Market Overview:

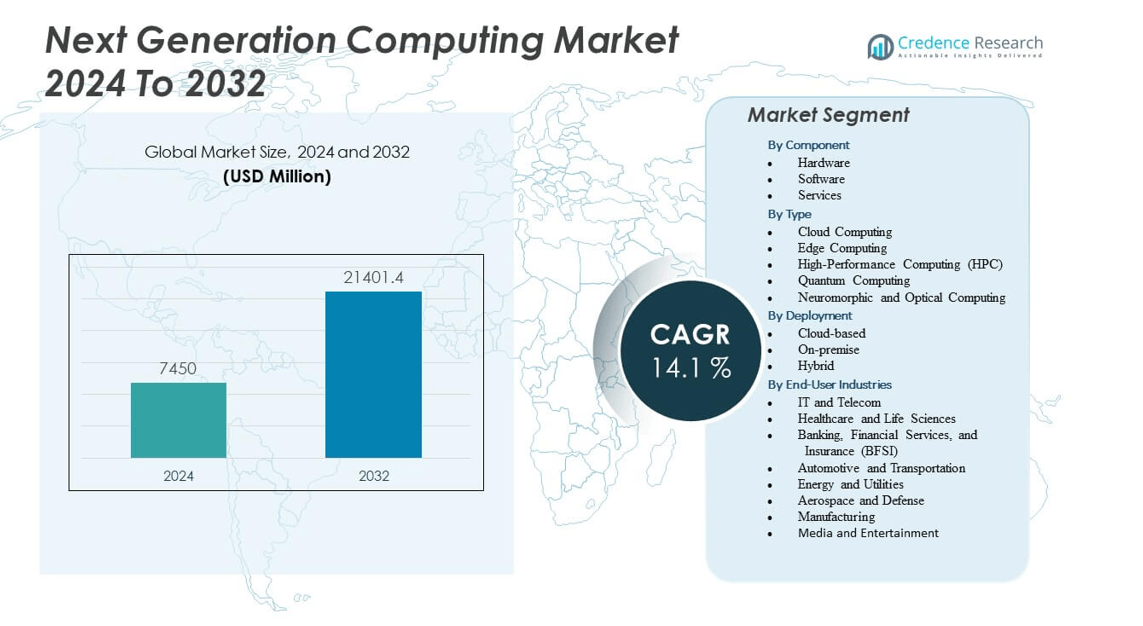

The Next Generation Computing Market is projected to grow from USD 7,450 million in 2024 to an estimated USD 21,401.4 million by 2032, with a compound annual growth rate (CAGR) of 14.1% from 2024 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Next Generation Computing Market Size 2024 |

USD 7,450 million |

| Next Generation Computing Market, CAGR |

14.1% |

| Next Generation Computing Market Size 2032 |

USD 21,401.4 million |

Growth in the Next Generation Computing Market is driven by rapid advancements in artificial intelligence, quantum computing, and cloud technologies. Enterprises are adopting these innovations to optimize workloads, enhance processing power, and enable real-time analytics. The increasing demand for secure, energy-efficient, and scalable computing solutions is fueling investment across industries. Additionally, rising applications in sectors such as healthcare, finance, and manufacturing are encouraging widespread deployment, while government support for digital transformation initiatives is further boosting momentum.

Regionally, North America leads the market due to strong adoption of advanced technologies and heavy investments by major tech players. Europe follows closely with growing emphasis on digital infrastructure and AI-driven applications. Asia-Pacific is emerging as a high-growth region, fueled by expanding IT infrastructure, government-backed innovation programs, and a rising startup ecosystem. Meanwhile, Latin America and the Middle East are gradually embracing next generation computing to support industrial modernization and digital transformation initiatives.

Market Insights:

- The Next Generation Computing Market is projected to grow from USD 7,450 million in 2024 to USD 21,401.4 million by 2032, at a CAGR of 14.1%.

- Growth is driven by demand for advanced computing power supporting AI, big data, and real-time analytics.

- Cloud-based and edge computing platforms are gaining traction, offering scalability and reduced latency for enterprises.

- High costs of development and integration challenges remain restraints slowing wider adoption across industries.

- North America leads with 38% market share, supported by strong R&D and technology infrastructure.

