Premium Cosmetics Market Overview:

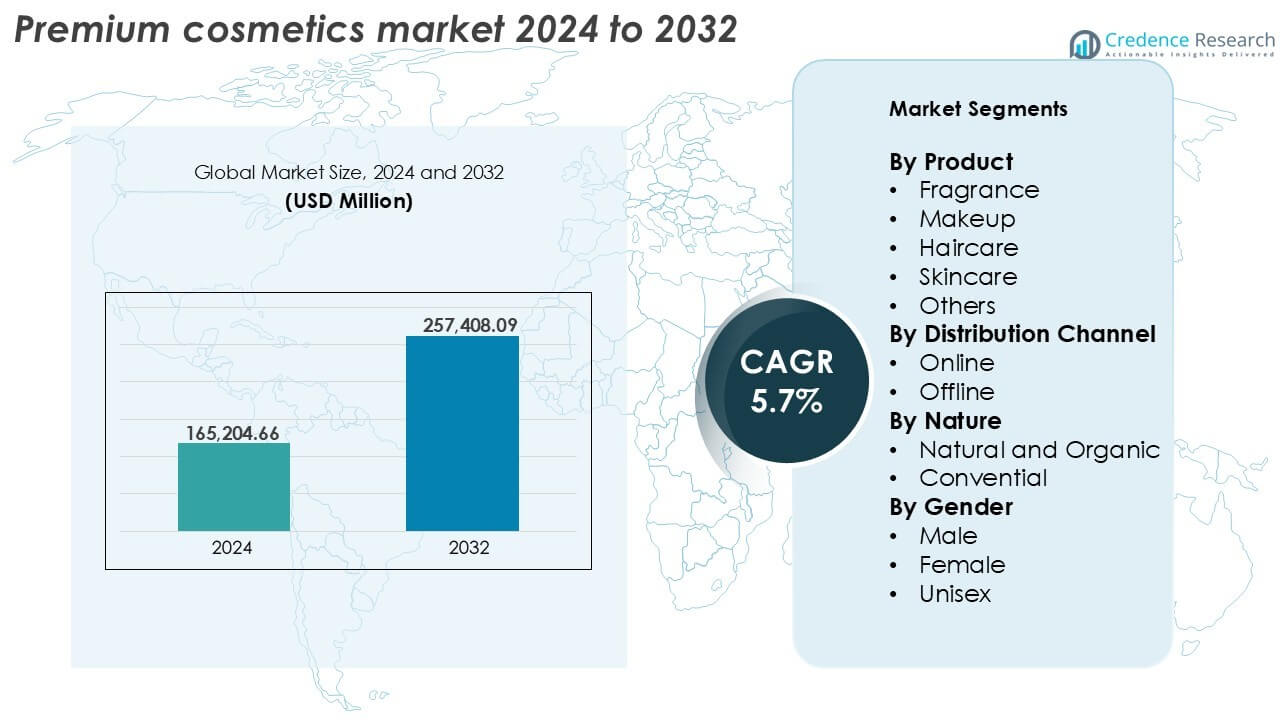

The Premium Cosmetics Market size was valued at USD 165,204.66 million in 2024 and is anticipated to reach USD 257,408.09 million by 2032, at a CAGR of 5.7% during the forecast period

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Premium Cosmetics Market Size 2024 |

USD 165,204.66 million |

| Premium Cosmetics Market, CAGR |

5.7% |

| Premium Cosmetics Market Size 2032 |

USD 257,408.09 million |

Premium Cosmetics Market Insights

- Demand is driven by rising disposable income, growing beauty consciousness and consumer willingness to spend on high-performance and luxury skincare, fragrance and makeup products.

- Key trends include the shift toward clean beauty, personalized skincare and the growing adoption of inclusive and gender-neutral cosmetics across all age groups.

- The market is highly competitive, with major players like L’Oréal, Estée Lauder, LVMH, Shiseido and Chanel investing in R&D, digital marketing and regional expansion to gain market share.

- Asia-Pacific holds the largest regional share at 28%, followed by North America at 30%, while skincare remains the dominant segment with over 35% share, driven by anti-aging and hydration-focused product demand.

