Market Overview

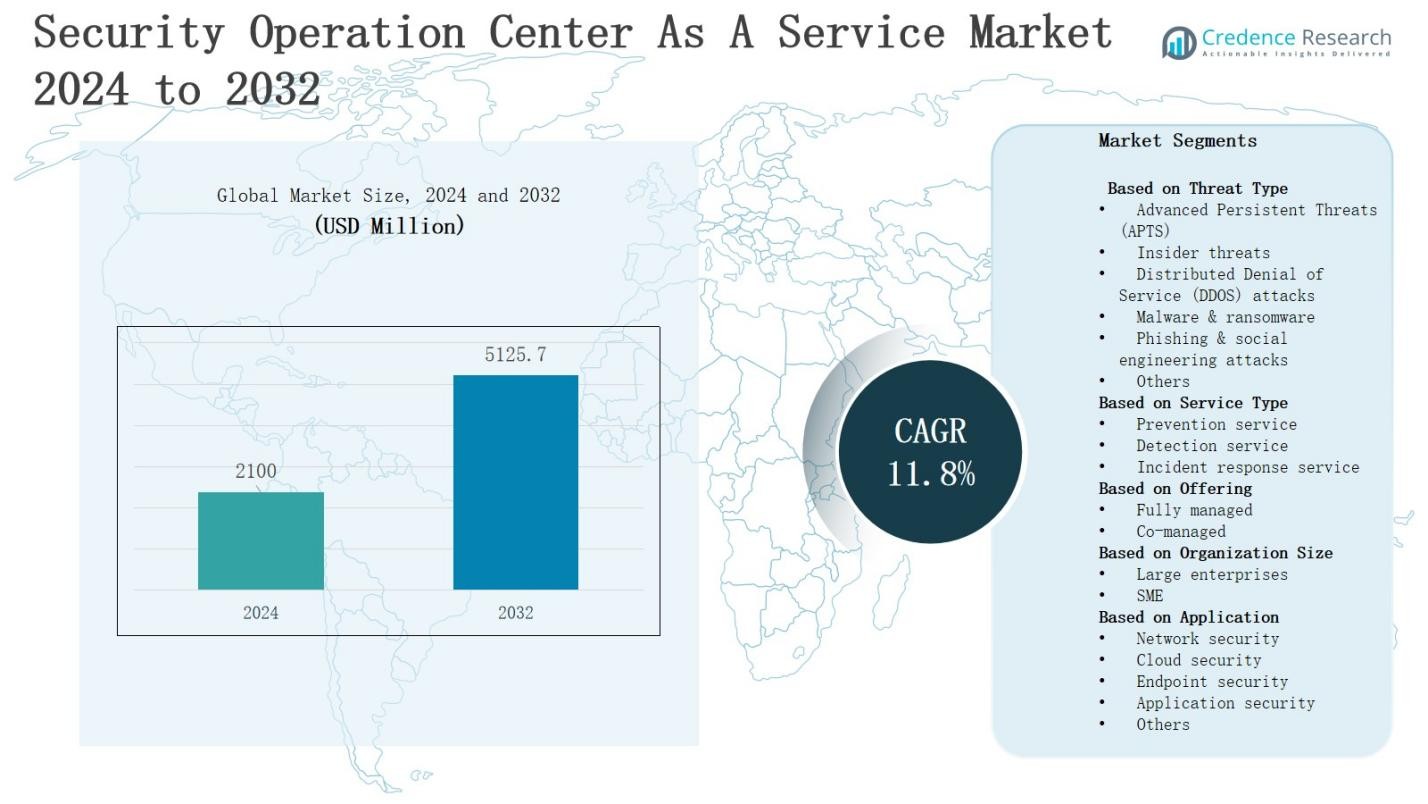

The security operation center as a service market is projected to grow from USD 2100 million in 2024 to USD 5125.7 million by 2032, registering a CAGR of 11.8% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Security Operation Center as a Service Market Size 2024 |

USD 2100 Million |

| Security Operation Center as a Service Market, CAGR |

11.8% |

| Security Operation Center as a Service Market Size 2032 |

USD 5125.7 Million |

The security operation center as a service market is driven by rising cyber threats, increasing regulatory compliance requirements, and the growing need for real-time monitoring across industries. Organizations adopt SOCaaS solutions to reduce costs, enhance scalability, and access advanced threat intelligence without heavy infrastructure investments. Trends highlight the integration of artificial intelligence and automation for faster incident detection, the adoption of cloud-based security operations, and the rise of managed detection and response services. Expanding demand from SMEs and the shift toward remote and hybrid work environments further accelerate market growth and innovation in SOCaaS offerings.

