Market Overview

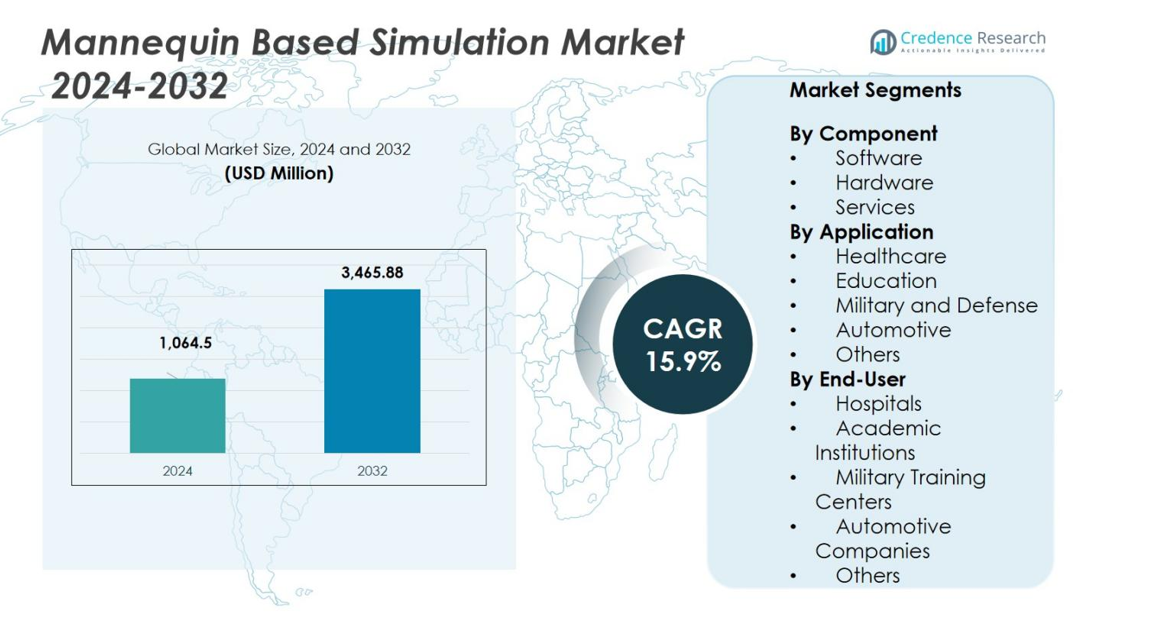

The Mannequin Based Simulation Market size was valued at USD 1,064.5 Million in 2024 and is anticipated to reach USD 3,465.88 Million by 2032, at a CAGR of 15.9% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Mannequin Based Simulation Market Size 2024 |

USD 1,064.5 Million |

| Mannequin Based Simulation Market, CAGR |

15.9% |

| Mannequin Based Simulation Market Size 2032 |

USD 3,465.88 Million |

The Mannequin Based Simulation Market features leading players such as Laerdal Medical, CAE Healthcare, Gaumard Scientific, Limbs & Things, 3B Scientific, Simulaids, Kyoto Kagaku, Mentice AB, Surgical Science Sweden AB and Operative Experience Inc.. These companies invest heavily in R&D to deliver high‑fidelity mannequins, integrated simulation software and comprehensive service offerings. The market is geographically led by the North America region, which held 35% market share in 2024 due to advanced healthcare infrastructure and strong training ecosystem. Urban centres across this region continue to adopt and scale simulation‑based training, reinforcing industry lead and providing a launch pad for global expansion.

Market Insights

- The Mannequin Based Simulation Market was valued at USD 1,064.5 Million in 2024 and is anticipated to reach USD 3,465.88 Million by 2032, registering a CAGR of 15.9 % during the forecast period.

- The Hardware segment held a dominant share of 55 % in 2024, supported by strong demand for high‑fidelity mannequins in healthcare and training settings.

- Integration of artificial intelligence and virtual reality into mannequin‑based systems is emerging as a key trend, creating enhanced training experiences across healthcare, military, and education verticals.