Premium Cosmetics Market Segmentation Analysis

By product

Skincare dominates the premium cosmetics market by product, accounting for over 35% of revenue share in 2024. Consumers increasingly seek high-performance anti-aging, hydrating and skin-repairing products, especially in Asia-Pacific and North America. The segment benefits from scientific formulations, clinical endorsements and personalized skincare innovations. Premium skincare brands continue to integrate ingredients like hyaluronic acid, peptides and plant-based actives to meet rising expectations. Growing awareness of skin health, coupled with strong marketing by luxury brands, supports the sustained dominance of this sub-segment across global markets.

- L’Oréal operates more than 4,000 researchers across 21 research centers globally. The company filed over 600 patents in one year for skincare-related innovations.

By distribution channel

Offline channels remain dominant in the premium cosmetics market, contributing nearly 60% of the overall distribution share in 2024. Department stores, specialty outlets and exclusive brand boutiques offer personalized consultations and in-store experiences, driving high-value purchases. Luxury brands leverage in-person product trials and loyalty programs to maintain brand exclusivity and trust. Online sales are growing fast due to influencer marketing, mobile app purchases and direct-to-consumer brand strategies. E-commerce is expanding access to premium products in emerging economies and among digital-first consumers.

- Chanel operates over 250 standalone beauty boutiques worldwide. Chanel Beauty counters offer trained advisors providing personalized skin analysis sessions.

By nature

Conventional cosmetics hold a larger share in the premium segment, comprising around 65% of the market in 2024. Leading global brands rely on clinically tested synthetic ingredients to ensure consistent performance, shelf stability and luxury textures. Natural and organic sub-segments are gaining traction due to consumer shifts toward clean beauty, transparency and ethical sourcing. The rise of ingredient-conscious buyers, especially in Europe and North America, is boosting demand for botanical formulations. While conventional products dominate, the natural and organic segment shows a stronger CAGR through 2032.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Key growth drivers

Rising affluence and consumer willingness to spend on luxury personal care

The global rise in disposable income, especially among middle- and upper-middle-class consumers, fuels demand for premium cosmetics. Urbanization, lifestyle upgrades and increasing beauty consciousness have pushed consumers toward high-end products that promise visible results and status appeal. In emerging markets like China, India and Southeast Asia, aspirational consumers are embracing luxury skincare and makeup as part of their identity and self-expression. Mature markets in North America and Western Europe also see strong demand due to loyalty to premium brands and regular use of prestige anti-aging and dermatology-grade skincare. Consumers are now more inclined to pay for specialized formulations, exclusivity and brand value, driving consistent revenue growth in the premium segment.

- Estée Lauder Companies operates more than 25 prestige beauty brands globally. The group reported net sales above $15 billion in a recent fiscal year.

Rapid growth of e-commerce and digital engagement channels

E-commerce platforms have become key sales drivers in the premium cosmetics market, transforming how brands reach and engage consumers. Luxury beauty brands are expanding direct-to-consumer channels, investing in mobile-first platforms, virtual try-ons and AI-powered product recommendations. Social commerce through platforms like Instagram, TikTok and YouTube boosts brand visibility and facilitates influencer-led campaigns. These digital tools enable consumers to explore and purchase high-end products with ease, especially in regions with limited access to offline luxury retail. E-commerce not only widens geographic reach but also deepens personalization and brand loyalty, especially among Gen Z and millennial buyers.

- LVMH integrates digital commerce across its beauty brands. Sephora, part of LVMH, operates e-commerce platforms in more than 30 countries.

Product innovation in clean beauty, anti-aging and dermatological formulations

Innovation remains central to growth in the premium cosmetics segment, particularly in clean beauty, age-defying formulas and dermatologist-developed products. Consumers now demand visible results, skin compatibility and ethically sourced ingredients, pushing brands to formulate with peptides, retinol, ceramides, probiotics and plant-based actives. Technologies like encapsulation, nanodelivery and biomimetic ingredients elevate product efficacy and attract tech-savvy users. Premium cosmetic companies also invest in research to launch multifunctional products combining skincare and makeup, such as foundation-serum hybrids. Clinical trials, dermatologist endorsements and transparent labeling appeal to informed consumers, while sustainable packaging and cruelty-free certifications strengthen brand image.

