| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Data Center ASIC Market Size 2024 |

USD 3,493.70 million |

| Data Center ASIC Market, CAGR |

5.34% |

| Data Center ASIC Market Size 2032 |

USD 5,460.53 million |

Market Overview:

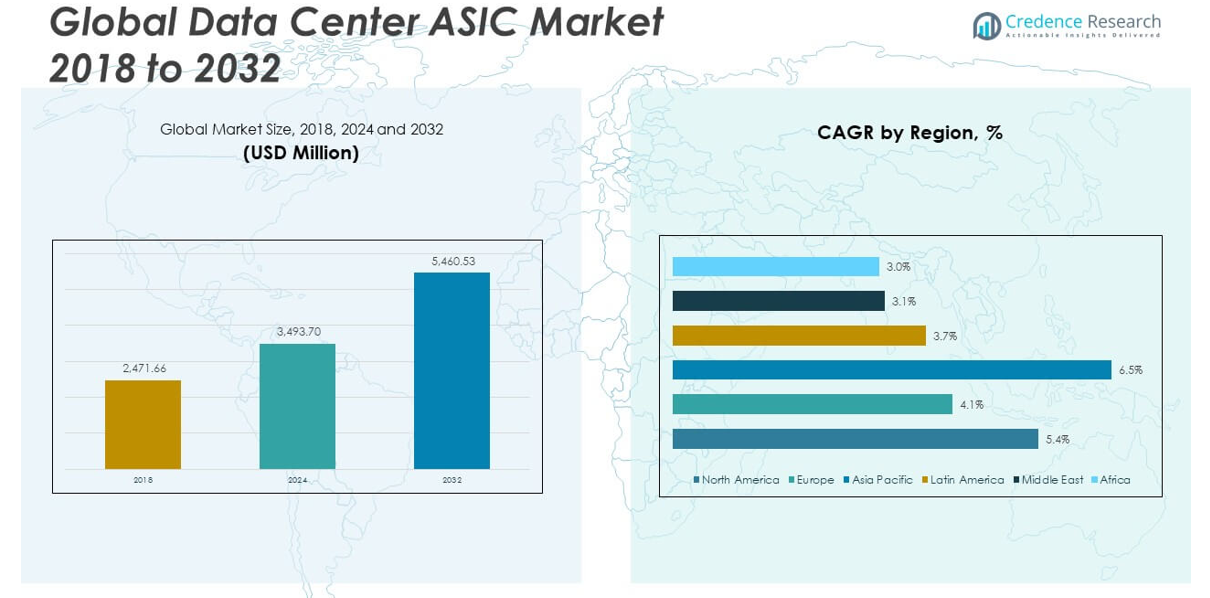

The Global Data Center ASIC Market size was valued at USD 2,471.66 million in 2018 to USD 3,493.70 million in 2024 and is anticipated to reach USD 5,460.53 million by 2032, at a CAGR of 5.34% during the forecast period.

Several key drivers are propelling the market forward. First, the rising volume and complexity of AI/ML workloads are prompting hyperscalers like Google, Microsoft, and AWS to invest in custom ASIC solutions to achieve lower latency and higher throughput. These companies are also pursuing cost efficiencies and performance advantages by designing proprietary chips such as Google’s TPU and AWS’s Graviton. Second, the surge in global data generation—driven by streaming services, IoT devices, and cloud computing—is pushing data centers to adopt faster and more efficient processing architectures, where ASICs outperform traditional chips in power efficiency and workload specialization. Third, the increasing emphasis on energy-efficient infrastructure is making ASICs an attractive solution, especially as organizations strive to lower operating costs and meet sustainability goals. Together, these factors are reinforcing ASIC adoption as a long-term strategic priority across the data center ecosystem.

Regionally, North America dominates the global data center ASIC market due to the presence of major cloud service providers and chip developers, with the U.S. leading investments in AI infrastructure and custom silicon. Europe holds a significant market share, fueled by strong regulatory emphasis on data sovereignty and a growing number of green data center initiatives in countries like Germany, Ireland, and the Nordic nations. However, Asia-Pacific is emerging as the fastest-growing region, led by hyperscale expansions in China, India, South Korea, and Japan. India, in particular, is rapidly expanding its data center footprint, backed by digital transformation and government incentives. Meanwhile, Southeast Asian countries are gaining traction as alternative AI infrastructure hubs due to their favorable energy profiles. Latin America and the Middle East & Africa are in the early stages of ASIC-driven modernization, but increasing investments in digital infrastructure and cloud adoption indicate growing potential in these emerging markets.

