| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Aerospace and Defense ASIC Market Size 2024 |

USD 1,817.07 million |

| Aerospace and Defense ASIC Market , CAGR |

10.69% |

| Aerospace and Defense ASIC Market Size 2032 |

USD 4,333.28 million |

Market Overview:

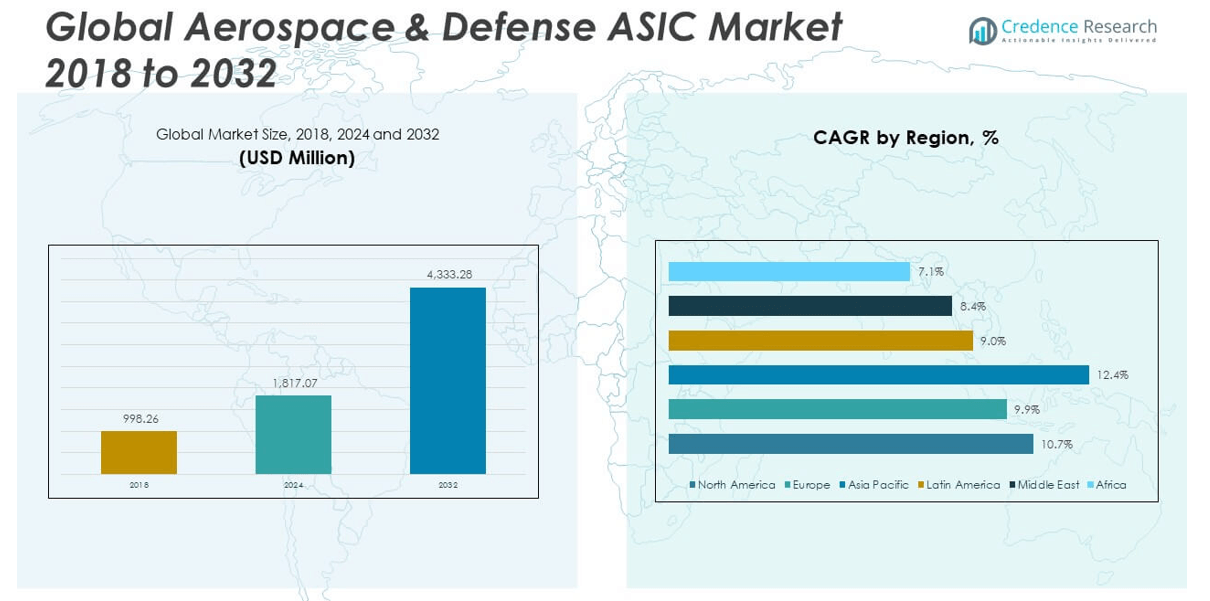

The Global Aerospace & Defense ASIC Market size was valued at USD 998.26 million in 2018 to USD 1,817.07 million in 2024 and is anticipated to reach USD 4,333.28 million by 2032, at a CAGR of 10.69% during the forecast period.

The market is primarily driven by several key factors. Increasing global defense expenditure is prompting governments and private contractors to modernize equipment with advanced technologies, including ASIC-based systems for radar, navigation, signal processing, and space electronics. These chips offer tailored functionality, enhanced performance, and better energy efficiency compared to general-purpose processors, making them ideal for rugged aerospace and defense environments. Moreover, the proliferation of unmanned systems such as drones and autonomous military vehicles has heightened the need for lightweight, power-optimized ASICs capable of performing AI and ML tasks on edge devices. Additionally, the commercial aerospace sector is embracing digital transformation, integrating ASICs in aircraft maintenance systems, avionics, and in-flight connectivity platforms. Together, these drivers are fostering a dynamic shift toward high-reliability, application-specific solutions across both defense and aerospace domains.

