Market Overview

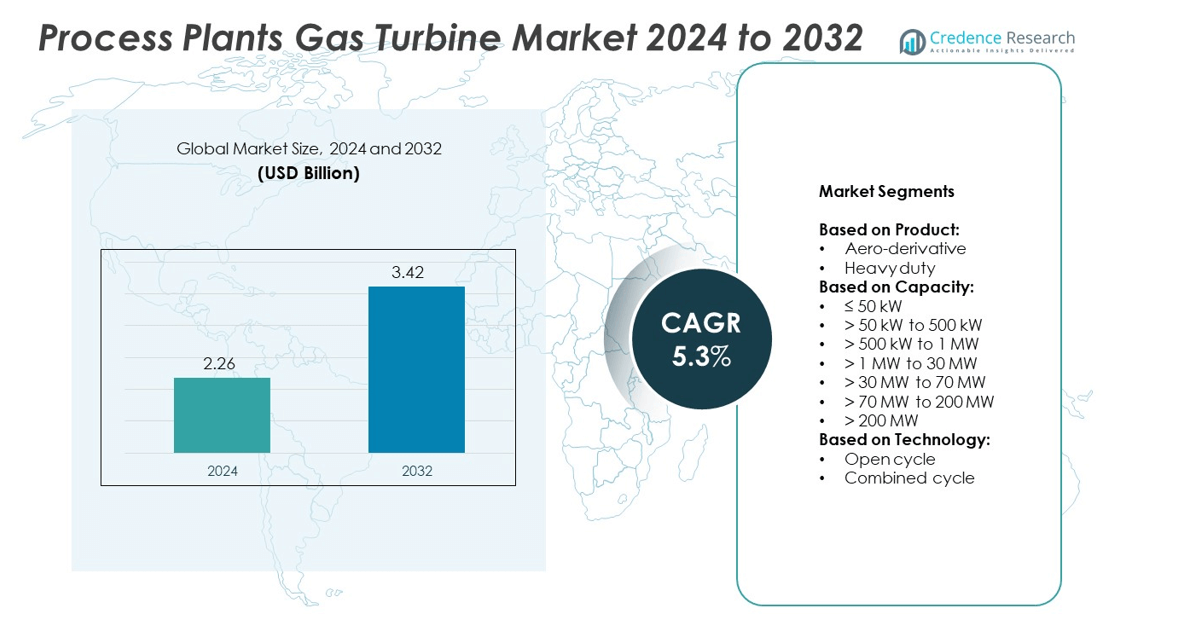

The Process Plants Gas Turbine Market size was valued at USD 2.26 billion in 2024 and is anticipated to reach USD 3.42 billion by 2032, at a CAGR of 5.3% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Process Plants Gas Turbine Market Size 2024 |

USD 2.26 billion |

| Process Plants Gas Turbine Market, CAGR |

5.3% |

| Process Plants Gas Turbine Market Size 2032 |

USD 3.42 billion |

The Process Plants Gas Turbine market is driven by rising demand for reliable and efficient power generation across industrial sectors, supported by advancements in turbine technologies. Increasing adoption of low-emission systems, hydrogen-ready solutions, and digital monitoring tools enhances operational efficiency and sustainability. Expanding oil, gas, petrochemical, and manufacturing facilities fuels consistent deployment of high-capacity turbines. The market also benefits from growing hybrid energy integration and regulatory initiatives promoting cleaner fuel usage. Continuous R&D investments by leading players strengthen innovation, while modernization projects and infrastructure development in emerging economies further accelerate growth and adoption of advanced turbine solutions.

Different regions show distinctive market dynamics in the Process Plants Gas Turbine market, with Asia Pacific witnessing rapid industrial expansion that boosts demand, North America focusing on modernization and retrofit programs, Europe pursuing decarbonization through hydrogen-ready technologies, Latin America gradually investing in captive and combined‑cycle systems, and the Middle East & Africa prioritizing heavy-duty deployments in energy complexes. Leading players include General Electric Company, Siemens Energy AG, Mitsubishi Power, Ltd., Ansaldo Energia S.p.A., and Baker Hughes Company.