Key trends and opportunities

Surge in demand for gender-neutral and inclusive cosmetics

The growing demand for inclusivity in the beauty industry creates new opportunities in premium cosmetics. Consumers now expect brands to offer diverse shade ranges, cater to all skin types and represent various identities across their campaigns. This has led to rising adoption of gender-neutral cosmetics that focus on skincare and grooming without targeting a specific gender. Major brands have launched unisex product lines with minimalist packaging and universal formulas. Inclusive marketing strategies that promote authenticity, diversity and social responsibility resonate with younger consumers. This trend reflects deeper societal shifts and opens a broader market for premium beauty brands looking to expand beyond traditional demographic boundaries.

- Fenty Beauty launched with 40 foundation shades at debut, later expanding beyond 50 shades globally. The brand reported over $500 million in annual revenue within its first year of operation.

Expansion of premium cosmetics in emerging markets

Emerging economies, particularly in Asia-Pacific, the Middle East and Latin America, offer substantial growth opportunities due to rising disposable incomes and urban lifestyles. Markets such as China, India, Brazil and the UAE show increased demand for international luxury beauty brands. Local consumers are influenced by global fashion trends, digital media and rising brand awareness. These regions also see rapid growth in organized retail and cross-border e-commerce, making premium cosmetics more accessible. Brands that localize their offerings, adapt pricing strategies and invest in regional marketing partnerships can gain a competitive edge.

Key challenges

High product cost and limited accessibility in price-sensitive regions

Premium cosmetics face challenges in penetrating cost-conscious markets where consumers prioritize affordability over brand prestige. In regions like Africa, Southeast Asia outside major metros and parts of Latin America, high price points and import duties limit consumer access. Luxury products often remain concentrated in urban centers and exclusive outlets, creating barriers to widespread adoption. Even where awareness is growing, the gap between aspiration and purchasing power restricts conversion. This pricing challenge forces brands to develop region-specific pricing models, smaller packaging formats or affordable luxury lines to appeal to budget-conscious but brand-curious consumers.

Increasing regulatory pressure and ingredient transparency requirements

Stricter regulations around product safety, ingredient sourcing, labeling and environmental impact pose operational hurdles for premium cosmetic brands. Markets like the European Union, U.S. and Japan demand full ingredient disclosure, banned substance compliance and sustainability certifications. Growing consumer awareness and activism around ingredient safety, cruelty-free testing and green labeling pressure brands to rework formulations and supply chains. Complying with global regulatory variations raises formulation costs, affects speed-to-market and complicates global launches. Navigating evolving compliance norms while maintaining luxury performance standards remains a complex challenge for manufacturers.

Regional analysis

North America

North America holds a substantial share in the premium cosmetics market, accounting for nearly 30% in 2024. The U.S. leads the region with high consumer spending, strong brand loyalty and an established luxury retail network. Demand is driven by advanced skincare, clinical-grade formulations and personalized beauty solutions. Premium makeup and anti-aging products remain popular among aging yet appearance-conscious consumers. Digital marketing, influencer partnerships and subscription-based beauty services further boost adoption. Canada follows with growing interest in clean and organic cosmetics. High disposable income and a strong online retail base sustain North America’s position in the global market.

Europe

Europe captures approximately 27% of the premium cosmetics market, supported by a heritage of luxury brands and strong consumer trust. France, Germany and the United Kingdom lead demand due to high fashion influence, innovation in skincare and emphasis on sustainability. European consumers prefer clean, cruelty-free and eco-labeled products, shaping brand strategies. Regulatory frameworks promote ingredient transparency and ethical practices, boosting consumer confidence. Offline channels like perfumeries and department stores remain key, while online sales are steadily increasing.

Asia-Pacific

Asia-Pacific commands a 28% share in the premium cosmetics market and remains the fastest-growing region. South Korea, China and Japan dominate due to rapid urbanization, beauty consciousness and a tech-savvy consumer base. South Korea’s K-beauty trends influence global innovation, while China’s expanding middle class drives strong demand for high-end skincare and makeup. Premium brands localize offerings and collaborate with influencers to boost reach. Japan maintains steady demand with a focus on anti-aging and minimalist formulations. E-commerce and mobile shopping apps fuel accessibility, making Asia-Pacific a strategic region for premium cosmetic expansion.