Regionally, North America dominates the global Aerospace & Defense ASIC Market due to its advanced defense infrastructure, significant R&D funding, and the presence of major aerospace companies and chip manufacturers. The U.S. continues to lead in deploying ASICs across a broad range of military and space applications. Europe follows closely, propelled by collaborative defense initiatives, increased military spending across NATO countries, and strong aerospace sectors in France, Germany, and the UK. Meanwhile, Asia Pacific is emerging as the fastest-growing region, driven by rising defense modernization in China, India, South Korea, and Japan. These nations are investing heavily in indigenous aerospace programs and next-gen military capabilities, which require robust, localized semiconductor development. Other regions like the Middle East and Latin America are also gradually increasing their adoption of ASICs for surveillance systems, secure communications, and regional aerospace programs, further expanding the global market footprint.

Market Insights:

- The market size reached USD 1,817.07 million in 2024 and is projected to grow to USD 4,333.28 million by 2032, expanding at a CAGR of 10.69%.

- Rising defense budgets and modernization programs are accelerating adoption of ASIC-based systems for radar, navigation, signal processing, and space applications.

- The proliferation of UAVs and autonomous military vehicles is increasing demand for power-efficient, AI-capable ASICs designed for real-time edge computing.

- Custom ASICs are preferred in harsh aerospace environments due to their secure communication capabilities, radiation tolerance, and optimized SWaP attributes.

- High development costs, long design cycles, and regulatory compliance are key challenges limiting broader market participation and innovation speed.

- North America leads the market share due to its advanced defense infrastructure, while Asia Pacific is the fastest-growing region, driven by defense self-reliance in China, India, and Japan.

- Global shifts toward domestic semiconductor supply chains and IP control are shaping long-term strategies, with countries investing in sovereign ASIC capabilities.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Rising Demand for Customized and Mission-Critical Electronics in Aerospace and Defense Systems

The Global Aerospace & Defense ASIC Market is gaining momentum due to the growing need for specialized, mission-specific electronics in both commercial aerospace and military platforms. ASICs offer tailored functionalities that meet stringent size, weight, and power (SWaP) constraints critical in avionics, radar systems, missile guidance, and satellite payloads. Defense programs increasingly prioritize compact and efficient systems that can withstand extreme environmental conditions and deliver consistent performance. Custom ASICs enable secure communication, high-speed data processing, and fault-tolerant operations in complex systems. Governments and defense contractors are investing heavily in next-generation platforms that depend on semiconductor innovation. This has created steady demand for ASICs tailored to perform critical functions across airborne, naval, and space-based defense infrastructure.

- For example, ON Semiconductor’s collaboration with ICs LLC produced radiation-hardened ASICs using the ONC110 110nm process, specifically designed for high-reliability environments such as satellite communication, avionics, and unmanned aerial vehicles.

Modernization of Defense Infrastructure and Growing Government Expenditure

Modern defense strategies rely on advanced electronics to improve precision, situational awareness, and system integration. The Global Aerospace & Defense ASIC Market benefits directly from increased military spending by countries seeking technological superiority. Programs related to unmanned aerial vehicles (UAVs), hypersonic weapons, space-based surveillance, and electronic warfare all require custom chipsets that deliver optimized processing capabilities. ASICs play an integral role in enhancing radar resolution, enabling secure telemetry, and powering onboard control systems. Many countries are shifting from legacy systems toward modular, upgradable electronics platforms that rely on ASICs for seamless interoperability. This focus on defense modernization continues to strengthen demand for ASICs designed for long lifecycle use and secure data handling.

- For example, the U.S. Department of Defense’s FY2025 budget allocated $6.9 billion for hypersonic research, up from $4.7 billion in FY2023, reflecting a substantial increase in investment for next-generation electronic systems.

Integration of Artificial Intelligence and Edge Computing in Defense Applications

Military operations increasingly depend on artificial intelligence (AI) and edge computing to support real-time decision-making and autonomous capabilities. The Global Aerospace & Defense ASIC Market is expanding as ASICs enable low-latency processing and energy-efficient execution of AI models at the device level. Drones, robotic systems, and advanced surveillance equipment now incorporate AI algorithms that must function in environments with limited connectivity and power resources. Standard processors often fail to meet the performance-to-power ratio required in such conditions, making ASICs the preferred choice. These chips offer embedded intelligence without compromising speed, accuracy, or security. The growing convergence of aerospace systems with AI technologies elevates the importance of custom silicon in operational readiness.

