Market Overview

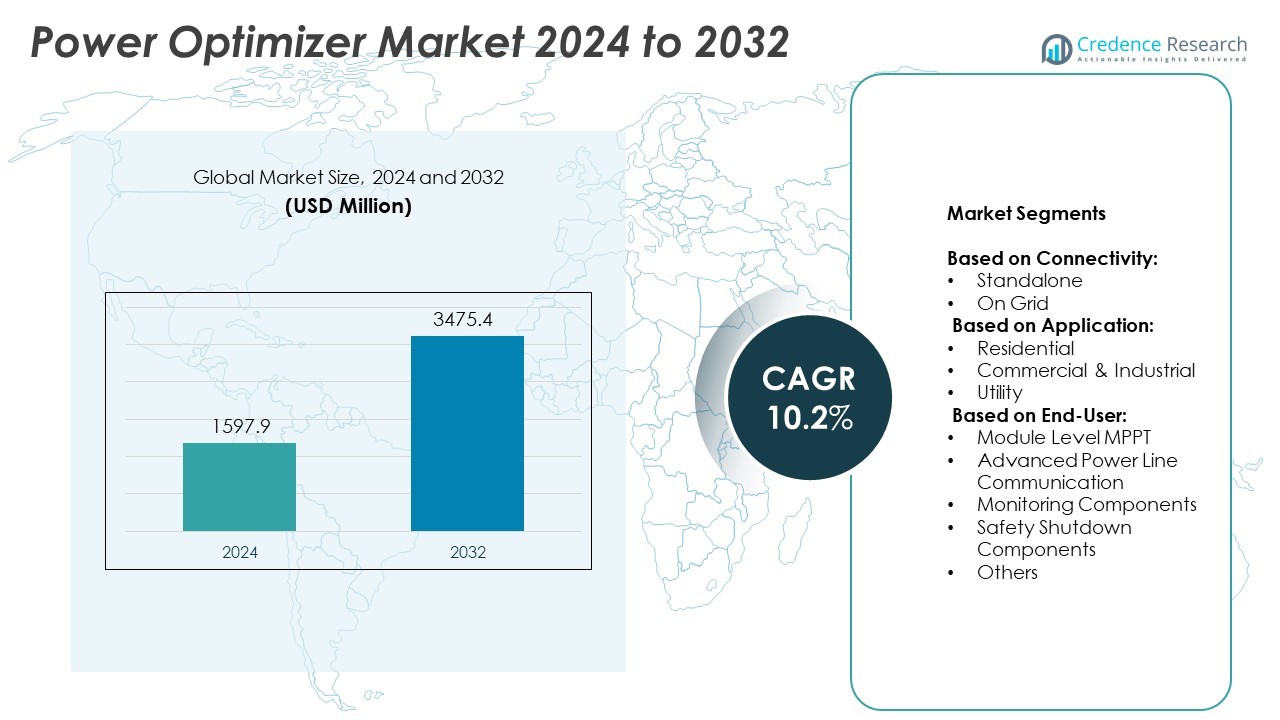

The Power Optimizer Market size was valued at USD 1,597.9 million in 2024 and is anticipated to reach USD 3,475.4 million by 2032, at a CAGR of 10.2% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Power Optimizer Market Size 2024 |

USD 1,597.9 Million |

| Power Optimizer Market, CAGR |

10.2% |

| Power Optimizer Market Size 2032 |

USD 3,475.4 Million |

The Power Optimizer market advances through strong drivers and evolving trends that highlight its critical role in solar energy systems. Rising adoption of residential, commercial, and utility-scale solar projects, combined with government incentives and strict safety regulations, accelerates demand. It gains momentum from the growing need for higher energy efficiency, cost savings, and compliance with rapid shutdown requirements. Trends emphasize integration with smart grids, IoT-enabled monitoring platforms, and hybrid solutions linking storage and electric vehicle charging

The Power Optimizer market demonstrates strong geographical presence across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with each region advancing adoption through renewable energy programs and supportive policies. It reflects robust demand in mature markets with established solar infrastructure and rising growth in emerging economies pursuing clean energy transitions. Key players shaping the industry include SolarEdge Technologies Inc., Tigo Energy, Huawei Technologies Co., Ltd., and Fronius International GmbH, all driving innovation and global competitiveness.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Power Optimizer market was valued at USD 1,597.9 million in 2024 and is projected to reach USD 3,475.4 million by 2032, growing at a CAGR of 10.2% between 2024 and 2032.

- Rising solar installations across residential, commercial, and utility-scale projects drive steady adoption, supported by government incentives, renewable energy mandates, and growing demand for energy-efficient technologies.

