| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Architectural Hardware Market Size 2024 |

USD 21,741.31 million |

| Architectural Hardware Market, CAGR |

6.53% |

| Architectural Hardware Market Size 2032 |

USD 37,405.28 million |

Market Overview

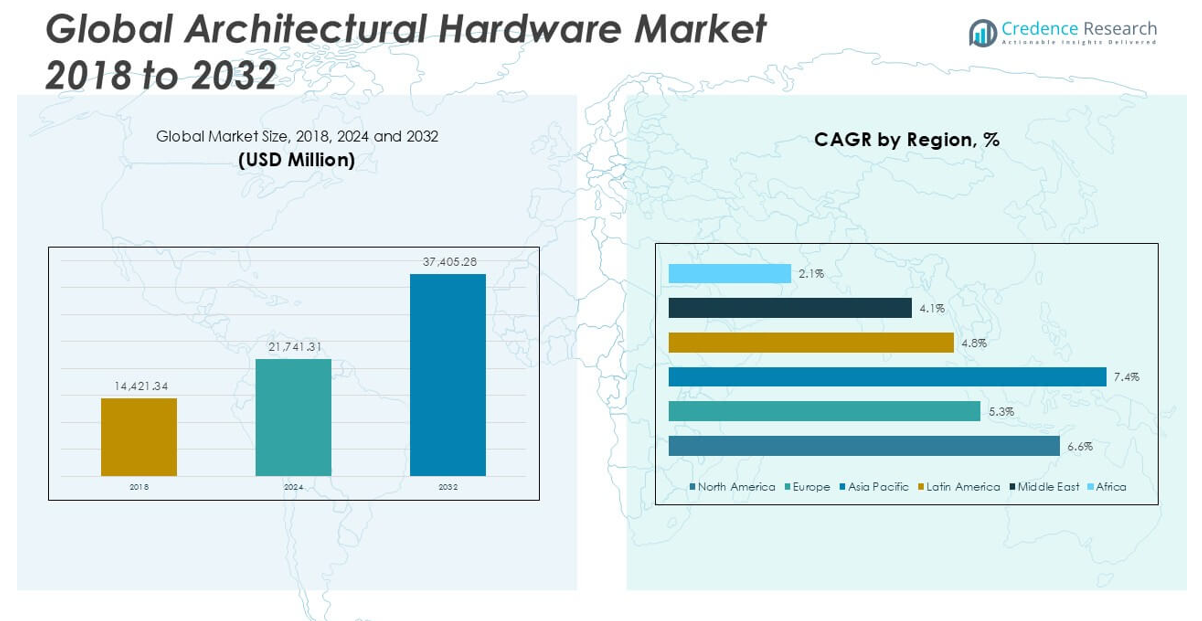

The Architectural Hardware Market size was valued at USD 14,421.34 million in 2018, increased to USD 21,741.31 million in 2024, and is anticipated to reach USD 37,405.28 million by 2032, growing at a CAGR of 6.53% during the forecast period.

The architectural hardware market is led by prominent players such as Assa Abloy AB, Allegion plc, CRH plc, Godrej & Boyce Mfg. Co. Ltd., Häfele GmbH & Co KG, and Hettich Holding GmbH, all of which hold strong positions due to their extensive product portfolios, global reach, and emphasis on innovation. These companies focus on advanced locking systems, smart hardware, and aesthetic designs to meet the evolving needs of residential and commercial users. Regionally, Asia Pacific dominates the market with a 43.3% share in 2024, driven by rapid urbanization, infrastructure development, and rising construction activities in countries like China and India. North America follows with a 31.3% share, fueled by demand for smart home solutions and high-end renovations.

Market Insights

- The architectural hardware market was valued at USD 21,741.31 million in 2024 and is projected to reach USD 37,405.28 million by 2032, growing at a CAGR of 6.53% during the forecast period.

- Market growth is primarily driven by rising urbanization, increasing residential and commercial construction, and growing demand for smart and secure architectural fittings.

- Key trends include the adoption of IoT-enabled smart locks, eco-friendly materials, and aesthetic product designs aligned with modern interior preferences.

- Leading players such as Assa Abloy AB, Allegion plc, and CRH plc dominate the competitive landscape, focusing on innovation, acquisitions, and expansion into emerging markets; however, the market faces restraints like fluctuating raw material prices and low standardization across product lines.