Shift Toward Secure, Sovereign Semiconductor Supply Chains

Geopolitical tensions and export control regulations have prompted governments to secure local supply chains for critical defense technologies. The Global Aerospace & Defense ASIC Market reflects this shift, with countries encouraging domestic ASIC design and fabrication to ensure strategic independence. National defense strategies increasingly include semiconductor self-sufficiency to avoid dependency on foreign chipmakers. It also helps mitigate risks of component shortages and cybersecurity breaches associated with imported hardware. Leading aerospace contractors collaborate with local foundries and IP providers to co-develop application-specific chips that meet national standards. This shift supports consistent investment in indigenous ASIC capabilities and reinforces the strategic value of semiconductors in national security planning.

Market Trends:

Adoption of Radiation-Hardened ASICs for Space and High-Altitude Applications

The Global Aerospace & Defense ASIC Market is experiencing strong interest in radiation-hardened (rad-hard) chip technologies, particularly for satellites, deep-space missions, and high-altitude defense systems. These environments expose electronics to extreme levels of radiation that can corrupt data and damage standard semiconductor components. Rad-hard ASICs ensure continued functionality by withstanding ionizing radiation without performance degradation. Space agencies and defense contractors prioritize these chips in missile defense systems, orbital surveillance, and secure satellite communication platforms. Demand continues to grow as governments fund more space-based initiatives. The focus on resilient electronics drives innovation in materials, layout design, and shielding techniques specific to aerospace-grade ASICs.

Increased Use of System-on-Chip (SoC) Designs for Compact Electronic Platforms

There is a noticeable shift toward integrating multiple subsystems into single-chip solutions using System-on-Chip (SoC) architecture. The Global Aerospace & Defense ASIC Market is embracing this trend to reduce board space, weight, and power consumption in mission-critical applications. SoCs combine processing units, memory, input/output controls, and specialized logic onto a single silicon die. It enables real-time performance improvements and simplifies system integration in platforms such as drones, fighter aircraft, and portable command systems. Design consolidation through SoC enhances reliability while reducing interconnect failure risks. The trend aligns with the sector’s broader objective of miniaturizing electronics without compromising capability.

- For instance, Microchip Technology’s PolarFire Core SoCs and FPGAs are tailored for aerospace and defense, integrating quad-core, 64-bit RISC-V processors and offering single-event upset immunity for mission-critical reliability. These devices achieve up to 30% cost savings by eliminating integrated transceivers while maintaining low power consumption and robust security.

Growing Emphasis on Lifecycle Support and Upgradability of ASIC-Based Systems

Defense procurement programs are emphasizing longer system lifecycles with upgradable electronics. The Global Aerospace & Defense ASIC Market is aligning with this shift by developing reconfigurable and modular ASIC designs. These chips support post-deployment updates through programmable logic blocks or hybrid analog-digital architectures. Manufacturers now provide extended product support, simulation tools, and lifecycle documentation to facilitate sustainment over decades. Lifecycle adaptability reduces the need for complete hardware replacement during system modernization efforts. It also ensures compatibility with evolving mission profiles and communication protocols. This trend reflects the sector’s preference for future-proof electronics that reduce total ownership cost.

Expansion of 3D IC and Heterogeneous Integration in Aerospace ASIC Designs

Advanced packaging methods such as 3D IC stacking and heterogeneous integration are gaining traction in aerospace ASIC manufacturing. The Global Aerospace & Defense ASIC Market benefits from these methods by enabling high-density interconnects and faster signal transmission between components. 3D architectures allow vertical stacking of dies to boost performance without enlarging the device footprint. Heterogeneous integration combines diverse technologies such as RF, digital, and photonic elements on a single substrate. These innovations enhance data processing speed and bandwidth, which are essential for real-time threat detection, navigation, and autonomous decision systems. Design flexibility and space optimization make these techniques vital in next-generation defense platforms.

- For instance, Alchip Technologieshas launched silicon-proven 3DIC ASIC design services, optimizing power delivery, die-to-die electrical interconnect, and system-wide thermal characterization for high-performance aerospace ASICs. Their 3DIC design flow utilizes through-silicon vias (TSVs) and hybrid bonding, achieving higher data transfer rates, reduced power consumption, and minimized device footprint.

