Market Overview:

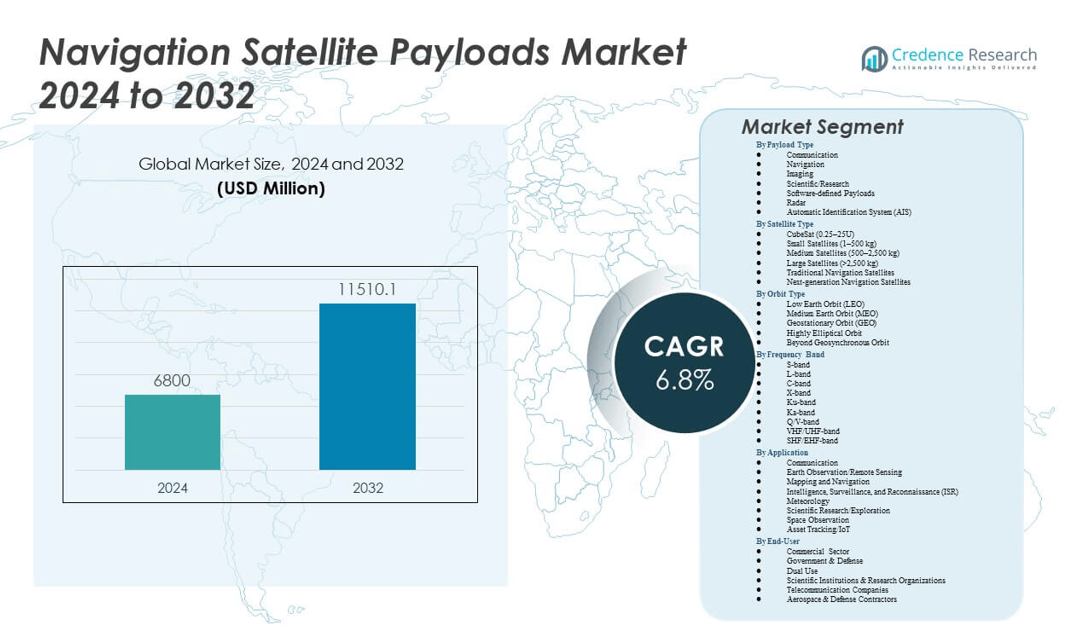

The Navigation Satellite Payloads Market is projected to grow from USD 6,800 million in 2024 to an estimated USD 11,510.1 million by 2032, with a compound annual growth rate (CAGR) of 6.8% from 2024 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Navigation Satellite Payloads Market Size 2024 |

USD 6,800 million |

| Navigation Satellite Payloads Market, CAGR |

6.8% |

| Navigation Satellite Payloads Market Size 2032 |

USD 11,510.1 million |

Market growth is primarily driven by the rising demand for accurate positioning, navigation, and timing solutions across defense, aviation, maritime, and commercial sectors. Increasing reliance on satellite navigation for autonomous vehicles, logistics optimization, and smart city infrastructure further strengthens adoption. Governments are investing heavily in next-generation navigation constellations to improve coverage and resilience. Technological advancements, including miniaturization of payloads and integration with artificial intelligence, are enhancing efficiency, reliability, and precision in satellite-based navigation systems, expanding their applicability across industries.

Regionally, North America leads the Navigation Satellite Payloads Market due to strong government space programs and defense investments. Europe follows with contributions from projects like Galileo, while Asia Pacific emerges as the fastest-growing region with significant developments in China and India’s satellite networks. These countries are focusing on strengthening independent navigation capabilities and reducing reliance on foreign systems. Meanwhile, the Middle East and Africa are adopting navigation technologies to support aviation, defense, and infrastructure development, showing steady progress in market penetration.

Market Insights

- The Navigation Satellite Payloads Market is projected to grow from USD 6,800 million in 2024 to USD 11,510.1 million by 2032, registering a CAGR of 6.8%.

- Rising dependence on precise positioning and timing solutions across defense, aviation, and logistics is driving strong adoption of satellite payloads.

- Technological advancements, including AI-enabled processing and miniaturized payload designs, are improving efficiency and expanding market applications.

