Market Overview

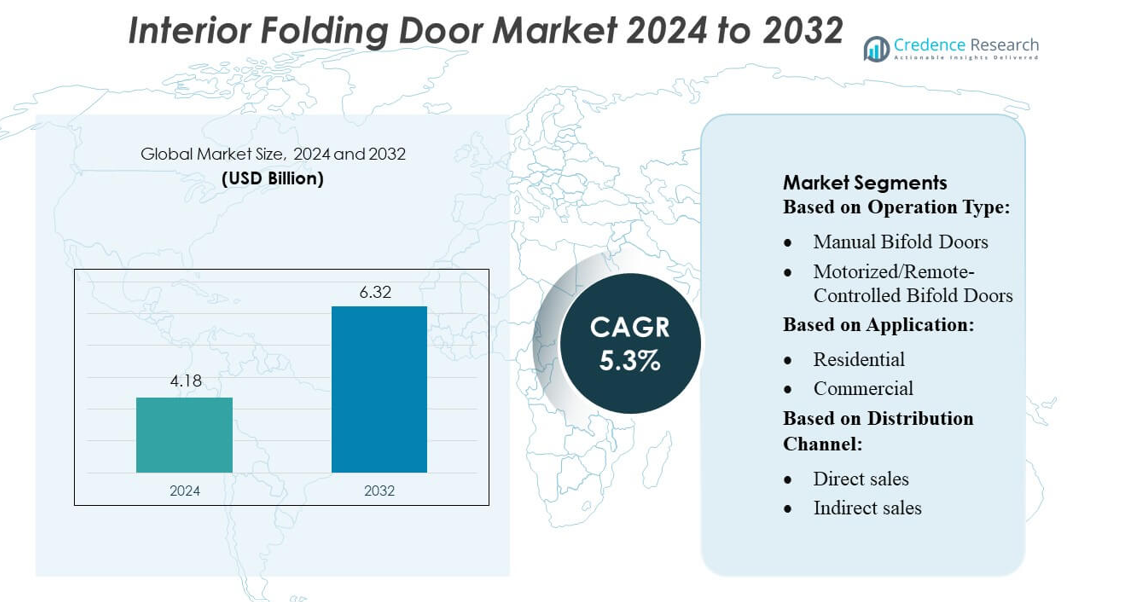

Interior Folding Door Market size was valued USD 4.18 billion in 2024 and is anticipated to reach USD 6.32 billion by 2032, at a CAGR of 5.3% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Interior Folding Door Market Size 2024 |

USD 4.18 billion |

| Interior Folding Door Market, CAGR |

5.3% |

| Interior Folding Door Market Size 2032 |

USD 6.32 billion |

The interior folding door market is driven by prominent global design and construction firms that influence product demand and adoption through large-scale residential, commercial, and hospitality projects. Key players actively shape the market by integrating innovative materials, advanced hardware systems, and customizable designs to meet evolving interior and space-efficiency requirements. Companies focus on delivering premium solutions with enhanced durability, aesthetic appeal, and operational convenience, including soft-close mechanisms and automated options. North America leads the market, accounting for approximately 32% of global share, supported by high renovation activity, preference for open-plan layouts, and strong collaboration between manufacturers and architects. The region’s emphasis on energy efficiency, modular interiors, and high-quality finishes further reinforces adoption, positioning North America as the most mature and influential market in the interior folding door landscape.

Market Insights

- The interior folding door market size was valued at USD 4.18 billion in 2024 and is projected to reach USD 6.32 billion by 2032, growing at a CAGR of 5.3% during the forecast period.

- Market growth is driven by large-scale residential, commercial, and hospitality projects, where design and construction firms integrate innovative materials, advanced hardware, and customizable folding-door solutions for enhanced space efficiency.

- Trends indicate rising adoption of automated and smart folding-door systems, modular designs, and sustainable materials to meet modern interior and energy-efficiency requirements.

- Competitive dynamics are shaped by manufacturers focusing on premium, durable, and aesthetically appealing solutions, with soft-close mechanisms and customized configurations differentiating products in mature and emerging markets.

