Market Overview

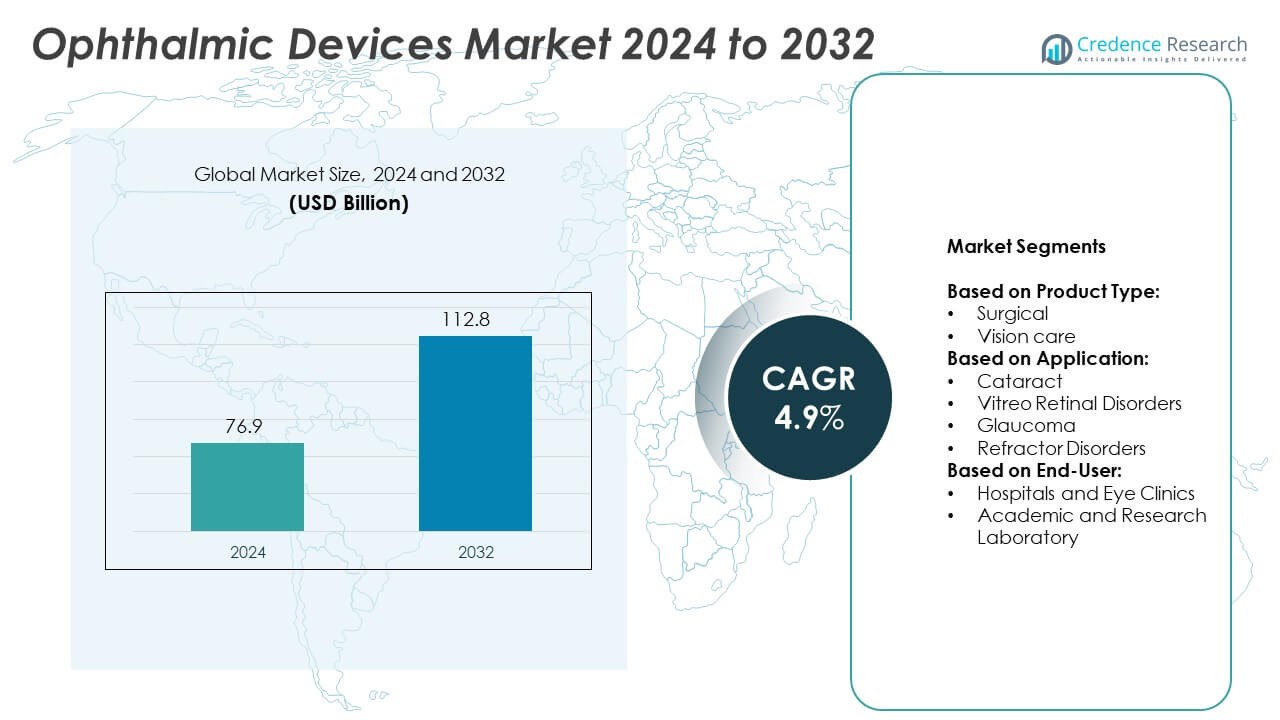

The Ophthalmic Devices Market size was valued at USD 76.9 billion in 2024 and is anticipated to reach USD 112.8 billion by 2032, at a CAGR of 4.9% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Ophthalmic Devices Market Size 2024 |

USD 76.9 Billion |

| Ophthalmic Devices Market, CAGR |

4.9% |

| Ophthalmic Devices Market Size 2032 |

USD 112.8 Billion |

The Ophthalmic Devices market grows through strong drivers such as the rising prevalence of cataracts, glaucoma, and refractive disorders, coupled with an aging global population that increases demand for advanced surgical and vision care solutions. It benefits from technological advancements, including femtosecond lasers, AI-powered diagnostics, and minimally invasive surgical platforms that enhance precision and patient outcomes. Increasing healthcare spending, insurance coverage, and awareness of preventive eye care further strengthen adoption across hospitals and specialty clinics.

The Ophthalmic Devices market demonstrates strong geographical presence with North America leading through advanced healthcare infrastructure and high adoption of innovative technologies. Europe shows steady growth supported by robust regulations and public health programs, while Asia Pacific emerges rapidly due to large patient populations and expanding healthcare access. Latin America and the Middle East & Africa display gradual progress driven by infrastructure improvements. Key players shaping the industry include ZEISS Medical Technology, Alcon Inc, EssilorLuxottica SA, and Topcon Corporation.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Ophthalmic Devices market was valued at USD 76.9 billion in 2024 and is projected to reach USD 112.8 billion by 2032, growing at a CAGR of 4.9%.

