North America Cardiovascular Drugs Market Overview:

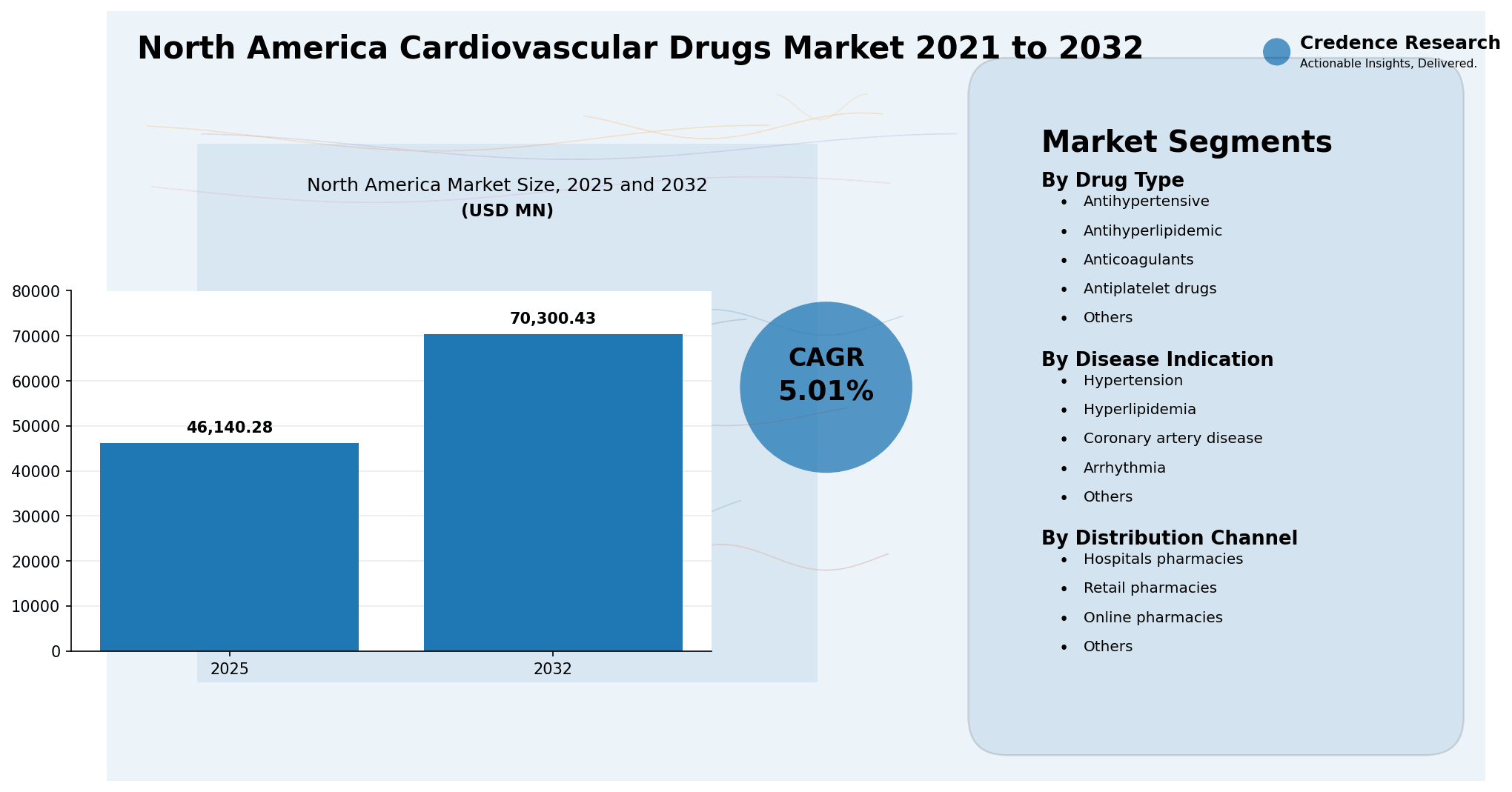

The North America Cardiovascular Drugs Market size was valued at USD 35,146.60 MN in 2021 and reached USD 46,140.28 MN in 2025. It is anticipated to reach USD 70,300.43 MN by 2032, growing at a CAGR of 5.01% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2021-2024 |

