| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Artificial Intelligence Market Size 2024 |

USD 440.3 million |

| Artificial Intelligence Market, CAGR |

22.64% |

| Artificial Intelligence Market Size 2032 |

USD 2,233.0 million |

Market Overview:

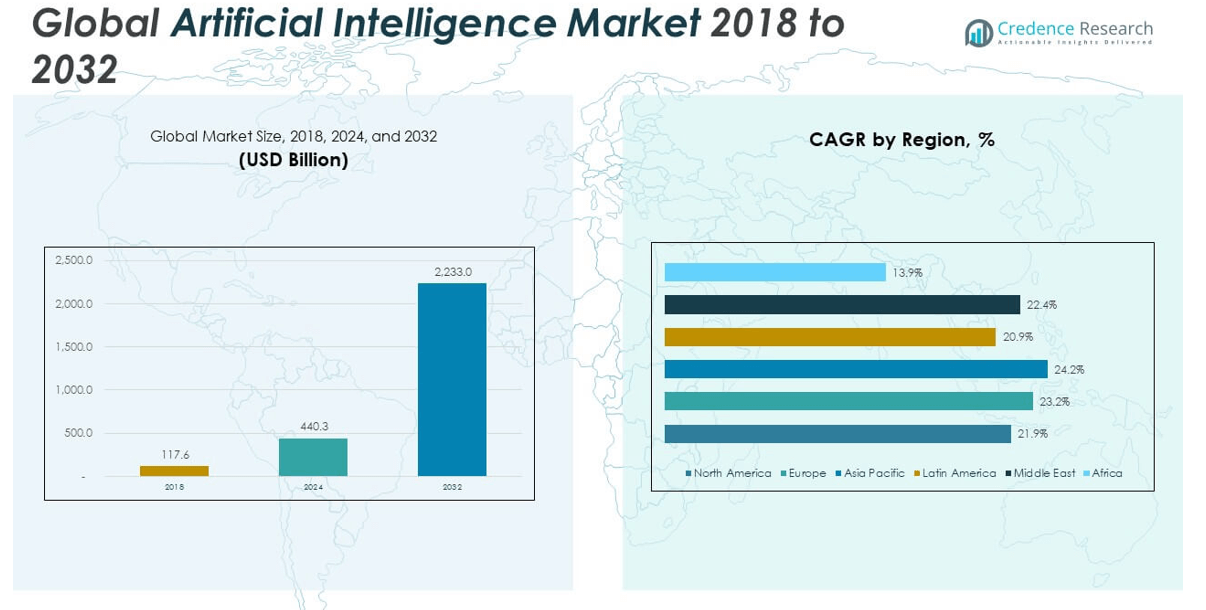

The Global Artificial Intelligence Market size was valued at USD 117.6 million in 2018 to USD 440.3 million in 2024 and is anticipated to reach USD 2,233.0 million by 2032, at a CAGR of 22.64% during the forecast period.

The primary growth drivers of the AI market include the push for enterprise automation, the proliferation of AI-powered applications, and advances in machine learning and neural network technologies. Organizations are embracing AI to reduce operational costs, enhance productivity, and deliver personalized customer experiences. Breakthroughs in deep learning and generative AI models are fueling innovation across diverse sectors, enabling smarter analytics, autonomous systems, and enhanced natural language interfaces. The rapid expansion of cloud computing platforms and AI-as-a-Service (AIaaS) models is making AI tools more accessible, scalable, and affordable for businesses of all sizes. Government investments and national AI strategies are also playing a pivotal role, with countries such as the United States, China, and members of European Union allocating billions of dollars toward AI research, talent development, and commercial deployment. These efforts are establishing AI as a strategic pillar of global economic competitiveness.

