| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Video Games Market Size 2024 |

USD 179.39 billion |

| Video Games Market, CAGR |

10.57% |

| Video Games Market Size 2032 |

USD 406.16 billion |

Market Overview

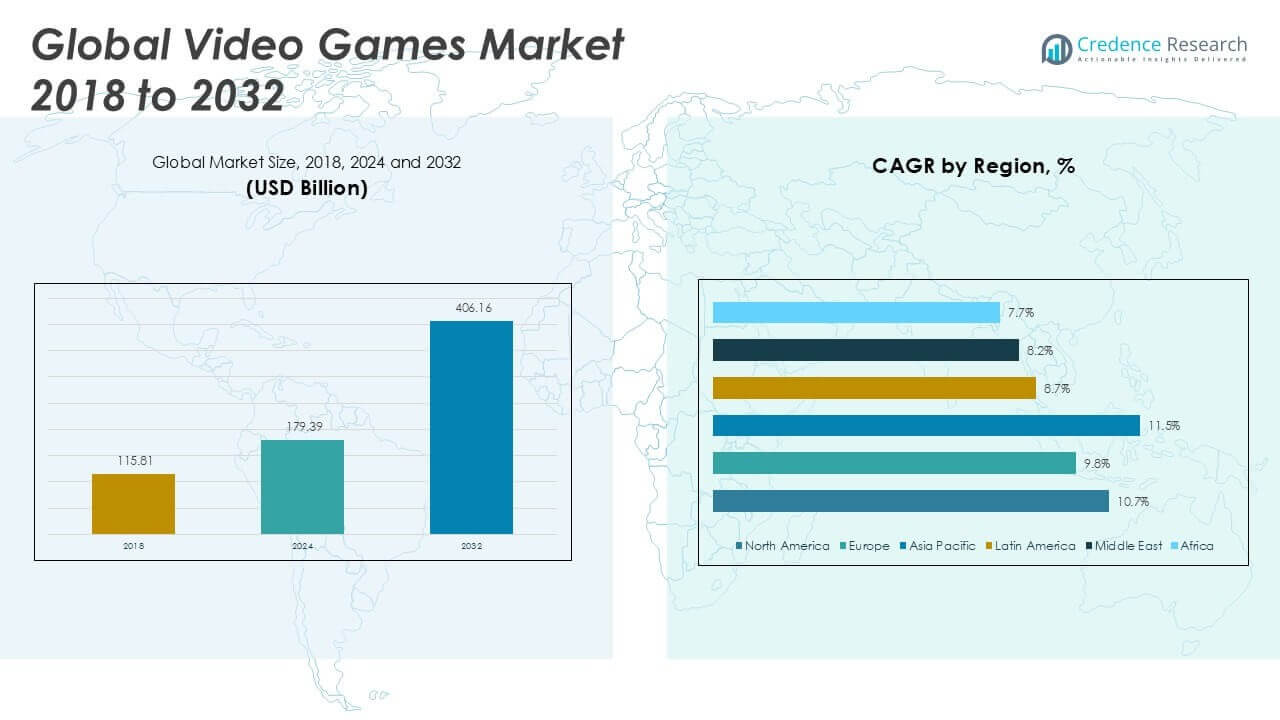

The Video Games Market size was valued at USD 115.81 billion in 2018 to USD 179.39 billion in 2024 and is anticipated to reach USD 406.16 billion by 2032, at a CAGR of 10.75% during the forecast period.

The Video Games Market is driven by rapid advancements in gaming technology, expanding internet penetration, and the proliferation of smartphones and high-performance gaming consoles, which collectively enhance user experiences and accessibility. Growing demand for immersive gameplay, including augmented reality (AR) and virtual reality (VR), fuels innovation and broadens the market’s appeal across diverse age groups. The rise of eSports, game streaming, and social gaming platforms encourages community engagement and monetization opportunities, attracting investment from both developers and advertisers. Cloud gaming services, digital distribution, and subscription-based models further reshape industry dynamics, enabling flexible access to a wide range of titles. Additionally, the increasing popularity of mobile games and cross-platform compatibility supports market expansion. Regulatory changes, digital payment integration, and heightened focus on data security continue to influence market strategies, ensuring that the Video Games Market remains vibrant, competitive, and responsive to evolving consumer preferences and technological trends.