| Base Year |

2025 |

| Forecast Period |

2025-2032 |

| North America Cardiovascular Drugs Market Size 2025 |

USD 46,140.28 million |

| North America Cardiovascular Drugs Market, CAGR |

5.01% |

| North America Cardiovascular Drugs Market Size 2032 |

USD 70,300.43 million |

North America Cardiovascular Drugs Market Insights

- Market growth is supported by high cardiovascular disease burden, hypertension prevalence, hyperlipidemia management, anticoagulant use, aging demographics and broader access to chronic disease therapies.

- Antihypertensive holds a strong position because high blood pressure remains highly prevalent and requires long-term medication use across primary care, cardiology and hospital settings.

- Antihyperlipidemic drugs continue to gain relevance as LDL-C reduction remains central to cardiovascular risk management, especially among patients with coronary artery disease and hyperlipidemia.

- Retail Pharmacies remain a major distribution channel because cardiovascular drugs are commonly used for long-term outpatient treatment, prescription refills and chronic disease management.

North America Cardiovascular Drugs Market Segment Insights

By drug type

By drug type, Antihypertensive drugs held a strong position in 2025 because hypertension requires long-term treatment and frequent medication adjustment. Antihyperlipidemic drugs remain important because lipid control is central to reducing risk among patients with hyperlipidemia, coronary artery disease and broader atherosclerotic cardiovascular disease. Anticoagulants support demand across arrhythmia, stroke prevention and thromboembolic risk management. Antiplatelet Drugs remain relevant in coronary artery disease, post-stent care and secondary prevention. Others include heart failure drugs, pulmonary hypertension therapies, metabolic-cardiovascular therapies and specialty cardiovascular medicines. Growth across drug types will depend on clinical guideline adoption, generic availability, premium innovation and patient adherence.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By disease indication

By disease indication, Hypertension held the strongest position in 2025 because it affects a large share of adults and requires sustained pharmacological control. Hyperlipidemia remains a major indication because LDL-C reduction is central to preventing cardiovascular events. Coronary Artery Disease supports demand for antiplatelets, antihyperlipidemic drugs, beta blockers, ACE inhibitors and other secondary prevention therapies. Arrhythmia drives demand for anticoagulants, rhythm control drugs and rate control therapies, particularly in patients at risk of stroke. Others include heart failure, pulmonary arterial hypertension and cardiometabolic conditions that require cardiovascular drug intervention. Market growth will be shaped by diagnosis rates, treatment persistence and access to innovative therapies.

By distribution channel

By distribution channel, Retail Pharmacies held a strong position in 2025 because cardiovascular drugs are mostly used in outpatient chronic care. Patients frequently refill prescriptions for hypertension, hyperlipidemia, arrhythmia and coronary artery disease management through retail networks. Hospital Pharmacies remain important for acute cardiovascular care, inpatient drug administration, complex therapies and discharge prescriptions. Online Pharmacies are gaining gradual traction as patients seek convenience, digital refill management and home delivery for chronic medications. Others include specialty pharmacies, mail-order pharmacies and integrated payer-provider channels. Distribution channel growth will favor models that improve adherence, affordability and continuity of therapy.

Key market drivers

High cardiovascular disease burden

High cardiovascular disease burden represents a major growth driver for the North America Cardiovascular Drugs Market. Cardiovascular conditions require long-term medication use across primary prevention, secondary prevention and advanced disease management. Demand remains strong for Antihypertensive, Antihyperlipidemic, Anticoagulants and Antiplatelet Drugs because many patients require multiple therapies to control blood pressure, lipids, clotting risk and coronary complications.