Regionally, North America holds the largest share of the global AI market, supported by the presence of major technology firms, strong venture capital activity, and advanced digital infrastructure. The United States leads in private AI funding, having invested. Asia Pacific is the fastest-growing regional market, driven by large-scale government investments, especially in China and India. China has committed over USD 100 billion toward AI initiatives, while India’s AI market is expanding at a CAGR, supported by robust startup activity and national programs. Europe is also advancing through regulatory leadership and funding, including the European Commission’s InvestAI initiative and the AI Act, which aim to promote innovation while ensuring ethical standards. Emerging regions such as Latin America, the Middle East, and Southeast Asia are gradually building AI ecosystems, leveraging investments in infrastructure, education, and international partnerships. These regional developments collectively contribute to a highly dynamic global AI landscape, with localized strengths shaping the competitive and innovation outlook of the market.

Market Insights:

- The Global Artificial Intelligence Market grew from USD 117.6 million in 2018 to USD 440.3 million in 2024 and is projected to reach USD 2,233.0 million by 2032, registering a CAGR of 22.64% during the forecast period.

- Enterprise-wide integration of AI across departments such as finance, HR, logistics, and customer service is driving operational efficiency and expanding market demand.

- Governments and technology firms are heavily investing in AI infrastructure, with national AI strategies and public-private partnerships accelerating innovation globally.

- AI-driven personalization is reshaping customer experiences across sectors like e-commerce, banking, and media, creating demand for dynamic, responsive systems.

- The proliferation of IoT and big data is compelling industries to adopt AI for predictive insights, anomaly detection, and intelligent edge computing applications.

- High implementation costs and lack of AI-ready infrastructure remain major barriers for small and mid-sized enterprises, restricting broader market participation.

- North America leads the market in revenue share, while Asia Pacific is growing fastest, led by aggressive government funding in China and India and regulatory leadership in Europe.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Rising Enterprise Adoption Across Core and Non-Core Operations:

Organizations are integrating AI into business functions ranging from customer service and HR to logistics and finance. This adoption is driven by the need to improve efficiency, reduce manual intervention, and enhance decision-making. Automation powered by AI models is helping enterprises eliminate redundancies and allocate resources strategically. Industries such as healthcare, BFSI, and retail are embedding AI into daily workflows to derive actionable insights from structured and unstructured data. Cloud-native AI platforms are reducing deployment barriers for small and mid-sized enterprises. The Global Artificial Intelligence Market is benefiting significantly from this widespread operational integration across both core and peripheral business domains.

- For instance, JPMorgan Chase deployed its AI-powered virtual assistant “COiN,” which analyzes and interprets legal documents at a rate of contracts in seconds, automating tasks previously requiring 360,000 hours of lawyer work per year.

Accelerating Investment in AI Infrastructure and R&D Initiatives:

Government agencies, private investors, and global technology firms are committing substantial capital toward AI infrastructure and research. Tech leaders like NVIDIA, Microsoft, and Google are expanding AI compute capabilities through GPU development and AI supercomputing projects. Governments in the U.S., China, and EU are sponsoring large-scale national AI strategies to enhance global competitiveness. These initiatives are supporting the growth of data centers, AI chips, and specialized research hubs. Public-private partnerships are fostering ecosystems where academia and industry collaborate to accelerate innovation. It is strengthening the foundation of the Global Artificial Intelligence Market, positioning it for long-term scalability.

- For instance, NVIDIA launched its H100 Tensor Core GPU in late 2023 and, by early 2025, shipped globally for use in hyperscale data centers, advancing large language model training and inference workloads.

Demand Surge for Personalized Customer Experience Solutions:

Companies are using AI to deliver real-time, context-aware experiences that improve customer satisfaction and engagement. AI models trained on behavioral and demographic data are enabling dynamic personalization across digital channels. E-commerce platforms, financial institutions, and streaming services are leveraging these capabilities to predict preferences and optimize recommendations. AI-driven personalization is also reshaping digital marketing, customer support, and product development strategies. These applications are raising consumer expectations for intelligent, responsive services. It is creating sustained demand within the Global Artificial Intelligence Market for solutions that enhance user interaction and retention.