The Video Games Market demonstrates strong geographical diversity, with North America, Asia Pacific, and Europe serving as major hubs for both consumption and innovation. North America remains a leader in console and PC gaming, supported by advanced infrastructure and a high concentration of prominent game developers. Asia Pacific, particularly China, Japan, and South Korea, stands out for its dominance in mobile gaming and the rapid growth of eSports communities, driven by a tech-savvy population and high smartphone penetration. Europe showcases a balanced demand across platforms and benefits from a thriving independent game development scene. Key players such as Tencent, Sony, and Nintendo continue to shape global market dynamics through expansive product portfolios, investment in new technologies, and strategic partnerships. These companies maintain competitive strength by adapting to evolving consumer preferences and exploring new monetization opportunities across regions.

Market Insights

Market Insights

- The Video Games Market was valued at USD 179.39 billion in 2024 and is projected to reach USD 406.16 billion by 2032, registering a CAGR of 10.75% during the forecast period.

- Advancements in gaming technology, widespread internet access, and the popularity of smartphones and consoles are key drivers fueling steady market growth.

- Trends such as the rise of cloud gaming, cross-platform play, augmented reality (AR), and virtual reality (VR) experiences are reshaping how consumers interact with games.

- Leading companies, including Tencent, Sony, and Nintendo, actively expand their product portfolios and invest in partnerships to capture new audiences and retain competitive advantage.

- The market faces restraints from intense competition, market saturation, regulatory complexities, and growing concerns around data privacy and user security.

- North America, Asia Pacific, and Europe dominate the Video Games Market, each offering unique strengths—North America leads in console and PC gaming, while Asia Pacific excels in mobile gaming and eSports.

- Strategic adoption of new monetization models, the evolution of subscription services, and regional consumer preferences continue to shape the market landscape and support sustained growth.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Technological Advancements and Platform Diversity

Technological innovation serves as a primary driver of the Video Games Market, enabling superior graphics, faster processing speeds, and more immersive gameplay experiences. Developers leverage advancements in artificial intelligence, real-time rendering, and cloud infrastructure to deliver dynamic and engaging content that attracts a broad user base. The expansion of gaming platforms, from high-performance consoles and PCs to smartphones and tablets, supports a wider demographic and boosts market reach. It adapts to evolving consumer demands by offering games that are compatible across multiple devices, creating seamless gaming experiences. Integration of augmented reality (AR) and virtual reality (VR) further elevates user engagement, while continuous hardware improvements keep pace with rising expectations. The trend toward platform diversity ensures sustained interest and encourages repeat purchases.

- For instance, the Game Developers Conference’s 2025 State of the Game Industry report highlights the growing appeal of PC gaming and the cautious adoption of AI tools in game development.

Rising Internet Penetration and Social Connectivity

Global expansion of high-speed internet access fuels the Video Games Market by enabling online multiplayer features, digital downloads, and live streaming. Players increasingly seek interactive and socially connected experiences, participating in online communities and engaging in collaborative gameplay. The popularity of eSports and game streaming platforms, such as Twitch and YouTube Gaming, fosters community building and encourages ongoing player involvement. Digital distribution channels reduce barriers to entry for both users and developers, facilitating broader access to a wide array of games. Social media integration amplifies reach, helping developers promote new titles and updates in real time. This digital ecosystem strengthens network effects and supports user retention.

- For instance, India has established itself as a global leader in internet affordability, with data costs averaging just USD 0.26 per gigabyte, significantly lower than in the United Kingdom (USD 6.66) and the United States (USD 12.37).