- Key trends highlight integration with smart grids, IoT-enabled monitoring platforms, and hybrid systems that connect solar generation with energy storage and electric vehicle charging infrastructure.

- The market reflects moderate concentration, with leading players focusing on advanced module-level optimization, cost efficiency, and compliance with safety regulations, while regional players strengthen niche markets through innovation.

- High initial installation costs, technical complexity, and supply chain challenges associated with semiconductors and electronic components act as key restraints for broader adoption in cost-sensitive markets.

- North America leads in adoption due to strong regulatory frameworks and advanced solar infrastructure, while Europe emphasizes carbon reduction goals and Asia-Pacific experiences rapid growth through large-scale solar programs in China, Japan, and India.

- Industry leaders such as SolarEdge Technologies Inc., Tigo Energy, Huawei Technologies, and Fronius International GmbH continue to shape the competitive landscape through product innovation, partnerships, and expansion into emerging markets.

Market Drivers

Rising Solar Energy Adoption and Grid Integration Needs

The Power Optimizer market advances strongly due to the rapid expansion of solar energy installations across residential, commercial, and utility-scale projects. Governments enforce renewable energy targets and incentives that accelerate deployment. It enables higher energy yields from photovoltaic systems by addressing mismatch losses and shading effects. Grid modernization initiatives demand advanced technologies that ensure stable integration of variable renewable sources. Rising energy demand in emerging economies further strengthens adoption. The combination of policy support and technological reliability makes power optimizers an essential component of solar projects.

- For instance, Enphase Energy announced that a 2 MW commercial installation deployed 3,200 IQ8P‑3P microinverters, estimated to generate over 3,800,000 kWh annually offset much of the school’s electricity

Growing Focus on Energy Efficiency and Cost Reduction

Energy efficiency remains a critical driver for the Power Optimizer market as consumers and enterprises seek to lower operational costs. It enhances module-level performance, ensuring maximum power output even under partial shading. Cost-sensitive sectors adopt power optimizers to reduce long-term electricity bills. Governments promote net metering and tariff reforms, reinforcing demand for optimized solar output. Large-scale adoption in commercial rooftops underscores the shift toward efficient energy management. The technology improves overall return on investment for solar projects.

- For instance, Enphase Energy has shipped a total of 45 million microinverters and its products are installed in 2 million homes across 135 countries. This volume reflects strong demand driven by energy‑efficiency benefits perceived across residential and commercial segments.

Technological Advancements in Smart Solar Solutions

Continuous innovation strengthens the Power Optimizer market by integrating digital monitoring and advanced analytics. Smart modules equipped with optimizers allow real-time performance tracking and predictive maintenance. It improves system reliability and minimizes downtime through early fault detection. Manufacturers introduce compact and efficient designs that lower installation complexity. Integration with IoT and AI-based platforms enhances decision-making for energy use. The market reflects strong demand for intelligent energy solutions across both developed and developing regions.

Supportive Regulatory Policies and Sustainability Goals

Regulatory frameworks drive the Power Optimizer market through strict renewable portfolio standards and carbon reduction mandates. It aligns with global commitments to decarbonization and sustainability. Financial incentives, tax credits, and subsidy schemes create favorable investment conditions. Utility companies encourage distributed generation by supporting advanced inverter and optimizer adoption. The technology also addresses compliance with safety standards, including rapid shutdown requirements. These regulatory and environmental priorities reinforce long-term growth prospects for the market.

Market Trends

Increasing Integration with Smart Energy Management Systems

The Power Optimizer market shows a clear trend toward integration with smart energy management platforms. Utilities and enterprises adopt solutions that allow seamless monitoring, control, and optimization of solar energy. It enables users to balance energy generation and consumption through real-time data analytics. Advanced communication protocols support connectivity with inverters, storage units, and grid systems. The growing adoption of smart homes and commercial energy management tools strengthens demand. This integration positions power optimizers as a critical element in intelligent solar ecosystems.

- For instance, Huawei’s Smart Module Controller solution supports real-time module‑level monitoring, with the capability to recognize and display module-wise layout in just 5 seconds, enabling rapid fault diagnostics and reducing maintenance time and costs

Expansion of Utility-Scale Solar Projects with Optimizer Adoption

The Power Optimizer market benefits from the rising share of utility-scale solar projects worldwide. Large-scale installations require enhanced efficiency and reliability to meet grid stability needs. It ensures module-level performance in challenging conditions such as partial shading or irregular terrain. Project developers deploy optimizers to secure higher returns and minimize downtime. Countries with aggressive renewable energy targets invest heavily in scalable technologies that optimize large solar plants. The trend underscores the transition from small-scale adoption to broader utility deployment.