Proliferation of Big Data and IoT Driving AI Integration:

The explosive growth of data from IoT devices, sensors, and enterprise systems is necessitating advanced analytics tools. AI models can process vast datasets at scale, detect anomalies, and generate predictive insights. Industries like manufacturing, energy, and transportation are deploying AI to monitor systems, predict failures, and optimize operations. The expansion of 5G and edge computing is further boosting real-time AI applications in smart factories and autonomous systems. These environments require intelligence at the edge, fueling demand for compact AI solutions. It is propelling the expansion of the Global Artificial Intelligence Market into data-intensive sectors.

Market Trends:

Expansion of Multimodal AI and Cross-Functional Intelligence Models:

Developers are shifting toward AI models that integrate text, images, video, and audio into a single system. Multimodal AI enables systems to interpret complex, real-world scenarios more accurately. This capability is driving innovation in autonomous vehicles, virtual assistants, and defense technologies. Applications in diagnostics, surveillance, and content creation are also gaining momentum. Companies are investing in foundational models that bridge domains for broader generalization. The Global Artificial Intelligence Market is evolving toward unified architectures that support multi-input intelligence.

- For instance, OpenAI’s GPT-4o launched in May 2024, serving over 100 million weekly active users by June and supporting input/output across voice, image, text, and code—all within a single conversational interface.

Growth of Synthetic Data Generation for Model Training:

Businesses are turning to synthetic data to overcome privacy challenges and data scarcity. AI-generated datasets are helping train models when real-world data is unavailable, biased, or insufficient. Sectors like autonomous driving, healthcare, and robotics are using synthetic data to simulate edge cases. It is improving model robustness while protecting sensitive information. Tools that automate synthetic dataset generation are gaining commercial traction. The Global Artificial Intelligence Market is responding to data availability issues by embracing artificial training environments.

- For instance, In healthcare, Syntegra produced fully anonymized, HIPAA-compliant synthetic medical records for clinical AI research by May 2025, enhancing data diversity and privacy protection.

Adoption of AI-Powered Design and Engineering Platforms:

AI is transforming engineering workflows by optimizing design parameters and accelerating prototyping. Generative design tools are helping engineers explore more design iterations in less time. Aerospace, automotive, and construction firms are using AI to simulate real-world stress tests and environmental factors. Machine learning models are assisting in materials selection and predictive maintenance strategies. These capabilities are shortening time-to-market and reducing engineering costs. The Global Artificial Intelligence Market is expanding across R&D-intensive sectors by embedding intelligence into design systems.

Rise of Responsible AI and Ethical Governance Frameworks:

Stakeholders are placing stronger emphasis on fairness, transparency, and accountability in AI systems. Companies are creating internal ethics boards, AI audits, and compliance protocols. Governments and regulatory bodies are drafting laws such as the EU AI Act to ensure responsible AI deployment. Consumers are demanding explainable AI that aligns with societal norms and values. Trust-enhancing technologies like federated learning and model interpretability tools are gaining interest. It is shifting the focus of the Global Artificial Intelligence Market from capability to accountability.

Market Challenges Analysis:

High Implementation Costs and Infrastructure Barriers for Small Enterprises:

The deployment of advanced AI solutions often demands substantial upfront investment in infrastructure, skilled personnel, and ongoing system training. Small and medium-sized enterprises face difficulties in allocating resources for dedicated data scientists, AI engineers, and high-performance computing systems. Complex integration with legacy IT environments further complicates adoption. Many firms lack access to clean, labeled datasets required for accurate AI model training. These financial and technical constraints are slowing AI penetration beyond large corporations. The Global Artificial Intelligence Market continues to face a divide where innovation is concentrated among players with deeper capital and digital readiness.

Data Privacy Concerns and Regulatory Complexity Across Regions:

Widespread use of AI technologies raises pressing concerns about data ownership, consent, and surveillance. Differing regional regulations—such as GDPR in Europe, HIPAA in the U.S., and evolving data localization laws in Asia—are creating compliance challenges for global AI providers. Companies must navigate fragmented legal frameworks while ensuring their models remain transparent, unbiased, and secure. Incidents of AI model bias, misuse, and opaque decision-making are fueling public skepticism. These concerns are prompting calls for explainable AI and third-party auditing protocols. It presents a regulatory headwind for the Global Artificial Intelligence Market, forcing firms to balance innovation with responsible governance.