- High development costs, complex engineering processes, and launch risks remain key restraints, limiting accessibility for smaller operators.

- North America holds the largest share due to government funding, defense priorities, and an active private space sector.

- Asia Pacific shows the fastest growth, supported by China and India’s expanding navigation constellations and regional independence goals.

- Europe maintains steady growth, strengthened by the Galileo program and collaborations among aerospace firms and government agencies.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising Global Dependence on Accurate Positioning and Timing Solutions

Growing reliance on positioning, navigation, and timing solutions drives steady demand for advanced satellite payloads. Industries such as defense, aviation, and maritime operations depend on real-time precision to maintain operational reliability. The Navigation Satellite Payloads Market benefits from this widespread adoption, particularly in critical applications like air traffic control and fleet monitoring. Demand increases further with autonomous systems requiring uninterrupted access to reliable navigation signals. It enhances efficiency in logistics, transportation, and infrastructure projects. Precision-based applications expand into financial transactions, disaster management, and emergency response operations. Governments and enterprises continue allocating budgets for resilient satellite networks to support global navigation needs.

- For instance, Lockheed Martin upgraded the GPS III satellite payloads, delivering 3× higher accuracy compared to legacy GPS satellites, significantly boosting real-time navigation for defense, aviation, and commercial platforms.

Expanding Military and Strategic Investments in National Navigation Capabilities

Governments invest heavily in independent satellite navigation constellations to reduce reliance on foreign systems. Military applications, including surveillance, intelligence gathering, and guided weaponry, prioritize accurate and secure signals. It strengthens national security strategies and creates sustained demand for advanced payload technologies. Defense budgets allocate significant funding toward modernization of space-based infrastructure. The Navigation Satellite Payloads Market benefits from countries deploying satellites capable of providing encrypted services to defense users. Secure payloads enable high-level communications while reducing vulnerabilities to jamming or spoofing. Growing geopolitical tensions and border security challenges accelerate the push for sovereign navigation programs. Military modernization further amplifies investment in satellite payload development worldwide.

- For instance, the European Space Agency’s Galileo constellation introduced the Public Regulated Service (PRS) payloads, offering encrypted navigation signals with a timing accuracy of under 30 nanoseconds, bolstering secure military-grade applications across member states.

Rapid Expansion of Commercial Applications Across Multiple Industries

Commercial sectors adopt satellite-based navigation for agriculture, logistics, mining, and resource exploration. Precision farming improves crop yields with satellite-guided machinery, creating steady market penetration. It enables transportation networks to optimize delivery routes, reduce fuel costs, and improve efficiency. The Navigation Satellite Payloads Market also benefits from adoption in ride-sharing and drone delivery systems. Mining companies use payloads for exploration, asset monitoring, and workforce safety in remote locations. Telecom providers integrate navigation services into smartphones and IoT devices, supporting billions of users globally. Commercial investment continues rising with demand for more accurate, faster, and resilient navigation services. This trend reinforces consistent demand from private operators seeking efficient payload solutions.

Continuous Technological Advancements in Payload Miniaturization and AI Integration

Innovations in payload miniaturization reduce weight, cost, and power requirements for satellite deployment. Smaller payloads enable low-cost launches through ridesharing programs and commercial launch providers. The Navigation Satellite Payloads Market benefits from AI integration, enhancing signal processing and resilience. It supports improved navigation accuracy in urban environments with dense obstacles and interference. Advanced payloads integrate machine learning to optimize resource allocation during satellite operations. This progress ensures satellites remain functional despite increased risks from space congestion. Developers explore hybrid payloads capable of serving multiple frequency bands, improving flexibility. Continuous R&D creates opportunities for scalable, efficient, and technologically advanced payload systems for global navigation.

