate the deployment of grid-scale storage solutions

The rise in renewable energy adoption, particularly solar and wind power, requires large-scale energy storage to balance grid fluctuations. Grid operators are investing in lithium-ion and advanced battery technologies that depend heavily on non-aqueous electrolytes for stability and efficiency. Governments are prioritizing clean energy infrastructure, driving steady demand growth for storage batteries. It enhances energy resilience and supports national decarbonization goals. The Non Aqueous Electrolyte Market finds significant opportunities in supporting these transitions. Strategic collaborations between energy companies and battery manufacturers are increasing research into safer electrolytes for long-duration storage. Continuous investments in hybrid storage technologies further strengthen market adoption. Increasing focus on energy security across developed and developing regions creates momentum for sustainable electrolytes in utility-scale projects.

Rising demand for portable electronics fosters innovation in energy-dense electrolyte formulations

The growing reliance on smartphones, laptops, and wearable devices creates high demand for compact and energy-dense batteries. Consumer electronics companies are focusing on thinner and more powerful devices, which require electrolytes with superior electrochemical stability. It drives innovation in non-aqueous electrolyte formulations tailored to meet efficiency and safety standards. The Non Aqueous Electrolyte Market is seeing strong traction from this sector, as miniaturization continues to define consumer technology. Constant product upgrades by leading electronics brands further boost battery demand. Manufacturers are developing tailored electrolyte solutions that balance energy density with reduced degradation. Governments in Asia Pacific, where most electronics production occurs, are encouraging R&D for high-performance components. These advancements provide long-term stability to the consumer electronics segment.

Strategic research and government funding strengthen development of safer and sustainable electrolytes

Global initiatives aimed at reducing dependency on fossil fuels are pushing governments to fund projects focused on energy innovation. Universities, research institutes, and private companies are collaborating to develop advanced non-aqueous electrolytes that enhance battery life and safety. It accelerates commercialization of innovative solutions in multiple sectors, including automotive and renewable energy. The Non Aqueous Electrolyte Market benefits from these policy-led actions that boost industry confidence. Research in solid-state batteries is opening pathways for electrolyte upgrades. Safety concerns related to flammability are driving innovations in non-flammable electrolyte chemistries. Public-private partnerships are promoting large-scale pilot projects that speed up adoption. Continuous improvements in regulatory standards provide stability for new entrants and established manufacturers.

- For example, QuantumScape demonstrated a solid-state lithium-metal battery with a non-aqueous electrolyte that achieved over 1,000 charge-discharge cycles while retaining more than 95% capacity, marking a breakthrough in both safety and longevity.

Market Trends

Increasing focus on solid-state battery integration creates demand for advanced non-aqueous electrolytes

Solid-state battery development is gaining traction due to its potential for higher safety, longer lifespan, and greater energy density. Companies are investing heavily in research to replace liquid electrolytes with advanced non-aqueous or hybrid systems. It highlights a trend toward electrolyte formulations designed for compatibility with solid-state structures. The Non Aqueous Electrolyte Market is responding with targeted R&D. Strategic investments from automakers and energy storage companies accelerate pilot-scale production. Governments are offering incentives for commercialization of safer battery technologies. Industry leaders are working to reduce cost barriers while ensuring scalability. Growing industrial adoption is reshaping electrolyte innovation across global markets.

- For example, QuantumScape reported that its solid-state lithium-metal battery prototype ran for over 800 cycles while retaining more than 80% capacity under 1C charge–discharge conditions at 30 °C. The company highlighted a single-layer pouch cell with thick cathodes and an anode-free design, demonstrating high coulombic efficiency above 99.97%.

