CHAPTER NO. 1 : INTRODUCTION 19

1.1. Report Description 19

Purpose of the Report 19

USP & Key Offerings 19

1.2. Key Benefits for Stakeholders 19

1.3. Target Audience 20

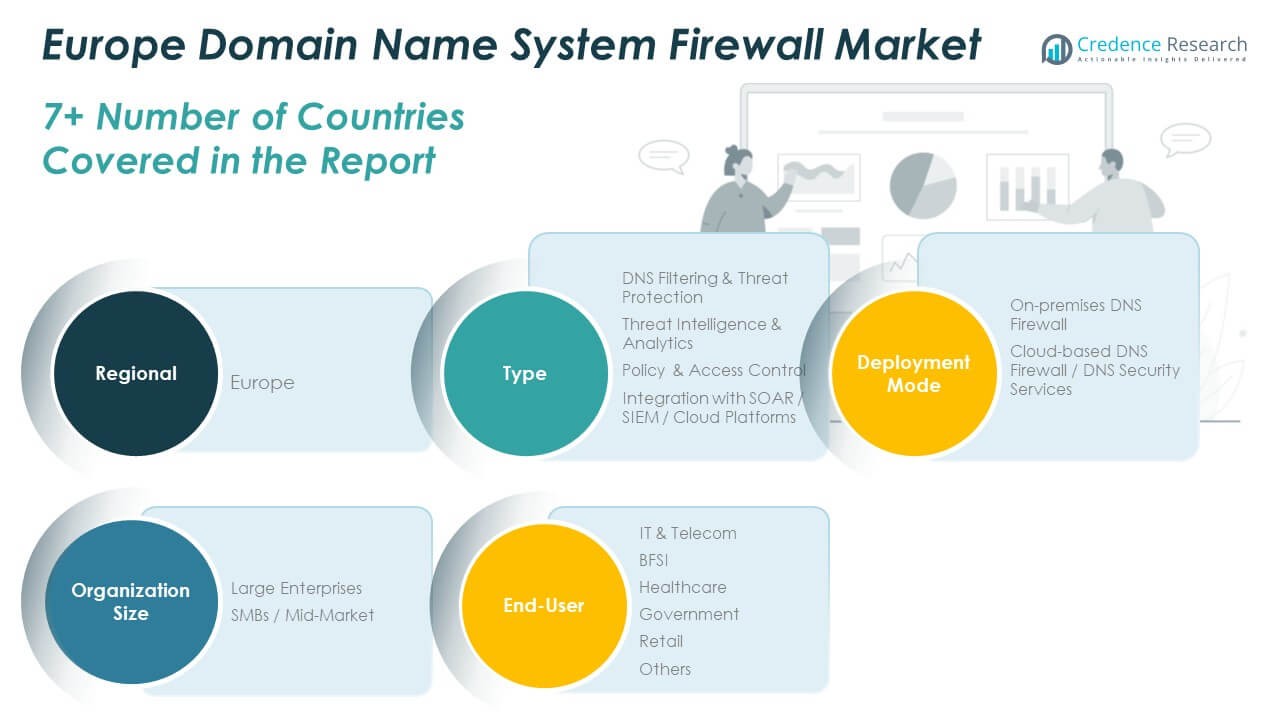

1.4. Report Scope 20

1.5. Regional Scope 21

CHAPTER NO. 2 : EXECUTIVE SUMMARY 22

2.1. Domain Name System Firewall Market Snapshot 22

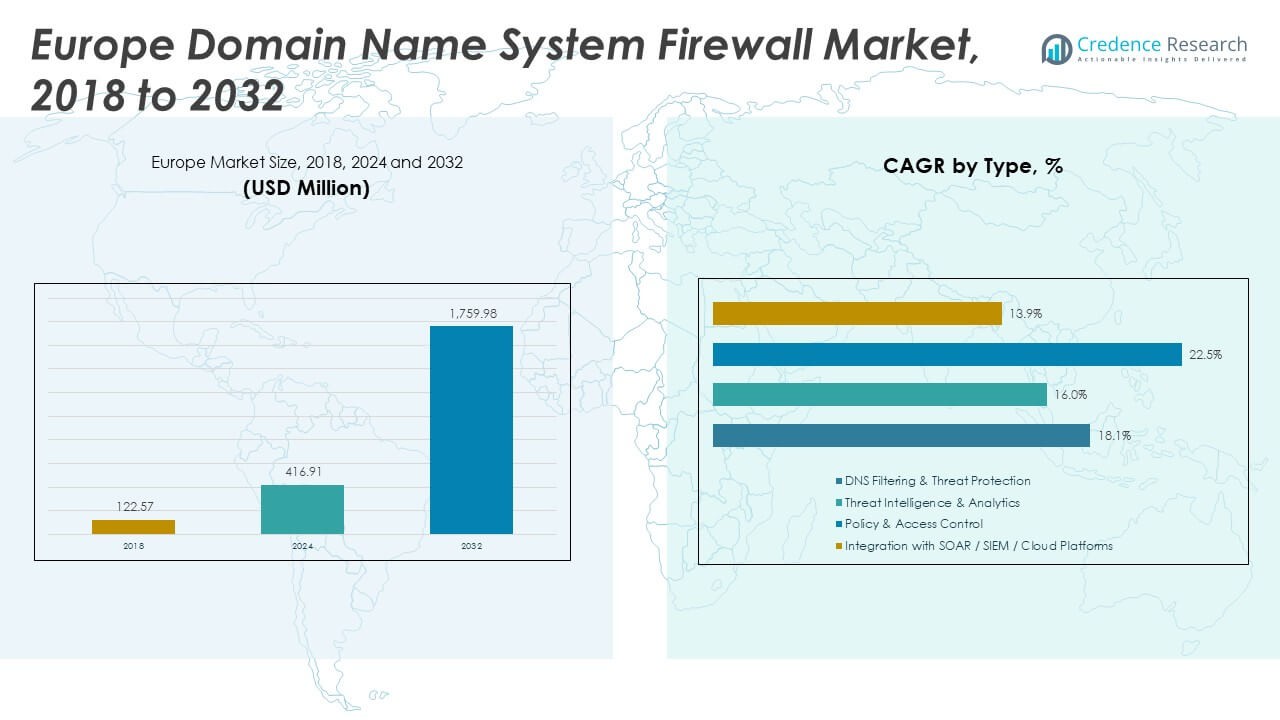

2.2. Europe Domain Name System Firewall Market, 2018 – 2032 (USD Million) 23

CHAPTER NO. 3 : DOMAIN NAME SYSTEM FIREWALL MARKET – INDUSTRY ANALYSIS 24

3.1. Introduction 24

3.2. Market Drivers 25

3.3. Growing adoption of cybersecurity automation and orchestration solutions 25

3.4. Increasing prevalence of DNS-based attacks and malware 26

3.5. Market Restraints 27

3.6. High complexity in integration with existing security infrastructure 27

3.7. Market Opportunities 28

3.8. Market Opportunity Analysis 28

3.9. Market Trends 29

3.10. Market Trend Analysis 29

3.11. Porter’s Five Forces Analysis 30

3.12. Value Chain Analysis 31

3.13. DNS Firewall Integration Workflow 32

3.14. Key Firewall Features and Benefits 33

3.15. Ease of Operations, Operational Planning, and Future Requirements 34

3.16. Ease of Implementation & Arguments for Adoption 35

3.17. Decision Timeline (PoV to Full Rollout) 36

CHAPTER NO. 4 : ANALYSIS COMPETITIVE LANDSCAPE 37

4.1. Company Market Share Analysis – 2024 37

4.1.1. Europe Domain Name System Firewall Market: Company Market Share, by Revenue, 2024 37

4.2. Europe Domain Name System Firewall Market Company Revenue Market Share, 2024 38

4.3. Company Assessment Metrics, 2024 39

4.3.1. Stars 39

4.3.2. Emerging Leaders 39

4.3.3. Pervasive Players 39

4.3.4. Participants 39

4.4. Start-ups /SMEs Assessment Metrics, 2024 39

4.4.1. Progressive Companies 39

4.4.2. Responsive Companies 39