Market Challenges Analysis:

High Development Costs and Extended Design Cycles Limit Market Accessibility

The Global Aerospace & Defense ASIC Market faces considerable barriers due to the high cost and time requirements associated with custom chip development. Designing an ASIC demands extensive verification, prototyping, and qualification processes to meet strict aerospace and defense standards. These requirements lead to prolonged development timelines and elevated non-recurring engineering (NRE) expenses. Smaller firms and new market entrants often struggle to justify the investment in low-volume applications where return on investment remains uncertain. It also creates dependency on a limited pool of specialized design firms and fabrication partners. This financial and technical complexity reduces market agility and slows innovation adoption across some defense segments.

Stringent Regulatory Compliance and Export Control Restrictions Hinder Global Collaboration

The Global Aerospace & Defense ASIC Market operates within a tightly regulated environment marked by export controls, intellectual property restrictions, and national security policies. Governments impose strict compliance mandates to protect sensitive technologies, especially in defense-grade semiconductors. These controls complicate international collaboration, delay cross-border supply chains, and limit access to advanced fabrication nodes for certain countries. Companies must navigate evolving geopolitical dynamics while maintaining secure design environments and traceable component sourcing. Regulatory risk also increases the operational burden on manufacturers, often requiring localized production or special licensing agreements. It places pressure on timelines and resources, particularly for multinational defense programs involving ASIC integration.

Market Opportunities:

Expansion of Commercial Space Programs and Private Aerospace Ventures

The Global Aerospace & Defense ASIC Market presents strong growth potential through the rise of commercial space exploration and private aerospace enterprises. Companies such as SpaceX, Blue Origin, and Rocket Lab are developing satellites, launch systems, and autonomous spacecraft that require high-performance, radiation-hardened ASICs. These private initiatives drive demand for advanced onboard computing, telemetry, and communication systems optimized for harsh space environments. It allows ASIC manufacturers to tap into a growing commercial segment that complements traditional government contracts. The expanding satellite internet and Earth observation markets also contribute to increased ASIC deployment in low-Earth orbit systems.

Integration of Quantum and Photonic Technologies into Defense Applications

Emerging quantum and photonic technologies create long-term opportunities for innovation in the Global Aerospace & Defense ASIC Market. Governments are funding research into secure quantum communication, ultra-precise navigation, and advanced sensing systems. These technologies require custom ASICs to support low-latency processing, ultra-fast data conversion, and interface control with new physical architectures. It opens pathways for collaborative development between defense agencies and semiconductor firms specializing in next-generation materials and packaging. The demand for novel chip architectures aligned with quantum systems is expected to grow steadily, creating a new frontier for specialized ASIC adoption.