CDC reports that heart disease is the leading cause of death in the U.S. and that 919,032 people died from cardiovascular disease in 2023, equal to about one in every three deaths. This clinical burden supports sustained drug utilization across hospitals, retail pharmacies and chronic care settings. Market growth will remain tied to early diagnosis, adherence programs, broader guideline-based treatment and access to innovative therapies.

Hypertension prevalence and treatment intensification

Hypertension prevalence and treatment intensification support strong demand for cardiovascular drugs. Antihypertensive therapies remain essential because high blood pressure is both common and frequently uncontrolled. Supporting statement: CDC reports that nearly half of U.S. adults have high blood pressure, representing 48.1% or 119.9 million adults, and only 22.5% of adults with high blood pressure have it under control. This creates steady demand for first-line therapies, combination products and resistant hypertension treatment options.

FDA approved TRYVIO based on evidence from a 730-patient trial in adults with hypertension despite taking at least three blood pressure drugs, with about 32% of patients enrolled at North American sites. The driver will remain central as health systems focus on better blood pressure control.

Hyperlipidemia management and LDL-C innovation

Hyperlipidemia management and LDL-C innovation are strengthening demand for Antihyperlipidemic drugs. Statins remain foundational, but many high-risk patients require additional lipid-lowering therapies to reach LDL-C targets. Supporting statement from key company data: Novartis reported full-year 2025 Leqvio sales of USD 1,198 million, up 59%, within its cardiovascular, renal and metabolic portfolio.

Merck reported that nearly 70% of people with ASCVD treated with lipid-lowering therapies do not reach target LDL-C levels, while its investigational oral PCSK9 inhibitor enlicitide is designed to deliver LDL-C reduction through a daily pill format. This driver supports premium innovation, adherence-focused therapies and long-term cholesterol management.

Arrhythmia and anticoagulant demand

Arrhythmia and anticoagulant demand support market growth because atrial fibrillation increases stroke risk and often requires long-term blood-thinning therapy. Anticoagulants are widely used in patients with arrhythmia, thromboembolic risk and selected cardiovascular comorbidities.

CDC estimates that 12.1 million people in the U.S. will have atrial fibrillation by 2050 and notes that treatment can include blood-thinning medicine to prevent clots and reduce stroke risk. This supports sustained demand for oral anticoagulants, hospital-based initiation and retail pharmacy refills. The driver will remain important as aging populations increase arrhythmia prevalence and chronic cardiovascular medication use.

Key Trends and Opportunities

Combination therapy and adherence-focused treatment gain relevance

Combination therapy and adherence-focused treatment are becoming major opportunities because many cardiovascular patients require multiple drugs to control blood pressure, lipids, clotting risk and coronary complications. Fixed-dose combinations, longer-acting therapies and simplified dosing can improve treatment persistence. Retail Pharmacies and Online Pharmacies can also support adherence through refill reminders, medication synchronization and home delivery. Payers and providers increasingly value therapies that improve long-term control and reduce avoidable cardiovascular events. The opportunity is strongest in Hypertension, Hyperlipidemia and Coronary Artery Disease. Companies that combine clinical efficacy with adherence support will gain stronger market access.

Advanced lipid-lowering therapies expand

Advanced lipid-lowering therapies are expanding as drug developers address patients who do not reach LDL-C goals with standard therapy. Injectable and oral PCSK9 approaches, small interfering RNA therapies and novel lipid pathways are creating new premium opportunities. These therapies are relevant for patients with Hyperlipidemia, Coronary Artery Disease and high atherosclerotic cardiovascular risk. Innovation can also improve adherence when therapies require less frequent administration or offer oral convenience. Adoption will depend on payer coverage, outcomes evidence and physician familiarity. This trend will support premium growth within Antihyperlipidemic drugs through 2032.

Digital pharmacy and chronic care models rise

Digital pharmacy and chronic care models are rising as patients manage cardiovascular diseases over long periods. Online Pharmacies, mail-order channels and integrated digital care platforms can improve refill continuity, adherence tracking and patient convenience. Retail pharmacies are also expanding chronic disease support through medication reviews, blood pressure checks and patient counseling. These services matter because poor adherence weakens blood pressure and lipid control. Digital models can also help payers and providers identify patients at risk of therapy gaps. The trend will strengthen distribution channel diversification while retail and hospital pharmacies remain central.