4.4.3. Dynamic Companies 39

4.4.4. Starting Blocks 39

4.5. Strategic Developments 40

4.5.1. Acquisitions & Mergers 40

New Type Launch 40

Regional Expansion 40

4.6. Key Players Type Matrix 41

CHAPTER NO. 5 : PESTEL & ADJACENT MARKET ANALYSIS 42

5.1. PESTEL 42

5.1.1. Political Factors 42

5.1.2. Economic Factors 42

5.1.3. Social Factors 42

5.1.4. Technological Factors 42

5.1.5. Environmental Factors 42

5.1.6. Legal Factors 42

5.2. Adjacent Market Analysis 42

CHAPTER NO. 6 : DOMAIN NAME SYSTEM FIREWALL MARKET – BY TYPE SEGMENT ANALYSIS 43

6.1. Domain Name System Firewall Market Overview, by Type Segment 43

6.1.1. Domain Name System Firewall Market Revenue Share, By Type, 2023 & 2032 44

6.1.2. Domain Name System Firewall Market Attractiveness Analysis, By Type 45

6.1.3. Incremental Revenue Growth Opportunity, by Type, 2024 – 2032 45

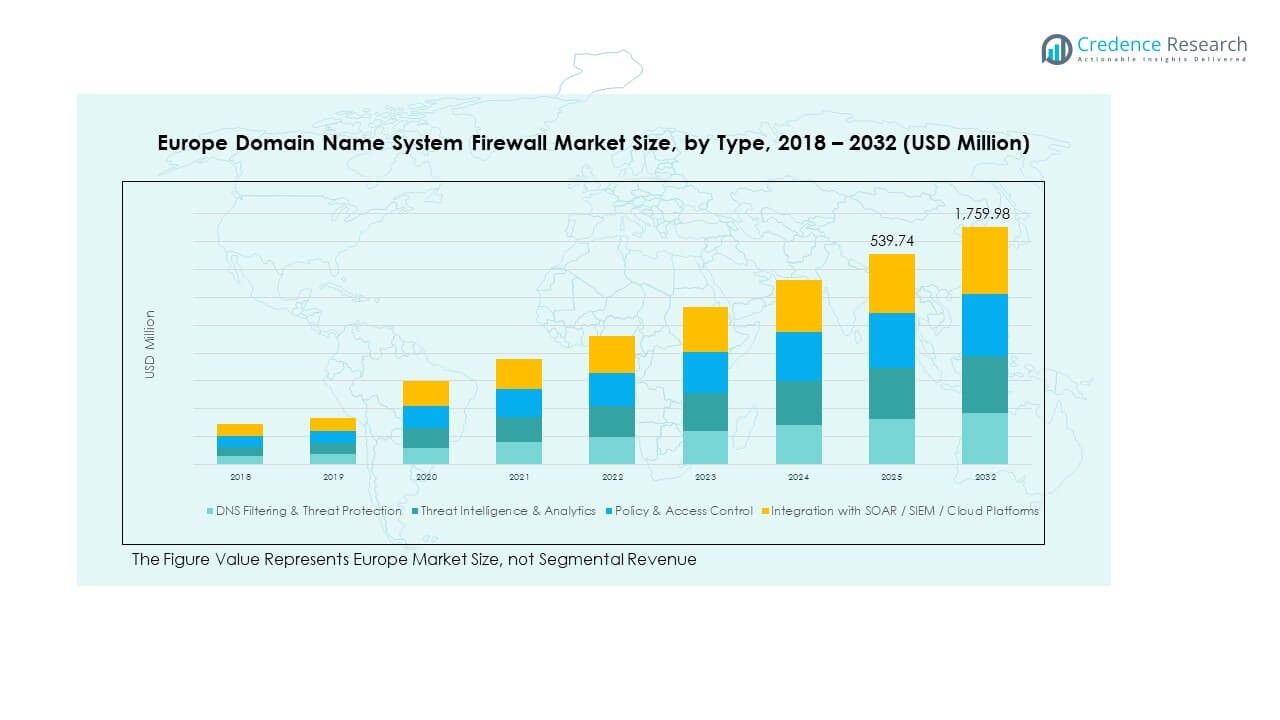

6.1.4. Domain Name System Firewall Market Revenue, By Type, 2018, 2023, 2027 & 2032 46

6.2. DNS Filtering & Threat Protection 47

6.3. Threat Intelligence & Analytics 48

6.4. Policy & Access Control 49

6.5. Integration with SOAR / SIEM / Cloud Platforms 50

CHAPTER NO. 7 : DOMAIN NAME SYSTEM FIREWALL MARKET – BY DEPLOYMENT MODE SEGMENT ANALYSIS 51

7.1. Domain Name System Firewall Market Overview, by Deployment Mode Segment 51

7.1.1. Domain Name System Firewall Market Revenue Share, By Deployment Mode, 2023 & 2032 52

7.1.2. Domain Name System Firewall Market Attractiveness Analysis, By Deployment Mode 53

7.1.3. Incremental Revenue Growth Opportunity, by Deployment Mode, 2024 – 2032 53

7.1.4. Domain Name System Firewall Market Revenue, By Deployment Mode, 2018, 2023, 2027 & 2032 54

7.2. On-premises DNS Firewall 55

7.3. Cloud-based DNS Firewall / DNS Security Services 56