- Regionally, North America leads with approximately 32% of global market share, followed by Europe and Asia-Pacific, while the residential segment dominates in demand, with commercial and hospitality applications steadily expanding as renovation and construction activities accelerate globally.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Operation Type:

In the interior folding door market, manual bifold doors hold the dominant share, driven by their cost-effectiveness, ease of installation, and broad suitability across residential and light-commercial spaces. Manufacturers emphasize improved hinge durability and lightweight aluminum or composite panels, enabling smoother operation and reduced long-term maintenance. While motorized or remote-controlled bifold doors are gaining traction with growing smart-home adoption, manual variants continue to lead due to their affordability, compatibility with diverse interior layouts, and lower infrastructure requirements, making them the preferred choice for most small- to medium-scale installations.

- For instance, one aluminum bifold door system widely used in the industry weighs about 65 % less than a comparable steel door, allowing for slimmer frame profiles and smoother operation with reduced load on hinges and tracks.

By Application:

The residential segment accounts for the largest share, supported by rising demand for space-saving door systems in apartments, modern homes, and renovation projects. Homeowners increasingly choose folding doors to create flexible partitions, enhance natural lighting, and optimize room functionality. Product innovations such as noise-dampening panels, slimline aluminum frames, and improved thermal sealing further strengthen adoption in living rooms, balconies, and wardrobe installations. Although commercial and industrial applications benefit from durability and wider openings, residential installations remain dominant due to higher replacement cycles and expanding interior design trends.

- For instance, CoreStation can handle up to 500,000 users and 1,000,000 fingerprint templates and operate within larger, scalable network topologies.CoreStation can store up to 1 million fingerprint templates.

By Distribution Channel:

Indirect sales—including dealers, distributors, and retail outlets—represent the dominant channel, as customers prefer in-store product evaluation, design consultation, and bundled installation services. This channel’s strong presence in urban and semi-urban markets ensures wider product availability and better brand visibility. Indirect distributors also support customization options and after-sales service coordination, reinforcing customer preference. While direct sales grow through online configurators and manufacturer-led project solutions, especially for commercial buyers, indirect sales remain the major contributor due to their extensive reach and established customer trust in physical showrooms.

Key Growth Drivers

Rising Demand for Space-Saving Architectural Solutions

The adoption of interior folding doors continues to increase as residential and commercial spaces prioritize flexible, space-efficient layouts. Urban housing constraints push developers to incorporate solutions that maximize usable area without compromising aesthetics. Interior folding systems offer seamless room transitions, enabling multifunctional environments such as convertible living–work zones. The growing popularity of compact homes, co-living spaces, and open-plan interiors further accelerates demand. Additionally, architects and interior designers increasingly specify folding doors to enhance natural light flow and improve spatial continuity, reinforcing their relevance in modern construction.

- For instance, Matrix Systems’ COSEC PATH RDFE V2 reader supports storage of 9,600 fingerprint templates with a 500 dpi optical sensor, and communicates via RS-232 and RS-485 in an IP65 enclosure.

Surge in Renovation and Home Improvement Activities

Growing consumer investment in home upgrades drives strong demand for folding doors, especially in markets where aging housing stock requires modernization. Homeowners favor folding systems for their ability to update interiors with minimal structural changes while improving ventilation and accessibility. The trend toward premium interior finishes also boosts adoption of high-quality wood, glass, and aluminum folding doors. E-commerce expansion and easy access to customized solutions further support growth, enabling consumers to explore various configurations, materials, and finishes that fit specific renovation goals.

- For instance, 3M Cogent’s MiY biometric access control reader processes authentication in 2.5 seconds per transaction (versus TWIC’s 3-second benchmark).

Advancements in Materials and Folding Mechanisms

Innovations in lightweight metals, engineered wood, composite materials, and durable hardware systems have significantly improved folding-door reliability, load-bearing capacity, and lifecycle performance. Enhanced track designs and smooth-glide mechanisms enable quieter, more stable operation, increasing preference among premium residential and commercial buyers. Manufacturers also integrate soft-close features, improved thermal insulation, and moisture-resistant panels to meet evolving performance standards. These innovations support broader adoption across humid regions, high-traffic environments, and modern smart-home settings, collectively driving growth in the interior folding-door market.

Key Trends & Opportunities

Growing Adoption of Smart and Automated Folding Systems

The expansion of smart-home ecosystems presents new opportunities for automated or sensor-controlled folding doors. Integration with home assistants, remote-operation systems, and app-based controls enables greater convenience and accessibility, particularly in premium residential and hospitality segments. Manufacturers are developing motorized mechanisms with improved safety features, silent operation, and energy-efficient components. As consumers increasingly seek intuitive interior solutions that complement connected-home environments, automated folding doors emerge as a high-value niche, offering substantial market growth potential.