Market Insights:

- The Global Data Center ASIC Market reached USD 3,493.70 million in 2024 and is projected to grow to USD 5,460.53 million by 2032, expanding at a CAGR of 5.34%.

- Surging AI and machine learning workloads are prompting major hyperscalers to integrate ASICs for lower latency and optimized processing efficiency.

- Companies like Google and Amazon are accelerating investment in custom silicon, strengthening internal capabilities and reducing third-party chip dependency.

- Rising global data consumption through streaming, IoT, and enterprise apps is fueling demand for high-throughput, energy-efficient ASIC-based architectures.

- ASICs support sustainability goals by offering better power efficiency, aligning with growing pressure to reduce carbon emissions in data centers.

- High development costs, complex design cycles, and limited flexibility post-deployment continue to restrict adoption among smaller enterprises.

- North America leads the market with strong hyperscaler presence, while Asia-Pacific emerges as the fastest-growing region driven by rapid infrastructure expansion in China and India.

[cr_cta type=”download_free_sample“]

Market Drivers:

Rising AI and Machine Learning Workloads are Accelerating ASIC Adoption

Artificial Intelligence (AI) and machine learning applications are driving exponential increases in computing demand, pushing data centers to seek more specialized and efficient processing solutions. General-purpose CPUs and GPUs often fall short when handling large-scale, repetitive AI tasks. In response, hyperscalers and enterprises are integrating Application-Specific Integrated Circuits (ASICs) into their data centers to execute these workloads more efficiently. ASICs offer higher throughput and lower latency, delivering optimized performance tailored to specific AI algorithms. The Global Data Center ASIC Market benefits significantly from this shift, as AI continues to influence a broad range of industries including healthcare, finance, and manufacturing. Companies prioritizing AI capabilities view ASICs as a long-term investment to maintain computational competitiveness.

- For instance, Google’s latest Ironwood TPU (TPUv7), launched in 2025, exemplifies this trend: it delivers a 5x increase in compute performance, 6x higher high-bandwidth memory (HBM) capacity, and 2x the performance-per-wattcompared to its predecessor.

Hyperscaler Investment in Custom Silicon is Driving Market Growth

Large cloud service providers such as Amazon, Google, and Microsoft are designing proprietary ASICs to reduce reliance on third-party chip manufacturers and gain greater control over performance and cost structures. These hyperscalers are allocating substantial resources to build internal silicon capabilities, leveraging in-house expertise to develop chips optimized for their specific workloads. It helps them reduce power consumption, improve efficiency, and tailor features for services like cloud-based AI inference or storage optimization. The Global Data Center ASIC Market benefits from this trend, as demand for high-performance infrastructure grows. Proprietary ASIC development reinforces the importance of flexible and scalable chip architectures that align with evolving cloud computing needs. This strategy also supports infrastructure differentiation in a highly competitive cloud services market.

- For instance, Amazon’s Inferentia chips, purpose-built for AI inference, have enabled AWS customers to achieve up to 3x higher throughput and 70% lower cost-per-inferencecompared to previous GPU-based solutions, according to official AWS documentation.

Surging Data Volumes are Necessitating High-Efficiency Compute Solutions

The rapid expansion of connected devices, video streaming, and cloud-based enterprise applications is generating massive volumes of data that must be processed, stored, and analyzed in real time. Conventional processors often struggle to meet the low-latency and high-bandwidth requirements of modern workloads. It creates a need for more efficient computing architectures, where ASICs provide targeted performance without excessive energy consumption. The Global Data Center ASIC Market is responding to these evolving demands with solutions that enable faster data throughput and improved workload acceleration. Enterprises view ASICs as a way to maintain data agility and responsiveness across their infrastructure. Demand will continue to rise as industries increase reliance on data-driven decision-making.