- Market growth faces restraints such as high initial investment costs and complexities in integrating advanced simulation systems into existing training infrastructures.

- Regionally, North America led the market with a 35 % share in 2024, followed by Europe at 25 % and Asia Pacific at 20 %, driven by advanced healthcare systems and robust defense training programs.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Component

In the Mannequin-Based Simulation Market, the Hardware segment holds the dominant share, accounting for 55% in 2024. Hardware-based simulators, including mannequins and associated equipment, are the primary focus of this market segment, driven by the increasing demand for realistic training environments across various sectors. The high adoption rates in healthcare training, where lifelike simulation is crucial, fuel the growth of the hardware segment. The Software segment follows closely with significant growth potential due to the increasing demand for advanced simulation software that enhances realism and user experience in various training applications.

- For instance, the Software segment is gaining traction with innovations like CAE Healthcare’s AI-powered simulation software developed to elevate training interactivity and adaptiveness, complementing the hardware with enhanced user experience and realism.

By Application

The Healthcare application segment is the largest, commanding a share of 45% in the Mannequin-Based Simulation Market in 2024. The increasing focus on medical training, patient safety, and the rising need for skill development in healthcare professionals, particularly for critical care and emergency procedures, are key growth drivers. Education follows with a growing share, as academic institutions adopt mannequin-based simulations to improve hands-on learning experiences. The Military and Defense segment is also gaining traction due to the rising use of simulation technologies for tactical and emergency training, contributing to the segment’s growth.

- For instance, MedVision’s manikins like Leonardo enable healthcare professionals to practice routine and emergency medical procedures, enhancing their skills in a risk-free environment.

By End-User

The Hospitals segment is the dominant end-user category in the mannequin-based simulation market, representing 38% of the market share in 2024. This is driven by the need for hospitals to ensure that healthcare professionals receive high-quality, hands-on training to handle real-world emergencies. The Academic Institutions segment also holds a significant share of about 32%, driven by the increasing adoption of simulation-based learning in medical and engineering courses. Military Training Centers follow with a growing share due to the rising demand for tactical training solutions that enhance combat readiness through realistic simulation technologies.

Key Growth Drivers

Rising Demand for Healthcare Training

The growing need for advanced healthcare training is a major driver for the mannequin-based simulation market. As medical professionals increasingly rely on simulation technology to hone their skills without risk to patients, the demand for high-quality, realistic mannequins continues to rise. This is particularly crucial for emergency medicine, surgery, and other high-stakes environments. Healthcare institutions are incorporating mannequins into their training programs to enhance skill development, reduce medical errors, and improve patient outcomes, contributing significantly to the market’s expansion.

- For instance, Laerdal Medical’s SimMan 3G PLUS offers immersive emergency care training with realistic patient handling, interchangeable face skins, and the ability to practice with real clinical devices, enhancing decision-making and teamwork skills in high-stress scenarios.

Technological Advancements in Simulation

Advancements in simulation technology, such as AI, VR, and haptic feedback, are propelling the growth of the mannequin-based simulation market. These technologies enhance realism and interaction, making training experiences more immersive and effective. The integration of software that mimics real-world scenarios allows trainees to engage in realistic, high-pressure situations. This innovation improves learning outcomes and drives the adoption of advanced simulation systems across sectors like healthcare, military, and automotive, further accelerating market growth.

- For instance, 3D Systems has introduced the Touch and Touch X haptic devices, delivering force-feedback technology that allows users to feel virtual objects, enhancing tactile realism for surgical training and design workflows.

Increasing Adoption in Military and Defense

The mannequin-based simulation market is witnessing robust growth in the military and defense sectors. Realistic training environments using mannequins enable military personnel to practice in scenarios that simulate combat situations, disaster response, and tactical operations. As governments and defense organizations focus on enhancing training quality and reducing operational risks, the demand for mannequin-based simulation systems in military and defense applications continues to rise. This adoption is bolstered by the need for cost-effective and safe training solutions for personnel in critical roles.

