Market Overview:

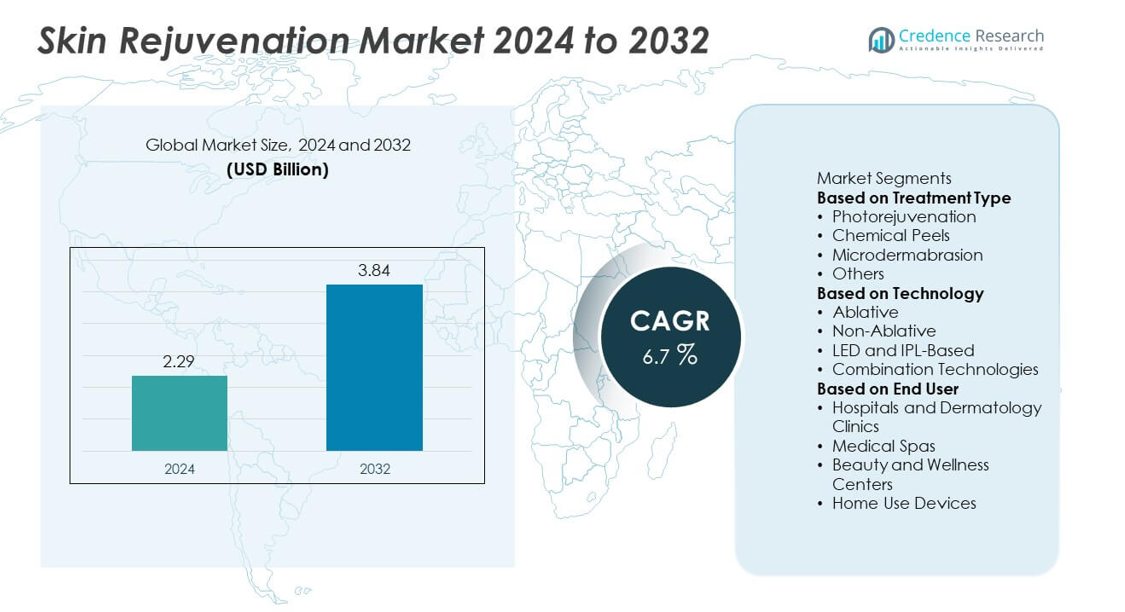

The Skin Rejuvenation market was valued at USD 2.29 billion in 2024 and is projected to reach USD 3.84 billion by 2032, expanding at a CAGR of 6.7% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Skin Rejuvenation Market Size 2024 |

USD 2.29 billion |

| Skin Rejuvenation Market, CAGR |

6.7% |

| Skin Rejuvenation Market Size 2032 |

USD 3.84 billion |

The Skin Rejuvenation market is led by major companies including Cutera Inc., Cynosure LLC, Lumenis Be Ltd., Alma Lasers (Sisram Medical), Sciton Inc., Bausch Health Companies Inc., Venus Concept Ltd., Lutronic Corporation, Fotona d.o.o., and Solta Medical (Bausch + Lomb). These players focus on technological advancements such as hybrid laser platforms, RF microneedling, and combination therapy systems to improve treatment precision and patient comfort. North America dominates the global market with a 37.2% share in 2024, supported by strong aesthetic awareness, high disposable income, and widespread adoption of energy-based skin rejuvenation devices. Europe holds 31.4% share, driven by well-established dermatology infrastructure and increasing demand for non-invasive treatments. Continuous innovation, growing medical spa networks, and the integration of AI-driven skincare diagnostics are expected to reinforce market leadership across both regions during the forecast period.

Market Insights

- The Skin Rejuvenation market was valued at USD 2.29 billion in 2024 and is projected to reach USD 3.84 billion by 2032, growing at a CAGR of 6.7%.

- Market growth is driven by rising demand for non-invasive aesthetic procedures and technological innovations in laser and RF-based rejuvenation systems.

- Key trends include the surge in combination therapy treatments, adoption of portable home-use devices, and the growing influence of AI in personalized skincare solutions.

- Leading companies such as Cutera, Cynosure, Lumenis, and Alma Lasers focus on developing energy-efficient, multi-technology platforms to gain competitive advantage.