Market Insights

- The Process Plants Gas Turbine market was valued at USD 2.26 billion in 2024 and is projected to reach USD 3.42 billion by 2032, growing at a CAGR of 5.3% during the forecast period.

- Rising demand for reliable and efficient power generation in industries such as oil & gas, petrochemicals, and manufacturing is driving the market growth globally.

- Increasing adoption of hydrogen-ready turbines, low-emission technologies, and digital monitoring systems is shaping industry trends and improving operational efficiency.

- The market is moderately concentrated, with major players like General Electric Company, Siemens Energy AG, Mitsubishi Power, Ltd., Ansaldo Energia S.p.A., and Baker Hughes Company focusing on innovation, partnerships, and regional expansions.

- High operational costs, complex maintenance requirements, and strict environmental regulations act as restraints, challenging smaller operators and increasing dependency on advanced technologies.

- Asia Pacific leads the market due to rapid industrialization and infrastructure development, while North America emphasizes modernization and Europe accelerates adoption of sustainable energy solutions.

- Emerging opportunities stem from hybrid energy integration, hydrogen-capable turbine technologies, and growing investments in clean energy infrastructure across Latin America and the Middle East & Africa.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising Demand for Reliable Power Generation Solutions

The Process Plants Gas Turbine market benefits from increasing demand for dependable and efficient power generation systems across industrial sectors. It enables continuous operations by supporting large-scale facilities that require stable energy supply. Manufacturers focus on developing advanced turbine technologies to meet evolving performance and efficiency expectations. Rapid industrialization in emerging economies accelerates investments in energy infrastructure, driving higher adoption. The market gains significant traction in industries such as oil and gas, chemicals, and petrochemicals, where uninterrupted power is critical. Growing operational requirements position gas turbines as a preferred choice for process plant applications.

- For instance, GE Vernova’s 9HA.02 turbine delivered a net combined‑cycle efficiency of 44.0% at 571 MW output.

Technological Advancements Driving Efficiency and Performance

Continuous innovation strengthens the capabilities of modern gas turbines, allowing process industries to achieve higher operational efficiency. It incorporates advanced materials, improved combustion systems, and digital monitoring technologies to enhance durability and precision. Leading companies invest heavily in R&D to design turbines that deliver superior fuel efficiency while reducing environmental impact. Integration of predictive analytics helps operators optimize performance and minimize downtime. Digital control systems improve load management, ensuring optimal energy utilization in process facilities. These technological developments create strong opportunities for broader deployment across multiple industrial settings.

- For instance, Siemens Energy raised machine‑tool overall equipment efficiency (OEE) from 65% to 85%, while reducing part‑machining time by 25–36% through digital twin implementation.

Transition Toward Cleaner and Sustainable Energy Sources

Stringent environmental regulations encourage industries to shift toward energy solutions that balance productivity and sustainability. The Process Plants Gas Turbine market benefits from growing preference for cleaner-burning fuels and lower-emission technologies. It supports energy producers in meeting global decarbonization goals by enabling efficient utilization of natural gas. Manufacturers develop hybrid solutions that combine turbines with renewable integration to improve overall energy profiles. Regulatory frameworks promote adoption in regions focused on reducing carbon footprints across industrial sectors. Increased focus on sustainability reinforces the role of gas turbines in future-ready energy strategies.

Expansion of Oil, Gas, and Petrochemical Infrastructure

Rising investments in upstream and downstream operations create substantial growth prospects for gas turbines in process industries. The Process Plants Gas Turbine market experiences strong demand from large-scale oil refineries, LNG facilities, and petrochemical complexes. It offers high power density, operational flexibility, and lower maintenance requirements that suit complex energy-intensive processes. Global energy producers adopt turbine systems to improve reliability and reduce operational risks. Companies prioritize scalable solutions to meet varying power requirements across production sites. Growing industrial expansion secures long-term opportunities for turbine manufacturers targeting diverse process plant applications.