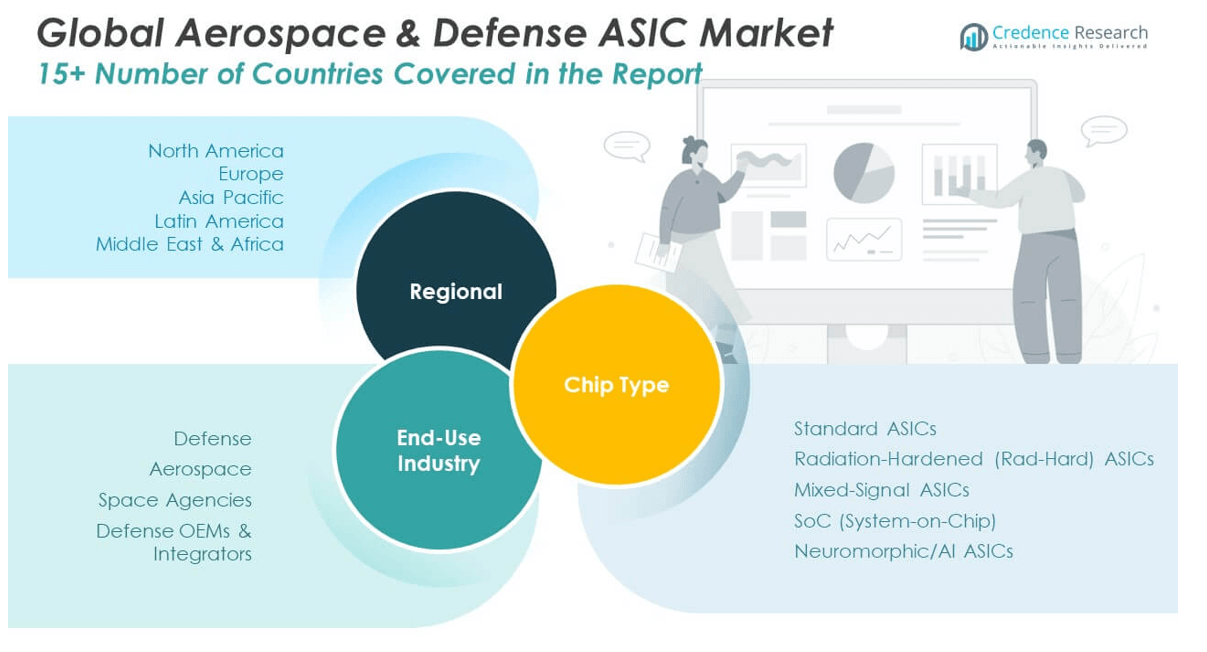

Market Segmentation Analysis:

The Global Aerospace & Defense ASIC Market is segmented by chip type and end-use industry, reflecting the diverse applications and specialized demands of this sector.

By chip type, Standard ASICs account for a significant share due to their versatility and use in general defense electronics. Radiation-Hardened (Rad-Hard) ASICs dominate critical space and high-altitude systems where resilience against cosmic radiation is essential. Mixed-Signal ASICs serve in communication, navigation, and signal-processing platforms, combining analog and digital functionalities. System-on-Chip (SoC) designs are gaining traction for compact, integrated solutions in avionics and UAVs. Neuromorphic/AI ASICs represent an emerging segment, driven by the integration of AI in autonomous defense systems and real-time surveillance.

- For example, BAE Systems’ RH12™ ASICs are deployed in geosynchronous satellites and deep-space probes. These chips are engineered to withstand radiation doses exceeding 1 megarad, ensuring uninterrupted operation in high-radiation environments such as NASA’s Mars missions and DoD missile defense satellites.

By end-use industry, the Defense segment leads the market, driven by consistent government spending on radar systems, electronic warfare, and missile guidance. The Aerospace segment follows closely, with demand for ASICs in flight control systems, avionics, and in-flight connectivity. Space Agencies increasingly deploy ASICs in satellite payloads and deep-space missions due to reliability and radiation tolerance. Defense OEMs & Integrators use customized ASICs to meet performance, security, and interoperability requirements across platforms. The market reflects a balanced mix of innovation, reliability, and mission-specific customization across all segments.

- For instance, Honeywell’s Application-Specific Integrated Circuits are embedded in the Primus Epic avionics suite, providing flight control, navigation, and in-flight connectivity for commercial and military aircraft, including the Gulfstream G650 and Embraer E2 jets.

Segmentation:

By Chip Type

- Standard ASICs

- Radiation-Hardened (Rad-Hard) ASICs

- Mixed-Signal ASICs

- SoC (System-on-Chip)

- Neuromorphic/AI ASICs

By End-Use Industry

- Defense

- Aerospace

- Space Agencies

- Defense OEMs & Integrators

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America

The North America Aerospace & Defense ASIC Market size was valued at USD 397.76 million in 2018 to USD 715.77 million in 2024 and is anticipated to reach USD 1,712.14 million by 2032, at a CAGR of 10.7% during the forecast period. North America holds the largest share in the Global Aerospace & Defense ASIC Market, accounting for nearly 38% of global revenue. The region benefits from substantial defense budgets, advanced R&D ecosystems, and the presence of major aerospace OEMs and chipmakers. The U.S. Department of Defense continues to prioritize ASIC-based technologies for applications in radar, electronic warfare, and satellite systems. It maintains a strong focus on domestic chip manufacturing and secure supply chains under initiatives such as CHIPS and Science Act. Defense primes like Lockheed Martin, Raytheon, and Northrop Grumman collaborate with semiconductor specialists to deliver customized, high-reliability ASICs. The region’s mature infrastructure and regulatory frameworks support continuous innovation and rapid deployment across land, air, sea, and space platforms.