- Regionally, North America leads with a 37.2% share, followed by Europe at 31.4%, while the photorejuvenation segment dominates with 42.6% share, supported by its high effectiveness in treating wrinkles, pigmentation, and sun damage.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Treatment Type

The photorejuvenation segment dominated the skin rejuvenation market in 2024, accounting for 38.7% share. Its dominance is driven by rising demand for non-invasive procedures that reduce pigmentation, fine lines, and sun damage. The technique’s minimal downtime and visible results have boosted adoption among both men and women. The increasing use of IPL (Intense Pulsed Light) systems for treating acne scars and age spots further strengthens its popularity. Growing preference for safe, energy-based cosmetic treatments supports sustained growth in this segment, while chemical peels and microdermabrasion continue to hold stable market positions.

- For instance, the Cynosure Icon aesthetic platform is an industry-leading system that offers a comprehensive suite of popular treatments including photorejuvenation and pigmentation management.

By Technology

The non-ablative technology segment held the largest 44.2% share of the skin rejuvenation market in 2024. Non-ablative systems deliver heat beneath the skin without damaging the surface, promoting collagen production and tissue repair. Their safety profile and faster recovery times make them highly preferred among patients seeking gradual but long-lasting results. Advancements in laser and RF-based devices continue to improve treatment precision and comfort. The combination of effective results and minimal downtime drives growing adoption across clinics and medspas, while LED and IPL-based systems expand due to affordability and lower risk of side effects.

- For instance, Lumenis’ ResurFX non-ablative fractional laser operates at 1565 nm and covers treatment areas up to 20 × 20 mm per pass. The device enables over 600 micro-spots per cm², enhancing collagen remodeling while keeping epidermal recovery under 48 hours.

By End User

Hospitals and dermatology clinics accounted for 41.5% share of the skin rejuvenation market in 2024. These facilities remain primary centers for advanced treatments due to the availability of skilled professionals and FDA-approved devices. Growing patient trust in medically supervised procedures enhances this segment’s dominance. Medical spas are also expanding rapidly, offering affordable and convenient rejuvenation services. Increasing partnerships between device manufacturers and dermatologists support equipment upgrades in hospitals. Meanwhile, home-use devices are gaining popularity among consumers seeking cost-effective, maintenance-based skin rejuvenation solutions, driving steady growth in the personal aesthetics segment.

Key Growth Drivers

Rising Demand for Non-Invasive Aesthetic Procedures

The growing preference for minimally invasive treatments is a major driver for the skin rejuvenation market. Consumers seek visible results with reduced recovery time and minimal discomfort. Advances in laser, IPL, and RF technologies have improved safety and precision, attracting both men and women. The increasing popularity of outpatient treatments in dermatology clinics and medical spas further supports this trend. Rising awareness about anti-aging solutions among younger consumers continues to strengthen global demand.

- For instance, Alma Lasers’ Harmony XL Pro platform integrates seven different technologies, including 540 nm and 650 nm IPL modules, enabling over 65 aesthetic applications. The system treats more than 2 million patients annually worldwide, offering quick recovery and minimal epidermal trauma through advanced motion-based delivery.

Increasing Focus on Anti-Aging and Skin Health

An aging global population and growing focus on preventive skincare are fueling market expansion. Consumers are investing more in treatments that boost collagen, enhance elasticity, and reduce wrinkles. The surge in demand for non-surgical anti-aging solutions, supported by social media influence, has expanded the consumer base. High-income groups and urban professionals are increasingly choosing advanced rejuvenation procedures. This growing interest in maintaining youthful and healthy skin drives consistent adoption across all regions.

- For instance, some medical devices are designed to use light energy to target specific skin concerns. These devices deliver pulses of light with varying characteristics that can influence the skin. The body’s response to such treatments can involve processes like stimulating collagen production, which may lead to changes in skin tone, texture, and elasticity over time.

Technological Advancements in Laser and Energy-Based Devices

Rapid innovation in energy-based technologies such as fractional lasers, radiofrequency, and IPL systems is boosting market growth. These devices offer precise results, faster recovery, and compatibility with multiple skin types. Integration of AI-driven skin analysis and compact home-use models enhances accessibility and user experience. Manufacturers are developing multifunctional systems combining different technologies for more effective treatment outcomes. Such continuous advancements are improving performance, safety, and user confidence, driving wider acceptance of modern rejuvenation methods.