Market Trends

Integration of Digital Technologies and Smart Monitoring Solutions

The Process Plants Gas Turbine market witnesses rising adoption of advanced digital technologies to improve performance and operational control. It utilizes real-time monitoring systems, predictive maintenance tools, and AI-driven analytics to enhance reliability. Industrial operators focus on minimizing downtime by deploying connected solutions that track turbine health and optimize energy efficiency. Digital twin technology enables simulation of operating conditions, helping businesses improve planning and asset management. Leading manufacturers invest in software upgrades to support automation and intelligent control capabilities. The shift toward smart systems strengthens competitiveness across energy-intensive process industries.

- For instance, GE Vernova validated a Dry Low NOₓ (DLN) hydrogen combustion system operating on 100% hydrogen with NOₓ emissions below 25 ppm, with deployment planned.

Growing Preference for Fuel-Efficient and Low-Emission Turbines

Rising environmental concerns and regulatory pressures accelerate the demand for energy-efficient turbines. The Process Plants Gas Turbine market benefits from innovation in low-NOx combustion technologies and advanced fuel management systems. It supports industries in achieving reduced emissions while maintaining operational productivity. Manufacturers introduce turbines designed to operate on multiple fuel types, including natural gas and hydrogen blends, ensuring greater flexibility. Industries adopt these solutions to meet sustainability goals without compromising performance standards. This transition toward fuel efficiency drives significant changes in the design and adoption of next-generation turbine systems.

- For instance, Ansaldo Energia’s AE94.3A turbines achieved over 5 million equivalent operating hours across more than 120 units sold, showcasing proven reliability and cost efficiency in demanding environments.

Hybrid Energy Systems and Renewable Integration

Industrial energy strategies increasingly combine traditional turbine systems with renewable energy sources to achieve balanced power generation. The Process Plants Gas Turbine market evolves to support hybrid systems where turbines complement solar and wind energy. It enables facilities to maintain consistent operations while addressing fluctuations in renewable supply. Energy producers invest in flexible turbine configurations that can rapidly respond to varying power demands. Manufacturers develop innovative turbine designs capable of running on cleaner fuels to integrate seamlessly with hybrid infrastructures. This trend creates opportunities for sustainable energy solutions across diverse industrial applications.

Rising Investments in Upgrading Aging Infrastructure

Process industries allocate significant resources to modernize existing facilities and improve operational efficiency. The Process Plants Gas Turbine market gains momentum from retrofitting projects aimed at replacing outdated systems with advanced turbine technologies. It enhances energy output, reduces maintenance costs, and extends equipment lifespan in large-scale process plants. Global manufacturers offer modular designs to simplify upgrades and minimize disruptions during transitions. Industrial operators prioritize efficiency improvements to remain competitive in high-demand markets. Ongoing modernization efforts support steady growth and fuel long-term adoption of innovative turbine solutions.

Market Challenges Analysis

High Operational Costs and Complex Maintenance Requirements

The Process Plants Gas Turbine market faces significant challenges due to rising operational expenses and complex maintenance procedures. It demands substantial investments in fuel, spare parts, and skilled labor, increasing the overall cost burden for industries. Frequent inspections and precision-based servicing are necessary to maintain turbine efficiency and reliability. Unplanned downtime caused by technical failures can disrupt production schedules and reduce profitability for process facilities. Manufacturers focus on improving durability and introducing modular designs to simplify repairs, yet high lifecycle costs remain a concern. The need for specialized expertise further limits easy adoption across smaller process plants.