The security operation center as a service market shows diverse geographical dynamics, with North America leading at 38% share, followed by Europe at 27% and Asia-Pacific at 22%. Latin America holds 7% share, while the Middle East & Africa account for 6%. Growth is fueled by rising cyber threats, regulatory compliance, and digital transformation across industries. Key players include AT&T Inc., Atos SE, Capgemini SE, Cloudflare, ESDS Software Solution Pvt. Ltd., Fortinet Inc., Fujitsu Ltd., Lumen Technologies Inc., NTT Security Ltd., and Verizon Communications Inc.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The security operation center as a service market will expand from USD 2100 million in 2024 to USD 5125.7 million by 2032, achieving a CAGR of 11.8%.

- Malware and ransomware dominate threat type with 32% share, followed by phishing and social engineering at 25%, while detection services lead with 45% share across service type.

- Fully managed offerings capture 60% share, reflecting enterprise preference for outsourced expertise, while co-managed models hold 40%, appealing to organizations balancing external support with in-house operational control.

- North America leads with 38% share, Europe follows at 27%, Asia-Pacific holds 22%, Latin America represents 7%, and the Middle East & Africa account for 6%.

- Key players driving competition include AT&T Inc., Atos SE, Capgemini SE, Cloudflare, ESDS Software Solution Pvt. Ltd., Fortinet Inc., Fujitsu Ltd., Lumen Technologies Inc., NTT Security Ltd., and Verizon Communications Inc.

Market Drivers

Rising Cybersecurity Threats and Growing Complexity

The security operation center as a service market is primarily driven by the increasing volume and sophistication of cyber threats targeting organizations worldwide. Enterprises face evolving risks such as ransomware, phishing, and insider threats that demand advanced security solutions. SOCaaS enables real-time monitoring and incident response, providing continuous protection against complex attacks. It ensures businesses safeguard sensitive data, maintain customer trust, and comply with strict security standards while reducing vulnerabilities across networks.

- For instance, Microsoft’s Security Intelligence revealed it blocked over 65 billion phishing and other malicious emails in 2023, demonstrating the scale of threats SOCaaS platforms must address.

Regulatory Compliance and Data Protection Mandates

Governments and industry regulators enforce stringent data protection rules that compel companies to adopt advanced security measures. The security operation center as a service market addresses this demand by offering scalable solutions aligned with global compliance frameworks. It assists enterprises in meeting requirements under GDPR, HIPAA, and PCI DSS, reducing risks of penalties or legal consequences. Organizations rely on SOCaaS providers for expertise and consistent adherence to changing security regulations across multiple jurisdictions.

- For instance, Palo Alto Networks’ Unit 42 MDR (Managed Detection and Response) has been deployed to healthcare providers in the U.S. to ensure HIPAA compliance while maintaining continuous threat monitoring.

Cost Efficiency and Resource Optimization

Enterprises seek ways to strengthen security operations while controlling capital expenditure and resource constraints. The security operation center as a service market provides a cost-efficient model that reduces the need for in-house infrastructure and staffing. It allows organizations to access advanced tools, skilled analysts, and threat intelligence through subscription-based models. This approach helps optimize budgets, improve operational resilience, and ensure proactive defense without overburdening internal IT teams managing multiple priorities.