- For instance, Bosch’s Building Integration System (BIS) underpins its access control and security offerings, with over 3,000 installations globally managing 10 million detectors across diverse facilities.

Expansion of Customizable and Modular Interior Solutions

Customization continues to shape market trends, with buyers demanding tailored folding doors that match interior themes and functional needs. Modular configurations, customizable panel widths, decorative glass inserts, and multiple finish options broaden design flexibility. This trend creates opportunities for manufacturers to introduce premium, bespoke collections that cater to varied consumer segments, from luxury residences to modern office environments. The ability to adapt folding-door systems for acoustic control, privacy enhancement, or aesthetic differentiation further strengthens their appeal in evolving architectural trends.

- For instance, Hitachi’s C-1 finger vein authentication unit verifies users by scanning three fingers from a contactless distance of approximately 20 mm. The authentication process, which occurs in seconds, enables fully contactless entry.

Sustainability-Driven Product Innovation

Growing emphasis on eco-friendly construction materials encourages manufacturers to develop folding doors made from recycled aluminum, sustainably sourced wood, and low-VOC finishes. Energy-efficient insulated panels and improved sealing systems help reduce indoor energy consumption, appealing to environmentally conscious consumers and green-building projects. This sustainability trend also aligns with regulatory shifts promoting responsible material use and carbon-footprint reduction. As green certifications gain prominence in residential and commercial developments, sustainable folding-door solutions present a significant opportunity for differentiation and market expansion.

Key Challenges

High Installation and Maintenance Complexity

Interior folding doors require precise installation to ensure smooth, long-term functionality. Misalignment or poor hardware integration can result in operational issues, creating hesitation among buyers seeking low-maintenance interior solutions. Skilled installation teams are essential, yet availability varies across regions, raising project costs and timelines. Additionally, commercial environments with heavy usage demand periodic maintenance to preserve door stability and panel integrity. These factors collectively pose a barrier to wider market penetration, particularly in cost-sensitive segments.

Price Sensitivity in Emerging Markets

While folding doors offer functional and aesthetic advantages, their higher initial cost compared with conventional hinged doors limits adoption in budget-driven markets. Premium materials, quality hardware, and customization options further elevate price points, restricting demand to mid- and high-end consumers. In many developing regions, limited awareness and preference for low-cost alternatives hinder market expansion. Manufacturers must balance affordability with performance to address this challenge, requiring optimized supply chains, localized production, and competitively priced product lines.

Regional Analysis

North America

North America holds a significant share of the interior folding door market, accounting for around 32% of global demand, driven by strong adoption in residential renovations and premium home-improvement projects. The region’s consumers prioritize aesthetic versatility, energy efficiency, and smooth-operating hardware systems, supporting rapid adoption of high-performance folding doors. Growing investments in multifamily housing, open-plan layouts, and flexible interior partitions further reinforce market expansion. Commercial sectors—particularly hospitality and office spaces—continue integrating glass and aluminum folding doors to optimize space utilization. The presence of established manufacturers and well-developed distribution networks strengthens North America’s dominant market position.

Europe

Europe represents approximately 28% of the global interior folding door market, supported by robust construction standards, strong preference for sustainable materials, and widespread adoption of modular interior designs. Demand is driven by renovation activities in Western Europe, where older residential structures undergo modernization through space-saving solutions like folding systems. The region’s emphasis on energy-efficient interiors accelerates the use of insulated panels and advanced hardware mechanisms. Commercial environments, including hotels, retail spaces, and coworking offices, increasingly incorporate premium glass folding doors to enhance natural lighting. Stringent environmental regulations also encourage the use of sustainably sourced wood and low-emission finishes across the market.

Asia-Pacific

Asia-Pacific commands about 30% of the interior folding door market, making it one of the fastest-growing regions due to rapid urbanization, rising middle-class incomes, and increased demand for compact living solutions. Housing developments in China, India, Japan, and Southeast Asia prioritize multifunctional layouts, boosting installations of folding doors in bedrooms, balconies, and partitioned living spaces. Commercial adoption grows in hospitality, retail, and modern office buildings seeking adaptable interiors. Local manufacturers benefit from lower production costs, enabling competitive pricing and wider adoption. Infrastructure growth and expanding real estate investments contribute significantly to APAC’s accelerating market share and long-term growth trajectory.