Europe

The Europe Aerospace & Defense ASIC Market size was valued at USD 314.79 million in 2018 to USD 554.41 million in 2024 and is anticipated to reach USD 1,252.80 million by 2032, at a CAGR of 9.9% during the forecast period. Europe represents nearly 29% of the Global Aerospace & Defense ASIC Market share, driven by joint defense programs and increased military modernization across EU and NATO countries. France, Germany, and the UK lead regional spending on ASIC-based systems in aircraft, missile systems, and communication platforms. European defense agencies actively pursue sovereignty in semiconductor technologies to reduce dependence on foreign suppliers. It also benefits from a growing number of space missions and satellite deployments under ESA and national programs. Firms like Airbus, BAE Systems, and Leonardo are accelerating ASIC adoption for modular avionics and secure data processing. The region emphasizes interoperability, long-term lifecycle support, and environmental compliance in its ASIC design standards.

Asia Pacific

The Asia Pacific Aerospace & Defense ASIC Market size was valued at USD 198.00 million in 2018 to USD 389.73 million in 2024 and is anticipated to reach USD 1,049.17 million by 2032, at a CAGR of 12.4% during the forecast period. Asia Pacific accounts for approximately 23% of the Global Aerospace & Defense ASIC Market and is the fastest-growing region due to aggressive defense modernization and expanding space programs. China, India, Japan, and South Korea are increasing investments in domestically developed ASICs to support indigenous missile, radar, and UAV systems. It is also driving innovation through public-private partnerships in semiconductor R&D and localized chip fabrication. National security strategies across the region prioritize ASIC deployment in surveillance, navigation, and cyber-defense platforms. The growth in commercial space ventures further supports regional ASIC demand. Regulatory support and growing defense exports contribute to Asia Pacific’s leadership in next-generation defense electronics.

Latin America

The Latin America Aerospace & Defense ASIC Market size was valued at USD 46.04 million in 2018 to USD 82.74 million in 2024 and is anticipated to reach USD 174.09 million by 2032, at a CAGR of 9.0% during the forecast period. Latin America holds a modest 4% share of the Global Aerospace & Defense ASIC Market, with Brazil and Mexico leading regional demand. Governments are investing selectively in satellite communications, border surveillance, and aerospace research centers that require reliable ASIC solutions. It faces challenges due to budget constraints and import dependencies, yet regional defense agencies are exploring co-development agreements to access advanced chip technologies. Strategic partnerships with European and U.S.-based defense firms are helping Latin America improve its ASIC capabilities. It presents niche opportunities in modernization programs for air traffic management and military avionics. Regional priorities include cost-effective, rugged ASICs that comply with international standards.

Middle East

The Middle East Aerospace & Defense ASIC Market size was valued at USD 28.07 million in 2018 to USD 46.73 million in 2024 and is anticipated to reach USD 94.10 million by 2032, at a CAGR of 8.4% during the forecast period. The Middle East contributes around 3% to the Global Aerospace & Defense ASIC Market and continues to grow steadily due to strategic defense procurement and sovereign capability building. Countries like Saudi Arabia and the UAE are investing in military electronics, satellite systems, and localized production of defense equipment. It emphasizes ASIC adoption in border security, air defense systems, and integrated command platforms. National Vision initiatives are pushing local semiconductor and defense tech development. Regional demand focuses on robust, secure chips with minimal power requirements for extreme operational environments. International collaborations are critical to boosting ASIC access and technical know-how.