Middle East and Africa

The Middle East and Africa region holds about 7% of the global premium cosmetics market, driven by rising affluence and brand aspirations in countries like the UAE, Saudi Arabia and South Africa. The market sees growing demand for luxury fragrances, skincare and halal-certified cosmetics. High heat and dry climates fuel interest in hydration-focused products. Offline retail in luxury malls and high-end boutiques remains dominant, but online platforms are expanding rapidly. African nations like Nigeria and Kenya show emerging potential as urban beauty culture grows.

Latin America

Latin America captures around 8% of the premium cosmetics market, with Brazil and Mexico leading regional consumption. Growth stems from rising income levels, beauty-centered culture and strong influence of social media. Consumers show high interest in luxury skincare, color cosmetics and salon-grade haircare. The region faces pricing sensitivity, yet aspirational buyers remain loyal to international and regional prestige brands. Local beauty influencers and culturally attuned campaigns help drive premium product visibility. Latin America remains a high-opportunity region with untapped demand in Tier 2 cities.

Premium Cosmetics Market Segmentations:

By Product

- Fragrance

- Makeup

- Haircare

- Skincare

- Others

By Distribution Channel

By Nature

- Natural and Organic

- Convential

By Gender

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The premium cosmetics market is highly competitive, dominated by global players such as L’Oréal, Estée Lauder, LVMH, Chanel and Shiseido. These companies lead through diversified brand portfolios, robust R&D capabilities and strong distribution networks. Innovation in clean beauty, age-defying formulations and digital engagement drives market differentiation. Strategic acquisitions — such as Estée Lauder’s stake in DECIEM and LVMH’s investment in Officine Universelle Buly — bolster brand offerings. Luxury houses like Dior and Chanel leverage heritage, exclusivity and direct-to-consumer channels to retain loyal customers. Meanwhile, emerging brands focus on niche positioning, ethical sourcing and influencer-driven marketing. Companies increasingly invest in AI-driven personalization, sustainable packaging and regional expansion strategies to capture evolving consumer demand.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key player analysis

- L’Oréal

- LVMH

- Estée Lauder

- Chanel

- Dior Beauty

- Shiseido

- Coty

- The Procter & Gamble Co.

- The Unilever Group

- KAO Corp.

- Avon Products

- Oriflame Holding AG

- Yves Rocher International

- Elizabeth Arden Inc.

Recent developments

- In July 2025, Robin James launched Anforh, a premium male hair care line developed based on community feedback and refined over two years. The line launched July 17 and features three products.

- In April 2025, Aditya Birla Group, led by Ananya Birla, launched LOVETC, a premium color cosmetics brand, following the earlier launch of Contraband that year.

- In April 2022, Chanel added L’Essence Fondamentale Yeux Eye Treatment, an anti-aging solution for the eye area, to its Sublimage skincare line.

Report coverage

The research report offers an in-depth analysis based on product, distribution channel, nature, gender and geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams and key applications. The report also includes insights into the competitive environment, SWOT analysis, current market trends, and primary drivers and constraints. It examines market dynamics, regulatory scenarios and technological advancements shaping the industry, and provides strategic recommendations for new entrants and established companies.

Future outlook

- Skincare will continue to lead the market, driven by demand for anti-aging and high-performance products.

- Clean beauty and sustainable formulations will gain stronger consumer preference across all age groups.

- Online sales will expand rapidly through mobile apps, influencer marketing and virtual try-on features.

- Asia-Pacific will remain the fastest-growing region with rising affluence and digital engagement.

- Premium brands will invest more in personalization and AI-driven skin diagnostics to enhance customer experience.

- Inclusive and gender-neutral product lines will attract younger and more diverse consumer bases.

- Natural and organic premium cosmetics will grow faster than conventional counterparts due to ingredient awareness.

- Global players will pursue mergers, acquisitions and regional brand collaborations for portfolio expansion.

- Evolving regulations on ingredient transparency and sustainability will shape product development strategies.

- Fragrance and hybrid makeup-skincare products will see increased demand in both mature and emerging markets.