Stringent Environmental Regulations and Fuel Dependency Issues

Compliance with evolving environmental standards presents another major challenge for the Process Plants Gas Turbine market. It requires manufacturers and operators to adopt low-emission technologies and advanced combustion systems to meet strict regulatory norms. High reliance on natural gas and limited availability of cleaner fuel alternatives increase operational risks in certain regions. Industries face pressure to balance energy efficiency with sustainability goals while ensuring uninterrupted power generation. Developing turbines compatible with alternative fuels, such as hydrogen, requires significant R&D investments, slowing rapid implementation. Companies must adapt quickly to regulatory changes to sustain competitiveness in global process industries.

Market Opportunities

Rising Demand for Energy Efficiency and Advanced Power Solutions

The Process Plants Gas Turbine market presents strong opportunities driven by increasing demand for energy-efficient and high-performance power systems. It supports industries seeking to optimize energy consumption while maintaining consistent operational output. Manufacturers develop turbines with improved fuel efficiency, advanced combustion systems, and higher power densities to address evolving industrial needs. Growing emphasis on reducing operational costs encourages process facilities to invest in modern turbine technologies. Expanding applications across oil and gas, petrochemicals, and chemical processing create long-term growth potential. The focus on maximizing productivity while minimizing energy losses accelerates adoption across global markets.

Adoption of Cleaner Fuels and Hybrid Energy Integration

Expanding initiatives toward decarbonization create new growth avenues for the Process Plants Gas Turbine market. It benefits from technological innovations that enable turbines to operate on hydrogen, biofuels, and blended natural gas, reducing environmental impact. Industries explore hybrid energy systems where turbines complement renewable sources to achieve stable and sustainable power generation. Government-backed policies supporting green technologies encourage investments in low-emission turbine solutions. Manufacturers prioritize developing flexible systems capable of adapting to future fuel transitions and evolving regulatory frameworks. Growing opportunities in integrating gas turbines with renewable infrastructures position them as a key enabler of industrial energy transformation.

Market Segmentation Analysis:

By Product:

Aero-derivative turbines are gaining popularity due to their lightweight design, high efficiency, and quick start-up capabilities, making them suitable for process plants requiring flexible power solutions. Heavy-duty turbines dominate large-scale applications, offering higher power output and durability to handle continuous operations in energy-intensive industries. Manufacturers focus on optimizing both segments by integrating advanced materials, digital controls, and low-emission technologies to meet evolving performance demands.

- For instance, GE Vernova’s fleet of H-Class gas turbines (specifically HA models) achieved 3 million commercial operating hours across 116 units globally, a milestone significant for powering homes, enabling the energy transition, and meeting the surge in electricity demand driven by AI and data centers.

By Capacity:

The market serves a wide range of industrial needs. Turbines with ≤ 50 kW capacity are preferred in smaller process plants and localized applications requiring lower power generation. The > 50 kW to 500 kW and > 500 kW to 1 MW categories support mid-sized facilities focusing on operational efficiency and cost optimization. Larger process industries increasingly adopt turbines in the > 1 MW to 30 MW range to balance energy output and performance. The > 30 MW to 70 MW and > 70 MW to 200 MW segments cater to refineries, petrochemical plants, and LNG facilities demanding high-capacity continuous power supply. For the largest-scale operations, turbines with > 200 MW capacity dominate, enabling advanced energy solutions for highly integrated process infrastructures.

- For instance, Mitsubishi Power’s H‑25 gas turbine series has exceeded 12.5 million operating hours globally and achieves combined-cycle efficiency around 54 percent LHV, offering highly reliable cogeneration options.

By Technology:

The market divides into open cycle and combined cycle systems. Open-cycle turbines remain a cost-effective option for industries seeking rapid power generation with lower initial investments and shorter installation timelines. It provides flexibility in operations, particularly in regions where fuel availability supports simpler turbine configurations. Combined-cycle turbines, on the other hand, gain strong traction due to their superior efficiency, lower emissions, and capability to reuse exhaust heat for enhanced energy output. The growing preference for cleaner and more efficient energy solutions supports higher adoption of combined-cycle systems in modern process plants. This technological shift aligns with increasing industrial focus on performance optimization and sustainability.