Key Market Challenges

Generic competition and pricing pressure

Generic competition and pricing pressure remain key challenges for the North America Cardiovascular Drugs Market. Many cardiovascular drug classes have mature therapies with established generic alternatives. Generics support affordability but limit revenue growth for branded products unless companies offer clear clinical differentiation. Payers often encourage low-cost options before premium therapies, especially in common conditions such as Hypertension and Hyperlipidemia. Branded manufacturers must prove outcome benefits, adherence advantages or patient-specific value to secure coverage. This challenge will remain significant across antiplatelets, antihypertensives and selected lipid-lowering therapies.

Patient adherence and long-term persistence

Patient adherence and long-term persistence create major barriers to effective cardiovascular drug use. Many patients take cardiovascular medicines for years, but asymptomatic conditions such as hypertension and hyperlipidemia can reduce urgency and consistency. Missed doses, cost barriers, side effects and regimen complexity can weaken treatment outcomes. Providers and pharmacies must support counseling, refill reminders and therapy simplification. Drug developers can also improve adherence through fixed-dose combinations and longer-acting therapies. Market growth depends not only on prescriptions but also on sustained patient use.

Reimbursement scrutiny for premium therapies

Reimbursement scrutiny for premium therapies can slow adoption of newer cardiovascular drugs. Advanced lipid-lowering therapies, pulmonary hypertension drugs and novel cardiovascular products often carry higher costs than generic standard-of-care therapies. Payers require evidence of clinical value, cardiovascular event reduction, mortality benefit or strong risk-stratified use. Prior authorization can delay patient access and increase administrative burden for prescribers. Manufacturers must invest in outcomes evidence, patient support and health economic data. Market access will remain a critical challenge for premium cardiovascular innovation.

Regional Analysis

United States

The United States leads the North America Cardiovascular Drugs Market due to its large treated patient population, high cardiovascular disease burden, broad insurance coverage and strong adoption of branded and generic cardiovascular therapies. Demand is strong across Hypertension, Hyperlipidemia, Coronary Artery Disease and Arrhythmia. Retail Pharmacies dominate chronic refill activity, while Hospital Pharmacies support acute cardiovascular care, inpatient anticoagulation and complex specialty treatments. The U.S. also drives premium innovation through advanced lipid-lowering therapies, pulmonary hypertension drugs and heart failure treatments. Drug companies prioritize the U.S. for launches and market access activity because it remains the largest revenue contributor in North America.

Canada

Canada represents a steady cardiovascular drugs market supported by public health coverage, primary care networks, hospital systems and guideline-based chronic disease management. Demand is strong across Antihypertensive, Antihyperlipidemic, Anticoagulants and Antiplatelet Drugs. Retail Pharmacies play a key role in medication access, adherence support and refill management. Hospital Pharmacies support acute coronary events, inpatient anticoagulation and specialty cardiovascular therapy use. Market access depends on health technology assessments, provincial reimbursement and formulary decisions. Growth will remain steady as aging demographics and cardiovascular risk factors continue to shape drug utilization.

Mexico

Mexico offers a smaller but gradually expanding market within North America. Demand is supported by rising chronic disease burden, private health care expansion, retail pharmacy access and broader diagnosis of Hypertension, Hyperlipidemia and Coronary Artery Disease. Retail Pharmacies remain highly important because many patients access chronic cardiovascular drugs through community-based channels. Hospital Pharmacies support acute care and specialist cardiovascular treatment. Affordability remains a key issue, which increases the role of generic drugs and lower-cost branded options. Growth will depend on access expansion, patient adherence, physician prescribing patterns and public-private health care investment.