- Regionally, Asia Pacific holds the largest share at 43.3%, followed by North America at 31.3%; by application, the doors segment leads, driven by essential utility and security needs in all building types.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Application:

In the architectural hardware market, the doors segment holds the largest share due to the widespread use of door hardware in both residential and commercial constructions. This dominance is attributed to rising infrastructure development, growing demand for secure and automated locking systems, and frequent renovations of entryways in commercial spaces. Door hardware, including locks, hinges, and handles, is critical for both functionality and aesthetics. Meanwhile, windows and furniture segments are also gaining traction, driven by interior design trends and demand for ergonomic fittings, whereas the shower and others segment remains niche but steadily growing.

- For instance, Assa Abloy has installed more than 5 million electronic door locks globally, supporting large-scale commercial and residential door hardware adoption, particularly through its Aperio and SMARTair product lines.

By End User:

The residential segment leads the architectural hardware market in terms of market share, propelled by increasing urbanization, rising disposable incomes, and a surge in new housing developments globally. Consumers are increasingly investing in modern home aesthetics and enhanced security features, boosting demand for stylish and durable hardware components. Additionally, growing interest in home renovation and smart home integration is accelerating the adoption of advanced architectural hardware in residential settings. While commercial and industrial segments show strong demand, especially for large-scale infrastructure and public facilities, residential usage remains the dominant end-user category.

- For instance, Godrej Locks has supplied over 75 million locks to the Indian residential sector alone and has launched over 80 unique residential security SKUs over the past five years, reflecting deep residential market penetration.

Market Overview

Rapid Urbanization and Infrastructure Development

The surge in global urbanization has led to increased demand for residential and commercial buildings, directly fueling the need for architectural hardware. Government investments in public infrastructure, smart cities, and housing projects particularly in emerging economies—are creating a strong pipeline for new construction activities. This, in turn, accelerates the demand for door locks, handles, hinges, and other hardware products. The rising middle-class population and improving lifestyles further amplify residential renovations and real estate development, positioning architectural hardware as an essential component in modern infrastructure.

- For instance, Häfele operates in over 150 countries and supplies architectural fittings to more than 120,000 residential and commercial building projects annually, illustrating its active role in supporting large-scale urban infrastructure development.

Rising Focus on Home Security and Smart Hardware

Growing concerns over safety and security are prompting consumers and businesses to adopt advanced architectural hardware solutions. There is a significant shift from conventional locking systems to smart locks, digital door closers, and access control systems. This trend is especially prominent in urban settings and smart homes, where technology integration enhances both security and convenience. Manufacturers are investing in R&D to deliver innovative, IoT-enabled hardware solutions, which is accelerating product adoption and creating new revenue streams within the architectural hardware market.

- For instance, Allegion’s Schlage Encode™ smart deadbolt supports integration with over 30 major smart home platforms and has recorded over 1.2 million units shipped globally since launch, indicating widespread adoption in residential smart security.

Growth in Interior Design and Aesthetic Renovations

Increasing interest in interior aesthetics is driving demand for customized and design-centric architectural hardware. Consumers are seeking products that not only serve functional purposes but also complement modern architectural styles. This trend is especially prevalent in the premium housing and hospitality sectors, where the appearance of door knobs, handles, and fittings influences buyer decisions. The availability of a wide range of finishes, styles, and materials from vintage to minimalist is fueling the replacement and upgrade market, particularly in developed regions.

Key Trends & Opportunities

Adoption of Sustainable and Eco-friendly Materials

With sustainability becoming a priority in the construction industry, manufacturers are shifting toward eco-friendly materials such as recycled metals, low-VOC coatings, and energy-efficient production processes. Green building certifications and regulations further push for environmentally responsible architectural hardware solutions. This trend presents an opportunity for innovation in product design, where brands that align with green construction goals can gain a competitive edge and attract environmentally conscious consumers and commercial clients.

- For instance, Hettich reduced its carbon footprint by 2,100 metric tons in 2023 by switching to recycled zinc and adopting water-based coatings across its European manufacturing facilities, demonstrating its tangible commitment to sustainable production.

Integration of Smart and Connected Hardware

The emergence of smart building technologies has opened new avenues for architectural hardware manufacturers. Products integrated with Bluetooth, Wi-Fi, and biometric technologies are increasingly used in homes, offices, and hospitality settings. These smart solutions offer remote access, real-time monitoring, and enhanced user control, aligning with the broader push toward home automation. As consumers become more tech-savvy, the demand for integrated hardware systems presents a long-term growth opportunity for market players focused on digital innovation.