Adoption of Cloud Services and Remote Work Models

The global shift toward cloud computing and hybrid work models increases demand for flexible, scalable security solutions. The security operation center as a service market supports this transition by offering centralized monitoring across distributed environments. It ensures consistent protection for endpoints, applications, and data hosted on cloud platforms. Organizations benefit from continuous oversight, advanced detection, and adaptive security measures, enabling safe digital transformation while addressing risks tied to remote and multi-cloud operations.

Market Trends

Integration of Artificial Intelligence and Automation

The security operation center as a service market is witnessing a strong trend toward incorporating artificial intelligence and automation into threat detection and response. AI-driven analytics enhance the accuracy of incident detection while reducing false positives. Automation accelerates repetitive tasks such as log analysis and vulnerability scanning, allowing security analysts to focus on complex threats. It improves operational efficiency, lowers incident response times, and strengthens organizational resilience against sophisticated cyberattacks in diverse industries.

- For instance, Fortinet uses AI to accelerate threat prevention and detection, automating repetitive tasks such as log analysis to improve response times.

Growing Demand for Cloud-Native Security Operations

The expansion of cloud computing and hybrid infrastructures is driving a shift toward cloud-native SOCaaS platforms. The security operation center as a service market is adapting to deliver scalable, centralized monitoring across multi-cloud environments. Enterprises are prioritizing flexible solutions that provide visibility into distributed workloads while ensuring compliance. It supports businesses in securing applications, data, and users with dynamic capabilities that align with digital transformation strategies, cloud adoption, and evolving security challenges.

- For instance, Microsoft Defender for Cloud integrates with Microsoft Sentinel to provide AI-driven threat detection and centralized monitoring across Azure, AWS, and Google Cloud workloads.

Rise of Managed Detection and Response (MDR) Services

Organizations increasingly demand advanced detection capabilities and rapid remediation support, fueling the rise of MDR within SOCaaS models. The security operation center as a service market leverages MDR to deliver continuous monitoring, proactive threat hunting, and guided response actions. This trend supports businesses lacking in-house expertise by offering 24/7 analyst support. It enables enterprises to minimize risks, contain attacks faster, and gain confidence in their ability to manage complex security incidents effectively.

Expansion into Small and Medium Enterprises (SMEs)

While large enterprises dominate adoption, SMEs are becoming a key growth segment for SOCaaS providers. The security operation center as a service market now targets this sector with cost-effective, subscription-based models. SMEs adopt these solutions to access enterprise-grade security capabilities without heavy infrastructure investments. It helps smaller businesses address cybersecurity skill gaps, meet compliance standards, and protect against rising digital threats while maintaining affordability and scalability in highly competitive business environments.

Market Challenges Analysis

Concerns Over Data Privacy and Trust in Outsourced Models

The security operation center as a service market faces challenges related to data privacy, control, and trust in outsourcing critical security operations. Enterprises hesitate to share sensitive information with third-party providers due to fears of breaches, unauthorized access, or misuse. Strict regulations around cross-border data transfers further complicate adoption, especially for industries handling financial, defense, or healthcare information. It must address transparency and trust-building by ensuring clear policies, advanced encryption, and compliance assurances to overcome enterprise reluctance.

Shortage of Skilled Professionals and Rising Service Costs

Another key challenge arises from the global shortage of skilled cybersecurity professionals required to manage complex SOCaaS environments. The security operation center as a service market often struggles with rising costs linked to high demand for talent and advanced technologies. Smaller businesses may find subscription costs difficult to sustain, limiting adoption. It requires continuous investment in automation, AI-driven tools, and workforce training to maintain efficiency and affordability while balancing growing client expectations and diverse security needs.

Market Opportunities

Adoption of Advanced Technologies and AI-Driven Security Models

The security operation center as a service market holds strong opportunities through the integration of artificial intelligence, machine learning, and predictive analytics. Enterprises seek solutions that can detect and mitigate threats faster while reducing human error. It offers providers the chance to deliver intelligent, adaptive platforms that evolve with emerging risks. AI-driven SOCaaS models can streamline workflows, improve incident response, and provide actionable insights, making them attractive for organizations pursuing digital resilience and operational efficiency.