Report Attribute Details

| Report Attribute |

Details |

| Historical Period |

2021–2024 |

| Base Year |

2025 |

| Forecast Period |

2025–2032 |

| Market Size in 2021 |

USD 35,146.60 MN |

| Market Size in 2025 |

USD 46,140.28 MN |

| Market Size in 2032 |

USD 70,300.43 MN |

| CAGR |

5.01% |

| Segments Covered |

Drug Type, Disease Indication, Distribution Channel and Geography |

| Key Companies Covered |

Pfizer Inc., Bayer AG, Janssen Pharmaceuticals, Inc., AstraZeneca, Sanofi, Novartis AG, Merck & Co., Inc., Gilead Sciences, Inc., F. Hoffmann-La Roche Ltd, Cipla Ltd., Sun Pharmaceutical Limited and Lupin Limited |

North America Cardiovascular Drugs Market Segmentations

By Drug Type

- Antihypertensive

- Antihyperlipidemic

- Anticoagulants

- Antiplatelet Drugs

- Others

By Disease Indication

- Hypertension

- Hyperlipidemia

- Coronary Artery Disease

- Arrhythmia

- Others

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Others

Key Players

- Pfizer Inc.

- Bayer AG

- Janssen Pharmaceuticals, Inc.

- AstraZeneca

- Sanofi

- Novartis AG

- Merck & Co., Inc.

- Gilead Sciences, Inc.

- F. Hoffmann-La Roche Ltd

- Cipla Ltd.

- Sun Pharmaceutical Limited

- Lupin Limited

Recent Developments

- In July 2025, Bayer announced U.S. FDA approval of finerenone for adults with heart failure and LVEF of 40% or higher, with the indication reducing risk of cardiovascular death, hospitalization for heart failure and urgent heart failure visits.

- In March 2024, FDA approved Merck’s WINREVAIR for adults with pulmonary arterial hypertension to increase exercise capacity, improve functional class and reduce clinical worsening.

- In 2025, Novartis reported Leqvio full-year sales of USD 1,198 million, up 59%, highlighting continued momentum in advanced lipid-lowering therapy.

- In March 2026, Merck reported that its investigational oral PCSK9 inhibitor enlicitide demonstrated greater LDL-C reductions at eight weeks versus guideline-recommended oral non-statin therapies when added to background statins.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Report Coverage

The research report offers an in-depth analysis based on drug type, disease indication, distribution channel and geography. It details leading market players, providing an overview of their business positioning, cardiovascular portfolios, market access strategies, generic and branded product roles and strategic relevance in the North America Cardiovascular Drugs Market. The report includes insights into the competitive environment, market trends, growth drivers, restraints and opportunities. It also examines cardiovascular disease burden, hypertension control, lipid management, anticoagulant use, chronic refill behavior, advanced therapy adoption and pharmacy channel evolution as major factors shaping market development. The report assesses the impact of generic competition, patient adherence, reimbursement scrutiny and long-term therapy persistence on market growth. It provides strategic recommendations for pharmaceutical companies, hospital systems, retail pharmacy networks, online pharmacies, payers, distributors, investors and new entrants seeking to navigate North America’s cardiovascular drugs ecosystem.

Future Outlook

- Demand for cardiovascular drugs will continue to rise as chronic disease prevalence, aging demographics and long-term medication needs expand across North America.

- Antihypertensive drugs will remain a leading category because high blood pressure affects a large adult population and requires sustained control.

- Antihyperlipidemic therapies will gain further importance as physicians intensify LDL-C management in high-risk patients.

- Anticoagulants will remain critical for arrhythmia and stroke-risk management, especially in atrial fibrillation patients.

- Antiplatelet Drugs will continue to support secondary prevention and coronary artery disease management.

- Retail Pharmacies will remain central to chronic cardiovascular medication access and refill continuity.

- Hospital Pharmacies will remain important for acute cardiovascular events, inpatient treatment and complex therapy initiation.

- Online Pharmacies will gain relevance as chronic medication refill management shifts toward digital convenience.

- Advanced lipid-lowering and resistant hypertension therapies will create premium growth opportunities.

- Competition will increase as companies compete on clinical outcomes, pricing, adherence support, payer access, differentiated formulations and patient assistance programs.