Evolving Monetization Models and Revenue Streams

The Video Games Market benefits from diverse monetization strategies, including free-to-play models, in-game purchases, subscriptions, and advertising. Developers create flexible payment options, allowing players to access content in ways that fit their preferences and budgets. Microtransactions and battle passes enhance revenue potential, while downloadable content (DLC) and seasonal updates encourage long-term engagement. Subscription-based services, such as Xbox Game Pass and PlayStation Now, provide access to extensive game libraries and drive recurring revenue. It supports a sustainable business environment by diversifying income streams and reducing reliance on single-title sales. The emergence of cloud gaming platforms also creates new opportunities for market growth.

Regulatory Environment and Data Security Considerations

The evolving regulatory landscape and growing concerns over data privacy shape the operational strategies within the Video Games Market. Governments implement policies on digital payments, content rating, and consumer protection to safeguard players and foster responsible gaming. Developers respond by enhancing cybersecurity measures and integrating robust parental controls, building trust among users and stakeholders. The rise of digital transactions increases focus on secure payment processing and fraud prevention. It navigates compliance requirements by adopting transparent practices and staying abreast of legal changes worldwide. Maintaining regulatory compliance and prioritizing user safety remains critical for sustainable growth and brand reputation.

Market Trends

Growth of Cloud Gaming and Subscription Services

Cloud gaming continues to reshape the Video Games Market by providing instant access to a vast library of titles without the need for high-end hardware. It leverages robust internet infrastructure and advanced streaming technology to deliver seamless gameplay across various devices. Subscription-based models, such as Xbox Game Pass and PlayStation Plus, attract a growing audience by offering value and convenience through all-inclusive packages. This trend reduces barriers to entry and expands the market to casual players who prefer flexible access over outright ownership. Developers and publishers optimize their offerings to suit evolving user preferences and keep players engaged over the long term. The adoption of cloud platforms also streamlines content updates and supports scalable distribution.

- For instance, cloud gaming services are projected to reach significant revenue milestones, driven by advancements in streaming technology and increased accessibility.

Integration of Augmented and Virtual Reality Experiences

The integration of augmented reality (AR) and virtual reality (VR) technologies defines a major trend within the Video Games Market, driving innovation and user engagement. Developers design highly immersive environments that appeal to both hardcore gamers and new entrants. Advances in AR and VR hardware enhance comfort, visual fidelity, and interactivity, making these technologies more accessible and appealing. It taps into the demand for novel experiences by offering games that blur the line between digital and physical worlds. Partnerships with technology companies accelerate content creation and expand the ecosystem. The trend toward experiential gaming strengthens market positioning and attracts fresh investment.

- For instance, the consumer VR market is expected to grow significantly, with businesses leveraging VR for customer experience, remote collaboration, and training.

Expansion of Social and Competitive Gaming Ecosystems

The Video Games Market witness robust growth in social and competitive gaming, supported by the rise of eSports, multiplayer formats, and in-game communication tools. Platforms foster active communities where players interact, collaborate, and compete on a global scale. It benefits from sponsorships, advertising, and media rights, transforming eSports into a mainstream entertainment segment. Social gaming features encourage repeat play and deepen user loyalty. Developers prioritize user-generated content, customizations, and cross-platform functionality to keep communities vibrant. This ecosystem supports ongoing innovation and helps sustain long-term market momentum.

Rise of Mobile and Cross-Platform Gaming

Mobile gaming and cross-platform compatibility represent significant trends in the Video Games Market, broadening access and enhancing player convenience. The ubiquity of smartphones and tablets accelerates market penetration, while advances in mobile hardware enable sophisticated gameplay experiences. Cross-platform functionality allows users to play seamlessly across devices, increasing retention and expanding user bases. It empowers developers to reach wider audiences and tailor content to diverse preferences. Partnerships with telecom providers and device manufacturers support market entry strategies. The convergence of mobile and traditional gaming ecosystems underpins strong growth prospects for the years ahead.

