Market Overview

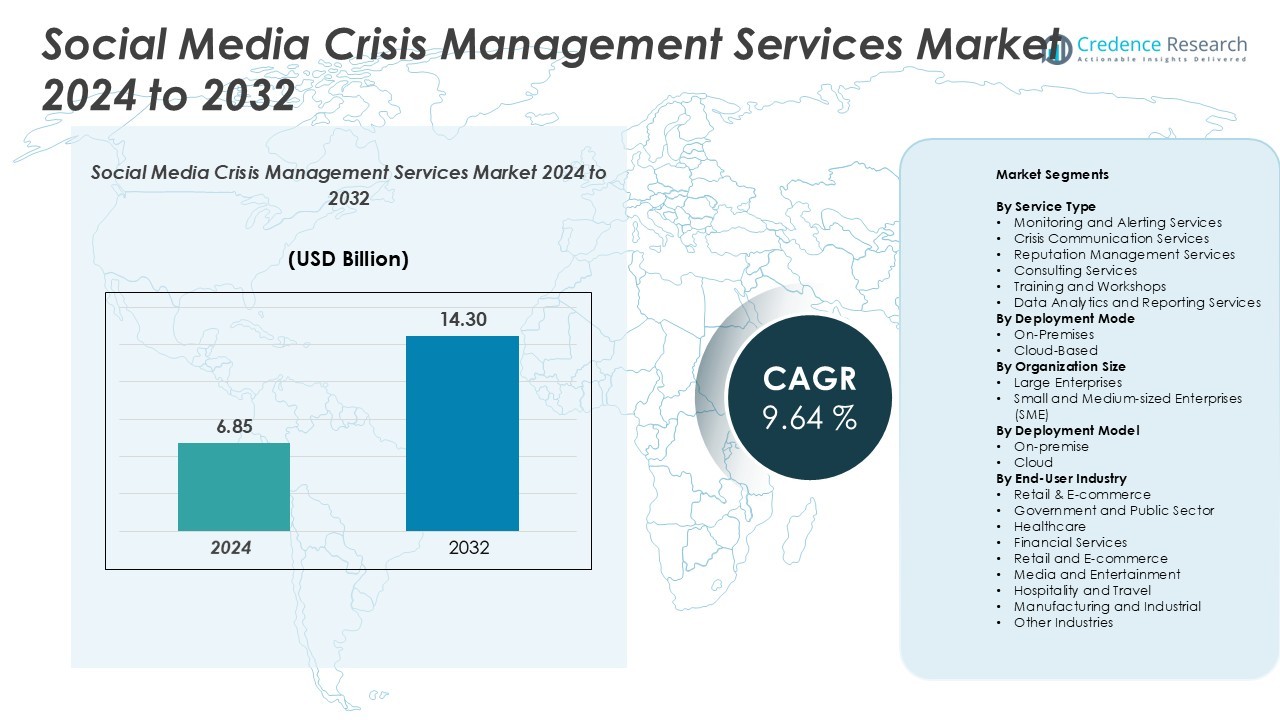

The Social Media Crisis Management Services Market size was valued at USD 6.85 billion in 2024 and is anticipated to reach USD 14.30 billion by 2032, at a CAGR of 9.64% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Social Media Crisis Management Services Market Size 2024 |

USD 6.85 Billion |

| Social Media Crisis Management Services Market, CAGR |

9.64% |

| Social Media Crisis Management Services Market Size 2032 |

USD 14.30 Billion |

The social media crisis management services market is led by key players such as Brandwatch, Hootsuite, Cision, Sprout Social, Sprinklr, and Meltwater. These companies dominate through advanced monitoring platforms, AI-powered analytics, and integrated communication tools that enable real-time crisis detection and response. North America leads the global market with a 36% share, supported by high enterprise adoption and strong digital infrastructure. Europe follows with 28%, driven by strict data protection regulations and growing investments in digital risk management. Asia Pacific, with a 22% share, remains the fastest-growing region due to rapid digitalization and rising social media engagement across industries.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Social Media Crisis Management Services Market was valued at USD 6.85 billion in 2024 and is projected to reach USD 14.30 billion by 2032, at a CAGR of 9.64%.