- Europe holds 27% share, emphasizing sustainability and advanced adoption in automotive, aerospace, and BFSI.

- Asia Pacific captures 25% share and is the fastest-growing, led by China, Japan, and India through government-backed innovation

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising demand for advanced computational power across diverse industries creating adoption momentum

The Next Generation Computing Market is gaining traction as industries seek faster and more efficient systems to handle complex workloads. It benefits from exponential growth in artificial intelligence, machine learning, and big data analytics that require powerful computational frameworks. Healthcare organizations adopt next generation systems for precision medicine and advanced diagnostics. Financial services leverage them for fraud detection, real-time trading, and risk modeling. Governments integrate high-performance computing to improve defense systems and smart city infrastructure. Cloud service providers are investing heavily in scalable solutions to meet enterprise needs. It is positioned as a critical enabler for digital transformation strategies across multiple sectors.

- For instance, NVIDIA launched its DGX H100 system in 2022, featuring eight H100 GPUs connected with NVLink, delivering up to 32 petaflops of AI performance at FP8 precision.

Expanding role of cloud-based solutions and edge infrastructure in supporting enterprise requirements

Growing adoption of hybrid cloud and edge computing environments supports the expansion of advanced computational platforms. Enterprises demand secure, flexible, and scalable models to manage evolving workloads across distributed ecosystems. It drives investments in high-performance hardware, energy-efficient processors, and advanced networking systems. Organizations pursue reduced latency and improved efficiency by deploying solutions closer to end-users. Telecom operators are integrating next generation computing with 5G networks to enhance connectivity and real-time processing. Enterprises are utilizing integrated platforms to improve supply chain visibility and resource optimization. Rising preference for cloud-native applications accelerates market growth. The Next Generation Computing Market strengthens its position within enterprise IT strategies.

Increasing focus on energy-efficient computing solutions to meet sustainability and performance goals

Sustainability initiatives are pushing industries to adopt greener computing technologies that minimize energy usage. The Next Generation Computing Market benefits from demand for low-power processors, liquid cooling systems, and optimized hardware. Enterprises emphasize reducing operational costs while achieving high computational performance. Data centers are deploying renewable energy sources to support efficiency in large-scale operations. Hardware innovators are developing advanced chips and memory architectures with reduced power consumption. Environmental regulations encourage businesses to embrace sustainable computing models. It creates opportunities for innovation in both hardware and software layers. The growing intersection of sustainability and technology positions next generation systems as key enablers of eco-friendly transformation.

- For instance, Google’s Hamina data center in Finland uses seawater from the Gulf of Finland to cool its servers. It operates with 97% carbon-free energy and channels recovered heat to fulfill 80% of local district heating needs

Growing integration of quantum computing and AI creating transformative business applications

Enterprises explore quantum computing capabilities for problem-solving across healthcare, logistics, and material science. AI-driven platforms require advanced computational frameworks to support predictive analytics and automation. The Next Generation Computing Market supports collaboration between quantum startups, cloud providers, and enterprises. Governments are funding research programs to accelerate breakthroughs in next generation systems. It provides solutions to tackle optimization problems, drug discovery, and cybersecurity challenges. Partnerships between universities and technology firms are enhancing commercialization efforts. High-profile investments from leading companies are reinforcing innovation pipelines. This integration of AI and quantum capabilities is establishing long-term value across industries.

Market Trends

Growing integration of neuromorphic computing and brain-inspired architectures into enterprise research

The Next Generation Computing Market is witnessing momentum in neuromorphic systems that replicate human brain structures. Neuromorphic chips enable real-time decision-making for robotics, autonomous vehicles, and advanced defense applications. Enterprises value these chips for their efficiency in pattern recognition and low-power design. It provides breakthroughs in sensor fusion, speech processing, and adaptive learning models. Governments and universities are increasing funding for brain-inspired research. Large technology companies are exploring neuromorphic integration into consumer electronics. Research collaborations across multiple countries support the commercialization of advanced neuromorphic platforms. These trends highlight long-term opportunities in industries that require cognitive computing capabilities.

- For example, Intel’s Loihi 2 neuromorphic research chip supports up to 1 million neurons and delivers processing speeds up to 10 times faster than its predecessor, enabling advancements in robotics and real-time decision systems.