Market Challenges Analysis

Regulatory Uncertainty and Security Risks

Regulatory uncertainty and security risks shape the strategic environment for the Video Games Market, as governments worldwide enforce evolving policies on data protection, microtransactions, and content standards. It faces increasing scrutiny regarding user privacy, cybersecurity, and responsible gaming practices. Compliance with diverse regional regulations requires agile adaptation and significant investment in legal resources. Security breaches, account hacks, and online harassment create negative publicity and erode user trust. The rise of digital payment systems and virtual economies intensifies the need for secure transactions and robust fraud prevention measures. Navigating these challenges is essential for safeguarding brand reputation and fostering sustainable growth.

- For instance, India’s online gaming industry faces increasing scrutiny, with concerns over addiction, financial fraud, and privacy prompting calls for stricter regulations.

Intense Competition and Market Saturation

Intense competition and market saturation present major challenges for the Video Games Market, as a growing number of developers and publishers enter the industry with similar products. It must contend with high user expectations and rapid innovation cycles, which demand continual investment in technology, content, and marketing. The sheer volume of new releases creates discovery issues for smaller studios and independent creators, who struggle to gain visibility amid established franchises. Pricing pressures and frequent discounts impact profitability, forcing companies to explore alternative monetization models. Successful differentiation through unique gameplay, narrative, or technology becomes critical for sustained relevance. Maintaining player engagement and loyalty remains a significant hurdle amid an abundance of choices.

Market Opportunities

Emergence of New Technologies and Untapped Demographics

The Video Games Market presents significant opportunities through the adoption of emerging technologies such as artificial intelligence, blockchain, and advanced cloud gaming platforms. Developers can leverage AI to enhance personalization, dynamic storytelling, and in-game decision-making, elevating user engagement. Blockchain technology supports the creation of unique digital assets and secure transactions, fostering new monetization models and digital ownership. The rise of mobile gaming and affordable AR/VR hardware expands the addressable market, reaching untapped demographics in developing regions. It supports inclusive and diverse gaming experiences, appealing to a broader spectrum of age groups and interests. Companies that innovate with these technologies can capture early-mover advantages and unlock new revenue streams.

Expansion through Cross-Industry Collaboration and Evolving Business Models

Collaborations with sectors such as entertainment, sports, and education open new growth avenues for the Video Games Market by enabling transmedia storytelling, branded content, and interactive learning experiences. Strategic partnerships with telecom providers and hardware manufacturers support wider distribution and improved user accessibility. The market benefits from the evolution of business models, such as subscription-based services, free-to-play formats, and in-game advertising, which drive recurring revenue and foster sustained user engagement. It can tap into global events, eSports tournaments, and influencer marketing to amplify brand exposure and community engagement. Companies that embrace flexible strategies and cross-industry alliances can secure a strong competitive position in a rapidly evolving landscape.

Market Segmentation Analysis:

By Type:

By type, mobile gaming commands a significant share due to the widespread adoption of smartphones and the ease of access to app-based titles. Console gaming maintains strong appeal through exclusive titles and immersive experiences enabled by high-performance hardware, while PC gaming attracts a dedicated user base with customization options and advanced graphics capabilities.

By Gaming Type:

The market differentiates itself further by gaming type, with online gaming experiencing rapid expansion supported by multiplayer functionality, social connectivity, and cloud-based content. Offline gaming continues to hold relevance for users seeking traditional, uninterrupted play or those with limited internet access.

By Revenue Model:

Revenue models further shape the competitive landscape. In-game purchases dominate, driven by the popularity of microtransactions, cosmetic upgrades, and downloadable content, allowing developers to generate continuous income streams. Subscription services grow steadily, offering players extensive libraries of titles and regular updates for a fixed fee, which encourages long-term engagement. Ad-supported models emerge as an accessible option, particularly within mobile gaming, enabling free access to games while providing revenue opportunities through integrated advertising. The Video Games Market leverages this segmented approach to address evolving consumer demands, maximize reach, and foster sustainable growth across all user segments.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Segments:

Based on Type:

- Mobile Gaming

- Console Gaming

- PC Gaming

Based on Gaming Type:

- Online Gaming

- Offline Gaming

Based on Revenue Model:

- In-Game Purchases

- Subscriptions

- Ad-Supported Models

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America Video Games Market

North America Video Games Market grew from USD 26.07 billion in 2018 to USD 39.58 billion in 2024 and is projected to reach USD 90.09 billion by 2032, reflecting a compound annual growth rate (CAGR) of 10.7%. North America holds a 22% market share, led by the United States and Canada, where high consumer spending and advanced digital infrastructure drive adoption of new gaming platforms. The region benefits from a strong ecosystem of developers, publishers, and eSports organizations. High penetration of consoles, increasing demand for cloud gaming, and the popularity of subscription services continue to shape market trends. Leading companies invest in virtual reality (VR), augmented reality (AR), and cross-platform experiences to maintain competitive advantage. Regulatory focus on data privacy and responsible gaming remains high, supporting sustained growth and innovation.

Europe Video Games Market

Europe Video Games Market grew from USD 33.48 billion in 2018 to USD 50.03 billion in 2024 and is expected to reach USD 106.76 billion by 2032, with a CAGR of 9.8%. It holds a 26% market share, with the United Kingdom, Germany, and France representing the largest contributors. The market thrives on rising eSports participation, robust PC and mobile gaming communities, and the adoption of cloud gaming platforms. Government support for creative industries and technological education further accelerates digital transformation. European consumers show strong demand for local and international gaming content. Stringent regulations around loot boxes and microtransactions influence market strategies, ensuring consumer protection and transparency.

Asia Pacific Video Games Market

Asia Pacific Video Games Market grew from USD 46.13 billion in 2018 to USD 74.35 billion in 2024 and is anticipated to reach USD 179.55 billion by 2032, at a CAGR of 11.5%. Asia Pacific commands a 44% market share, driven by China, Japan, and South Korea, which serve as global gaming powerhouses. High smartphone adoption, vibrant eSports scenes, and a vast base of young gamers propel rapid market expansion. Leading developers invest in mobile-first strategies and localization to cater to diverse audiences. Regional governments support digital economies, spurring innovation and investment. Competitive pricing and accessible payment methods support continued user growth.

Latin America Video Games Market

Latin America Video Games Market grew from USD 4.94 billion in 2018 to USD 7.54 billion in 2024 and is projected to reach USD 14.90 billion by 2032, reflecting a CAGR of 8.7%. It holds a 4% market share, with Brazil, Mexico, and Argentina leading regional demand. Mobile gaming remains dominant due to widespread smartphone usage and affordable internet connectivity. The region sees rising interest in eSports and live streaming, which builds strong online communities. Developers introduce localized content and flexible payment models to overcome economic barriers. Investments in digital infrastructure and youth engagement further boost market growth.

Middle East Video Games Market

Middle East Video Games Market grew from USD 3.23 billion in 2018 to USD 4.57 billion in 2024 and is forecast to reach USD 8.73 billion by 2032, registering a CAGR of 8.2%. The Middle East commands a 2% market share, with key countries including Saudi Arabia, United Arab Emirates, and Egypt. The region benefits from a young population and high social media engagement, fostering rapid growth in online and mobile gaming. Governments invest in technology parks and digital events to develop local gaming industries. Content localization and culturally relevant titles help increase adoption and retention rates. Regulatory frameworks support secure digital payments and consumer protection, strengthening market confidence.

Africa Video Games Market

Africa Video Games Market grew from USD 1.96 billion in 2018 to USD 3.33 billion in 2024 and is set to reach USD 6.13 billion by 2032, growing at a CAGR of 7.7%. Africa accounts for a 2% market share, led by countries such as South Africa, Nigeria, and Kenya. Expanding internet connectivity and affordable smartphones drive mobile gaming growth, while traditional gaming platforms remain limited. Developers create tailored content to suit local preferences and languages. Youthful demographics and increased social gaming activity support user growth. Investments in digital infrastructure and partnerships with global developers enhance market accessibility and potential.