Segments:

Based on Product:

- Aero-derivative

- Heavy duty

Based on Capacity:

- ≤ 50 kW

- > 50 kW to 500 kW

- > 500 kW to 1 MW

- > 1 MW to 30 MW

- > 30 MW to 70 MW

- > 70 MW to 200 MW

- > 200 MW

Based on Technology:

- Open cycle

- Combined cycle

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

The Process Plants Gas Turbine market in North America holds a 35.7% share, supported by advanced energy infrastructure and strong reliance on natural gas power generation. The region focuses on deploying combined-cycle systems in refineries, petrochemical plants, and manufacturing facilities to enhance operational efficiency. It benefits from continuous modernization programs that improve turbine performance and reduce emissions. Digital monitoring solutions and predictive analytics strengthen operational reliability for process industries. OEMs invest in advanced low-emission combustion technologies to align with evolving environmental regulations. A well-established service network and robust financial support reinforce North America’s leadership in this market.

Asia Pacific

The Process Plants Gas Turbine market in Asia Pacific accounts for 37.2% of the global share, making it the largest regional contributor. Rapid industrialization in China, India, Japan, and Southeast Asia drives increasing demand for reliable and efficient onsite power generation. It shifts from coal-based energy systems toward natural gas turbines to comply with strict emission policies. Expanding LNG terminals, petrochemical capacities, and manufacturing clusters further accelerate adoption. The region favors medium- to high-capacity turbines ranging between 1 MW and 70 MW, supporting diverse industrial operations. Growing investment in hybrid energy solutions and renewable integration strengthens Asia Pacific’s dominance.

Europe

The Process Plants Gas Turbine market in Europe captures a 28% share, driven by the region’s aggressive decarbonization strategies. Countries focus on hydrogen-ready turbines and flexible power generation systems to replace aging coal and nuclear facilities. It invests heavily in cogeneration systems and advanced combined-cycle technologies to improve operational efficiency. Industrial hubs in Germany, the U.K., and Italy lead in adopting digital solutions and emission control technologies. Manufacturers enhance product offerings with low-NOx combustion systems and heat recovery features. The region’s R&D-driven initiatives ensure long-term competitiveness while supporting its transition to sustainable energy.

Latin America

The Process Plants Gas Turbine market in Latin America holds a 7% share, with steady growth supported by industrial expansion and infrastructure development. The region focuses on adopting combined-cycle turbines for manufacturing zones and captive power plants. It relies on turbines to overcome grid limitations and ensure operational reliability. Growing oil & gas refining activities in Brazil and Mexico create opportunities for heavy-duty turbine deployment. Governments offer incentives to encourage investments in energy-efficient technologies. Rising industrialization strengthens the role of gas turbines in achieving reliable and cost-effective power generation.

Middle East & Africa

The Process Plants Gas Turbine market in the Middle East & Africa secures an 8.3% share, driven by large-scale investments in petrochemical, refining, and LNG facilities. The region benefits from abundant natural gas reserves, ensuring a steady supply of fuel for turbines. It increasingly adopts combined-cycle and cogeneration systems to improve efficiency and meet high energy demands. Industrial operators focus on hydrogen-compatible solutions to align with long-term sustainability objectives. Gulf Cooperation Council nations lead with ambitious projects designed to diversify energy portfolios. Robust infrastructure growth supports consistent demand for advanced turbine technologies.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Mitsubishi Power, Ltd. (Japan)

- Rolls-Royce plc (U.K.)

- Siemens Energy AG (Germany)

- OPRA Turbines B.V. (Netherlands)

- Baker Hughes Company (U.S.)

