Market Overview

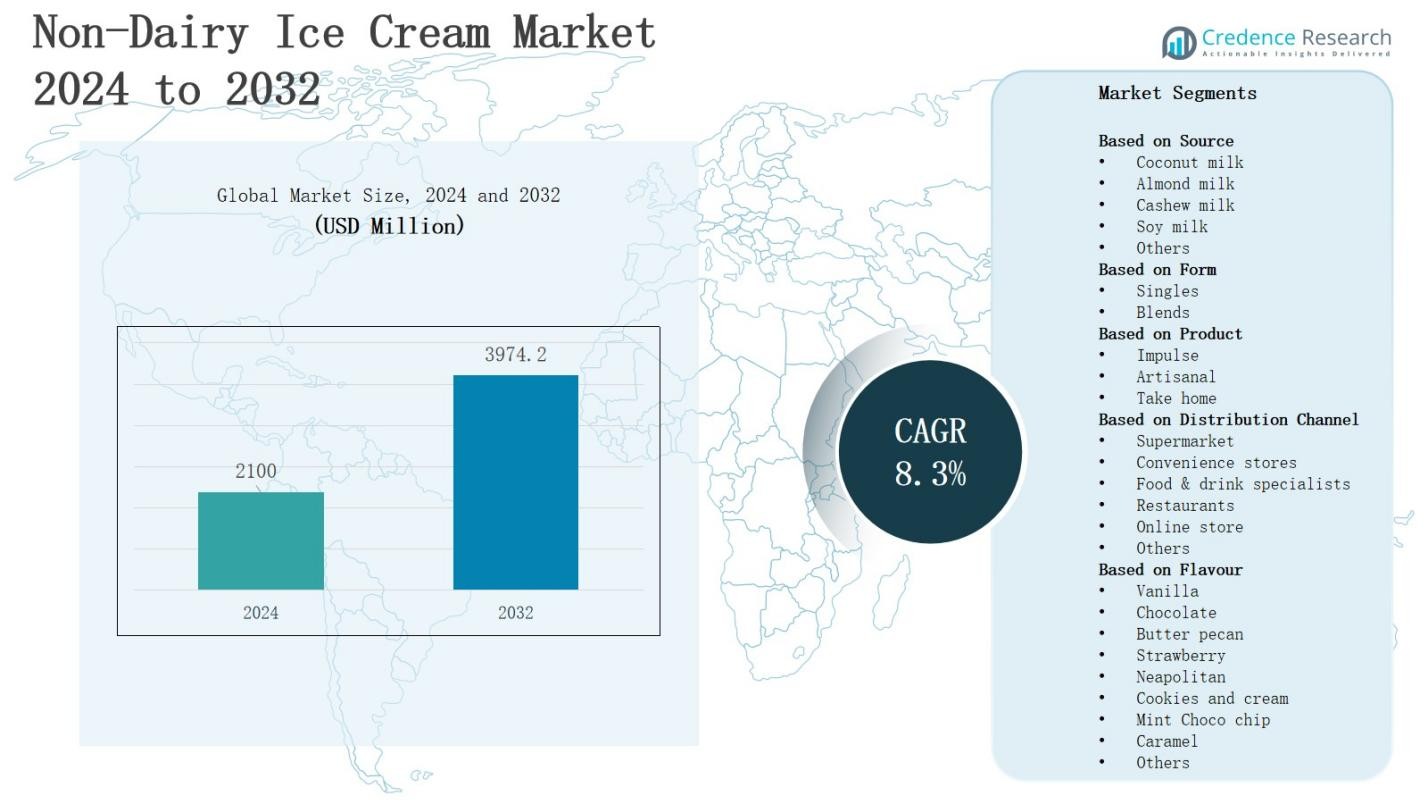

The Non-Dairy Ice Cream Market is projected to grow from USD 2100 million in 2024 to USD 3974.2 million by 2032, registering a CAGR of 8.3% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Non-Dairy Ice Cream Market Size 2024 |