Energy Efficiency and Sustainability Goals are Shaping Infrastructure Investment

Data center operators are under pressure to reduce energy consumption and carbon emissions while maintaining performance standards. ASICs, by design, consume less power than general-purpose alternatives, offering a clear advantage in sustainability-focused operations. It allows operators to meet both regulatory compliance requirements and internal carbon neutrality targets. The Global Data Center ASIC Market aligns well with these objectives by delivering performance-per-watt benefits at scale. Organizations are increasingly selecting ASICs for long-term cost efficiency and environmental impact reduction. The push for greener infrastructure reinforces the role of ASICs in shaping next-generation data centers.

Market Trends:

Emergence of Domain-Specific Architectures is Reshaping Design Priorities

The increasing need for task-specific computing has led to a shift toward domain-specific architectures in chip design. These architectures allow ASICs to focus on narrowly defined functions, which enhances speed and energy efficiency without requiring general-purpose flexibility. Companies are prioritizing customized ASICs for workloads like video encoding, blockchain validation, and database query acceleration. This trend is driving innovation in how chip designers approach layout and functionality. The Global Data Center ASIC Market reflects this evolution, where demand for precision and specialization is outpacing the appeal of universal processors. It encourages collaboration between hardware engineers and software developers to align functionality with exact application needs.

- For example, Google’s Tensor Processing Units (TPUs) have demonstrated up to 30x better energy efficiency and 50x faster performance in deep neural network operations versus traditional CPUs and GPUs.

Open-Source Hardware and Collaboration Frameworks Are Gaining Ground

The growth of open-source hardware initiatives is transforming the way ASICs are developed and deployed in data centers. Platforms like RISC-V have allowed organizations to customize and license processor architectures without the high costs and restrictions imposed by proprietary vendors. It fosters innovation by enabling faster prototyping and greater flexibility in chip design. In the Global Data Center ASIC Market, open hardware tools are making ASIC development more accessible to mid-sized companies and startups. The increased openness is accelerating design cycles while reducing long-term dependency on major chipmakers. This shift promotes a more diversified competitive landscape and encourages cost-efficient development strategies.

Integration of Advanced Packaging Techniques is Enhancing Chip Performance

Advanced packaging methods such as chiplet integration and 3D stacking are becoming integral to maximizing the performance and density of ASICs. These techniques allow multiple dies with specialized functions to be combined within a single package, minimizing latency and improving thermal efficiency. Designers are now pushing performance boundaries without increasing die size or power consumption. The Global Data Center ASIC Market is seeing increased investment in such packaging innovations to support high-bandwidth applications. It enables more modular and scalable chip solutions tailored to data center requirements. This approach supports higher interconnect speeds and more efficient use of silicon real estate.

- For example, TSMC’s CoWoS (Chip-on-Wafer-on-Substrate) and Intel’s Foveros 3D packaging technologies enable the integration of high-bandwidth memory (HBM) and logic dies within a single package. These advanced integration methods support extremely high aggregate memory bandwidth exceeding 2 TB/s in systems using multiple HBM3 stacks and feature interconnect pitches below 10 microns, enabling dense and efficient die-to-die communication.

Supply Chain Localization is Influencing ASIC Manufacturing Strategies

Geopolitical tensions and chip supply disruptions have prompted countries and corporations to rethink their semiconductor supply chains. Many data center operators are now investing in regional manufacturing capabilities to reduce exposure to global risks. It affects how ASICs are produced, sourced, and distributed within the ecosystem. In the Global Data Center ASIC Market, companies are exploring partnerships with local foundries and fabless models to ensure production continuity. This localization trend is altering the traditional reliance on a few global fabrication hubs. It also aligns with growing government incentives to boost domestic semiconductor capacity.

Market Challenges Analysis:

High Development Costs and Long Design Cycles are Limiting Wider Adoption

Designing and producing ASICs requires significant upfront investment, often exceeding that of general-purpose processors. Companies must allocate extensive resources toward R&D, fabrication tooling, and verification processes. This complexity makes ASICs less accessible to smaller firms that lack the financial strength or technical expertise to pursue custom silicon. The Global Data Center ASIC Market faces a bottleneck due to these high barriers to entry, which slows innovation across a broader segment of potential users. It also delays time-to-market, particularly when design iterations are necessary to align performance with emerging workload requirements. Without economies of scale, cost per chip remains high, limiting widespread deployment beyond large hyperscale environments.