- For instance, Enphase produces microinverters at two U.S. manufacturing facilities, located in South Carolina and Texas, with a combined capacity of 20 million units per year, enough to power over a million homes. These facilities support thousands of jobs, bolster U.S. energy independence, and contribute to a cleaner environment.

Rising Demand for Module-Level Monitoring and Safety Features

Safety and monitoring remain dominant trends in the Power Optimizer market, driven by stricter regulatory standards. It supports rapid shutdown compliance for fire safety in residential and commercial installations. Real-time monitoring helps detect faults early, reducing maintenance costs and improving operational security. Consumers favor solutions that provide transparency in energy generation and system performance. Manufacturers focus on advanced monitoring platforms that simplify remote oversight. The demand for higher safety standards accelerates the adoption of optimizers across diverse projects.

Growing Emphasis on Technological Miniaturization and Cost Efficiency

Manufacturers in the Power Optimizer market increasingly prioritize compact, lightweight, and cost-effective designs. It reduces installation complexity and improves compatibility with various photovoltaic modules. Production advancements drive down component costs, making optimizers accessible to broader markets. The shift supports widespread adoption in both emerging and mature economies. Companies innovate to balance affordability with performance, reinforcing long-term competitiveness. The emphasis on miniaturization and efficiency reflects a broader industry focus on sustainable and scalable solar technology.

Market Challenges Analysis

High Initial Costs and Complex Installation Requirements

The Power Optimizer market faces challenges linked to high upfront investment and installation complexity. Many residential and small commercial customers remain cautious about adopting optimizers due to added costs compared to traditional string inverters. It requires skilled labor for installation, which increases project expenses in regions with limited technical expertise. Complex wiring and module-level deployment extend installation timelines, slowing adoption in cost-sensitive markets. Limited awareness among end users about long-term efficiency benefits further constrains growth. The balance between short-term expenses and long-term savings remains a key obstacle for wider adoption.

Reliability Concerns and Supply Chain Disruptions

Technical reliability and supply chain stability create significant hurdles for the Power Optimizer market. Harsh environmental conditions raise concerns about durability and long-term performance of optimizers in large installations. It also faces risks of component failures that may impact entire system efficiency. Global supply chain disruptions, driven by raw material shortages and geopolitical uncertainties, restrict timely availability. Manufacturers struggle to maintain consistent production schedules under fluctuating costs of semiconductors and electronic components. These reliability and supply chain challenges pose long-term risks that require strategic mitigation through innovation and diversified sourcing.

Market Opportunities

Expansion of Renewable Energy Infrastructure and Distributed Generation

The Power Optimizer market holds significant opportunities through the rapid expansion of renewable energy infrastructure across global economies. Distributed generation models, including rooftop solar and community solar projects, require optimized performance at the module level. It enhances energy yield and ensures consistent output, making it a preferred choice for both residential and commercial applications. Emerging economies with strong renewable energy targets present untapped potential for large-scale adoption. Government incentives, favorable policies, and financing programs further stimulate demand. The alignment of power optimizers with long-term sustainability goals strengthens their role in future energy ecosystems.

Integration with Energy Storage and Electric Vehicle Charging Systems

Growing investment in energy storage and electric vehicle charging networks creates new avenues for the Power Optimizer market. Coupling optimizers with storage systems maximizes efficiency by managing power flows more effectively. It supports advanced energy management strategies that balance demand and supply within decentralized grids. The rise of EV adoption drives integration of solar with charging infrastructure, where optimizers secure higher reliability and system stability. Technological innovation around hybrid solutions that combine storage, solar, and mobility enhances growth prospects. The convergence of these sectors ensures broader adoption of optimizers in next-generation clean energy systems.

Market Segmentation Analysis:

By Connectivity:

Standalone and on-grid solutions. Standalone optimizers serve off-grid and hybrid systems where independence from centralized grids is crucial. It ensures consistent power generation in remote areas with weak or absent grid networks. On-grid optimizers dominate due to widespread integration with residential rooftops, commercial facilities, and large-scale solar farms. Their ability to enhance efficiency while complying with grid safety regulations strengthens adoption. Growing demand for smart grid infrastructure further reinforces the on-grid segment.