CHAPTER NO. 8 : DOMAIN NAME SYSTEM FIREWALL MARKET – BY ORGANIZATION SIZE SEGMENT ANALYSIS 57

8.1. Domain Name System Firewall Market Overview, by Organization Size Segment 57

8.1.1. Domain Name System Firewall Market Revenue Share, By Organization Size, 2023 & 2032 58

8.1.2. Domain Name System Firewall Market Attractiveness Analysis, By Organization Size 59

8.1.3. Incremental Revenue Growth Opportunity, by Organization Size, 2024 – 2032 59

8.1.4. Domain Name System Firewall Market Revenue, By Organization Size, 2018, 2023, 2027 & 2032 60

8.2. Large Enterprises 61

8.3. SMBs / Mid-Market 62

CHAPTER NO. 9 : DOMAIN NAME SYSTEM FIREWALL MARKET – BY END-USER SEGMENT ANALYSIS 63

9.1. Domain Name System Firewall Market Overview, by End-User Segment 63

9.1.1. Domain Name System Firewall Market Revenue Share, By End-User, 2023 & 2032 64

9.1.2. Domain Name System Firewall Market Attractiveness Analysis, By End-User 65

9.1.3. Incremental Revenue Growth Opportunity, by End-User, 2024 – 2032 65

9.1.4. Domain Name System Firewall Market Revenue, By End-User, 2018, 2023, 2027 & 2032 66

9.2. IT & Telecom 67

9.3. Healthcare 68

9.4. Government 69

9.5. Retail 70

9.6. Others 71

CHAPTER NO. 10 : DOMAIN NAME SYSTEM FIREWALL MARKET – EUROPE 72

10.1. Europe 72

10.1.1. Key Highlights 72

10.1.2. Europe Domain Name System Firewall Market Revenue, By Country, 2018 – 2023 (USD Million) 73

10.1.3. Germany Domain Name System Firewall Market Revenue, By Type, 2018 – 2023 (USD Million) 74

10.1.4. Europe Domain Name System Firewall Market Revenue, By Deployment Mode, 2018 – 2023 (USD Million) 75

10.1.5. Europe Domain Name System Firewall Market Revenue, By Organization Size, 2018 – 2023 (USD Million) 76

10.1.6. Europe Domain Name System Firewall Market Revenue, By End-User, 2018 – 2023 (USD Million) 77

10.2. Germany 78

10.3. UK 78