- Rising prevalence of cataracts, glaucoma, and refractive disorders drives consistent demand for advanced diagnostic and surgical solutions.

- Technological innovations such as femtosecond lasers, AI-powered diagnostics, and minimally invasive platforms enhance precision, safety, and patient outcomes.

- The market is moderately concentrated, with leading players competing through innovation, acquisitions, and global distribution networks.

- High device costs, strict regulatory frameworks, and shortage of skilled professionals act as restraints to wider adoption, especially in emerging economies.

- North America leads growth with advanced infrastructure and favorable reimbursement policies, while Europe benefits from strong healthcare regulations and Asia Pacific expands rapidly with increasing patient demand.

- The market outlook remains positive with steady demand for preventive care, customized eyewear, and digital solutions, ensuring long-term industry growth across all regions.

Market Drivers

Rising Prevalence of Eye Disorders Driving Demand for Advanced Solutions

The Ophthalmic Devices market gains strength from the global rise in cataracts, glaucoma, refractive errors, and retinal diseases. Aging populations in both developed and emerging economies significantly increase the number of patients requiring surgical and vision care devices. It supports growth through the need for regular diagnostic procedures, corrective lenses, and surgical interventions. Governments and health organizations promote awareness campaigns that encourage early detection and treatment, further expanding device adoption. The consistent demand for corrective eyewear and advanced surgical technologies sustains a stable revenue stream. It benefits from growing demand for high-quality vision correction, ensuring steady expansion across regions.

- For instance, Alcon’s LenSx femtosecond laser platform is accurate, as evidenced by multiple sources citing its widespread adoption, with over 950 units installed across 67 countries and more than 800,000 procedures completed as of 2016, according to a 2016 NCBI article.

Technological Advancements Enhancing Diagnostic and Surgical Accuracy

The market benefits from constant innovation in diagnostic imaging, surgical robotics, and minimally invasive procedures. It supports faster, safer, and more accurate treatment outcomes that appeal to both healthcare providers and patients. Enhanced technologies such as femtosecond lasers, intraocular lenses, and optical coherence tomography are now widely used in hospitals and clinics. The demand for precision-based procedures encourages manufacturers to invest in R&D and expand product portfolios. It creates opportunities for integrating digital solutions, AI-based diagnostics, and real-time monitoring tools. Advanced surgical platforms improve patient recovery times and reduce risks, strengthening confidence in device adoption.

- For instance, Topcon Aladdin optical biometry device operates in over 70 countries with more than 19,000 units deployed worldwide.

Rising Healthcare Expenditure and Insurance Coverage Fueling Access

The Ophthalmic Devices market benefits from rising healthcare spending and broader insurance coverage across key economies. Patients gain better access to advanced surgical procedures, vision correction therapies, and long-term care services. It drives higher adoption rates in both public and private healthcare facilities. Favorable reimbursement policies across developed markets encourage wider use of advanced devices. Expansion of healthcare infrastructure in emerging economies enables faster penetration of ophthalmic technologies. It strengthens the market by reducing barriers to treatment and ensuring affordability for larger populations.

Growing Demand for Personalized and Preventive Eye Care Solutions

The market strengthens its position with the growing demand for personalized treatment and preventive care. Patients increasingly prefer customized eyewear, advanced intraocular lenses, and digital diagnostic solutions tailored to individual needs. It ensures more precise outcomes and greater patient satisfaction, creating strong brand loyalty. Preventive care services, including regular screening and early intervention, enhance long-term market growth. The trend toward proactive eye health management increases the role of specialized ophthalmic devices. It creates a sustainable pathway for expansion by addressing both treatment and prevention.

Market Trends

Integration of Digital Technologies and Artificial Intelligence in Eye Care

The Ophthalmic Devices market shows strong momentum with the adoption of AI-powered diagnostic platforms, teleophthalmology, and digital health applications. It supports faster disease detection and more accurate treatment planning through automated image analysis and predictive analytics. AI algorithms assist ophthalmologists in identifying early signs of glaucoma, macular degeneration, and diabetic retinopathy. Remote consultation platforms expand access to eye care services, especially in underserved regions. It encourages the use of connected devices that facilitate continuous patient monitoring. The trend reflects a broader shift toward technology-driven, patient-centric care models.