- Growing digital engagement and rising reputational risks are driving strong adoption of advanced monitoring and communication platforms. Enterprises are prioritizing rapid response solutions to protect brand trust and maintain customer loyalty.

- Cloud-based deployment holds the largest segment share, supported by scalability, cost-effectiveness, and integration flexibility. Monitoring and Alerting Services lead by service type, with strong demand from large enterprises.

- North America dominates with a 36% market share, followed by Europe with 28% and Asia Pacific with 22%, driven by rapid digital transformation and regulatory frameworks.

- Market growth faces restraints such as high implementation costs for SMEs and complex data privacy compliance requirements, which limit adoption in price-sensitive regions.

Market Segmentation Analysis:

By Service Type

Monitoring and Alerting Services hold the dominant share in the social media crisis management services market. Businesses rely on real-time monitoring to detect reputation threats, misinformation, or viral negative content at an early stage. This allows brands to respond quickly and limit reputational damage. High demand comes from industries such as retail, banking, and healthcare, where response speed directly impacts trust and revenue. The growing use of AI-driven alert systems and automated dashboards also enhances efficiency and accuracy. This dominance is further supported by rising brand reputation risks in highly competitive digital spaces.

- For instance, Meltwater’s media intelligence platform processes approximately 1 billion pieces of content daily, not limited to social media posts. It uses AI-based sentiment and anomaly detection to deliver real-time alerts across more than 15 major social networks, as well as a range of other content sources.

By Deployment Mode

Cloud-Based deployment leads the market with a major share due to its scalability, lower infrastructure costs, and ease of access. Companies prefer cloud solutions to manage high-volume data from multiple social platforms without needing complex IT infrastructure. These solutions allow instant updates, integration with analytics tools, and faster response time during crises. Enterprises also benefit from improved flexibility and remote access, making it ideal for distributed teams. The increasing adoption of SaaS models and advanced cloud security is accelerating this deployment trend across industries.

- For instance, Muck Rack, a SaaS-based media-monitoring platform, covers over 600,000 media sources globally via its cloud solution.

By Organization Size

Large Enterprises dominate the market due to their higher exposure to reputational risks and larger online footprints. These organizations invest in advanced monitoring tools, real-time communication systems, and dedicated crisis management teams. The ability to allocate larger budgets enables them to deploy integrated platforms that cover detection, response, and recovery. Brand visibility and customer engagement are key drivers behind this dominance, as large enterprises face more complex and frequent crises. However, growing awareness among SMEs is expected to increase their adoption over the forecast period.

Key Growth Drivers

Rising Frequency of Online Reputational Crises

The increasing number of online controversies, viral misinformation, and data breaches is driving demand for advanced crisis management solutions. Social platforms amplify both positive and negative narratives, making reputational damage swift and widespread. Brands now rely on early detection, rapid response, and targeted communication strategies to protect their image. Real-time monitoring tools and AI-powered alerts allow organizations to address issues before they escalate. This trend is strong across sectors such as retail, healthcare, and banking, where consumer trust directly impacts revenue. Proactive reputation control is becoming a core element of brand strategy, fueling market growth.

- For instance, Brand24 monitors over 100,000 brands and has collected 25 billion mentions across the web, enabling detection of mention-spikes via its “Anomaly Detector” module.

Growing Enterprise Investment in Digital Brand Protection

Large and mid-sized enterprises are increasing investments in digital risk management to safeguard brand credibility. As consumer interactions shift online, companies face rising risks from misinformation, cyber incidents, and coordinated smear campaigns. Organizations are adopting integrated platforms that combine communication tools, sentiment analysis, and reporting capabilities. These systems help decision-makers react strategically during crises. Demand is particularly high in industries with strong consumer engagement, including financial services and e-commerce. This enterprise focus on preparedness and rapid action continues to accelerate market adoption of crisis management solutions.

- For instance, Amazon invested around $1.2 billion in brand-protection efforts in 2023 and employed more than 15,000 people in that domain.