Market Opportunities:

Expanding Role of AI in Industry-Specific Applications and Edge Environments:

Sector-specific AI solutions are opening new commercial pathways in industries such as agriculture, logistics, mining, and pharmaceuticals. Companies are seeking AI models tailored to unique data environments, regulatory frameworks, and operational needs. Demand for edge AI is rising in remote and latency-sensitive applications, including autonomous vehicles, field robotics, and industrial automation. These use cases require compact, power-efficient models that operate without continuous cloud connectivity. The Global Artificial Intelligence Market is well-positioned to capture this opportunity by supporting custom model development, low-power chipsets, and on-device inference capabilities. It is enabling the transition from centralized AI deployments to decentralized intelligence across physical assets and field operations.

Emerging Markets and Public Sector Digital Transformation Initiatives:

Developing regions in Latin America, Southeast Asia, and the Middle East are investing in AI to support smart city development, healthcare access, and education reform. National AI strategies and cross-border technology partnerships are unlocking funding for pilot projects and infrastructure. Governments are adopting AI to improve service delivery, optimize public administration, and address socioeconomic gaps. These initiatives are driving adoption of AI platforms in public healthcare, traffic management, and digital identity systems. The Global Artificial Intelligence Market is gaining traction in these regions by aligning with digital transformation agendas and offering scalable, language-adaptable solutions. It is creating pathways for AI vendors to expand beyond mature economies.

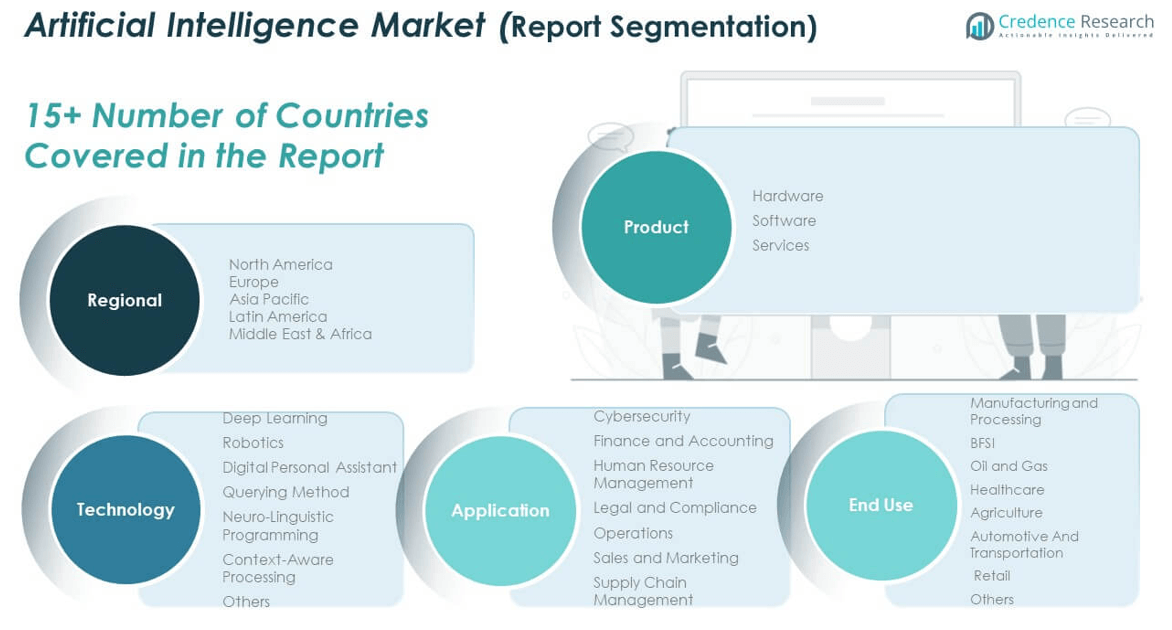

Market Segmentation Analysis:

By Product

The market is categorized into hardware, software, and services. Software accounts for the largest share, driven by widespread deployment of AI platforms, algorithms, and analytics tools across industries. Hardware demand is growing due to the adoption of GPUs, AI accelerators, and edge devices. Services are expanding steadily, including system integration, deployment, and support functions that assist enterprises in leveraging AI capabilities.