- For instance, while case‑specific yield gains vary, a detailed field study using selective deployment of power optimizers (SDPO) in shaded residential systems showed an annual energy yield increase of 1–2% compared to unoptimized reference systems—a modest gain that may not always justify added cost and complexity

By Application:

The Power Optimizer market segments into residential, commercial and industrial, and utility-scale projects. Residential installations benefit from optimizers by addressing shading and mismatch losses, improving household solar yields. It supports commercial and industrial sectors where operational cost savings and reliability remain priorities. Utility-scale projects deploy optimizers to secure stable integration with large solar plants and grid networks. Growing emphasis on high-return renewable energy investments accelerates adoption across all applications. The shift toward decentralized generation strengthens demand across these segments.

- For instance, SolarEdge reported that its DC-optimized residential systems were installed in over 3 million homes globally by 2024, with more than 3.3 million inverters and 89 million power optimizers shipped, enabling panel-level optimization and enhanced production across varying rooftops.

By End-User:

The Power Optimizer market categorizes into module level MPPT, advanced power line communication, monitoring components, safety shutdown components, and others. Module level MPPT leads due to its ability to maximize energy production at the individual panel level. It drives efficiency gains that appeal to both residential and utility-scale projects. Advanced power line communication enhances connectivity, enabling data transmission and system coordination across complex installations. Monitoring components ensure predictive maintenance and performance transparency, while safety shutdown components meet fire safety and regulatory requirements. Other solutions, including hybrid features, expand flexibility and widen deployment options. The diversity of these end-user categories reflects broad adoption across varying customer needs and project scales.

Segments:

Based on Connectivity:

Based on Application:

- Residential

- Commercial & Industrial

- Utility

Based on End-User:

- Module Level MPPT

- Advanced Power Line Communication

- Monitoring Components

- Safety Shutdown Components

- Others

Based on the Geography:

- North America

- Europe

- Germany

- France

- UK.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- The Rest of the Middle East and Africa

Regional Analysis

North America

North America holds the leading position in the Power Optimizer market with a market share of 35%. The region benefits from strong government incentives, tax credits, and renewable portfolio standards that promote solar adoption across residential, commercial, and utility projects. It advances rapidly due to mature infrastructure and high awareness among consumers about energy efficiency. The United States drives the majority of demand, supported by state-level solar programs and rapid shutdown regulations that require module-level safety components. Canada also contributes through increased investments in renewable projects across provinces with ambitious decarbonization goals. It remains a strong hub for technological innovation, with leading manufacturers and integrators focusing on advanced monitoring and grid integration features. The presence of established players and a favorable policy landscape reinforce North America’s dominance in this sector.

Europe

Europe accounts for 28% of the Power Optimizer market, supported by strict carbon reduction policies and ambitious renewable energy directives. Countries such as Germany, Italy, France, and Spain drive large-scale solar deployments under national clean energy targets. It benefits from the European Union’s Green Deal, which emphasizes decarbonization and distributed generation. Residential rooftops and commercial facilities adopt optimizers to comply with fire safety and grid integration standards. The region also invests heavily in research collaborations to advance module-level optimization and monitoring technologies. Growing focus on energy independence strengthens adoption, particularly in Eastern European countries seeking to reduce reliance on fossil fuel imports. It continues to position power optimizers as a key technology in achieving Europe’s long-term sustainability goals.

Asia-Pacific

Asia-Pacific secures 25% of the Power Optimizer market, driven by rapid urbanization, industrial growth, and aggressive renewable energy targets. China leads the region through massive solar deployments backed by state policies and large-scale utility projects. Japan demonstrates strong demand in residential rooftops, encouraged by net metering schemes and advanced safety standards. India contributes through expanding solar parks and government-backed distributed generation programs that promote module-level efficiency. It also benefits from rising demand across Southeast Asian countries where electrification and rural solar access create strong opportunities. The availability of low-cost manufacturing further supports adoption by lowering system costs. The region’s fast-growing energy demand ensures that power optimizers remain critical to strengthening renewable energy reliability and performance.

Latin America

Latin America represents 7% of the Power Optimizer market, with growth concentrated in Brazil, Mexico, and Chile. National programs promoting solar rooftops and utility-scale plants stimulate demand for optimization technologies. It supports strong adoption in Brazil’s residential and commercial sectors, where distributed solar systems are expanding rapidly. Mexico’s energy reforms encourage integration of advanced technologies for grid stability and reliability. Chile drives large-scale utility projects in the Atacama Desert, where high solar irradiation strengthens the case for efficient optimization solutions. Limited awareness and financing constraints slow adoption across smaller markets, but government-backed incentives and falling equipment costs are expected to improve penetration. It positions Latin America as a promising growth market despite existing challenges.