Rising emphasis on recycling and circular economy initiatives influences electrolyte development

The battery industry is under pressure to address end-of-life challenges through sustainable practices. Companies are focusing on electrolyte recovery and recycling to reduce environmental impacts. It is driving a trend where manufacturers explore eco-friendly non-aqueous electrolyte formulations that align with global circular economy goals. The Non Aqueous Electrolyte Market is influenced by growing environmental regulations across major economies. Firms are adopting closed-loop processes that minimize waste. Industry collaborations are emerging to standardize recycling methods for electrolyte components. Research is also focused on reducing toxic by-products during disposal. Regulatory support and consumer awareness further strengthen this movement toward greener production cycles.

Integration of artificial intelligence in electrolyte research accelerates formulation breakthroughs

AI-driven modeling is transforming research by enabling faster analysis of electrolyte stability, compatibility, and performance. Research labs are employing machine learning algorithms to predict material behavior under various operating conditions. It allows faster prototyping and lowers costs associated with trial-and-error experimentation. The Non Aqueous Electrolyte Market is witnessing a digital transformation in product development. AI tools are enhancing collaboration between research institutes and commercial manufacturers. Predictive analytics are helping scale up lab discoveries to industrial production. Investment in computational chemistry platforms is expanding globally. The integration of digital innovation accelerates time-to-market for advanced electrolyte solutions.

- For instance, BASF applied AI-driven molecular discovery systems that reduced research timelines from 18 months to just 3 weeks, allowing faster identification of electrolyte candidates with improved thermal stability and ionic conductivity compared to traditional experimental methods.

Strategic partnerships between global players foster standardization and market expansion

Battery manufacturers, automakers, and chemical companies are forming alliances to share expertise and resources. Joint ventures are targeting standardized electrolyte formulations that can meet the diverse needs of multiple industries. It creates consistency in performance benchmarks and accelerates large-scale adoption. The Non Aqueous Electrolyte Market benefits from this collaborative momentum. Partnerships are supporting cross-industry trials and pilot-scale commercialization. Emerging startups are gaining access to funding and infrastructure through these collaborations. Governments encourage alliances to speed up adoption of sustainable battery technologies. These trends are reshaping competitive dynamics across regional and global markets.

Market Challenges Analysis

Safety concerns and flammability issues restrain large-scale adoption of non-aqueous electrolytes in critical applications

The performance of non-aqueous electrolytes comes with safety concerns, particularly their flammability under high temperatures. Manufacturers face challenges in ensuring electrolytes meet rigorous safety standards for EVs and large storage systems. It creates hesitation among buyers who prioritize long-term reliability. The Non Aqueous Electrolyte Market is working toward solutions, yet accidents related to thermal runaway highlight ongoing risks. Strict regulations increase compliance costs for manufacturers. Companies must balance innovation with safety certification processes, which delay commercialization timelines. Limited awareness about advanced non-flammable alternatives adds to the adoption gap. Industry players are investing in R&D to address these safety bottlenecks and build consumer trust.

High production costs and supply chain disruptions challenge consistent global expansion of electrolyte manufacturing

Producing high-quality non-aqueous electrolytes requires advanced materials and strict processes, driving up costs. Smaller manufacturers struggle to compete with established companies that benefit from economies of scale. It leads to price volatility and uneven supply, particularly in emerging economies. The Non Aqueous Electrolyte Market faces additional challenges from raw material shortages and geopolitical tensions affecting supply chains. Trade restrictions impact access to essential chemical inputs. Companies are forced to diversify sourcing strategies, increasing operational costs. Limited infrastructure for scaling production in some regions slows adoption. These challenges hinder the market’s ability to meet rapidly rising global demand effectively.

Market Opportunities

Expansion of electric mobility and renewable integration presents major growth avenues for electrolyte manufacturers

The accelerating shift toward electrification in transportation and renewable energy expansion is opening vast opportunities for electrolyte providers. EV adoption is growing across developed and emerging markets, with strong government support for clean mobility. It creates consistent demand for safer and more energy-dense electrolyte formulations. The Non Aqueous Electrolyte Market is positioned to benefit from this large-scale industrial transformation. Grid modernization projects in Asia, North America, and Europe require advanced storage systems powered by high-performance batteries. Companies innovating in non-aqueous chemistry will gain a competitive edge. Partnerships with automakers and renewable energy firms offer growth avenues. Sustained policy support ensures a long-term opportunity horizon for electrolyte adoption.