- For instance, in the field of optical coherence tomography (OCT), Carl Zeiss Meditec’s IOLMaster 700 utilizes advanced SS-OCT for precise biometry, and as of 2024, there are over 32,000 units operational globally

Expansion of Minimally Invasive and Laser-Based Surgical Procedures

The market gains traction from innovations in minimally invasive and laser-assisted surgeries for cataracts and refractive disorders. It enables faster recovery, reduced complications, and improved surgical precision. Femtosecond lasers and advanced intraocular lenses continue to set new benchmarks for outcomes in ophthalmic surgery. Hospitals and specialty clinics prioritize these technologies to attract patients seeking safer and more effective procedures. It also boosts training programs for surgeons to adapt to high-tech systems. The preference for advanced surgical techniques strengthens the overall demand for premium devices.

- For instance, SCHWIND eye-tech-solutions reports that over 2,250 laser systems have been installed globally, with two-thirds of these installations being the AMARIS platform, highlighting broad adoption in refractive laser surgery

Rising Popularity of Contact Lenses and Premium Eyewear Solutions

The Ophthalmic Devices market benefits from growing consumer preference for contact lenses and customized eyewear. It reflects lifestyle changes, increasing urbanization, and rising interest in aesthetic and functional products. Specialty contact lenses, including toric and scleral types, address complex vision needs with greater comfort. Demand for blue light-blocking and smart lenses further accelerates product innovation. It enhances the retail channel with strong growth in e-commerce and direct-to-consumer sales. The trend underscores how lifestyle choices and fashion influence the adoption of ophthalmic solutions.

Shift Toward Preventive Eye Care and Regular Screening Programs

The market highlights a shift toward preventive care with rising emphasis on routine screenings and early detection. It expands the role of diagnostic imaging systems and portable devices in hospitals and clinics. Public health campaigns and corporate wellness programs increase awareness about eye health. Portable fundus cameras and handheld OCT systems gain popularity in primary care and community health centers. It ensures early treatment and helps reduce the long-term burden of visual impairment. The focus on prevention and early diagnosis secures long-term demand for ophthalmic technologies.

Market Challenges Analysis

High Cost of Advanced Devices and Limited Accessibility in Emerging Regions

The Ophthalmic Devices market faces significant pressure from the high cost of advanced surgical and diagnostic equipment. It creates barriers for smaller clinics and healthcare providers in emerging economies where budgets are limited. Many patients struggle to afford premium intraocular lenses, femtosecond lasers, or advanced imaging systems without strong insurance support. This restricts access to effective treatment for large sections of the population, especially in rural areas. It also slows adoption in regions where healthcare infrastructure remains underdeveloped. Price-sensitive markets often rely on basic or refurbished devices, limiting opportunities for advanced solutions.

Regulatory Hurdles and Shortage of Skilled Professionals Affecting Growth

The market experiences challenges from stringent regulatory requirements that extend approval timelines and increase compliance costs. It complicates product launches for manufacturers trying to introduce innovative technologies quickly. Frequent changes in regulatory frameworks across regions further create uncertainty in global expansion strategies. A shortage of skilled ophthalmologists and trained technicians also hinders effective device utilization. It reduces the efficiency of advanced surgical platforms and diagnostic tools in many healthcare settings. Limited training opportunities in developing economies intensify this gap, leaving advanced equipment underused despite growing demand.

Market Opportunities

Growing Demand for Early Diagnosis and Preventive Eye Care

The Ophthalmic Devices market holds strong opportunities through the rising emphasis on preventive eye care and early detection. It benefits from increasing awareness campaigns that highlight the importance of routine screenings for glaucoma, cataracts, and diabetic retinopathy. Portable diagnostic devices and AI-powered imaging systems create access in community health centers and primary care facilities. Expanding teleophthalmology platforms enable timely consultations, especially in underserved regions. It strengthens adoption of advanced diagnostic tools that ensure better outcomes through early intervention. This focus on preventive care aligns with global health priorities and drives long-term market expansion.

Expansion in Emerging Markets and Adoption of Advanced Surgical Technologies

The market presents significant opportunities in emerging economies where healthcare infrastructure and insurance coverage are expanding. It creates demand for both affordable vision care products and advanced surgical equipment. Rising middle-class populations with higher disposable incomes support greater uptake of premium devices such as intraocular lenses and laser-based platforms. The spread of specialty eye clinics and collaborations between local providers and global manufacturers accelerate adoption. It also encourages investments in training programs to address the shortage of skilled professionals. These developments position emerging markets as key growth drivers for the industry’s future.