Key Trends & Opportunities

Integration of Artificial Intelligence and Virtual Reality

The integration of artificial intelligence (AI) and virtual reality (VR) in mannequin-based simulation systems is a key trend that offers significant opportunities for the market. AI enables adaptive learning systems that tailor scenarios based on individual performance, enhancing the training experience. Virtual reality further immerses trainees, allowing them to interact with their environment in a virtual space. These technologies improve the realism and efficiency of training, creating opportunities for manufacturers to innovate and provide advanced solutions that cater to various industries like healthcare, military, and education.

- For instance, Boeing has utilized AR-assisted assembly instructions in manufacturing training that reduced production time by 25% and error rates by 40%, highlighting AI and VR’s role in industrial skills training by providing personalized, interactive guidance and feedback.

Growth in Emerging Markets

Emerging markets, particularly in Asia-Pacific, are presenting lucrative opportunities for the mannequin-based simulation market. The growing demand for advanced training solutions in developing economies, coupled with increasing investments in education and healthcare infrastructure, drives market expansion in these regions. As these markets witness improvements in medical training and defense capabilities, there is a surge in the adoption of simulation systems. The expansion of global healthcare standards and military modernization further supports the uptake of mannequin-based simulation technologies in these regions.

- For instance, Laerdal Medical A/S has reported rising adoption of their patient simulators in developing countries to enhance medical training and patient safety.

Key Challenges

High Initial Investment Costs

A key challenge faced by the mannequin-based simulation market is the high initial investment required for advanced simulation systems. The cost of acquiring high-quality mannequins, along with the integration of sophisticated software and hardware, can be prohibitive for some institutions, particularly in developing regions. This financial barrier limits the adoption of mannequin-based training solutions, especially among smaller organizations or those with constrained budgets, hindering the market’s potential growth.

Complexity in System Integration

The complexity involved in integrating mannequin-based simulation systems with existing training programs presents a significant challenge. Many organizations struggle to seamlessly incorporate new technology into their established training processes, particularly in healthcare and military settings. Ensuring compatibility between simulation equipment, software, and existing training infrastructure requires substantial technical expertise and resources, which can slow the pace of adoption. This challenge necessitates ongoing research and development to streamline system integration and reduce implementation barriers.

Regional Analysis

North America

The North America region held a market share of 35% in the mannequin‑based simulation market in 2024. The adoption is strong due to its advanced healthcare infrastructure, established training centres, and significant defence spending that require high‑fidelity simulation systems. The presence of major players and continuous innovations in simulation hardware and software further bolster this dominance. Hospitals and academic institutions in the US and Canada increasingly incorporate mannequin‑based systems to improve clinical competency and patient safety. With rising demand for minimally invasive procedures and high‑stakes training environments, the North America region continues to drive market growth.

Europe

Europe accounted for a market share of 25% in the mannequin‑based simulation market in 2024. Countries such as Germany, the UK and France show significant uptake of training simulations in both healthcare and military sectors. The region benefits from well‑regulated medical education frameworks and strong investments in simulation training technologies. European institutions prioritise patient safety and surgical skill development, which strengthens the demand for high‑fidelity mannequins and accompanying systems. Emerging regulatory mandates and partnerships between simulation vendors and academic/training centres are further advancing market penetration across Europe.

Asia Pacific

The Asia Pacific region represented 20% of the mannequin‑based simulation market in 2024. Rapid expansion of healthcare infrastructures, rising training standards and growing defence budgets in countries such as China, India and Japan are key growth drivers. The region is witnessing accelerated adoption of simulation solutions to enhance clinical training and operational readiness in military and emergency response settings. Furthermore, lower cost of labour and increasing number of training centres are enabling broader use of mannequin‑based systems across both public and private sectors, positioning Asia Pacific as a fast‑growing region in the forecast period.

Latin America

Latin America held an estimated share of 10% of the mannequin‑based simulation market in 2024. While adoption levels are lower compared with developed regions, increasing investments in healthcare education, simulation training programmes within military units, and the expansion of private sector training centres are beginning to contribute to growth. Economic constraints and budget challenges remain barriers, yet governments in Brazil and Mexico are gradually prioritising training infrastructures to reduce clinical error rates and improve patient outcomes, which supports future market opportunities in Latin America.