Market Trends

Growing Adoption of Multi-Frequency Payload Systems for Enhanced Precision

The industry shifts toward multi-frequency payloads capable of transmitting signals across multiple bands. It provides redundancy against interference and improves accuracy for end users. The Navigation Satellite Payloads Market experiences higher adoption of systems supporting civil and defense requirements together. These payloads enable seamless service continuity in challenging urban or maritime environments. Demand rises for robust payload systems that ensure improved performance in adverse weather conditions. Manufacturers focus on developing payloads offering compatibility across regional constellations. Integration across multi-constellation systems enhances global coverage and reliability. This trend ensures broader market penetration and stronger user trust in satellite navigation services.

Rising Role of Private Companies in Satellite Payload Development and Launch

Private enterprises gain prominence by supporting governments and commercial customers with innovative payload solutions. It accelerates cost efficiency, shortens development cycles, and broadens access to satellite navigation. The Navigation Satellite Payloads Market now sees collaborations between established aerospace firms and agile startups. Commercial launch providers reduce costs, encouraging smaller nations and enterprises to deploy satellites. Partnerships between technology firms and satellite developers foster rapid prototyping and faster time-to-market. This trend shifts the landscape from government dominance to a balanced ecosystem with private participation. Competitive dynamics lead to innovation in payload design, capacity, and operational resilience. Private involvement reshapes the long-term trajectory of satellite navigation payload markets globally.

- For instance, in early 2024, SpaceX’s Falcon 9 successfully launched batches of 22 Starlink v2 Mini satellites into low Earth orbit such as on the Group 7-10 and Group 7-11 missions meeting planned deployment numbers precisely.

Integration of Navigation Payloads with Advanced Communication Networks

Growing need for seamless connectivity drives integration of navigation payloads with 5G and IoT networks. It enables advanced applications such as smart transportation, connected vehicles, and precision robotics. The Navigation Satellite Payloads Market aligns with next-generation communication systems to ensure interoperability. Integration with terrestrial networks allows enhanced positioning in dense urban areas. Payloads capable of supporting both navigation and communication services are in demand. This dual-use functionality maximizes efficiency and strengthens return on investment for operators. It also reduces dependence on ground-based infrastructure by offering combined services from orbit. Convergence of communication and navigation technologies establishes a transformative trend across global industries.

- For instance, Thales Alenia Space, alongside Ericsson and Qualcomm, successfully tested satellite–terrestrial 5G interoperability under 3GPP NTN standards, proving that standard 5G devices can maintain seamless connectivity over simulated low-Earth orbit satellite links in Europe.

Rising Demand for Resilient Navigation Systems Against Threats and Interference

Growing cyber threats and electronic warfare risks create demand for more secure satellite payloads. It drives innovation in anti-jamming, anti-spoofing, and signal encryption capabilities. The Navigation Satellite Payloads Market adapts with advanced payloads that offer stronger signal protection. Governments prioritize development of sovereign payload technologies to protect critical infrastructure. Commercial operators adopt resilient payload systems to ensure service continuity during disruptions. Manufacturers enhance payload software to quickly identify and neutralize interference sources. Emerging nations also emphasize secure payload capabilities to safeguard essential industries. This trend positions security and resilience as key differentiators in satellite payload adoption worldwide.

Market Challenges Analysis

High Costs, Technical Complexities, and Lengthy Development Cycles

High costs of satellite design, testing, and deployment limit entry for smaller players. Complex engineering requirements demand specialized expertise, extending development timelines significantly. It creates financial strain on operators seeking rapid deployment of navigation solutions. The Navigation Satellite Payloads Market also faces risks of failure during launch or early operations. Technical errors can lead to heavy financial losses and program delays. Limited access to launch windows further prolongs deployment schedules. Integration with existing constellations requires strict compliance with standards. These challenges collectively restrain growth by creating barriers for new entrants and smaller economies.

Space Debris, Spectrum Management, and Global Coordination Issues

Rising space debris increases collision risks, forcing operators to design durable payload systems. It requires investment in protective measures, adding to overall costs. The Navigation Satellite Payloads Market also contends with spectrum allocation conflicts across regions. Frequency overlaps lead to signal interference and reduced service reliability. Global coordination becomes critical to ensure interoperability between constellations. Regulatory delays slow down deployment schedules, particularly for emerging nations. Security concerns limit international technology sharing, creating uneven access to advanced payloads. These issues highlight the need for collaborative frameworks and stricter standards to maintain market growth.