Market Segmentation Analysis:

By Product Type:

The Ophthalmic Devices market divides into surgical and vision care devices, both playing a central role in meeting diverse patient needs. Surgical devices hold strong demand due to the rising number of cataract and refractive surgeries worldwide. It benefits from advanced technologies such as femtosecond lasers, intraocular lenses, and robotic-assisted platforms that enhance surgical precision and recovery outcomes. Vision care products such as contact lenses, eyeglasses, and specialty lenses remain essential for correcting refractive errors and improving quality of life. Growing lifestyle-driven demand for customized eyewear and smart lenses strengthens this segment. It ensures steady growth by balancing surgical innovations with mass adoption of vision correction solutions.

- For instance, as of September 2023, the Marietta Eye Clinic indicates that more than 20 million people worldwide have undergone LASIK eye surgery since its introduction

By Application:

The market spans cataract, vitreoretinal disorders, glaucoma, and refractive disorders, with each segment showing unique growth drivers. Cataract treatment dominates due to the high prevalence among aging populations and the availability of effective surgical solutions. It continues to grow with the integration of premium intraocular lenses and minimally invasive techniques. Vitreoretinal disorders gain focus with rising incidences of diabetic retinopathy and macular degeneration, supported by the adoption of advanced imaging and laser systems. Glaucoma treatment benefits from early screening technologies and pressure-monitoring devices that prevent vision loss. It also expands in refractive disorders, where corrective surgeries and advanced lenses address the needs of younger demographics seeking long-term solutions.

- For instance, data shows that nearly 800,000 LASIK surgeries are performed each year in the United States, with over 10 million people having had laser vision surgery since the procedure’s FDA approval

By End-User:

The Ophthalmic Devices market segments into hospitals and eye clinics, and academic and research laboratories. Hospitals and eye clinics dominate due to their wide patient base, advanced surgical facilities, and ability to invest in high-end technologies. It strengthens this segment with the demand for comprehensive care, including diagnostics, surgeries, and vision correction services. Academic and research laboratories contribute by advancing product innovation, clinical trials, and technology validation. Their role in developing next-generation imaging tools, surgical platforms, and AI-powered solutions ensures long-term industry progress. It creates a balance between clinical adoption and research-driven innovation, supporting the continued growth of the market.

Segments:

Based on Product Type:

Based on Application:

- Cataract

- Vitreo Retinal Disorders

- Glaucoma

- Refractor Disorders

Based on End-User:

- Hospitals and Eye Clinics

- Academic and Research Laboratory

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America holds the largest share of the Ophthalmic Devices market, accounting for 38% of the global revenue. The region benefits from advanced healthcare infrastructure, high awareness levels, and widespread access to innovative diagnostic and surgical technologies. It drives strong demand for premium intraocular lenses, femtosecond lasers, and AI-powered imaging systems used for cataract and refractive surgeries. Favorable reimbursement policies and supportive government initiatives further enhance device adoption in hospitals and specialty eye clinics. The rising prevalence of age-related eye disorders such as glaucoma and macular degeneration creates consistent growth opportunities. It also gains momentum from strong collaborations between global manufacturers and regional research institutions, ensuring innovation and accessibility remain aligned.

Europe

Europe represents a significant share of the Ophthalmic Devices market with 27% contribution to global revenues. The region benefits from strict regulatory frameworks that ensure the adoption of high-quality and safe devices. It shows steady demand for diagnostic imaging systems and surgical platforms, driven by an aging population and government-supported screening programs. Increasing investments in public health systems across countries such as Germany, France, and the United Kingdom strengthen accessibility. It supports the development of advanced research in ophthalmology, creating an environment that promotes adoption of innovative products. Rising demand for vision correction solutions, including premium contact lenses and eyewear, also supports market expansion.

Asia Pacific

Asia Pacific holds a growing share of the Ophthalmic Devices market, contributing 22% of the overall value. The region shows rapid expansion due to large patient populations and increasing incidences of cataract, diabetic retinopathy, and myopia. It benefits from government-led healthcare reforms, rising disposable incomes, and expanding insurance coverage across countries like China, India, and Japan. Hospitals and specialty eye clinics in urban centers are adopting advanced surgical and diagnostic technologies at a faster rate. The strong presence of local manufacturers also improves affordability and market penetration. It gains further momentum from international collaborations that expand training and skill development in ophthalmic care.