Middle East & Africa

The Middle East & Africa region accounts for 5% of the Power Optimizer market, driven by large utility-scale projects and emerging residential adoption. The Middle East invests heavily in renewable diversification programs, with countries like the UAE and Saudi Arabia prioritizing solar energy in national energy strategies. Africa demonstrates rising potential, with South Africa and Morocco deploying solar plants to improve energy access and grid stability. It faces challenges in financing and technical expertise, which limit widespread adoption in rural areas. However, international partnerships and foreign investments strengthen the pipeline of solar projects across the region. Growing energy demand, abundant sunlight, and ambitious clean energy commitments ensure long-term opportunities for optimizers. The region is gradually expanding its role in the global market with steady project development.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- SolarEdge Technologies Inc.

- Fronius International GmbH

- Ampt, LLC

- Infineon Technologies AG

- Alencon Systems, LLC

- Tigo Energy, Inc.

- Huawei Technologies Co., Ltd.

- ferroamp

- PCE Process Control Electronic GmbH

- Altenergy Power System Inc.

Competitive Analysis

The leading players in the Power Optimizer market include SolarEdge Technologies Inc., Fronius International GmbH, Ampt, LLC, Infineon Technologies AG, Alencon Systems, LLC, Tigo Energy, Inc., Huawei Technologies Co., Ltd., ferroamp, PCE Process Control Electronic GmbH, and Altenergy Power System Inc.These companies drive market growth through strong portfolios, technological advancements, and global reach. One major area of competition lies in innovation, with firms investing in advanced module-level power electronics that deliver higher efficiency, improved safety, and intelligent monitoring capabilities. Strategic partnerships with solar module manufacturers and inverter suppliers expand their market footprint and create integrated solutions that enhance system performance. Global expansion strategies are evident, with players targeting emerging economies where solar deployment is accelerating, supported by favorable government incentives. Competition also intensifies in pricing, as companies aim to make optimizers more accessible in cost-sensitive markets while balancing profitability. Continuous investment in research and development secures technological differentiation, while after-sales support and service networks strengthen customer loyalty. The competitive environment remains dynamic, shaped by regulatory changes, demand for distributed generation, and integration with smart energy management platforms. These factors ensure that competition fosters sustained innovation and broader adoption of power optimizers worldwide.

Recent Developments

- In April 30, 2025, Tigo released a software update for its Energy Intelligence (EI) platform, enhancing system sorting, optimizing PPL (Power Point Limiting) settings, introducing off‑grid system support, and improving the user interface and overall experience.

- In November 2024, SolarEdge announced plans to shut down its energy storage unit and lay off approximately 12% of its workforce—nearly 500 employees—primarily in South Korea. This move reflects decreased residential solar demand in Europe, intensified competition from Chinese manufacturers, and will involve charges recorded.

- In January 2023, SolarEdge announced its acquisition of Hark Systems, a European-based energy analytics and IoT company, strengthening its offerings in energy management and analytics

Market Concentration & Characteristics

The Power Optimizer market demonstrates moderate concentration with a few global leaders holding significant shares while regional players contribute to niche segments. It is characterized by strong technological innovation, with companies focusing on module-level monitoring, safety compliance, and integration with smart energy systems. Intense competition arises from pricing strategies and product differentiation, as firms balance cost efficiency with advanced features to capture wider adoption. The market reflects a dynamic structure where established players expand through mergers, partnerships, and global distribution networks, while emerging firms leverage innovation to penetrate specific applications. It benefits from regulatory frameworks that mandate safety standards and promote renewable energy integration, driving consistent demand across residential, commercial, and utility-scale projects. The industry also shows resilience through adaptation to supply chain disruptions by diversifying sourcing and investing in localized production. It remains shaped by sustainability goals, digitalization trends, and the need for reliable solar energy optimization across developed and developing regions.

Report Coverage

The research report offers an in-depth analysis based on Connectivity, Application, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The Power Optimizer market will expand with rising solar installations across residential, commercial, and utility sectors.

- It will gain traction through increasing adoption of module-level power electronics for higher efficiency.

- Strong regulatory support and renewable energy mandates will drive consistent demand.

- Integration with smart grids and digital energy management platforms will strengthen its role.

- Advances in safety features and rapid shutdown compliance will boost residential and commercial adoption.

- Cost reductions through technological innovation and localized manufacturing will widen accessibility.

- Growing demand for hybrid solutions combining storage and solar will enhance market opportunities.

- Expansion in emerging economies with strong renewable targets will create new growth avenues.

- Strategic collaborations between manufacturers and inverter suppliers will improve system compatibility.

- Focus on sustainability and long-term reliability will position power optimizers as a core technology in solar energy systems.