USD 2100 Million |

| Non-Dairy Ice Cream Market, CAGR |

8.3% |

| Non-Dairy Ice Cream Market Size 2032 |

USD 3974.2 Million |

The non-dairy ice cream market is driven by rising consumer demand for plant-based alternatives, growing lactose intolerance cases, and increasing vegan lifestyles. Health-conscious consumers prefer dairy-free options with lower cholesterol and allergen-free benefits, boosting adoption across regions. Expanding product innovation, including flavors, textures, and protein-rich formulations, strengthens market appeal. Trends highlight the shift toward clean-label, organic, and sustainably sourced ingredients, as well as the use of alternative bases such as almond, coconut, oat, and soy milk. Premium offerings, eco-friendly packaging, and strong presence on e-commerce platforms further enhance growth and shape competitive dynamics in this market.

The non dairy ice cream market shows strong geographical diversity, led by North America with the largest share, followed by Europe and the rapidly growing Asia-Pacific region. Latin America and the Middle East & Africa are smaller but expanding markets supported by rising health awareness and modern retail growth. It is driven by leading players such as Danone, General Mills, Bliss Unlimited, Eden Creamery, NadaMoo, Swedish Glace, Dream, Over The Moo, Happy Cow, and The Booja-Booja, all competing through innovation, sustainability, and broad distribution networks.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The non dairy ice cream market will grow from USD 2100 million in 2024 to USD 3974.2 million by 2032, registering an 8.3% CAGR, driven by plant-based demand and vegan lifestyles.

- Coconut milk leads the source segment with 32% share in 2024, followed by almond milk at 26%, soy milk at 18%, cashew milk at 14%, and other sources, including oat, at 10%.

- Singles dominate the form segment with 61% share in 2024, reflecting consumer preference for consistency in taste and texture, while blends capture 39% share with rising adoption.

- Impulse products lead by product type with 45% share, followed by take-home formats at 37% and artisanal products at 18%, supported by growing demand for indulgent, premium, clean-label offerings.

- North America holds 38% share, Europe 27%, Asia-Pacific 22%, Latin America 7%, and Middle East & Africa 6%, with growth driven by awareness, retail expansion, and premium product innovations.

Market Drivers

Rising Demand for Plant-Based Alternatives

The non dairy ice cream market is expanding due to increasing adoption of plant-based diets. Consumers are choosing dairy-free options to align with vegan, vegetarian, and flexitarian lifestyles. It benefits from the growing perception that plant-based foods are healthier, offering lower fat and cholesterol levels. Companies are responding with diverse formulations using almond, oat, soy, and coconut bases. This broad variety attracts health-conscious buyers while meeting dietary restrictions effectively. The demand continues to strengthen global sales.

Health and Wellness Focus Among Consumers

The non dairy ice cream market is gaining traction due to rising concerns over lactose intolerance and dairy allergies. Consumers seek alternatives that avoid digestive discomfort while still delivering indulgence. It is increasingly positioned as a healthier option with fewer allergens and lower saturated fat levels. Manufacturers highlight added functional benefits such as protein or fiber content. This alignment with wellness trends enhances consumer trust. Growing awareness of balanced nutrition strengthens its competitive position in the frozen dessert sector.

- For instance, Halo Top Creamery introduced dairy‑free options made with coconut milk that offer lower calories and higher protein compared to many traditional ice creams.

Product Innovation and Flavor Diversification

The non dairy ice cream market benefits from continuous innovation in flavors, textures, and nutritional profiles. Manufacturers are introducing gourmet options and experimenting with natural sweeteners to meet diverse preferences. It is also witnessing growth in premium offerings with organic and clean-label ingredients. Flavor variety ranging from classic chocolate to exotic fruit blends attracts wider demographics. This product differentiation builds brand loyalty and consumer excitement. Expanding flavor portfolios drive repeat purchases across multiple retail and online channels.

- For instance, Coconut Bliss expanded its portfolio with flavors such as Dark Chocolate Salted Caramel made with organic coconut milk, responding to rising demand for both indulgent and clean‑label options.