Africa

The Africa Aerospace & Defense ASIC Market size was valued at USD 13.60 million in 2018 to USD 27.69 million in 2024 and is anticipated to reach USD 50.96 million by 2032, at a CAGR of 7.1% during the forecast period. Africa holds under 2% of the Global Aerospace & Defense ASIC Market but is beginning to adopt advanced electronics for strategic applications. Countries such as South Africa, Nigeria, and Egypt are strengthening defense and aerospace infrastructure, creating demand for surveillance and communication ASICs. It is engaging in limited space missions, border monitoring systems, and drone programs that rely on custom chip solutions. Budget limitations and lack of domestic semiconductor capabilities pose ongoing challenges. International aid, defense partnerships, and academic collaborations are shaping ASIC-related capacity building. Growth is gradual, but focused investment in specific defense programs is helping the region enter the ASIC value chain.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Honeywell International Inc.

- Raytheon Technologies

- Northrop Grumman

- BAE Systems

- Lockheed Martin

- General Electric (GE Aerospace)

- Airbus

- Boeing

- Siemens

- Thales Group

Competitive Analysis:

The Global Aerospace & Defense ASIC Market is highly competitive, with a mix of established semiconductor manufacturers and specialized defense contractors. Key players include BAE Systems, Lockheed Martin, Raytheon Technologies, Northrop Grumman, Intel, Xilinx (AMD), and Microsemi (Microchip Technology). It benefits from vertically integrated capabilities where companies manage design, fabrication, and testing to meet stringent aerospace requirements. Leading firms focus on developing radiation-hardened, secure, and low-power ASICs tailored for avionics, radar, and space systems. Strategic partnerships with defense agencies and space organizations enhance product development and long-term contracts. The market shows high entry barriers due to IP protection, compliance standards, and significant R&D costs. Innovation, reliability, and supply chain resilience define competitive positioning across this sector.

Recent Developments:

- In February 2025, Honeywell announced a strategic collaborationwith ForwardEdge ASIC LLC, a subsidiary of Lockheed Martin Corporation, to develop reliable and radiation-hardened microelectronics for space applications. This partnership aims to combine Honeywell’s proven foundry technology with ForwardEdge ASIC’s advanced architecture and design solutions, focusing on the creation of innovative Application Specific Integrated Circuits (ASICs) for satellites and other space missions.

- In late June 2025, TransDigm Group revealed its acquisition of Simmonds Precision Products from RTX Corp for $765 million in cash. Simmonds is known for its expertise in fuel, proximity sensing, and structural health monitoring technologies—fields deeply intertwined with aerospace and defense electronics. By adding Simmonds to its portfolio, TransDigm strengthens its position in ASIC-powered sensor systems across both commercial and military aircraft platforms.

Market Concentration & Characteristics:

The Global Aerospace & Defense ASIC Market exhibits moderate to high market concentration, with a few dominant players holding a significant share due to specialized expertise and long-term defense contracts. It is characterized by high entry barriers, driven by complex design requirements, strict regulatory compliance, and the need for secure, mission-specific performance. The market favors vertically integrated companies capable of handling end-to-end ASIC development under secure, defense-grade environments. Long product development cycles and extended system lifespans define procurement behavior. It relies heavily on trusted supply chains, domestic sourcing policies, and government-backed funding for R&D. The demand for reliability, fault tolerance, and environmental durability shapes both product features and vendor selection.

Report Coverage:

The research report offers an in-depth analysis based on Chip Type and End-Use Industry. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Increasing investments in AI-powered defense platforms will drive demand for low-latency, application-specific ASICs.

- Expansion of commercial space programs will create new opportunities for radiation-hardened chip solutions.

- Growing emphasis on edge computing in UAVs and autonomous systems will support ASIC integration.

- Enhanced government focus on semiconductor self-sufficiency will boost domestic ASIC development.

- Advancements in 3D IC and heterogeneous integration will redefine performance benchmarks.

- Rising cybersecurity threats will accelerate adoption of secure and tamper-resistant ASIC architectures.

- Long-term defense contracts will ensure consistent revenue streams for established ASIC vendors.

- Miniaturization of aerospace electronics will favor compact, high-density ASICs over traditional processors.

- International collaborations will lead to co-development of mission-specific ASIC platforms.

- Sustainable procurement policies will encourage energy-efficient and lifecycle-optimized chip designs.