Market Opportunities

Expanding Role of Navigation Payloads in Smart Infrastructure and Mobility

Smart cities and connected transportation systems increasingly rely on accurate satellite navigation. It strengthens opportunities for payload providers to support urban mobility and logistics optimization. The Navigation Satellite Payloads Market benefits from growing demand in autonomous vehicles and drone delivery. Emerging applications include precision farming, disaster relief, and energy grid monitoring. Integration with IoT devices further broadens applicability across industries. Governments promote investments to align navigation services with national infrastructure projects. Growing reliance on satellite-based mobility solutions enhances the potential for long-term market growth. Operators leveraging payload innovation will capture significant opportunities from these expanding applications.

Growth in Emerging Economies and Private Sector Participation

Emerging economies prioritize independent navigation capabilities to reduce dependence on foreign networks. It opens new markets for payload providers offering cost-effective solutions. The Navigation Satellite Payloads Market gains momentum with private firms entering satellite design and launch. Local partnerships accelerate adoption by aligning services with regional needs. Increasing investment in low-cost launch services supports broader participation. Demand rises for compact payloads suitable for small satellite constellations. This trend promotes scalability and makes navigation solutions accessible for smaller nations. Expanding presence of private players combined with government support presents lucrative opportunities for global market expansion.

Market Segmentation Analysis:

By Payload Type

The Navigation Satellite Payloads Market is segmented by payload type into communication, navigation, imaging, scientific/research, software-defined payloads, radar, and Automatic Identification System (AIS). Communication payloads remain essential for global data transfer and connectivity, while navigation payloads drive accuracy for defense, transport, and commercial applications. Imaging payloads support mapping and Earth observation, serving governments and enterprises. Scientific and research payloads strengthen space exploration missions and climate monitoring. Software-defined payloads are gaining importance for flexible, reconfigurable operations. Radar systems provide high-resolution detection in varied conditions, while AIS payloads enhance maritime safety and logistics efficiency.

By Satellite Type

The Navigation Satellite Payloads Market by satellite type includes CubeSats, small satellites, medium satellites, large satellites, traditional navigation satellites, and next-generation navigation satellites. CubeSats and small satellites are driving low-cost launches and commercial adoption due to miniaturization. Medium satellites maintain relevance for balanced cost and capacity requirements. Large satellites dominate defense and global navigation systems, offering advanced payload capacity. Traditional navigation satellites remain foundational for national programs. Next-generation navigation satellites focus on higher accuracy, resilience, and interoperability with new technologies.

- For instance, Planet Labs operates the world’s largest commercial Earth-imaging satellite constellation comprising over 430 PlanetScope Doves which deliver near-daily imagery of Earth’s landmasses for mapping, environmental monitoring, and commercial applications.

By Orbit Type

The Navigation Satellite Payloads Market by orbit type includes Low Earth Orbit (LEO), Medium Earth Orbit (MEO), Geostationary Orbit (GEO), Highly Elliptical Orbit, and Beyond Geosynchronous Orbit. LEO provides fast deployment and cost efficiency, ideal for small satellites and commercial constellations. MEO remains central to global navigation systems, offering wide coverage and balanced signal performance. GEO supports continuous communication services and weather monitoring with stable positioning. Highly Elliptical Orbit supports coverage in polar regions and specialized missions. Beyond Geosynchronous Orbit, though less common, enables research and exploration missions requiring extended range and visibility.

By Frequency Band

The Navigation Satellite Payloads Market by frequency band includes S-band, L-band, C-band, X-band, Ku-band, Ka-band, Q/V-band, VHF/UHF-band, and SHF/EHF-band. L-band and S-band are widely adopted for navigation due to signal robustness and penetration. C-band and X-band serve defense and secure communications with resilience against interference. Ku-band and Ka-band enable high-capacity communication, supporting broadband and commercial services. Q/V-band offers emerging opportunities for high-data-rate applications. VHF/UHF-band supports tracking and monitoring functions. SHF/EHF-band provides secure military-grade communications, enhancing strategic defense capabilities.