- For instance, NVIDIA’s global shipment of H100 GPUs since 2023 set a record in the high-performance AI hardware segment.

By Technology

Key technologies include deep learning, robotics, digital personal assistants, querying methods, neuro-linguistic programming (NLP), context-aware processing, and others. Deep learning leads the segment, enabling breakthroughs in computer vision, speech recognition, and autonomous systems. Robotics and NLP are gaining adoption in industrial automation and customer engagement. Other technologies, such as context-aware systems, are emerging in IoT and smart environments.

- For instance, Siemens deployed MindSphere IoT platform in factories worldwide by 2025, integrating context-aware AI to optimize energy and resource management in real time.

By Application

Application segments comprise cybersecurity, finance and accounting, human resource management, legal and compliance, operations, sales and marketing, and supply chain management. Cybersecurity dominates due to its role in real-time threat detection, behavioral analytics, and anomaly prediction. Sales and marketing applications are also rising with the use of AI for personalization, targeting, and customer insights.

By End Use

End-use sectors include manufacturing and processing, BFSI, oil and gas, healthcare, agriculture, automotive and transportation, retail, and others. Healthcare and BFSI are leading adopters, driven by needs in diagnostics, risk management, and fraud detection. The Global Artificial Intelligence Market continues to expand its footprint as adoption deepens across both mature and emerging industries.

Segmentation:

By Product

- Hardware

- Software

- Services

By Technology

- Deep Learning

- Robotics

- Digital Personal Assistant

- Querying Method

- Neuro-Linguistic Programming

- Context-Aware Processing

- Others

By Application

- Cybersecurity

- Finance and Accounting

- Human Resource Management

- Legal and Compliance

- Operations

- Sales and Marketing

- Supply Chain Management

By End Use

- Manufacturing and Processing

- BFSI

- Oil and Gas

- Healthcare

- Agriculture

- Automotive and Transportation

- Retail

- Others

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America

The North America Artificial Intelligence Market size was valued at USD 38.35 million in 2018 to USD 138.39 million in 2024 and is anticipated to reach USD 667.01 million by 2032, at a CAGR of 21.9% during the forecast period. The region holds the largest share in the Global Artificial Intelligence Market, accounting for 30% of the total revenue. This leadership stems from the presence of key technology firms, advanced digital infrastructure, and significant venture capital investments. The U.S. dominates in private AI funding and patent filings, supported by government-backed research initiatives and defense-related AI programs. Cloud service providers and AI chipset manufacturers continue to expand operations in this region. It remains the global hub for AI innovation, offering high scalability for enterprise solutions and foundational model development.

Europe

The Europe Artificial Intelligence Market size was valued at USD 30.71 million in 2018 to USD 118.53 million in 2024 and is anticipated to reach USD 625.25 million by 2032, at a CAGR of 23.2% during the forecast period. Europe contributes approximately 28% of the total share in the Global Artificial Intelligence Market, driven by a balanced focus on innovation and regulation. The European Commission’s AI Act and InvestAI initiative are shaping a responsible ecosystem with strong compliance mechanisms. Countries such as Germany, France, and the UK are investing in national AI strategies targeting healthcare, manufacturing, and smart infrastructure. Enterprises are adopting AI for compliance automation, cybersecurity, and green energy optimization. It shows growing demand for explainable and ethical AI across both public and private sectors.