Sustainability and Ethical Consumerism

The non dairy ice cream market is shaped by rising demand for eco-friendly and ethical products. Consumers value sustainable sourcing, recyclable packaging, and cruelty-free production practices. It appeals strongly to environmentally aware demographics that connect food choices with sustainability. Brands emphasizing transparency in sourcing and production are gaining a competitive advantage. Ethical positioning enhances brand image and consumer loyalty. This trend drives both niche and mainstream adoption, supporting long-term growth within global frozen dessert markets.

Market Trends

Innovation in Ingredients and Formulations

The non dairy ice cream market is witnessing rapid innovation in ingredients to meet evolving consumer expectations. Brands are developing products with oat, cashew, almond, soy, and coconut milk to replace traditional dairy bases. It benefits from increasing consumer demand for functional ingredients such as added protein, probiotics, and reduced sugar. Clean-label and organic formulations are gaining traction, reflecting consumer preference for transparency. These innovations expand market reach by aligning with health-focused and ethical purchasing behaviors.

- For instance, Van Leeuwen’s utilizes cashew and oat milk as base ingredients, creating rich flavors like pistachio and oat milk chocolate crunch with cookie dough, emphasizing smoothness and novel tastes.

Premiumization and Flavor Diversification

The non dairy ice cream market is experiencing strong growth from premiumization strategies adopted by leading brands. Companies are introducing gourmet flavors, unique textures, and indulgent inclusions such as nut clusters, fruit swirls, and plant-based chocolate. It is expanding appeal beyond traditional vegan consumers to mainstream buyers seeking luxury indulgence. Exotic flavor combinations and limited-edition launches create excitement among younger demographics. This trend strengthens brand positioning in retail and foodservice channels, driving repeat purchases and higher revenue streams.

- For instance, Ben & Jerry’s expanded their plant-based line with exotic flavors and mix-ins such as plant-based chocolate chunks and fruit swirls, targeting younger demographics with a focus on responsible sourcing and richer textures.

Expansion of Distribution Channels

The non dairy ice cream market is benefitting from wider availability across supermarkets, convenience stores, specialty outlets, and online platforms. Growing penetration in e-commerce, supported by delivery apps and subscription models, is fueling access and sales. It appeals strongly to urban consumers who value convenience and variety. Retailers are allocating larger shelf space to plant-based frozen desserts. Partnerships with cafes and restaurants further strengthen market presence. This diversification enhances visibility, improves accessibility, and sustains competitive growth momentum.

Sustainability and Ethical Branding

The non dairy ice cream market is increasingly shaped by rising consumer interest in sustainability and ethical sourcing. Brands emphasize recyclable packaging, carbon footprint reduction, and cruelty-free production processes to align with eco-conscious values. It resonates strongly with younger demographics who prioritize ethical consumption. Transparency in ingredient sourcing enhances consumer trust and loyalty. Companies adopting strong sustainability narratives are strengthening brand image globally. This focus is transforming purchasing decisions and driving broader acceptance of dairy-free frozen desserts.

Market Challenges Analysis

High Production Costs and Pricing Pressure

The non dairy ice cream market faces challenges due to high production costs and pricing disparities compared to conventional ice cream. Premium plant-based ingredients such as almond, cashew, and oat bases are often more expensive, raising overall manufacturing expenses. It struggles to achieve price parity, making products less accessible to price-sensitive consumers. Rising costs for packaging, logistics, and cold chain storage further add to the burden. This limits affordability and slows adoption in emerging markets where consumers prioritize cost-effective options.

Taste, Texture, and Consumer Acceptance Barriers

The non dairy ice cream market continues to face obstacles in delivering taste and texture comparable to traditional dairy products. Consumers often perceive differences in creaminess, flavor richness, and mouthfeel, which restricts repeat purchases. It requires continuous innovation to close this sensory gap and improve overall product experience. Brand loyalty is difficult to build when mainstream consumers hesitate to switch from dairy-based ice cream. Negative perceptions impact marketing efforts. Overcoming these barriers is critical to expanding global adoption.

Market Opportunities

Rising Demand in Emerging Economies

The non dairy ice cream market holds strong opportunities in emerging regions where rising disposable incomes and changing dietary preferences are reshaping consumption patterns. Growing middle-class populations in Asia-Pacific, Latin America, and the Middle East are driving higher demand for premium and health-focused frozen desserts. It benefits from increasing awareness of plant-based nutrition and the influence of Western dietary trends. Expanding retail infrastructure and online grocery platforms further boost accessibility. This creates new revenue streams and long-term growth potential.