10.4. France 78

10.5. Italy 78

10.6. Spain 78

10.7. Russia 78

10.8. Belgium 78

10.9. Netherland 78

10.10. Austria 78

10.11. Sweden 78

10.12. Poland 78

10.13. Denmark 78

10.14. Switzerland 78

10.15. Rest of Europe 78

CHAPTER NO. 12 : COMPANY PROFILES 79

12.1. Infoblox 79

12.1.1. Company Overview 79

12.1.2. Type Portfolio 79

12.1.3. Swot Analysis 79

12.2. Business Strategy 80

12.3. Financial Overview 80

12.4. Cisco 81

12.5. Palo Alto Networks 81

12.6. Fortinet 81

12.7. Check Point Software Technologies 81

12.8. BlueCat Networks 81

12.9. EfficientIP 81

12.10. Company 8 81

12.11. Company 9 81

12.12. Company 10 81

12.13. Company 11 81

12.14. Company 12 81

12.15. Company 13 81

12.16. Company 14 81

List of Figures

FIG NO. 1. Europe Domain Name System Firewall Market Revenue, 2018 – 2032 (USD Million) 23

FIG NO. 2. Porter’s Five Forces Analysis for Europe Domain Name System Firewall Market 30

FIG NO. 3. Value Chain Analysis for Europe Domain Name System Firewall Market 31

FIG NO. 4. Company Share Analysis, 2024 37

FIG NO. 5. Domain Name System Firewall Market – Company Revenue Market Share, 2024 38

FIG NO. 6. Domain Name System Firewall Market Revenue Share, By Type, 2023 & 2032 44

FIG NO. 7. Market Attractiveness Analysis, By Type 45

FIG NO. 8. Incremental Revenue Growth Opportunity by Type, 2024 – 2032 45

FIG NO. 9. Domain Name System Firewall Market Revenue, By Type, 2018, 2023, 2027 & 2032 46

FIG NO. 10. Europe Domain Name System Firewall Market for DNS Filtering & Threat Protection, Revenue (USD Million) 2018 – 2032 47

FIG NO. 11. Europe Domain Name System Firewall Market for Threat Intelligence & Analytics, Revenue (USD Million) 2018 – 2032 48

FIG NO. 12. Europe Domain Name System Firewall Market for Policy & Access Control, Revenue (USD Million) 2018 – 2032 49