Rapid Technological Shifts and Fabrication Constraints Challenge Scalability

The pace of technological change in data center operations demands continuous updates to chip design, yet ASICs offer limited post-deployment flexibility. Once fabricated, they cannot be reprogrammed like FPGAs or updated through software patches like general-purpose processors. This rigidity exposes data centers to potential obsolescence if workloads evolve faster than anticipated. The Global Data Center ASIC Market must also contend with fabrication bottlenecks, where access to advanced nodes is restricted due to limited foundry capacity or geopolitical factors. It creates uncertainty in supply chains and hampers timely scaling of infrastructure. Navigating these challenges requires careful long-term forecasting and strong coordination between design and manufacturing teams.

Market Opportunities:

Rising Demand for Edge Computing and Industry-Specific Data Centers is Creating New Growth Channels

Edge computing is driving the need for localized, low-latency processing across sectors such as manufacturing, healthcare, and retail. These environments benefit from ASICs that deliver high performance with minimal energy consumption in constrained spaces. The Global Data Center ASIC Market can capitalize on this shift by offering purpose-built solutions tailored for decentralized architectures. It supports a growing preference for domain-specific acceleration closer to the data source. Industry-specific data centers also require chips optimized for unique workloads, creating demand for customized ASICs beyond general cloud deployments. This diversification opens doors for new design collaborations and niche market penetration.

Government Incentives and Strategic Investments are Encouraging Localized ASIC Production

National initiatives promoting semiconductor self-reliance are creating favorable conditions for ASIC developers and manufacturers. Governments across the U.S., India, and Europe are funding infrastructure, research labs, and fabrication facilities. The Global Data Center ASIC Market stands to benefit from these efforts, gaining access to localized ecosystems that reduce dependence on offshore supply chains. It enables more resilient production strategies and supports long-term cost efficiency. Strategic investments in advanced packaging and chip design also enhance the market’s ability to meet evolving data center demands. Public-private partnerships are accelerating innovation cycles and expanding global deployment capacity.

Market Segmentation Analysis:

The Global Data Center ASIC Market is segmented by application, deployment mode, and end user, reflecting its diverse operational landscape.

By application segment, AI/ML accelerators dominate due to increasing demand for low-latency, high-performance computing in artificial intelligence workloads. Networking ASICs hold a strong share, driven by growing data traffic and the need for efficient packet processing. Storage controllers and security/encryption ASICs follow, supporting scalable storage systems and data protection protocols. Custom cloud and enterprise ASICs are gaining traction among organizations seeking tailored performance.

- For example, Cisco Silicon One Q200 is a legitimate and advanced ASIC designed for scalable packet processing in next-generation data center networks. It’s known for integrating advanced telemetry and security features. It’s a key component in Cisco’s Silicon One architecture, which aims to unify network silicon across various applications.

By deployment mode, the cloud-based segment leads the market due to widespread adoption of cloud-native infrastructure and increasing preference for scalable, on-demand compute environments. On-premises deployments remain relevant for enterprises requiring dedicated infrastructure for compliance, latency, or security-sensitive workloads.

By end users, hyperscale cloud providers account for the largest share, leveraging ASICs to optimize efficiency and performance at scale. It also sees significant adoption by enterprise data centers modernizing legacy systems, while colocation providers implement ASICs to enhance service offerings and energy efficiency.

- For example, Meta (Facebook) modernizes its data centers with custom ASICs to accelerate content delivery and AI inference, improving user experience and operational efficiency.