Innovations in next-generation chemistries and strategic collaborations enable new revenue streams for producers

Research in solid-state, lithium-sulfur, and sodium-ion batteries is creating new opportunities for advanced electrolytes. Manufacturers that innovate in compatible non-aqueous formulations can secure leadership positions in these emerging segments. It gives scope for differentiation through performance, safety, and scalability. The Non Aqueous Electrolyte Market benefits from expanding collaboration between universities, startups, and industry leaders. Joint ventures are enabling faster commercialization of new chemistries. Intellectual property development around safer and eco-friendly electrolytes creates additional value. Expanding production facilities in Asia Pacific and North America strengthens the supply base. Growing venture capital interest in energy storage innovation adds further momentum to market opportunities.

Market Segmentation Analysis:

By type, organic electrolytes dominate due to their high compatibility with lithium-ion batteries and widespread commercial use. They provide superior voltage stability and efficiency, making them the preferred choice for automotive and consumer electronics applications. Inorganic electrolytes, while holding a smaller share, are gaining attention for their potential in next-generation solid-state batteries, where safety and performance improvements are critical. The Non Aqueous Electrolyte Market is expected to see both categories advancing as research expands toward higher energy density solutions.

- For example, a recent study demonstrated lab-scale lithium metal batteries using Ag‑coated garnet-type LLZTO solid electrolyte with a silver–carbon interlayer. These cells achieved 800 cycles at 1.6 mA/cm² and 25 °C, maintaining about 85% discharge capacity retention.

By application, lithium-ion batteries account for the largest share, driven by their extensive use in electric vehicles, portable electronics, and energy storage systems. It continues to gain strength from ongoing innovation in high-capacity cells. Sodium-ion batteries are emerging as a cost-effective alternative for stationary storage applications, supported by abundant raw material availability. Solid-state batteries represent a promising segment with strong R&D focus, though commercialization remains limited. Other battery technologies, including advanced hybrids, also contribute to niche demand across industrial uses.

- For instance, Stellantis and Factorial Energy have validated automotive-sized solid-state battery cells with 375 Wh/kg energy density and fast charging capabilities, signaling progress toward commercial solid-state EV batteries.

By end-use industry, automotive leads due to rapid electric vehicle adoption and government mandates for sustainable mobility. Consumer electronics follows with steady demand for compact and efficient devices, which require reliable electrolytes. Energy storage holds strong growth potential, supported by global renewable integration projects and grid modernization efforts. It is further supported by other industries, including aerospace and defense, which are exploring advanced energy solutions. Each segment plays a critical role in shaping the overall demand landscape and supporting long-term growth opportunities.

Segmentation:

By Type:

- Organic Electrolytes

- Inorganic Electrolytes

By Application:

- Lithium-ion Batteries

- Sodium-ion Batteries

- Solid-State Batteries

- Other Battery Technologies

By End-Use Industry:

- Automotive

- Consumer Electronics

- Energy Storage

- Other Industries

By Region:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis:

Asia Pacific dominates the Non Aqueous Electrolyte Market, accounting for 46% share in 2024. China leads the region with large-scale production of lithium-ion batteries supported by strong government policies. Japan and South Korea contribute significantly with advancements in EV battery technology and consumer electronics. It benefits from extensive supply chains and established manufacturing clusters that ensure consistent growth. The presence of leading automotive and electronics manufacturers further strengthens demand. Continuous investment in renewable integration projects positions the region as the primary hub for future market expansion.