Expanding Demand Across Emerging Economies and SME Sector

Growing digital transformation in Asia-Pacific, Latin America, and the Middle East opens new opportunities for SOCaaS adoption. The security operation center as a service market is well-positioned to address the needs of SMEs in these regions with cost-effective subscription models. It provides scalable solutions to businesses with limited resources while ensuring compliance with evolving regulations. Providers can expand market presence by tailoring services to regional requirements, creating significant growth potential in underpenetrated markets worldwide.

Market Segmentation Analysis:

By Threat Type

In the security operation center as a service market, malware and ransomware represent the dominant threat type, accounting for around 32% share in 2024. This segment leads due to the rising frequency of targeted attacks disrupting business continuity and causing financial losses. Phishing and social engineering attacks follow with nearly 25% share, driven by human-factor vulnerabilities. Advanced persistent threats hold about 18% share, while insider threats capture 12%, DDoS attacks 9%, and others 4%, highlighting diverse risk exposure across industries.

By Service Type

Detection services dominate the service type segment in the security operation center as a service market, holding approximately 45% share in 2024. Enterprises prioritize continuous monitoring and early threat identification to minimize downtime and reduce risks. Prevention services account for 30% share, reflecting investments in proactive measures and compliance requirements. Incident response services represent about 25% share, fueled by demand for rapid remediation and expert support to contain breaches and mitigate operational impacts effectively.

- For instance, Microsoft’s Sentinel cloud-native SIEM integrates with more than 300 data connectors, enabling AI-driven detection across hybrid environments to enhance early threat visibility.

By Offering

Fully managed services lead the offering segment of the security operation center as a service market, capturing around 60% share in 2024. Organizations prefer fully outsourced solutions to overcome skills shortages, reduce infrastructure costs, and gain access to advanced expertise. Co-managed services hold the remaining 40% share, appealing to enterprises that seek collaboration with in-house teams while retaining some operational control. This model is gaining traction among large organizations balancing internal resources with external security expertise.

- For instance, AT&T Cybersecurity offers co-managed SOC options through its USM Anywhere platform, letting enterprises integrate existing security tools while leveraging AT&T’s 24/7 monitoring expertise.

Segments:

Based on Threat Type

- Advanced Persistent Threats (APTS)

- Insider threats

- Distributed Denial of Service (DDOS) attacks

- Malware & ransomware

- Phishing & social engineering attacks

- Others

Based on Service Type

- Prevention service

- Detection service

- Incident response service

Based on Offering

Based on Organization Size

Based on Application

- Network security

- Cloud security

- Endpoint security

- Application security

- Others

Based on Industry Vertical

- BFSI

- Healthcare

- Government

- Manufacturing

- Energy & utilities

- IT & telecom

- Transportation & logistics

- Others

Based on the Geography:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis

North America

North America leads the security operation center as a service market with a 38% share in 2024. Strong adoption of advanced cybersecurity solutions across banking, healthcare, and government sectors drives dominance. High digitalization and frequent cyberattacks push enterprises toward fully managed SOCaaS platforms. It benefits from the presence of global providers, advanced infrastructure, and strict compliance regulations. Cloud adoption and remote workforce expansion strengthen demand. Continuous innovation in AI-driven security further reinforces North America’s leading position.

Europe

Europe holds a 27% share of the security operation center as a service market in 2024. The region emphasizes compliance with GDPR and data protection standards, which drives investments in outsourced security operations. Enterprises rely on SOCaaS to handle increasing cyberattacks targeting financial services, automotive, and manufacturing sectors. It gains traction as businesses seek cost-effective models amid rising operational risks. Partnerships between European enterprises and global providers expand service adoption. The push for digital sovereignty enhances market growth.

Asia-Pacific

Asia-Pacific accounts for 22% share of the security operation center as a service market in 2024. Rapid digital transformation across China, India, and Southeast Asia creates strong demand for cloud-based security services. SMEs increasingly adopt SOCaaS to bridge cybersecurity skill gaps. It experiences significant growth fueled by rising ransomware cases, expanding e-commerce, and government-led digitalization programs. Telecom and IT sectors invest heavily in managed services. The region is projected to register the fastest expansion during the forecast period.