Segmentation:

By Application:

- AI/ML Accelerators

- Networking ASICs

- Storage Controllers

- Security/Encryption ASICs

- Custom Cloud/Enterprise ASICs

By Deployment Mode:

By End User:

- Hyperscale Cloud Providers

- Enterprise Data Centers

- Colocation Providers

By Region:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

The North America Data Center ASIC Market size was valued at USD 1,031.79 million in 2018 to USD 1,442.60 million in 2024 and is anticipated to reach USD 2,261.29 million by 2032, at a CAGR of 5.4% during the forecast period. North America holds the largest share of the Global Data Center ASIC Market, accounting for over 34% of global revenue in 2024. The presence of major cloud providers such as Amazon Web Services, Google Cloud, and Microsoft Azure continues to fuel demand for high-performance ASICs. It benefits from strong investment in AI, cloud computing, and edge infrastructure. Ongoing development of hyperscale data centers and proprietary silicon by leading tech firms supports market expansion. The region also leads in adoption of advanced packaging techniques and integration of AI accelerators. Government initiatives supporting domestic semiconductor production further strengthen its position in the global market.

The Europe Data Center ASIC Market size was valued at USD 467.45 million in 2018 to USD 625.01 million in 2024 and is anticipated to reach USD 889.50 million by 2032, at a CAGR of 4.1% during the forecast period. Europe represents 15% of the Global Data Center ASIC Market, driven by a rising focus on data sovereignty, sustainability, and digital infrastructure development. Countries like Germany, Ireland, and the Netherlands are expanding their data center footprints with emphasis on green energy and efficient hardware. It also benefits from public-private partnerships and funding for AI-driven infrastructure under the EU’s Digital Strategy. Growing demand for industry-specific cloud services supports localized ASIC integration. Despite lower hyperscaler presence compared to North America, the region maintains steady growth through regulatory support and innovation in telecom and industrial data solutions.

The Asia Pacific Data Center ASIC Market size was valued at USD 736.86 million in 2018 to USD 1,097.92 million in 2024 and is anticipated to reach USD 1,866.94 million by 2032, at a CAGR of 6.5% during the forecast period. Asia Pacific holds a 26% share of the Global Data Center ASIC Market and is the fastest-growing region. Rapid digital transformation in China, India, South Korea, and Southeast Asia is expanding demand for ASIC-based acceleration. Governments are investing heavily in domestic chip manufacturing and AI infrastructure. It sees increasing ASIC adoption across telecom, financial services, and public sector data centers. The presence of major foundries and semiconductor suppliers adds strategic depth to regional growth. Data localization laws and rising AI deployment reinforce the region’s role in shaping future demand.

The Latin America Data Center ASIC Market size was valued at USD 116.46 million in 2018 to USD 162.57 million in 2024 and is anticipated to reach USD 224.83 million by 2032, at a CAGR of 3.7% during the forecast period. Latin America accounts for 4% of the Global Data Center ASIC Market and is gradually evolving with improved connectivity and cloud adoption. Brazil and Mexico lead regional investments in data center infrastructure. It benefits from growing enterprise demand for low-latency processing and AI-enablement in sectors like banking and e-commerce. Market growth remains steady despite limited local chip production. Regional initiatives focused on digital transformation are increasing demand for energy-efficient ASICs. Partnerships with global tech providers are helping accelerate ASIC deployment across public and private clouds.

The Middle East Data Center ASIC Market size was valued at USD 69.50 million in 2018 to USD 89.84 million in 2024 and is anticipated to reach USD 118.57 million by 2032, at a CAGR of 3.1% during the forecast period. The Middle East holds 2% of the Global Data Center ASIC Market, supported by increasing investment in smart cities and digital infrastructure. The UAE and Saudi Arabia are leading regional growth with national AI strategies and hyperscale deployments. It is attracting global cloud service providers seeking regional data hubs. ASIC adoption is growing in areas such as public sector IT, healthcare, and finance. The market is limited by manufacturing dependencies but strengthened by strong government backing. Expanding regional demand for secure, energy-efficient compute is driving interest in custom silicon.

The Africa Data Center ASIC Market size was valued at USD 49.59 million in 2018 to USD 75.76 million in 2024 and is anticipated to reach USD 99.41 million by 2032, at a CAGR of 3.0% during the forecast period. Africa represents the smallest share just under 2% of the Global Data Center ASIC Market. It is in the early stages of ASIC adoption, with demand centered around telecom, education, and public sector applications. Countries like South Africa, Kenya, and Nigeria are developing regional cloud and data center ecosystems. It faces challenges due to limited infrastructure and supply chain constraints. Still, increasing mobile penetration and digital service delivery are creating future growth opportunities. International investment in local data centers is likely to support gradual ASIC integration across emerging workloads.