- For instance, Spectrum Brands’ Kwikset division has deployed over 10 million connected locksets, including its Halo Wi-Fi series, with mobile app downloads exceeding 2.3 million globally, validating consumer interest in smart hardware ecosystems.

Key Challenges

Fluctuations in Raw Material Prices

Volatility in the prices of key raw materials such as stainless steel, aluminium, and brass poses a significant challenge to manufacturers. These cost fluctuations impact production planning and profitability, especially for small and medium enterprises with limited pricing flexibility. Additionally, global supply chain disruptions and geopolitical tensions can exacerbate cost pressures, forcing companies to either absorb losses or increase product prices, which may affect competitiveness in price-sensitive markets.

Lack of Standardization and Fragmented Market Structure

The architectural hardware market remains highly fragmented, with numerous local and regional players offering varied quality and pricing structures. The lack of standardization across products and installation practices creates inconsistency in performance and reliability. This fragmentation complicates large-scale procurement for commercial projects and can result in compatibility issues, delaying installations or increasing maintenance costs. For global players, maintaining consistent brand quality and compliance across regions remains a substantial challenge.

Slow Adoption in Emerging Economies

Despite growing construction activities, the adoption of advanced and premium architectural hardware in emerging economies remains relatively slow. Budget constraints, lack of awareness about modern solutions, and preference for low-cost traditional alternatives hinder market penetration. Additionally, limited access to organized retail or distribution channels in rural and semi-urban areas restricts product visibility and availability. Market players must invest in awareness campaigns and distribution networks to overcome these barriers and tap into underserved regions.

Regional Analysis

North America

North America accounted for the largest share of the architectural hardware market in 2024, contributing approximately 31.3% of the global revenue with a market size of USD 6,800.79 million, up from USD 4,576.47 million in 2018. The market is projected to reach USD 11,745.45 million by 2032, registering a strong CAGR of 6.6%. Growth in the region is driven by advanced construction practices, high adoption of smart home systems, and significant investments in residential renovation and commercial infrastructure. The presence of established manufacturers and demand for premium-grade hardware also support sustained market expansion.

Europe

Europe represented about 17.4% of the architectural hardware market in 2024, with a market size of USD 3,784.57 million, rising from USD 2,657.85 million in 2018. The market is forecasted to reach USD 5,912.75 million by 2032, expanding at a CAGR of 5.3%. Growth is supported by increased emphasis on aesthetic interiors, adoption of sustainable building materials, and renovation of aging infrastructure across Western Europe. Regulatory standards for energy efficiency and safety also contribute to demand for high-quality architectural fittings, while growing tourism boosts the hospitality sector’s use of modern architectural hardware solutions.

Asia Pacific

Asia Pacific held the largest regional share after North America in 2024, contributing around 43.3% of the global market with a value of USD 9,424.31 million, rising sharply from USD 6,018.60 million in 2018. The region is expected to reach USD 17,248.14 million by 2032, growing at the fastest CAGR of 7.4%. Rapid urbanization, large-scale infrastructure projects, and increasing residential construction in China, India, and Southeast Asia are major growth drivers. Additionally, expanding middle-class populations and rising disposable incomes are fueling demand for both affordable and premium architectural hardware across residential and commercial sectors.

Latin America

In 2024, Latin America contributed 4.3% to the global architectural hardware market, with a market size of USD 948.85 million, increasing from USD 637.86 million in 2018. The market is forecast to reach USD 1,431.98 million by 2032, growing at a moderate CAGR of 4.8%. Growth is driven by the recovery of construction sectors in Brazil, Mexico, and Chile, along with gradual investments in residential housing and commercial infrastructure. Rising demand for modern, aesthetically appealing hardware in urban centers and the gradual penetration of smart and sustainable hardware solutions support market expansion in the region.

Middle East

The Middle East accounted for approximately 2.4% of the global architectural hardware market in 2024, with a market value of USD 517.95 million, up from USD 378.27 million in 2018. It is projected to reach USD 741.50 million by 2032, growing at a CAGR of 4.1%. Market growth is fueled by mega construction projects in the UAE, Saudi Arabia, and Qatar, including commercial complexes, luxury hotels, and residential high-rises. The demand for premium-grade and customized architectural hardware is on the rise, supported by regional visions like Saudi Arabia’s Vision 2030 and increasing tourism-related infrastructure.