Latin America

Latin America captures a 7% share of the security operation center as a service market in 2024. The rise of digital banking, retail, and government modernization projects drives adoption. Enterprises look for scalable security solutions to address growing cybercrime in the region. It gains demand as cost-effective SOCaaS offerings appeal to mid-sized companies. Cloud infrastructure development and regional partnerships improve service availability. Local regulatory frameworks are evolving, creating opportunities for broader adoption.

Middle East & Africa

The Middle East & Africa holds a 6% share of the security operation center as a service market in 2024. Growing investments in smart cities, energy, and critical infrastructure projects fuel security needs. Governments and enterprises adopt SOCaaS to mitigate rising cyber threats targeting vital sectors. It benefits from regional partnerships and cloud expansion across Gulf nations. Limited cybersecurity talent accelerates demand for outsourced models. Increasing awareness and compliance requirements support steady growth across the region.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Fujitsu Ltd.

- Cloudflare

- Verizon Communications Inc.

- Lumen Technologies Inc.

- ESDS Software Solution Pvt. Ltd.

- Fortinet Inc.

- Capgemini SE

- Atos SE

- AT&T Inc.

- NTT Security Ltd.

Competitive Analysis

The security operation center as a service market is highly competitive, shaped by global technology leaders and specialized cybersecurity providers delivering advanced threat detection and response capabilities. It features strong participation from established companies such as AT&T Inc., Atos SE, Capgemini SE, Cloudflare, ESDS Software Solution Pvt. Ltd., Fortinet Inc., Fujitsu Ltd., Lumen Technologies Inc., NTT Security Ltd., and Verizon Communications Inc., each focusing on innovation, scalability, and compliance-driven solutions. Players differentiate by offering AI-driven monitoring, automation, and managed detection and response services that address diverse enterprise needs. Large firms leverage global infrastructure, partnerships, and broad client bases to dominate adoption, while regional vendors concentrate on affordability, customization, and niche expertise. Competition is further influenced by rising demand from small and medium enterprises, pushing providers to deliver cost-efficient subscription models. Continuous investment in cloud integration, incident response, and predictive analytics enhances market positioning. It remains dynamic, with mergers, acquisitions, and technology alliances shaping strategies to expand service portfolios, strengthen customer trust, and secure leadership in an evolving threat landscape.

Recent Developments

- In July 2025, Palo Alto Networks announced the $25 billion acquisition of CyberArk, strengthening its SOC capabilities with advanced identity and privileged access management.

- In April 2025, Westcon-Comstor, through its Comstor arm, introduced a managed SOC solution to expand security services for Cisco partners.

- In August 2024, Fortinet completed its acquisition of Lacework to enhance SOC-as-a-Service offerings with AI-driven cloud-native application protection.

- In April 2025, Logicalis became the first Cisco partner in APAC to launch Cisco’s MXDR as a global managed service, supported by its 24/7 APAC SOC.

Report Coverage

The research report offers an in-depth analysis based on Threat Type, Service Type, Offering, Organization Size, Application, Industry Vertical and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Enterprises will increasingly adopt SOCaaS to address evolving cyber threats and strengthen digital resilience.

- AI and machine learning will enhance detection accuracy and reduce false positives in security operations.

- SMEs will drive adoption by choosing affordable subscription-based SOCaaS models to manage cyber risks.

- Cloud-native SOCaaS platforms will expand as organizations shift workloads to multi-cloud and hybrid environments.

- Managed detection and response services will gain traction, offering faster incident handling and expert guidance.

- Regulatory compliance requirements will push enterprises to adopt SOCaaS for consistent global security monitoring.

- Partnerships between technology vendors and enterprises will accelerate SOCaaS innovation and broader market adoption.

- Automation will streamline routine tasks, allowing human analysts to focus on complex threat management.

- Remote work expansion will fuel demand for SOCaaS to secure distributed endpoints and applications.

- Regional growth will accelerate in Asia-Pacific, Latin America, and Middle East with rising digitalization.