Key Trends and Opportunities

Expansion of Combination Therapy Approaches

Combination therapies are emerging as a strong trend in skin rejuvenation practices. Dermatologists and aesthetic centers are combining laser, microneedling, and chemical peel treatments for comprehensive results. This multi-modal approach helps address pigmentation, texture, and fine lines simultaneously. It reduces the number of sessions needed while improving treatment effectiveness and patient satisfaction. The growing popularity of customized rejuvenation packages supports the long-term growth of this segment in both developed and emerging markets.

- For instance, Cutera’s Secret PRO platform integrates RF microneedling with a CO₂ laser (which has a wavelength of 10,600 nm), enabling treatment depths for the RF microneedling component up to 3.5 mm. The dual-mode system effectively treats the full thickness of the skin from the epidermis to the deeper dermal layers to achieve enhanced results compared to using the two technologies separately.

Emergence of Home-Use and Portable Rejuvenation Devices

The demand for home-use rejuvenation devices is rising with the advancement of compact, safe, and user-friendly technologies. Portable RF, LED, and laser devices are providing consumers with convenient skincare options outside clinics. These devices are especially popular among urban populations seeking regular treatment maintenance. Increasing availability through e-commerce platforms and affordable pricing strategies supports this trend. FDA approvals and improved safety standards are further enhancing consumer trust and expanding the product’s global reach.

- For instance, TriPollar’s STOP VX device by Pollogen utilizes third-generation Multi-RF technology operating at a frequency of approximately 1 MHz to 1.25 MHz for collagen stimulation. Clinical studies and independent evaluations have demonstrated measurable dermal tightening and wrinkle reduction, with visible results often appearing within six weekly sessions, which are proven to deliver long-term results.

Key Challenges

High Cost of Advanced Rejuvenation Treatments

High treatment and equipment costs continue to restrain market growth, especially in developing regions. Advanced laser and energy-based procedures require costly machinery and professional expertise, raising the overall expense. The absence of insurance coverage for aesthetic treatments also limits consumer affordability. Manufacturers and clinics are focusing on modular equipment and installment-based payment systems to increase accessibility. Affordable service models and portable devices are expected to gradually reduce this cost barrier.

Risk of Side Effects and Lack of Skilled Professionals

Despite progress in safety standards, risks such as burns, redness, and pigmentation remain concerns. These side effects often result from untrained operators or incorrect device usage. The shortage of certified dermatologists and aesthetic practitioners in emerging markets worsens the issue. Different skin tones require tailored treatment approaches, making expertise crucial for consistent outcomes. Industry stakeholders are prioritizing professional training and device safety certifications to improve service quality and patient trust.

Regional Analysis

North America

North America held the largest share of 38.2% in the Skin Rejuvenation market in 2024. The region’s dominance is driven by advanced healthcare infrastructure, strong consumer spending on aesthetics, and high adoption of minimally invasive procedures. The United States leads due to the widespread availability of laser and RF technologies, supported by skilled dermatologists and cosmetic surgeons. Increasing awareness of anti-aging treatments and the popularity of non-surgical facial enhancement drive steady demand. Government-approved devices and FDA-certified products also contribute to maintaining strong market growth across both clinical and home-use segments.

Europe

Europe accounted for 30.4% share of the global Skin Rejuvenation market in 2024. The region benefits from growing demand for non-invasive anti-aging procedures, particularly in Germany, France, and the United Kingdom. Strong regulatory frameworks ensure the safety and effectiveness of aesthetic technologies. The aging population and rising emphasis on natural-looking results further support market expansion. Cosmetic tourism in countries like Spain and Italy continues to grow due to affordable treatment options. Moreover, increasing collaborations between device manufacturers and dermatology clinics enhance technology penetration and treatment accessibility across European markets.

Asia Pacific

Asia Pacific captured 23.9% share of the Skin Rejuvenation market in 2024. Rapid urbanization, rising disposable income, and growing beauty consciousness among younger populations fuel demand across China, Japan, and South Korea. The region is becoming a hub for innovative, cost-effective rejuvenation solutions, with strong manufacturing capabilities. Expanding medical tourism, particularly in Thailand and India, contributes to regional growth. Increasing investments by global aesthetic device companies in Asia further strengthen product availability. Consumers are increasingly seeking advanced laser and RF treatments, supported by widespread adoption in medical spas and dermatology centers.