Middle East & Africa

The Middle East & Africa (MEA) region accounted for the remaining 10% of the global mannequin‑based simulation market in 2024. Growth is driven by increasing military and defence training expenditures, the development of simulation‑based healthcare education in GCC countries, and the rising presence of international medical training providers. Despite the growth potential, challenges such as limited local manufacturing capacity, infrastructure gaps and budgetary constraints restrict faster uptake. However, initiatives focusing on building simulation centres and enhancing training quality for healthcare and defence personnel point to improved prospects for MEA over the forecast period.

Market Segmentations:

By Component

- Software

- Hardware

- Services

By Application

- Healthcare

- Education

- Military and Defense

- Automotive

- Others

By End-User

- Hospitals

- Academic Institutions

- Military Training Centers

- Automotive Companies

- Others

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The competitive landscape in the mannequin‑based simulation market features major key players such as Laerdal Medical, CAE Healthcare, Gaumard Scientific, Limbs & Things, 3B Scientific, Simulaids, Kyoto Kagaku, Mentice AB, Surgical Science Sweden AB and Operative Experience Inc.. These firms actively pursue differentiation through product innovation, partnerships, and geographic expansion to capture market share. They deploy extensive R&D to enhance fidelity in hardware and simulation software, leveraging digital integration such as AI and VR. Many also form strategic alliances with healthcare institutions and defense organizations to broaden training solutions. Market consolidation and mergers add further intensity, raising barriers for smaller entrants. As a result, competitive rivalry remains moderate‑to‑high, with companies striving to maintain leadership by expanding application scopes and improving service offerings.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Mentice AB

- Gaumard Scientific

- Limbs & Things

- Surgical Science Sweden AB

- 3B Scientific

- Operative Experience Inc.

- Kyoto Kagaku

- CAE Healthcare

- Laerdal Medical

- Simulaids

Recent Developments

- In January 2024, Laerdal also unveiled its new obstetric simulator, “MamaAnne™”, developed in collaboration with Limms & Things, designed to train maternal‑health teams on labour, delivery, and emergency scenarios.

- In March 2024, IngMar Medical launched Aurora, a medical simulation manikin used to train clinicians in all forms of ventilation, featuring an innovative Internal Simulated Lung (ISL) based on IngMar’s ASL 5000 Breathing Simulator technology with tetherless, internal system integration.

- In December 2024, Fujifilm India launched the innovative Mikoto Colon Model, a cutting-edge endoscopy simulation technology combining advanced sensor technology with artificial intelligence, featuring four difficulty levels for self-paced learning among practitioners of varying expertise.

Report Coverage

The research report offers an in-depth analysis based on Component, Application, End User and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will expand as more training programmes embed high‑fidelity mannequins into standard curricula across healthcare and defence sectors.

- Artificial intelligence and virtual‑reality integration will enable personalised simulation scenarios, boosting training effectiveness and driving demand.

- Emerging economies will account for increasing volume growth as government policies support simulation‑based education and defence training infrastructure builds out.

- The shift toward competency‑based education will elevate demand for mannequins that simulate complex clinical events, enhancing experiential learning outcomes.

- Cross‑industry adoption, including automotive and industrial safety training, will open new vertical applications beyond healthcare and military.

- Service‑and‑maintenance models will expand, enabling vendors to offer full‑lifecycle support and recurring revenue streams tied to simulation hardware.

- Modular and scalable mannequin systems will gain traction as institutions seek cost‑effective upgrades rather than full‑system replacements.

- Partnerships between simulation vendors and academic/clinical centres will accelerate product validation and generate site‑specific use‑cases driving uptake.

- Standardisation and certification requirements for simulation training by regulatory bodies will elevate baseline demand for certified mannequin‑based solutions.

- Consolidation through mergers and acquisitions will accelerate, with larger players acquiring niche specialists to broaden functionality and strengthen global distribution.