Innovation and Customization Potential

The non dairy ice cream market offers opportunities through innovation in flavors, formats, and functional benefits. Consumers are showing interest in products with added protein, probiotics, and reduced sugar content. It also gains from rising demand for customized offerings that cater to dietary needs such as keto-friendly, gluten-free, and allergen-free options. Developing indulgent yet health-oriented products strengthens consumer appeal. Collaborations with foodservice outlets and co-branding initiatives expand visibility. These efforts enhance competitive positioning and drive global adoption rates.

Market Segmentation Analysis:

By Source

The non dairy ice cream market by source is dominated by coconut milk, holding around 32% share in 2024. Its creamy texture, wide availability, and consumer perception of being natural and allergen-friendly make it the most preferred base. Almond milk follows with 26% share, driven by its light taste and nutritional value. Soy milk accounts for 18% share, appealing to cost-sensitive buyers. Cashew milk captures 14% share, favored for premium offerings. Other sources contribute 10% share, including oat and rice milk innovations.

- For instance, Naturals Ice Cream in India is a pioneer of the popular Tender Coconut flavor, made with real malai from tender coconuts sourced locally.

By Form

In terms of form, singles lead the non dairy ice cream market with 61% share in 2024, as consumers prefer single-source bases for consistency in taste and texture. It benefits from strong popularity of coconut and almond milk products across mainstream retail shelves. Blends hold 39% share, gaining traction due to their ability to combine nutritional benefits and unique flavor profiles. Manufacturers are increasingly experimenting with blend-based recipes to attract health-conscious and adventurous consumers seeking novelty.

By Product

By product type, impulse products dominate the non dairy ice cream market with 45% share in 2024, driven by strong sales in convenience stores and quick-service outlets. Take-home formats follow closely with 37% share, supported by family consumption and availability in larger pack sizes through supermarkets and online channels. Artisanal products hold 18% share, reflecting rising demand for premium, handcrafted, and clean-label options. Growing consumer interest in indulgence and premiumization continues to push artisanal offerings into niche but expanding segments.

- For instance, Unilever expanded its Magnum Non-Dairy bars, a popular impulse purchase available through convenience channels and quick-service outlets.

Segments:

Based on Source

- Coconut milk

- Almond milk

- Cashew milk

- Soy milk

- Others

Based on Form

Based on Product

- Impulse

- Artisanal

- Take home

Based on Distribution Channel

- Supermarket

- Convenience stores

- Food & drink specialists

- Restaurants

- Online store

- Others

Based on Flavour

- Vanilla

- Chocolate

- Butter pecan

- Strawberry

- Neapolitan

- Cookies and cream

- Mint Choco chip

- Caramel

- Others

Based on the Geography:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis

North America

North America dominates the non dairy ice cream market with 38% share in 2024, driven by high consumer awareness and strong demand for plant-based foods. The region benefits from a well-established vegan community and wide retail availability across supermarkets, specialty stores, and online platforms. It gains momentum from innovation in flavors, clean-label products, and sustainable packaging. Rising lactose intolerance cases further fuel adoption. Strong presence of leading brands and investments in premium product development strengthen market growth across the United States and Canada.

Europe

Europe accounts for 27% share of the non dairy ice cream market in 2024, supported by rising health-consciousness and increasing preference for dairy-free lifestyles. The region shows strong demand in countries like Germany, the UK, and France, where consumers value sustainability and organic offerings. It benefits from strict food labeling regulations that encourage transparency and trust. Growth in artisanal and premium plant-based desserts enhances product acceptance. The market is further strengthened by expanding vegan populations and innovative retail distribution strategies.