Rising adoption of blockchain-enabled computing models for secure digital infrastructure development

Blockchain integration is emerging as a significant trend in enterprise computing. The Next Generation Computing Market benefits from secure frameworks supporting data integrity, decentralized processing, and transparent workflows. Blockchain-based systems improve cybersecurity by reducing the risk of tampering or unauthorized access. Enterprises integrate blockchain with cloud and AI solutions for improved traceability. Governments are using blockchain computing frameworks to support secure identity verification and supply chain visibility. Financial services are leveraging distributed ledgers for cross-border transactions. It establishes a foundation for scalable and secure computing models. This convergence is shaping next generation architectures for long-term enterprise growth.

Expanding applications of high-performance computing in research, climate modeling, and drug discovery

High-performance computing is advancing scientific breakthroughs across multiple industries. The Next Generation Computing Market benefits from growing demand for simulations in weather forecasting, genetics, and pharmaceutical research. Researchers leverage supercomputers to process enormous datasets and deliver accurate insights. It supports modeling of pandemics, environmental changes, and molecular interactions. Universities and laboratories are partnering with industry players to access advanced computational power. Governments fund supercomputing projects to enhance national research capabilities. Corporations invest in HPC platforms for predictive maintenance and product innovation. These initiatives create a strong ecosystem that drives innovation in critical fields of science and industry.

Development of hybrid computing models merging classical and quantum systems for practical use cases

Enterprises are pursuing hybrid systems that combine quantum capabilities with traditional computing power. The Next Generation Computing Market is experiencing growing investment in pilot projects that validate hybrid efficiency. Hybrid models solve optimization and cryptography challenges that classical systems cannot address alone. It provides industries with gradual integration pathways without full reliance on quantum-only solutions. Cloud providers are offering hybrid quantum platforms accessible to enterprises of all sizes. Governments invest in hybrid system testing to drive faster commercialization. Technology firms are filing patents to protect hybrid innovations. This hybridization trend is shaping the future of enterprise adoption.

- For example, Microsoft’s Azure Quantum platform handled NASA JPL’s Deep Space Network scheduling with a hybrid workflow that shrank compute times from over two hours to approximately two minutes using quantum-inspired optimization algorithms.

Market Challenges Analysis

High cost of development and complexity of integration limiting adoption of advanced systems

The Next Generation Computing Market faces barriers due to significant costs involved in developing high-performance systems. Enterprises struggle with balancing investment requirements against uncertain return timelines. It creates hesitation in large-scale deployment across industries with limited budgets. Complexity in integrating advanced architectures with legacy IT systems further adds challenges. Organizations must hire specialized talent to manage new technologies, increasing operational expenses. Governments and enterprises are collaborating to mitigate these obstacles, but financial risks remain significant. Technology adoption is often delayed because companies wait for proven performance before committing resources. Such constraints restrict widespread market penetration.

Concerns over security, data privacy, and regulatory frameworks slowing enterprise uptake

Data security concerns create hesitation among enterprises planning next generation computing adoption. The Next Generation Computing Market requires robust regulatory frameworks to guide implementation across sectors. It faces risks related to quantum cryptography and the protection of sensitive information. Enterprises must comply with global regulations that often vary across regions. This fragmentation creates additional costs and delays in deployment. Cybersecurity threats are increasing with the expansion of interconnected platforms. Governments attempt to balance innovation with secure regulatory oversight. These uncertainties hinder immediate enterprise trust and adoption of next generation systems.

Market Opportunities

Expanding commercial potential across healthcare, financial services, and industrial transformation sectors

The Next Generation Computing Market presents opportunities in healthcare through precision medicine and advanced diagnostic models. Financial institutions can utilize predictive computing for fraud prevention, algorithmic trading, and risk assessment. It enhances industrial operations by enabling predictive maintenance, robotics, and automation. Governments support investments that align with industrial modernization and national competitiveness. Cloud providers are opening platforms for startups to accelerate innovative applications. The versatility of next generation systems creates a foundation for multi-sector adoption. Growing collaborations between technology firms and research institutions are expanding commercialization pathways. These developments strengthen opportunities across global industries.