- For instance, SES deployed its O3b mPOWER satellites in Medium Earth Orbit, operating on the Ka-band with software-defined payloads that can generate thousands of steerable beams, each scalable from tens of Mbps up to multi-Gbps, delivering flexible high-throughput connectivity for broadband and government services.

By Application

The Navigation Satellite Payloads Market by application covers communication, Earth observation/remote sensing, mapping and navigation, intelligence, surveillance and reconnaissance (ISR), meteorology, scientific research/exploration, space observation, and asset tracking/IoT. Communication remains vital for global connectivity and mobile platforms. Earth observation and remote sensing support agriculture, environment monitoring, and disaster management. Mapping and navigation underpin transport, logistics, and autonomous systems. ISR strengthens defense and homeland security capabilities. Meteorology payloads provide accurate weather forecasting and climate analysis. Scientific research missions explore planetary and space phenomena. Space observation expands knowledge of celestial bodies, while asset tracking and IoT enhance logistics visibility and industrial automation.

By End-User

The Navigation Satellite Payloads Market by end-user includes commercial sector, government and defense, dual use, scientific institutions and research organizations, telecommunication companies, and aerospace and defense contractors. Government and defense users dominate with investments in secure, sovereign navigation systems. Commercial sector adoption grows through logistics, mobility services, and telecom integration. Dual-use satellites serve both defense and civil purposes, optimizing cost and capability. Scientific institutions rely on payloads for research and space exploration projects. Telecommunication companies use payloads to expand broadband and mobile services. Aerospace and defense contractors play a key role in development, integration, and system deployment, ensuring continued market expansion.

Segmentation:

By Payload Type

- Communication

- Navigation

- Imaging

- Scientific/Research

- Software-defined Payloads

- Radar

- Automatic Identification System (AIS)

By Satellite Type

- CubeSat (0.25–25U)

- Small Satellites (1–500 kg)

- Medium Satellites (500–2,500 kg)

- Large Satellites (>2,500 kg)

- Traditional Navigation Satellites

- Next-generation Navigation Satellites

By Orbit Type

- Low Earth Orbit (LEO)

- Medium Earth Orbit (MEO)

- Geostationary Orbit (GEO)

- Highly Elliptical Orbit

- Beyond Geosynchronous Orbit

By Frequency Band

- S-band

- L-band

- C-band

- X-band

- Ku-band

- Ka-band

- Q/V-band

- VHF/UHF-band

- SHF/EHF-band

By Application

- Communication

- Earth Observation/Remote Sensing

- Mapping and Navigation

- Intelligence, Surveillance, and Reconnaissance (ISR)

- Meteorology

- Scientific Research/Exploration

- Space Observation

- Asset Tracking/IoT

By End-User

- Commercial Sector

- Government & Defense

- Dual Use

- Scientific Institutions & Research Organizations

- Telecommunication Companies

- Aerospace & Defense Contractors

By Region

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Regional Analysis:

North America holds the largest share of the Navigation Satellite Payloads Market with 36%. Strong government funding, defense modernization, and NASA-led space initiatives ensure a steady pipeline of satellite deployments. The United States leads with advanced payload development and a thriving private space sector, supported by SpaceX, Lockheed Martin, and Northrop Grumman. Canada contributes through Earth observation and navigation-focused missions. Europe accounts for 28% of the market, driven by the Galileo program and investments from the European Space Agency. Countries such as Germany, France, and the UK focus on secure payloads, scientific missions, and space-based communication. It maintains a strong position through collaborations between aerospace manufacturers and national governments.

Asia Pacific represents 24% of the Navigation Satellite Payloads Market and shows the fastest growth. China and India dominate through expanding navigation constellations like BeiDou and NavIC, reinforcing regional independence in satellite navigation. Japan and South Korea invest in next-generation payloads to support space security and technological innovation. Growing demand for navigation systems in aviation, defense, and smart infrastructure accelerates market expansion across the region. Small satellite programs in Australia and Southeast Asia enhance accessibility and broaden participation. It continues to strengthen through rising investments in national space programs, public-private partnerships, and advancements in low-cost launch capabilities.