Asia-Pacific

Asia-Pacific holds 22% share in the non dairy ice cream market in 2024, emerging as the fastest-growing regional segment. Rising disposable incomes, urbanization, and growing middle-class populations drive higher demand for healthier and premium desserts. It benefits from increasing lactose intolerance prevalence across China, India, and Southeast Asia. Global and local brands are expanding product portfolios to match regional taste preferences. Rapid growth of e-commerce and modern retail further accelerates sales. This region offers significant long-term growth potential.

Latin America

Latin America captures 7% share in the non dairy ice cream market in 2024, supported by increasing adoption of plant-based diets and influence from global food trends. Brazil and Mexico lead consumption, driven by younger demographics seeking healthier indulgence options. It faces challenges from higher product pricing compared to traditional ice cream, but rising awareness is creating opportunities. Expanding distribution networks and greater availability in retail outlets strengthen visibility. Growing interest in sustainable and ethical products boosts regional market growth.

Middle East & Africa

The Middle East & Africa account for 6% share in the non dairy ice cream market in 2024, with growth supported by increasing urban populations and rising health awareness. Demand is concentrated in Gulf countries where premium and imported brands dominate. It benefits from growing hospitality and foodservice sectors that introduce dairy-free desserts into menus. Limited cold-chain infrastructure poses a challenge, yet expanding modern retail helps improve accessibility. Consumer preference for lactose-free and healthier indulgence continues to strengthen adoption.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

Competitive Analysis

The non dairy ice cream market is highly competitive, characterized by strong brand positioning, continuous innovation, and expanding distribution strategies. Key players such as Danone, General Mills, Bliss Unlimited, Eden Creamery, NadaMoo, Swedish Glace, Dream, Over The Moo, Happy Cow, and The Booja-Booja compete by introducing diverse flavors, plant-based formulations, and premium offerings to capture wider consumer segments. It is shaped by increasing demand for clean-label, organic, and allergen-free products that align with health and sustainability trends. Companies are strengthening their presence across supermarkets, specialty stores, and online channels, while partnerships with foodservice outlets enhance visibility. Investment in product differentiation, marketing, and eco-friendly packaging is driving brand loyalty. Emerging regional players are challenging global leaders with locally tailored flavors and competitive pricing. Innovation in functional ingredients such as protein-enriched and low-sugar variants is further intensifying rivalry. The competitive landscape reflects a balance of global corporations leveraging scale advantages and niche brands focusing on authenticity, taste, and ethical sourcing, ensuring sustained dynamism across the industry.

Recent Developments

- In August 2025, Japanese food tech startup Kinish introduced The Rice Creamery, a rice-based plant ice cream brand with 60% less sugar and 62% lower greenhouse gas emissions.

- In early 2024, Perfect Day partnered with Unilever’s Breyers to unveil a lactose-free chocolate ice cream made with animal-free whey protein to promote sustainable dairy alternatives.

- In January 2025, Breyers introduced a new Non‑Dairy Chocolate ice cream made with an oat‑milk base, offering the classic creamy experience in a dairy‑free format.

- In January 2025, Ben & Jerry’s introduced a new Bohemian Raspberry non‑dairy flavor, expanding its dairy-free lineup with a fruity, indulgent offering.

Report Coverage

The research report offers an in-depth analysis based on Source, Form, Product, Distribution Channel, Flavour and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Rising vegan and flexitarian lifestyles will drive strong global demand for non dairy ice cream.

- Growing health awareness will increase preference for lactose-free, allergen-free, and low-cholesterol frozen dessert options.

- Product innovation in flavors, textures, and functional benefits will attract wider consumer demographics worldwide.

- Expansion of e-commerce platforms and subscription models will enhance consumer accessibility and brand visibility.

- Premium and artisanal offerings will strengthen positioning, catering to indulgent consumers seeking clean-label authenticity.

- Sustainability initiatives, including eco-friendly packaging and ethical sourcing, will shape long-term consumer loyalty patterns.

- Strategic partnerships with restaurants, cafes, and foodservice outlets will expand market penetration and distribution.

- Emerging economies will witness rising adoption driven by urbanization, disposable income, and modern retail growth.

- Technological advancements in plant-based formulations will improve taste, texture, and product acceptance among mainstream consumers.

- Competition among global leaders and regional players will intensify, encouraging continuous innovation and differentiation strategies.