Rising government investments and global collaboration driving innovation and commercialization initiatives

Governments worldwide are prioritizing next generation computing through dedicated funding programs and public-private partnerships. The Next Generation Computing Market benefits from these initiatives as enterprises align with national strategies. It supports cross-border collaborations that accelerate breakthroughs in AI, quantum, and neuromorphic technologies. International research consortia are pooling resources to solve global challenges in energy, healthcare, and sustainability. Venture capital is increasingly directed toward startups advancing disruptive computing technologies. Standardization bodies are working on frameworks to support secure adoption. Collaborative innovation ensures rapid scaling and integration into commercial markets. These opportunities reflect long-term growth potential across regions.

Market Segmentation Analysis:

The Next Generation Computing Market is segmented

By Component into hardware, software, and services. Hardware dominates with demand for advanced processors, accelerators, and memory to support heavy workloads. Software platforms such as AI tools, simulation models, and analytics solutions are gaining traction with enterprises focusing on intelligence-driven decisions. Services including consulting, integration, and maintenance ensure smooth adoption and scalability for organizations investing in advanced computing infrastructure.

By Type, the market covers cloud computing, edge computing, high-performance computing (HPC), quantum computing, and neuromorphic and optical computing. Cloud and edge platforms lead adoption due to demand for scalable and low-latency solutions. HPC continues to serve research, engineering, and defense needs, while quantum and neuromorphic systems are emerging with disruptive potential for optimization, cybersecurity, and cognitive applications. It reflects a transition toward specialized and hybrid computing models across industries.

- For instance, AWS Lambda processes tens of trillions of invocations annually, highlighting its global scalability; Oak Ridge National Laboratory’s Frontier HPC system delivers 1.1 exaFLOPS of performance, making it the world’s fastest publicly ranked supercomputer.

By Deployment is categorized into cloud-based, on-premise, and hybrid models. Cloud-based systems drive growth with enterprises embracing flexible and cost-effective computing frameworks. On-premise deployment remains important in sectors requiring strict data control, while hybrid approaches are expanding to balance security with scalability.

- For example, Google Cloud served around 960,000 businesses in 2024, reflecting strong enterprise engagement. Dell Technologies continues to lead with its PowerEdge servers, though specific figures on on-premise deployments for government or financial services remain unconfirmed.

By End-user industries span IT and telecom, healthcare and life sciences, BFSI, automotive and transportation, energy and utilities, aerospace and defense, manufacturing, and media and entertainment. IT and telecom dominate adoption, driven by demand for network optimization and AI integration. Healthcare applies next generation systems in diagnostics and drug discovery, while BFSI leverages advanced computing for fraud detection and risk modeling. Manufacturing, defense, and energy sectors adopt these solutions to improve efficiency, security, and predictive capabilities.

Segmentation:

By Component

- Hardware

- Software

- Services

By Type

- Cloud Computing

- Edge Computing

- High-Performance Computing (HPC)

- Quantum Computing

- Neuromorphic and Optical Computing

By Deployment

- Cloud-based

- On-premise

- Hybrid

By End-User Industries

- IT and Telecom

- Healthcare and Life Sciences

- Banking, Financial Services, and Insurance (BFSI)

- Automotive and Transportation

- Energy and Utilities

- Aerospace and Defense

- Manufacturing

- Media and Entertainment

By Region

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis:

North America holds the largest share of the Next Generation Computing Market with 38%. Strong presence of technology giants, extensive R&D investment, and early adoption of quantum and HPC platforms drive regional growth. The United States leads with advanced infrastructure supporting AI, cloud, and hybrid computing initiatives. Canada contributes through government-backed innovation programs and collaborations between academia and enterprises. Enterprises across healthcare, BFSI, and defense sectors are prioritizing next generation solutions to enhance efficiency and security. It benefits from robust digital ecosystems, making North America the most mature market.

Europe accounts for 27% of the market, supported by high demand for secure and sustainable computing systems. The region emphasizes energy-efficient technologies in alignment with strict environmental policies. Germany, France, and the United Kingdom lead adoption in automotive, aerospace, and financial sectors. Research institutions and public-private partnerships are fueling advancements in HPC and neuromorphic computing. The European Union’s investments in data sovereignty and digital transformation enhance market strength. It reflects a balanced approach combining innovation, regulation, and cross-border collaboration.