Asia Pacific

The Asia Pacific Artificial Intelligence Market size was valued at USD 27.17 million in 2018 to USD 110.30 million in 2024 and is anticipated to reach USD 617.44 million by 2032, at a CAGR of 24.2% during the forecast period. Asia Pacific holds nearly 27% share in the Global Artificial Intelligence Market, emerging as the fastest-growing region. China and India are leading through heavy government investments, digital infrastructure expansion, and talent development. China’s AI strategy includes funding exceeding USD 100 billion, while India’s AI programs are driving growth in agriculture, healthtech, and fintech. The region is also strengthening its chip manufacturing ecosystem to reduce dependence on external supply chains. It offers strong market potential through localized language AI models and AI adoption in smart cities and public services.

Latin America

The Latin America Artificial Intelligence Market size was valued at USD 12.26 million in 2018 to USD 42.45 million in 2024 and is anticipated to reach USD 192.04 million by 2032, at a CAGR of 20.9% during the forecast period. Latin America accounts for around 6% share in the Global Artificial Intelligence Market, with Brazil and Mexico leading AI adoption. Governments are introducing AI policies aimed at improving public administration, healthcare access, and traffic systems. Regional startups are exploring AI for financial inclusion, agritech, and logistics optimization. Lack of advanced infrastructure and limited funding remain key challenges in this market. It is gradually gaining momentum as international firms invest in AI partnerships and training programs across the region.

Middle East

The Middle East Artificial Intelligence Market size was valued at USD 5.49 million in 2018 to USD 20.35 million in 2024 and is anticipated to reach USD 101.83 million by 2032, at a CAGR of 22.4% during the forecast period. The region holds close to 4% share of the Global Artificial Intelligence Market, supported by national visions and sovereign investment strategies. The UAE and Saudi Arabia are making rapid advancements through smart city projects, government automation, and AI-powered security systems. Public and private sector collaboration is funding AI research hubs and innovation centers. It is fostering demand for AI across oil and gas, retail, and public services. The region is positioning itself as a future-ready digital economy with strong AI adoption potential.

Africa

The Africa Artificial Intelligence Market size was valued at USD 3.65 million in 2018 to USD 10.29 million in 2024 and is anticipated to reach USD 29.48 million by 2032, at a CAGR of 13.9% during the forecast period. Africa contributes just over 1% to the Global Artificial Intelligence Market, yet presents growing interest in education, agriculture, and healthtech use cases. AI applications are helping address local challenges such as crop failure prediction, disease diagnosis, and school administration. Countries like South Africa, Nigeria, and Kenya are emerging as early adopters of AI through innovation hubs and international partnerships. Infrastructure limitations and skills gaps continue to restrict scale, but policy support is increasing. It has untapped potential where AI could serve inclusive growth and public development goals.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Google Inc.

- IBM Corporation

- Microsoft Corporation

- Nvidia Corporation

- Intel Corporation

- General Vision, Inc.

- Numenta, Inc.

- Sentient Technologies Holdings Ltd.

- Fingenius Limited

- Other Key Players

Competitive Analysis:

The Global Artificial Intelligence Market is highly competitive, driven by rapid innovation and strong investment across major technology firms and startups. Key players such as Google, Microsoft, IBM, Nvidia, and Intel dominate through extensive R&D, robust product portfolios, and cloud-based AI services. These companies continuously advance AI capabilities in language processing, computer vision, and edge computing. Emerging firms like Numenta and General Vision are introducing niche innovations in neuromorphic computing and cognitive frameworks. Strategic collaborations, acquisitions, and open-source contributions are common tactics to accelerate AI integration and expand market presence. Cloud infrastructure providers and chip manufacturers play a vital role in enabling scalable AI deployments across industries. It remains dynamic with frequent product updates, algorithm enhancements, and expansion into new sectors such as healthcare, automotive, and retail. The market favors players with strong computing infrastructure, access to large datasets, and capabilities to deliver industry-specific AI solutions.