Latin America

Latin America accounts for 7% of the Ophthalmic Devices market, supported by rising demand for accessible vision care services. The region faces a growing burden of cataract and glaucoma, creating opportunities for surgical devices and vision correction solutions. It experiences gradual improvements in healthcare infrastructure and government-led initiatives to increase patient access. Brazil and Mexico lead adoption trends, with expanding private healthcare facilities and specialty clinics investing in advanced technologies. The demand for affordable solutions also drives reliance on refurbished devices in some areas. It balances between premium product adoption in metropolitan regions and cost-sensitive demand in rural markets.

Middle East and Africa

The Middle East and Africa hold 6% of the Ophthalmic Devices market, with opportunities driven by expanding healthcare systems and rising awareness of preventive eye care. The region benefits from growing investments in hospitals and specialty clinics across the Gulf states and South Africa. It demonstrates strong demand for diagnostic and surgical devices due to the increasing prevalence of cataract and uncorrected refractive errors. Limited access in rural areas continues to restrict widespread adoption, but urban centers show steady growth. International partnerships and mobile healthcare initiatives help bridge gaps in accessibility. It positions the region as an emerging contributor to long-term industry development.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- ZEISS Medical Technology

- Topcon Corporation

- Leica Microsystems

- Alcon Inc

- Volk Optical

- HOYA Surgical Optics

- Nidek Co., Ltd.

- Ziemer Ophthalmic Systems AG

- EssilorLuxottica SA

- Bausch + Lomb Surgical

- Haag-Streit Group

Competitive Analysis

The leading players in the Ophthalmic Devices market include ZEISS Medical Technology, Topcon Corporation, Leica Microsystems, Alcon Inc, Volk Optical, HOYA Surgical Optics, Nidek Co., Ltd., Ziemer Ophthalmic Systems AG, EssilorLuxottica SA, Bausch + Lomb Surgical, and Haag-Streit Group. These companies maintain strong competitive positions through advanced product portfolios, global presence, and continuous investments in research and development.The market remains highly competitive, with emphasis on innovation in surgical platforms, diagnostic imaging systems, and premium vision care products. Companies focus on integrating AI-based diagnostics, laser technologies, and customized intraocular lenses to strengthen clinical outcomes and patient satisfaction. Strategic mergers, acquisitions, and partnerships expand their geographical reach and diversify product lines. Intense rivalry drives consistent improvements in precision, safety, and ease of use, ensuring rapid adoption among hospitals and specialty clinics. Competition also extends to affordability, with firms investing in cost-effective solutions to increase penetration in emerging markets. Strong brand equity, wide distribution networks, and clinical collaborations allow these players to maintain long-term leadership in the industry. The competitive environment reflects a balance between premium technology providers and innovators delivering scalable solutions for global healthcare demands.

Recent Developments

- In 2025, The FDA approved ENCELTO, the first therapy for Macular Telangiectasia type 2, based on encapsulated cell technology that delivers sustained proteins to the retina.

- In May 7, 2024, Bausch and Lomb Corporation, a leading worldwide eye health enterprise that helps patients see better, introduced Zenlens ECHO in the United States as a response to a challenge to design custom scleral contact lenses to fit corneas with different shapes and dimensions. Zenlens ECHO was launched in 2020 and aimed to provide top-notch custom scleral contact lenses, especially for people with sophisticated ocular disorders such as multiple stages of corneal degeneration and epithelial coma, and specific postoperative conditions.

- In February 6, 2024, Iridex Corporation, a worldwide leader in advancing laser-based medical systems, delivery devices, and procedure probes to treat glaucoma and retinal diseases, announces the European Patent EP 3009093 Number. The patent was awarded for the invention entitled Laser System with Short Pulse Characteristics and its Method of Use. In the European marketplace, this patent greatly enhances the company’s intellectual property coverage, especially when it comes to laser systems in ophthalmology and related fields. It covers technology intended to improve the safety and effectiveness of laser therapy. MicroPulse ® devices powered by this patented technology are exclusively produced and distributed by Iridex.

Report Coverage

The research report offers an in-depth analysis based on Product Type, Application, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will expand through rising demand for advanced diagnostic imaging systems.

- It will gain momentum from increasing adoption of AI-powered ophthalmic solutions.

- Hospitals and clinics will continue to drive demand for premium surgical platforms.

- It will benefit from growing awareness of preventive eye care and early screening.

- Emerging economies will offer strong opportunities through expanding healthcare access.

- It will experience growth in demand for minimally invasive and laser-based surgeries.

- Vision care products will remain essential with rising adoption of customized eyewear.

- It will advance through integration of teleophthalmology and remote patient monitoring.

- Research collaborations will support continuous innovation in ophthalmic technologies.

- It will maintain steady growth through increasing prevalence of age-related eye disorders.