Africa

Africa represented the smallest regional share in 2024, contributing 1.2% of the global market with a value of USD 264.83 million, growing from USD 152.29 million in 2018. The market is projected to reach USD 325.47 million by 2032, at a CAGR of 2.1%. Despite limited growth, demand is slowly increasing due to urban migration, government-led affordable housing initiatives, and infrastructure development in countries like Nigeria, Kenya, and South Africa. However, challenges such as limited access to advanced hardware products, low consumer awareness, and pricing sensitivity continue to restrict large-scale market penetration across the continent.

Market Segmentations:

By Application

- Doors

- Windows

- Furniture

- Shower

- Others

By End User

- Commercial

- Industrial

- Residential

By Geography:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The architectural hardware market is characterized by a mix of global giants and regional players competing on the basis of product quality, innovation, brand reputation, and distribution reach. Key players such as Assa Abloy AB, Allegion plc, CRH plc, Godrej & Boyce Mfg. Co. Ltd., Häfele GmbH & Co KG, and Hettich Holding GmbH hold a significant market share due to their broad product portfolios and strong global presence. These companies focus heavily on research and development to introduce smart and energy-efficient hardware solutions aligned with evolving construction trends. Strategic initiatives such as mergers, acquisitions, and partnerships are commonly adopted to strengthen regional footprints and access emerging markets. Furthermore, market participants are increasingly investing in e-commerce and digital marketing channels to enhance customer engagement. Despite the dominance of established players, regional and local manufacturers continue to thrive by offering cost-effective and customized solutions, maintaining a highly competitive and fragmented market structure.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- CRH plc

- Godrej & Boyce Mfg. Co. Ltd.

- Häfele GmbH & Co KG

- Hettich Holding GmbH and Co. oHG

- Allegion plc

- Assa Abloy AB

- Spectrum Brands Inc.

- Archer Daniels Midland Company

- HOPPE Holding AG

Recent Developments

- In May 2025, CRH chose Neocrete to participate in its Sustainable Building Materials Accelerator program. This initiative focuses on piloting low-carbon concrete technologies within CRH’s global operations, emphasizing sustainability in building materials, including architectural hardware. Neocrete was selected from over 100 startups globally.

- In 2025, market reports highlight Häfele’s continued innovation in architectural hardware, specifically focusing on smart and luxury fittings, along with user-friendly digital locking systems. The company is also expanding its range of finishes and designs to align with contemporary architectural trends.

- In 2025, Allegion is indeed gaining recognition for its advancements in smart security hardware, specifically in digital locks and access control systems that allow for remote management via smartphones. This is driven by their continued investment in research and development, which has led to the introduction of new products that enhance both building security and user convenience.

- In 2025, ASSA ABLOY is continuing its focus on digital and connected locking solutions, including biometric and wireless access control, while also prioritizing sustainable materials and finishes to align with green building standards. The company is showcasing its integrated solutions at events like Intersec 2025.

Market Concentration & Characteristics

The Architectural Hardware Market displays a moderately fragmented structure, with a mix of global corporations and regional manufacturers operating across various segments. It features a competitive environment driven by product innovation, customization, and design aesthetics. Companies focus on expanding product lines to meet the rising demand for smart, secure, and visually appealing hardware in residential and commercial spaces. It benefits from consistent demand in mature regions and rapid growth in emerging markets due to urbanization and infrastructure development. Leading players invest in research and development, strategic mergers, and acquisitions to enhance market share and technological capabilities. The market shows strong alignment with evolving construction practices and sustainability standards. Standardization remains limited, particularly among regional suppliers, which creates challenges in large-scale commercial procurement. Price sensitivity influences consumer choices in developing regions, while quality and brand reputation hold more weight in developed markets. The market demonstrates steady growth, supported by government housing projects, commercial real estate expansion, and consumer preference for aesthetic interiors.

Report Coverage

The research report offers an in-depth analysis based on Application, End User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will continue to grow steadily, driven by rising residential and commercial construction activities worldwide.

- Demand for smart and connected hardware systems will increase with the adoption of home automation technologies.

- Urbanization in developing countries will create new opportunities for hardware suppliers and manufacturers.

- Sustainability and eco-friendly materials will become standard requirements in hardware product development.

- Manufacturers will focus more on design aesthetics to meet the expectations of modern interior design trends.

- E-commerce platforms will play a greater role in product distribution and customer engagement.

- Investments in R&D will rise to support innovation in functionality, durability, and digital integration.

- The replacement and renovation segment will expand due to aging infrastructure and design upgrades.

- Market players will strengthen their regional presence through strategic partnerships and acquisitions.

- Regulatory compliance and quality certification will grow more important in competitive positioning.