Latin America

Latin America accounts for around 6% of the global market, with moderate but steadily rising adoption of interior folding doors across residential and commercial segments. Urban centers in Brazil, Mexico, Chile, and Colombia increasingly incorporate folding systems to enhance space efficiency in compact homes and apartments. The region’s growing hospitality and retail sectors also adopt glass and aluminum folding doors to improve interior aesthetics and natural light flow. However, price sensitivity and limited availability of premium products slow widespread adoption. As regional distributors expand product accessibility and renovation activity increases, demand is expected to strengthen progressively.

Middle East & Africa (MEA)

The Middle East & Africa region captures approximately 4% of the global interior folding door market, with demand concentrated in urban and high-income areas. Growth is driven by premium residential developments, luxury hotels, and commercial buildings adopting high-end folding solutions for spacious and visually appealing interiors. Gulf countries such as the UAE and Saudi Arabia lead adoption, supported by strong construction pipelines and rising preferences for glass and aluminum folding systems. However, broader market penetration remains limited in Africa due to affordability challenges and slower modernization of residential properties. Increasing investments in commercial infrastructure are gradually supporting MEA’s market presence.

Market Segmentations:

By Operation Type:

- Manual Bifold Doors

- Motorized/Remote-Controlled Bifold Doors

By Application:

By Distribution Channel:

- Direct sales

- Indirect sales

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The interior folding door market features a competitive landscape shaped by leading global design and engineering firms such as Hirsch Bedner Associates, Areen Design Services Ltd, Cannon Design, Perkins and Will, NELSON & Associates Interior Design and Space Planning Inc., IA Interior Architects, Gensler, Stantec Inc., Aecom, and Jacobs Engineering Group Inc. The interior folding door market is shaped by continuous innovation in materials, hardware mechanisms, and design flexibility as manufacturers compete to meet evolving architectural and residential requirements. Companies increasingly focus on developing lightweight, durable, and aesthetically versatile door systems that support modern open-plan layouts and multifunctional spaces. Market competition also intensifies through advancements in soft-close mechanisms, insulated panels, and moisture-resistant finishes that enhance performance across residential and commercial applications. Customization has become a major differentiator, prompting brands to expand offerings in glass, wood, aluminum, and composite configurations. Additionally, sustainability expectations and smart-home integration trends drive manufacturers to introduce eco-friendly materials and automated, app-controlled folding systems. As distributors broaden global reach and renovation activity rises, competitive positioning strengthens around product reliability, design adaptability, and premium interior experiences.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Hirsch Bedner Associates

- Areen Design Services Ltd

- Cannon Design

- Perkins and Will

- NELSON & Associates Interior Design and Space Planning Inc.

- IA Interior Architects

- Gensler

- Stantec Inc.

- Aecom

- Jacobs Engineering Group Inc.

Recent Developments

- In June 2024, NanaWall Systems launched folding glass walls designed and manufactured specifically for mid and high-rise buildings with higher windload and deflection requirements. This will ideally open new market segments for NanaWall, addressing the unique structural considerations for urban vertical construction and increase their product application versatility.

- In May 2024, Remax Furnitures, an Indian luxury furniture brand, launched a new flagship store in New Delhi, India, to expand its retail footprint. The store offers a curated selection of premium furniture and customized interior design services, providing an immersive experience for customers to explore different home decor possibilities.

- In February 2024, Origin launched the Soho External Door (product code OB-36+), an aluminum bi-fold system with a slim profile and 36mm sightlines that complies with the Future Homes Standard 2025, a year ahead of the new building regulations requiring it.

- In February 2024, U.S.-based interior design company Havenly acquired The Citizenry, a direct-to-consumer home decor brand known for ethically crafted products. This acquisition was part of Havenly’s strategy to expand its product portfolio and consolidate its position in the home decor market

Report Coverage

The research report offers an in-depth analysis based on Operation Type, Application, Distribution Channel and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market is expected to grow steadily due to increasing urbanization and space-constrained housing.

- Rising demand for multifunctional and flexible interiors will drive adoption of folding doors.

- Integration of smart-home technology will create opportunities for automated and remote-controlled systems.

- Sustainable and eco-friendly materials will gain prominence in product development.

- Customization and modular designs will continue to attract premium residential and commercial buyers.

- Renovation and home improvement activities will contribute significantly to market expansion.

- Advanced hardware mechanisms and soft-close features will enhance product appeal.

- Expansion in hospitality, retail, and office sectors will fuel commercial segment demand.

- E-commerce and online distribution channels will improve accessibility and consumer reach.

- Emerging markets will show strong growth potential as awareness and affordability increase.