FIG NO. 13. Europe Domain Name System Firewall Market for Integration with SOAR / SIEM / Cloud Platforms, Revenue (USD Million) 2018 – 2032 50

FIG NO. 14. Domain Name System Firewall Market Revenue Share, By Deployment Mode, 2023 & 2032 52

FIG NO. 15. Market Attractiveness Analysis, By Deployment Mode 53

FIG NO. 16. Incremental Revenue Growth Opportunity by Deployment Mode, 2024 – 2032 53

FIG NO. 17. Domain Name System Firewall Market Revenue, By Deployment Mode, 2018, 2023, 2027 & 2032 54

FIG NO. 18. Europe Domain Name System Firewall Market for On-premises DNS Firewall, Revenue (USD Million) 2018 – 2032 55

FIG NO. 19. Europe Domain Name System Firewall Market for Cloud-based DNS Firewall / DNS Security Services, Revenue (USD Million) 2018 – 2032 56

FIG NO. 20. Domain Name System Firewall Market Revenue Share, By Organization Size, 2023 & 2032 58

FIG NO. 21. Market Attractiveness Analysis, By Organization Size 59

FIG NO. 22. Incremental Revenue Growth Opportunity by Organization Size, 2024 – 2032 59

FIG NO. 23. Domain Name System Firewall Market Revenue, By Organization Size, 2018, 2023, 2027 & 2032 60

FIG NO. 24. Europe Domain Name System Firewall Market for Large Enterprises, Revenue (USD Million) 2018 – 2032 61

FIG NO. 25. Europe Domain Name System Firewall Market for SMBs / Mid-Market, Revenue (USD Million) 2018 – 2032 62

FIG NO. 26. Domain Name System Firewall Market Revenue Share, By End-User, 2023 & 2032 64

FIG NO. 27. Market Attractiveness Analysis, By End-User 65

FIG NO. 28. Incremental Revenue Growth Opportunity by End-User, 2024 – 2032 65

FIG NO. 29. Domain Name System Firewall Market Revenue, By End-User, 2018, 2023, 2027 & 2032 66

FIG NO. 30. Europe Domain Name System Firewall Market for IT & Telecom, Revenue (USD Million) 2018 – 2032 67

FIG NO. 31. Europe Domain Name System Firewall Market for Healthcare, Revenue (USD Million) 2018 – 2032 68

FIG NO. 32. Europe Domain Name System Firewall Market for Government, Revenue (USD Million) 2018 – 2032 69

FIG NO. 33. Europe Domain Name System Firewall Market for Retail, Revenue (USD Million) 2018 – 2032 70

FIG NO. 34. Europe Domain Name System Firewall Market for Others, Revenue (USD Million) 2018 – 2032 71

FIG NO. 35. Europe Domain Name System Firewall Market Revenue, 2018 – 2032 (USD Million) 72

List of Tables

TABLE NO. 1. : Europe Domain Name System Firewall Market: Snapshot 22

TABLE NO. 2. : Drivers for the Domain Name System Firewall Market: Impact Analysis 25

TABLE NO. 3. : Restraints for the Domain Name System Firewall Market: Impact Analysis 27

TABLE NO. 4. : Europe Domain Name System Firewall Market Revenue, By Country, 2018 – 2023 (USD Million) 73

TABLE NO. 5. : Europe Domain Name System Firewall Market Revenue, By Country, 2024 – 2032 (USD Million) 73

TABLE NO. 6. : Europe Domain Name System Firewall Market Revenue, By Type, 2018 – 2023 (USD Million) 74

TABLE NO. 7. : Europe Domain Name System Firewall Market Revenue, By Type, 2024 – 2032 (USD Million) 74

TABLE NO. 8. : Europe Domain Name System Firewall Market Revenue, By Deployment Mode, 2018 – 2023 (USD Million) 75

TABLE NO. 9. : Europe Domain Name System Firewall Market Revenue, By Deployment Mode, 2024 – 2032 (USD Million) 75

TABLE NO. 10. : Europe Domain Name System Firewall Market Revenue, By Organization Size, 2018 – 2023 (USD Million) 76

TABLE NO. 11. : Europe Domain Name System Firewall Market Revenue, By Organization Size, 2024 – 2032 (USD Million) 76

TABLE NO. 12. : Europe Domain Name System Firewall Market Revenue, By End-User, 2018 – 2023 (USD Million) 77

TABLE NO. 13. : Europe Domain Name System Firewall Market Revenue, By End-User, 2024 – 2032 (USD Million) 77