- Kawasaki Heavy Industries, Ltd. (Japan)

- Ansaldo Energia S.p.A. (Italy)

- Solar Turbines Incorporated (U.S.)

- MAN Energy Solutions SE (Germany)

- General Electric Company (U.S.)

Competitive Analysis

General Electric Company (U.S.), Siemens Energy AG (Germany), Mitsubishi Power, Ltd. (Japan), Ansaldo Energia S.p.A. (Italy), Baker Hughes Company (U.S.)These leading companies dominate the Process Plants Gas Turbine market by focusing on innovation, operational efficiency, and strategic global expansion. General Electric Company leverages its advanced engineering capabilities and diversified energy portfolio to deliver highly efficient turbine solutions, with increasing emphasis on hydrogen-ready technologies. Siemens Energy AG prioritizes technological advancements and production scalability to meet rising global power demands, integrating digital monitoring solutions to enhance operational performance. Mitsubishi Power, Ltd. focuses on high-efficiency combined-cycle turbines and hydrogen-compatible systems, strengthening its position in energy transition projects worldwide. Ansaldo Energia S.p.A. competes through a strong portfolio of reliable medium- and heavy-duty turbines, supported by cost-effective pricing strategies and comprehensive maintenance services that cater to process plant operators. Baker Hughes Company capitalizes on robust financial performance, supplying advanced turbines for large-scale industrial facilities and responding quickly to evolving power generation needs. These players face challenges from increasing supply chain pressures, long lead times, and growing environmental regulations. However, they continue to strengthen their market positions by adopting digitalization, investing in R&D, and forming strategic collaborations to meet diverse industrial power requirements efficiently.

Recent Developments

- In April 2025, Duke Energy entered into a major deal with GE Vernova to procure up to 11 of the advanced 7HA gas turbine units for future energy projects.

- In February 2025, GE Vernova announced the launch of its next-generation HA gas turbine, a technological advancement focused on improving operational efficiency and reducing carbon emissions. This development supports cleaner energy production in process plants, aligning with global sustainability goals. The new turbine is expected to enhance power output while lowering fuel consumption, offering significant cost and environmental benefits to industrial users.

- In 2024, Siemens Energy introduced a cutting-edge digital twin technology designed to optimize the performance of gas turbines. By enabling real-time monitoring and predictive maintenance, this innovation enhances operational reliability and reduces downtime. The integration of this solution is anticipated to boost cost-efficiency for process plants, driving the broader adoption of smart energy systems across the sector

Report Coverage

The research report offers an in-depth analysis based on Product, Capacity, Technology and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand for gas turbines continues to rise due to accelerating industrialization and ongoing electrification across process industries.

- Manufacturers face extended lead times—often five years or more—driven by unprecedented demand, particularly in the U.S.

- Global deployment of new gas-fired capacity may reach nearly 890 GW between 2025 and 2040, with the U.S. and China contributing almost half of annual additions.

- The market value for process plants gas turbines will continue expanding, with projected compound annual growth rates (CAGR) between approximately 5.6% and 5.7% through the early 2030s.

- Heavy-duty gas turbines will dominate market share, exceeding 60% in several forecasts, thanks to their reliability in base-load and heavy process applications.

- Combined-cycle systems will remain the preferred configuration, capturing roughly 80% of deployment thanks to superior efficiency and heat recovery—especially in large process facilities.

- Hybrid solutions and hydrogen-ready turbines will gain ground, aligning with decarbonization goals and efforts to reduce emissions in industrial thermal energy generation.

- Regulatory pressure and low-emission mandates will continue driving modernization and retrofitting of legacy turbine systems in regions such as North America and Europe.

- Infrastructure investment, particularly in regions like Asia Pacific, will support deployment growth, given rising energy demand and industrial expansion.

- Manufacturers must navigate high capital costs, supply constraints, and competition from renewables, while maintaining operational flexibility and meeting stringent environmental standards.