Expansion of AI and Data Analytics in Crisis Detection

AI-powered analytics is transforming how companies detect and respond to potential crises. Advanced algorithms analyze millions of posts and conversations in real time, identifying early signals of reputational risks. Predictive analytics helps forecast crisis impact, enabling faster decision-making and more targeted messaging. This capability reduces manual workload and improves accuracy in issue tracking. The integration of AI with social media platforms is expanding the market beyond traditional PR services. Organizations across industries are prioritizing data-driven response systems to maintain operational continuity and protect brand reputation.

Key Trends & Opportunities

Integration with Customer Experience Platforms

Crisis management services are increasingly merging with customer experience and engagement platforms. This integration allows brands to unify reputation tracking with service delivery, enabling quick customer support during critical incidents. Real-time engagement tools and automated response mechanisms help prevent escalation. Companies are using integrated platforms to address negative sentiment while maintaining transparency with customers. This shift creates strong opportunities for vendors offering flexible, multi-channel solutions. Industries with large customer-facing operations, such as travel and retail, are early adopters of this trend.

- For instance, Sprinklr’s AI-powered chatbot—a component of its unified CXM platform—helped the telecommunications company Umniah reduce the average handling time of chatbot conversations by 91%.

Growing Demand from SMEs Through Scalable Cloud Solutions

Small and medium-sized enterprises are adopting cloud-based crisis management tools due to their cost-effectiveness and ease of use. Scalable platforms allow SMEs to monitor brand mentions, manage communication, and access analytics without heavy infrastructure costs. As digital engagement grows among smaller brands, their vulnerability to reputational threats also increases. This creates a significant growth opportunity for vendors offering simplified and affordable services. Cloud-native solutions are enabling SMEs to implement proactive crisis strategies once limited to large corporations.

- For instance, Crises Control offers cloud-based solutions tailored for SMEs, including mass notification, remote access and automated playbooks.

Increasing Role of Training and Capacity Building

Organizations are recognizing the importance of preparedness through crisis simulations and team training. Training and workshops help employees develop structured response plans and communication strategies. This trend reflects a shift from reactive to proactive management, reducing the impact of sudden incidents. Vendors offering integrated training services along with monitoring platforms are gaining competitive advantage. The growing focus on human readiness and digital resilience presents new opportunities in service diversification.

Key Challenges

Data Privacy and Compliance Risks

Monitoring and analyzing user-generated content on social platforms raises serious data privacy concerns. Companies must navigate complex regulations like GDPR and CCPA while conducting sentiment analysis and tracking conversations. Non-compliance can result in legal penalties and reputational harm. Vendors must implement strict data handling protocols, encryption, and anonymization methods to maintain trust. Balancing real-time monitoring with privacy protection remains a key challenge for market growth, especially in highly regulated sectors like healthcare and finance.

High Implementation Costs for Advanced Solutions

While large enterprises can afford comprehensive platforms, smaller businesses often face barriers due to cost. Advanced monitoring tools, AI-driven analytics, and integrated communication systems require significant investment in both technology and skilled personnel. This cost structure limits adoption among SMEs, creating a gap in market reach. Vendors must address this challenge by offering tiered pricing models and simplified solutions. Bridging this affordability gap will be essential to expanding market penetration and supporting broader digital crisis readiness.

Regional Analysis

North America

North America holds the largest market share of 36% in the social media crisis management services market. The region benefits from mature digital infrastructure, strong enterprise adoption, and a high frequency of online engagement. U.S.-based companies prioritize reputation protection due to high media visibility and strong consumer activism. Major technology vendors and service providers in the region offer advanced monitoring, AI-driven analytics, and real-time communication platforms. Industries such as retail, finance, and healthcare are key adopters. Regulatory frameworks and strong cybersecurity standards further drive investments, making North America the dominant hub for market growth and innovation.

Europe

Europe accounts for 28% of the market share, driven by strict data protection laws, increasing digitalization, and a high emphasis on brand reputation. Companies in the region focus on GDPR-compliant solutions, which enhances trust and ensures secure crisis response. The presence of global brands and active regulatory bodies encourages investment in robust monitoring and communication systems. Industries such as finance, public services, and manufacturing are major adopters. The region’s structured approach to crisis management and growing demand for cloud-based solutions strengthen its position in the global market.