North America holds 27% market share in 2024, driven by strong EV adoption and federal funding for energy storage projects. The United States remains the largest contributor due to large-scale investments in gigafactories and clean energy initiatives. Canada is expanding its renewable power capacity, supporting battery storage deployment. It gains momentum from strong private and public sector collaboration in advancing battery technologies. High demand for consumer electronics also supports market growth in the region. Strategic alliances between automakers and material suppliers ensure steady progress toward innovative electrolyte solutions.

Europe captures 21% share in 2024, with Germany, France, and the United Kingdom leading adoption through sustainability mandates and EV infrastructure expansion. The European Union’s strict regulations on emissions and recycling create strong demand for safe and eco-friendly electrolytes. It is also supported by government-backed projects that enhance renewable energy integration. Regional players are focusing on solid-state battery research to strengthen competitiveness. The remaining 6% share is held by Latin America and the Middle East & Africa, where markets are emerging gradually through renewable projects and early EV adoption. Growing investments in energy security and regional industrialization will expand opportunities in these developing regions.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Ampcera

- Electrovaya

- GS Yuasa International Ltd.

- LG Chem

- POSCO

- American Elements

- NEI Corporation

- Targray

- Amprius Technologies

- Mitsubishi Gas Chemical Company, Inc.

- Solid Power

- CAPCHEM

- Mitsui Chemicals, Inc.

- UBE Corporation

Competitive Analysis:

The Non Aqueous Electrolyte Market is highly competitive with the presence of global and regional players focusing on innovation, scalability, and partnerships. Leading companies emphasize advanced formulations that improve thermal stability, safety, and energy density to meet the rising demand from electric vehicles, consumer electronics, and energy storage. It is characterized by strategic investments in R&D, pilot projects, and large-scale manufacturing facilities. Key players are forming alliances with automakers, battery producers, and renewable energy developers to strengthen their market positions. Firms are also prioritizing sustainable chemistry and recycling initiatives to align with environmental regulations and customer expectations. Regional competitors in Asia Pacific dominate production due to integrated supply chains, while North American and European firms focus on high-performance solutions and solid-state technologies. Intense price competition, combined with rapid technological advancement, continues to shape the competitive dynamics of this growing market.

Recent Developments:

- In July 2025, Electrovaya launched multiple battery system products for robotic vehicle platforms developed in collaboration with three major OEM partners from the USA and Japan. These batteries feature long runtimes, extended life expectancy, and rapid wireless charging for 24/7 operations.

- In May 2025, Ampcera launched breakthrough nano sulfide solid electrolyte powders designed to enable next-generation high-performance all-solid-state batteries. Initial global shipments to solid-state battery makers have commenced, boosting the company’s momentum in the solid-state battery market and targeting applications in electric vehicles, consumer electronics,

- In May 2025, GS Yuasa announced a renewed sales launch for its high-performance battery series “ECO.R Revolution” tailored for vehicles with Idling Stop systems. The updated product achieves a balance of long life and high starting performance, enhancing the brand image of GS Yuasa’s automotive batteries.

Report Coverage:

The research report offers an in-depth analysis based on Type, Application and End-Use Industry. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Growing adoption of electric vehicles will expand demand for high-performance non-aqueous electrolytes across major markets.

- Development of solid-state batteries will create opportunities for advanced electrolyte formulations focused on safety and efficiency.

- Expansion of renewable energy projects will accelerate the need for reliable grid-scale energy storage using advanced electrolytes.

- Rising investments in R&D will drive innovations in safer, eco-friendly electrolyte chemistries tailored for emerging technologies.

- Strategic collaborations between automakers, energy firms, and chemical producers will strengthen supply chain resilience and innovation.

- Increasing focus on circular economy practices will encourage recycling and sustainable production of electrolyte materials.

- Asia Pacific will maintain leadership through strong battery manufacturing capabilities and government support for clean energy.

- North America will expand rapidly, supported by federal funding for EV adoption and grid modernization.

- Europe will strengthen its market presence through strict emission norms and investment in sustainable battery technologies.

- Emerging markets in Latin America and the Middle East & Africa will unlock growth opportunities through renewable integration.