[cr_cta type=”customize_now“]

Key Player Analysis:

- Broadcom

- Marvell Technology

- NVIDIA Corporation

- Intel Corporation

- Advanced Micro Devices (AMD)

- Google (Alphabet Inc.) – TPU

- Amazon Web Services (AWS) – Graviton

- Synopsys Inc.

- Microchip Technology Inc.

- Lattice Semiconductor Corporation

Competitive Analysis:

The Global Data Center ASIC Market is highly competitive, driven by rapid innovation and increasing demand for custom silicon. Leading players such as NVIDIA, Intel, Alphabet Inc. (Google), Amazon Web Services, and Broadcom dominate with proprietary architectures tailored for AI, cloud, and high-performance computing workloads. It is witnessing growing participation from emerging fabless semiconductor companies that specialize in domain-specific ASICs. Strategic collaborations between cloud providers and chip manufacturers are strengthening supply chains and accelerating design cycles. Companies are investing in R&D to enhance energy efficiency, thermal performance, and workload optimization. The market is also seeing vertical integration, where hyperscalers develop in-house ASICs to reduce costs and differentiate services. Competitive advantage hinges on scalability, performance-to-power ratios, and the ability to support evolving data center architectures. It reflects a dynamic landscape where both established firms and startups compete to shape the future of infrastructure computing.

Recent Developments:

- In May 2025, NTT completed a $16.4 billion buyout of its IT services arm, NTT Data. This acquisition is part of NTT’s broader strategy to consolidate control, streamline decision-making, and accelerate global data center expansion, with nearly a gigawatt of new capacity planned across several strategic markets.

- In October 2024, AMD introduced the Alveo UL3422, an electronic trading accelerator specifically engineered for ultra-low latency applications in the financial sector. This new product utilizes the AMD Virtex UltraScale+ FPGA and allows trading firms to achieve sub-3 nanosecond latency for trade execution, providing a cost-effective solution for high-frequency trading environments.

- In September 2024, Intel launched its next-generation AI solutions, including the Xeon 6 processor and Gaudi 3 AI accelerators. The Xeon 6 processor doubles the performance for AI and high-performance computing workloads, while the Gaudi 3 accelerator enhances throughput by 20% and offers a superior price-to-performance ratio. These launches are designed to facilitate scalable AI infrastructure in data centers and cloud environments.

Market Concentration & Characteristics:

The Global Data Center ASIC Market is moderately concentrated, with a few dominant players controlling a significant portion of the market share. It features a mix of established semiconductor giants and hyperscale cloud providers that design proprietary ASICs to optimize infrastructure performance. Barriers to entry remain high due to substantial capital requirements, complex design processes, and limited access to advanced fabrication nodes. It is characterized by rapid technological evolution, short product lifecycles, and strong emphasis on energy efficiency and workload specialization. Customization, integration capability, and ecosystem support play a critical role in vendor differentiation. The market favors companies with deep R&D capabilities and strategic manufacturing partnerships. It continues to evolve with rising demand for AI acceleration, edge computing, and high-throughput data processing.

Report Coverage:

The research report offers an in-depth analysis based on application, deployment mode, and end user. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Demand for AI-optimized ASICs will grow rapidly, driven by expansion in machine learning and inference workloads.

- Hyperscalers will increase investment in proprietary silicon to reduce reliance on third-party chip vendors.

- Advanced packaging technologies such as chiplets and 3D integration will enhance ASIC performance and density.

- Edge data centers will adopt compact, energy-efficient ASICs for localized processing needs.

- Government incentives for semiconductor manufacturing will support regional ASIC production ecosystems.

- Emerging applications in blockchain, video processing, and cybersecurity will drive niche ASIC development.

- Open-source architectures like RISC-V will lower design barriers and expand innovation across smaller firms.

- Strategic partnerships between cloud providers and fabless designers will accelerate time-to-market for custom chips.

- Growing emphasis on energy efficiency will favor ASIC deployment in sustainability-focused data centers.

- Supply chain resilience and localization will become critical to meet rising global demand and reduce geopolitical risk.