Asia Pacific

Asia Pacific holds a 22% market share, supported by rapid digital transformation and growing social media usage. Expanding e-commerce, fintech, and telecom sectors create strong demand for advanced crisis monitoring solutions. Enterprises across China, India, Japan, and Southeast Asia are increasingly adopting AI-based alerting and cloud-enabled communication tools. High internet penetration and strong consumer engagement amplify the need for reputation protection. Governments and enterprises are investing in digital risk management frameworks, which is accelerating regional market expansion. Asia Pacific remains one of the fastest-growing regions for crisis management services.

Latin America

Latin America represents a 7% market share, with growing adoption among retail, government, and media industries. Rising social media engagement and political activism increase the importance of real-time monitoring and response tools. Brazil and Mexico lead in deployment, supported by expanding digital infrastructure. Although adoption rates are lower than in North America or Europe, the region is experiencing steady growth due to rising brand awareness and increased vulnerability to online crises. SMEs are increasingly adopting cost-effective cloud-based solutions, which is expected to strengthen market presence over the forecast period.

Middle East & Africa

The Middle East & Africa region holds a 7% market share, driven by increasing digital communication, government modernization initiatives, and growing social media engagement. Countries such as the UAE, Saudi Arabia, and South Africa are early adopters of advanced monitoring tools. Public sector organizations and large enterprises in retail and telecom lead adoption. While infrastructure development is still evolving in parts of the region, investments in digital risk mitigation and cybersecurity are rising. Growing awareness of brand reputation and regulatory advancements are expected to fuel gradual but steady market growth in the coming years.

Market Segmentations:

By Service Type

- Monitoring and Alerting Services

- Crisis Communication Services

- Reputation Management Services

- Consulting Services

- Training and Workshops

- Data Analytics and Reporting Services

By Deployment Mode

By Organization Size

- Large Enterprises

- Small and Medium-sized Enterprises (SME)

By Deployment Model

By End-User Industry

- Retail & E-commerce

- Government and Public Sector

- Healthcare

- Financial Services

- Retail and E-commerce

- Media and Entertainment

- Hospitality and Travel

- Manufacturing and Industrial

- Other Industries

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The social media crisis management services market is highly competitive, with major players focusing on advanced monitoring tools, AI integration, and real-time analytics to strengthen their market positions. Key companies include Brandwatch, Hootsuite, Cision, Sprout Social, Sprinklr, and Meltwater, each offering specialized solutions for crisis detection, response, and reputation management. These vendors emphasize platform scalability, data security, and multichannel engagement to support enterprise needs. Strategic partnerships with communication agencies and technology providers are common to enhance service offerings. Product innovation, cloud-based deployments, and predictive analytics capabilities are key differentiators. Companies are also investing in training modules, automated workflows, and customizable dashboards to provide end-to-end solutions. This competition drives continuous innovation, making the market dynamic and technologically advanced.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

Recent Developments

- In May 2024, Sprinklr launched its Crisis Management Solution App at the CXUnifiers 2024 event, featuring AI models tailored for over 30 platforms, enabling rapid detection and response to emerging brand crises with minimal setup.

- In April 2023, Dataminr launched Pulse for Cyber Risk, enhancing its Pulse platform with AI-augmented capabilities that deliver real-time alerts on cyber-physical threats like malware and ransomware. It cross-correlates text, images, and sensor data to support enterprise security and CISOs with actionable threat intelligence.

Report Coverage

The research report offers an in-depth analysis based on Service Type, Deployment Mode, Organization Size, Deployment Model, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Adoption of AI-powered monitoring tools will increase for faster crisis detection.

- Cloud-based platforms will become the preferred deployment mode across industries.

- SMEs will accelerate adoption through scalable and cost-efficient solutions.

- Predictive analytics will play a larger role in early risk identification.

- Integration with customer experience platforms will improve coordinated responses.

- Demand for training and simulation services will grow among enterprises.

- Regulatory compliance will shape platform design and service offerings.

- Partnerships between tech vendors and PR agencies will strengthen service portfolios.

- Real-time multilingual monitoring will expand global crisis response capabilities.

- Automation and workflow intelligence will reduce response time and operational costs.