Latin America holds 6% of the Navigation Satellite Payloads Market, with Brazil and Mexico leading regional participation. Investments focus on Earth observation and navigation support for agriculture, environmental monitoring, and defense applications. Middle East & Africa account for 6% as well, where nations such as the UAE, Saudi Arabia, and South Africa expand space ambitions. These regions rely heavily on collaborations with international space agencies and commercial players. Demand is rising for satellite navigation to support aviation safety, smart cities, and defense modernization. It remains a developing market space with long-term potential driven by capacity building, regional partnerships, and adoption of navigation-enabled technologies.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Raytheon Technologies Corporation (RTX)

- Thales Alenia Space

- L3Harris Technologies, Inc.

- Airbus S.A.S.

- Boeing

- OHB System AG

- Honeywell International Inc.

- Mitsubishi Electric Corporation

- Viasat Inc.

- Intelsat

- Collins Aerospace

- General Dynamics Mission Systems Inc.

- OneWeb

Competitive Analysis:

The Navigation Satellite Payloads Market is characterized by strong competition among global aerospace and defense companies, regional agencies, and emerging private firms. Leading players such as Lockheed Martin, Airbus, Thales Alenia Space, Northrop Grumman, and OHB SE dominate with established portfolios in navigation and communication payloads. It benefits from ongoing collaborations between government agencies and commercial operators to develop secure, resilient, and next-generation satellite systems. Chinese and Indian organizations strengthen their positions with indigenous navigation constellations and expanding satellite programs. Startups and smaller firms drive innovation through software-defined payloads, miniaturization, and cost-effective small satellite solutions. Partnerships across supply chains, combined with investments in advanced frequency bands and AI-driven payloads, intensify competition. Global players focus on differentiation through reliability, precision, and adaptability to remain competitive in evolving market conditions.

Recent Developments:

- In August 2025, Rocket Lab demonstrated notable expansion in the navigation satellite payloads market by acquiring GEOST LLC, a move aimed at broadening its capabilities in advanced payload integration for commercial and defense customers.

- In August 2025, the U.S. Space Force launched the L3Harris-built NTS-3 experimental navigation satellite. This mission marks the first U.S. integrated navigation satellite system in almost 50 years, developed to test and demonstrate cutting-edge PNT technologies.

- In June 2025, Xona Space Systems secured $92 million in new funding following the successful launch of its Pulsar-0 satellite. The investment came via a Series B round led by Craft Ventures and a strategic funding boost from SpaceWERX, the U.S. Space Force’s innovation arm. This positions Xona to expand its satellite-based positioning, navigation, and timing (PNT) services for automotive, logistics, mining, and defense sectors.

- In August 2024, Lockheed Martin completed the acquisition of Terran Orbital to strengthen its market presence in satellite manufacturing, particularly for small satellite payloads that support advanced navigation and Earth observation functions. The deal allowed Lockheed Martin to incorporate.

Report Coverage:

The research report offers an in-depth analysis based on Payload Type, Satellite Type, Orbit Type, Frequency Band, Application and End-User. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Expansion of autonomous vehicles and drone ecosystems will increase demand for advanced navigation payloads.

- Integration of artificial intelligence with payload systems will enhance precision, adaptability, and resilience in signal processing.

- Growing defense modernization programs will accelerate adoption of secure and encrypted navigation payloads.

- Development of software-defined payloads will create flexibility for reconfiguration and multi-mission applications.

- Increased participation of private enterprises will broaden competition and reduce deployment costs for satellite payloads.

- Demand for low-cost small satellites will rise, enabling broader access to navigation services across industries.

- Advancements in high-frequency payload bands will support complex applications requiring faster and more reliable data transmission.

- Collaboration between governments and commercial firms will strengthen global navigation constellations and improve interoperability.

- Expanding role of navigation payloads in smart infrastructure and IoT ecosystems will boost long-term market penetration.

- Investments in space sustainability and debris management will influence payload design, emphasizing durability and extended mission lifecycles.