Key Player Analysis

- Tencent

- Sony

- Microsoft

- Nintendo

- Activision Blizzard

- Electronic Arts

- Epic Games

- Bandai Namco

- Square Enix

- NetEase

- Apple

- Netmarble

Competitive Analysis

The competitive landscape of the Video Games Market is defined by a combination of global reach, technological innovation, and diversified portfolios among leading companies. Key players include Tencent, Sony, Microsoft, Nintendo, Activision Blizzard, Electronic Arts, Epic Games, Bandai Namco, Square Enix, NetEase, Apple, and Netmarble. These industry leaders consistently invest in advanced gaming technologies, exclusive titles, and immersive experiences to attract and retain users across platforms. Strategic mergers, acquisitions, and partnerships allow them to expand market presence and access new segments, particularly in mobile gaming and cloud-based services. Companies prioritize recurring revenue streams through subscription services, in-game purchases, and dynamic online content, responding to evolving consumer preferences and maximizing long-term engagement. The industry also witnesses a surge in investment toward eSports, live events, and influencer marketing to build vibrant gaming communities and enhance user loyalty. Competition remains intense, driving continuous improvements in user experience, security, and personalized gameplay. This dynamic environment ensures sustained innovation and keeps the Video Games Market at the forefront of the global entertainment industry.

Recent Developments

- In April 2025, Microsoft released an updated Game Development Kit (GDK) with enhanced certification tools and a new screenshot management CLI for developers. This update aimed to improve the game development workflow by streamlining certification processes and providing better tools for screenshot management.

- In March 2025, At GDC 2025, Tencent showcased new game development technologies, including AI-driven anti-cheat systems and the GiiNEX AI platform, now supporting 150 million daily active users. They also demoed Honor of Kings: World, an open-world RPG spin-off, which received regulatory approval in China in January 2025 and is expected to launch this year.

- In February 2025, Sony’s State of Play event revealed major releases including Borderlands 4 (September 23), Directive 8020 (October 2), Shinobi: Art of Vengeance (August 29), and Digimon Story Time Stranger (TBA 2025).

Market Concentration & Characteristics

The Video Games Market demonstrates moderate to high market concentration, with a select group of global companies driving the majority of revenue through their extensive product portfolios and innovative technology adoption. It features a blend of established franchises and frequent new releases, ensuring a dynamic competitive environment. The market is defined by rapid technology cycles, high consumer engagement, and the ability to quickly adapt to emerging trends such as cloud gaming, AR, and VR. Its characteristics include strong network effects, a growing emphasis on digital distribution, and a focus on community-driven content. Barriers to entry remain significant due to the need for large development budgets, advanced technical capabilities, and effective global distribution channels. The Video Games Market stands out for its ability to capture diverse audiences across age groups and geographies, driving sustained growth through constant evolution in gaming experiences and monetization strategies.

Report Coverage

The research report offers an in-depth analysis based on Type, Gaming Type, Revenue Model and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market is projected to experience steady growth, driven by technological advancements and increasing global demand.

- Cloud gaming is expected to gain traction, offering players access to high-quality games without the need for expensive hardware.

- Mobile gaming will continue to dominate, with improvements in smartphone technology enhancing the gaming experience.

- Virtual reality (VR) and augmented reality (AR) technologies are anticipated to become more mainstream, providing immersive gaming experiences.

- Subscription-based models are likely to become more prevalent, offering gamers access to a wide range of titles for a monthly fee.

- The integration of artificial intelligence (AI) in games is expected to enhance gameplay by providing more responsive and adaptive experiences.

- Esports is projected to grow further, attracting larger audiences and increasing investment from sponsors and advertisers.

- Cross-platform gaming will become more common, allowing players on different devices to play together seamlessly.

- The market will see increased focus on user-generated content, enabling players to create and share their own game modifications and levels.

- Emerging markets, particularly in Asia and Latin America, are expected to contribute significantly to the industry’s growth due to rising internet penetration and smartphone adoption.