Asia Pacific secures 25% of the market and represents the fastest-growing region. China, Japan, and India lead through large-scale investments in quantum, edge, and cloud computing platforms. Government programs in China and India are supporting innovation hubs and tech startups. Enterprises across telecom, healthcare, and manufacturing sectors are integrating advanced computing to meet rising digital demands. Growing 5G infrastructure further strengthens adoption across the region. It reflects an accelerating trajectory that positions Asia Pacific as a future leader. Latin America holds 6% and the Middle East and Africa account for 4%, with both regions expanding steadily through industrial modernization and digital infrastructure projects.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- IBM Corporation

- Amazon Web Services Inc.

- Alphabet Inc. (Google Cloud)

- Microsoft Corporation

- NVIDIA Corporation

- Intel Corporation

- Advanced Micro Devices Inc. (AMD)

- Cisco Systems Inc.

- Oracle Corporation

- Hewlett Packard Enterprise Development LP (HPE)

- Dell Technologies Inc.

- Atos SE

- Fujitsu Ltd.

- Baidu Inc.

- D-Wave

- Alibaba Group Holding Ltd.

- Samsung Electronics Co. Ltd.

- NEC Corporation

- Huawei Technologies Co. Ltd.

Competitive Analysis:

The Next Generation Computing Market is defined by strong competition among global technology leaders and emerging innovators. Companies such as IBM, Microsoft, Amazon Web Services, and Google Cloud dominate cloud and AI-driven platforms with extensive infrastructure and service portfolios. NVIDIA, Intel, and AMD lead in hardware innovation through advanced processors, GPUs, and accelerators that power high-performance and AI applications. Cisco, Dell, Oracle, and HPE strengthen enterprise adoption with integrated solutions combining hardware, software, and services. Quantum computing pioneers such as D-Wave and Rigetti are building specialized ecosystems, while Fujitsu, NEC, Huawei, and Samsung drive advancements in hybrid computing and regional leadership. Alibaba and Baidu are reinforcing Asia Pacific presence through investments in AI, edge, and quantum platforms. It reflects a competitive environment shaped by partnerships, R&D investments, and rapid product launches that expand the reach of next generation technologies across industries.

Recent Developments:

- In August 2025, IBM and AMD announced a strategic partnership to develop next-generation quantum-centric supercomputing architectures, aiming to blend IBM’s quantum expertise with AMD’s high-performance computing and AI acceleration capabilities. The hybrid architecture will leverage AMD’s CPUs, GPUs, and FPGAs to advance fault-tolerant quantum computing, with an initial demonstration planned later this year.

- In May 2025, D-Wave launched its sixth-generation Advantage2 annealing quantum computer, significantly enhancing performance through higher qubit coherence and improved system integration. This new product targets enterprise workloads in logistics and advanced machine learning, marking a major leap in quantum computing capabilities.

- In May 2025, NVIDIA announced expanded partnerships with Acer, GIGABYTE, MSI, HP, ASUS, Dell, and Lenovo to build the new DGX Spark and DGX Station personal AI supercomputers, broadening availability worldwide. The DGX Spark, powered by the NVIDIA Grace Blackwell platform, is now available for reservation and will enable desktop AI research with data-center-class capabilities.

Report Coverage:

The research report offers an in-depth analysis based on Component, Type, Deployment and End-User Industries. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- The Next Generation Computing Market will expand with broader adoption of quantum systems for optimization, logistics, and material science.

- Enterprises will integrate AI-driven platforms with advanced computing to improve automation, predictive analytics, and decision-making.

- Hybrid models combining quantum, classical, and cloud computing will evolve to meet industry-specific requirements.

- Growing deployment of edge computing will support real-time processing for connected devices and smart infrastructure.

- Neuromorphic and optical computing architectures will progress from research to commercial applications across robotics and defense.

- Demand for secure computing frameworks will rise, driving investment in post-quantum cryptography and blockchain integration.

- Sustainability initiatives will encourage energy-efficient hardware designs and eco-friendly data center operations.

- Healthcare and life sciences will increasingly rely on high-performance computing for drug discovery and precision medicine.

- Government-backed research programs and public-private partnerships will accelerate commercialization of disruptive computing models.

- Competition among global and regional players will intensify, fostering strategic alliances and continuous innovation.