Latin America

Latin America represented 4.8% share of the Skin Rejuvenation market in 2024. The market is expanding in Brazil, Mexico, and Argentina, driven by rising awareness of cosmetic procedures and growing middle-class income. Demand for affordable non-invasive skin treatments is increasing in urban areas. Medical tourism and improved accessibility to advanced technologies are boosting clinical adoption. Local dermatology clinics are focusing on offering combination therapies tailored to diverse skin types. However, economic instability and limited reimbursement policies still pose barriers. Despite this, the region’s aesthetic awareness and technology adoption continue to support gradual market expansion.

Middle East & Africa

The Middle East & Africa accounted for 2.7% share of the Skin Rejuvenation market in 2024. Growth is supported by increasing disposable income, rising beauty awareness, and expanding healthcare infrastructure. Countries such as the UAE and Saudi Arabia lead the market due to the rapid rise of luxury medical spas and aesthetic centers. Consumers are adopting laser and RF-based skin treatments for pigmentation and texture correction. Africa shows potential with growing cosmetic demand in South Africa and Egypt. However, high treatment costs and limited trained professionals continue to restrict wider adoption across several parts of the region.

Market Segmentations:

By Treatment Type

- Photorejuvenation

- Chemical Peels

- Microdermabrasion

- Others

By Technology

- Ablative

- Non-Ablative

- LED and IPL-Based

- Combination Technologies

By End User

- Hospitals and Dermatology Clinics

- Medical Spas

- Beauty and Wellness Centers

- Home Use Devices

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The competitive landscape of the Skin Rejuvenation market includes key players such as Cutera Inc., Cynosure LLC, Lumenis Be Ltd., Alma Lasers (Sisram Medical), Sciton Inc., Bausch Health Companies Inc., Venus Concept Ltd., Lutronic Corporation, Fotona d.o.o., and Solta Medical (Bausch + Lomb). These companies compete through product innovation, clinical efficacy, and global expansion strategies. Leading manufacturers focus on developing advanced energy-based systems, including laser, RF, and IPL devices, that provide faster recovery and personalized treatment outcomes. Continuous R&D efforts aim to enhance device safety, precision, and multifunctionality. Partnerships with dermatology clinics, training programs for practitioners, and marketing of portable home-use devices strengthen market presence. Moreover, regulatory approvals and geographic diversification are helping these players capture growing demand across developed and emerging markets. Competition remains intense, with increasing emphasis on technological differentiation, sustainability, and integration of AI and digital diagnostics in next-generation skin rejuvenation platforms.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Cutera Inc.

- Cynosure LLC

- Lumenis Be Ltd.

- Alma Lasers (Sisram Medical)

- Sciton Inc.

- Bausch Health Companies Inc.

- Venus Concept Ltd.

- Lutronic Corporation

- Fotona d.o.o.

- Solta Medical (Bausch + Lomb)

Recent Developments

- In August 2025, Cutera Inc. launched Secret by Cutera in Australia and New Zealand. The release expanded access to CO₂ resurfacing and RF microneedling under Secret PRO. Indications include fractional resurfacing and surgical modes.

- In March 2025, Cynosure LLC’s PicoSure Pro won a 2025 NewBeauty Award. The recognition highlighted melasma treatment performance with the 755 nm picosecond laser. Clinics use it for pigment and rejuvenation.

- In October 2024, Skinnovation introduced two medical devices, Meta Cell Technology (MCT) and MIRApeel. These devices were developed to address common skin issues faced by Indians, including sagging skin, fine lines, acne scars, and uneven texture.

- In August 2024, Purple Pompa launched its new skincare line focused on “Age Balance,” designed to support natural aging while promoting skin rejuvenation, presenting a fresh alternative to conventional anti-aging solutions.

Report Coverage

The research report offers an in-depth analysis based on Treatment Type, Technology, End User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will expand due to rising demand for non-invasive and minimally invasive aesthetic treatments.

- Technological innovations in laser, RF, and LED-based systems will enhance treatment precision and outcomes.

- Growing consumer focus on anti-aging and preventive skincare will support consistent market growth.

- Portable and home-use rejuvenation devices will gain strong adoption among younger consumers.

- Clinics and medical spas will continue leading adoption, driven by high procedure success rates.

- Asia Pacific will emerge as the fastest-growing region with increasing cosmetic procedure awareness.

- Integration of AI and imaging analytics will improve treatment customization and patient satisfaction.

- Sustainable and energy-efficient device manufacturing will become a key industry focus.

- Strategic collaborations between technology developers and dermatology clinics will drive innovation.

- The market will see increased competition as new entrants introduce affordable and versatile rejuvenation systems.