Recent Developments:

- In July 2025, Google began rolling out an AI-powered business-calling feature across the United States, enabling its AI to autonomously call and interact with local businesses to gather real-time information about availability and pricing. This update is part of enhancements to Google Search’s AI Mode, which integrated the Gemini 2.5 Pro model for deeper, multimodal search capabilities and launched agentic AI features for both consumers and developers. Additional launches in June included Gemini CLI, an open-source AI agent for development, and Gemini 2.5 Flash-Lite, their fastest, most cost-effective large language model to date.

- In May 2025, IBM announced a major collaboration with Lumen Technologies to deploy IBM’s watsonx AI suite on Lumen’s Edge Cloud infrastructure. This initiative aims to deliver enterprise-grade AI inferencing at the edge, improving real-time data analysis for industries such as finance, retail, and manufacturing. The partnership is designed to minimize latency, enhance security, and allow clients to develop and deploy AI models closer to where data is generated. At IBM THINK 2025 in the same month, the company also revealed more than 150 pre-built AI agents within Watson Orchestrate, alongside a broadened Oracle partnership, reaffirming a transition from AI experimentation to large-scale integration.

- In May 2025, Microsoft introduced over 50 new enterprise AI tools—including next-generation Copilot updates and cloud-based agentic web solutions—at its annual Build and Inspire conferences. These tools are integrated across Bing, Office, Azure, and developer platforms, focusing on autonomous agent creation, workflow automation, cybersecurity enhancements, and advanced content generation. The company also opened a $2.9 billion AI data center in Wisconsin in April 2025, supporting 470 megawatts of AI computational capacity for large-scale supercomputing and next-generation AI services.

- In May 2025, Nvidia unveiled significant advancements in custom AI infrastructure and humanoid robotics at Computex Taipei. The company introduced the Isaac GR00T-Dreams platform for training industrial robots with large-scale, AI-generated synthetic environments. Nvidia also launched NVLink Fusion solutions, enabling customers to build semi-custom AI servers integrating the Grace CPU with third-party AI accelerators. Strategic deals were announced, including plans to deliver 100,000 processors to AI startups in Saudi Arabia over the next five years. CEO Jensen Huang outlined Nvidia’s “AI factory” vision for scalable, full-stack intelligence platforms and continued expansion of its AI hardware lineup.

Market Concentration & Characteristics:

The Global Artificial Intelligence Market exhibits moderate to high market concentration, with a few dominant players controlling a significant share of revenue and technological advancements. Companies such as Google, Microsoft, IBM, and Nvidia lead through extensive research capabilities, proprietary algorithms, and large-scale infrastructure. It features strong barriers to entry due to high capital requirements, specialized talent, and the need for access to vast datasets. The market is characterized by rapid innovation cycles, continuous product evolution, and strong emphasis on scalability and performance. Cloud computing, deep learning, and natural language processing define the core technological focus areas. It supports both horizontal and vertical AI solutions, offering applications across sectors including healthcare, BFSI, automotive, and manufacturing. Competitive differentiation depends on model accuracy, explainability, integration ease, and compliance with regional regulations.

Report Coverage:

The research report offers an in-depth analysis based on product, technology, application, and end use. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Demand for AI-driven automation will intensify across enterprise operations, driving investment in intelligent process optimization.

- Expansion of AI chipsets and edge computing will support real-time applications in autonomous systems and IoT networks.

- Generative AI models will reshape content creation, customer interaction, and decision-making processes across industries.

- Adoption of AI in healthcare will increase through advancements in diagnostics, treatment planning, and patient monitoring.

- BFSI will scale AI use for fraud detection, credit scoring, and personalized financial services.

- AI regulation and ethical frameworks will gain prominence, influencing model development and deployment practices.

- Cloud-based AI-as-a-Service offerings will lower entry barriers for SMEs and accelerate global adoption.

- Cross-industry collaboration will foster innovation in domain-specific AI tools and applications.

- Emerging economies will invest in AI talent and infrastructure to compete in the global digital economy.

- AI integration in supply chain and logistics will enhance predictive planning and operational efficiency.