Market Overview

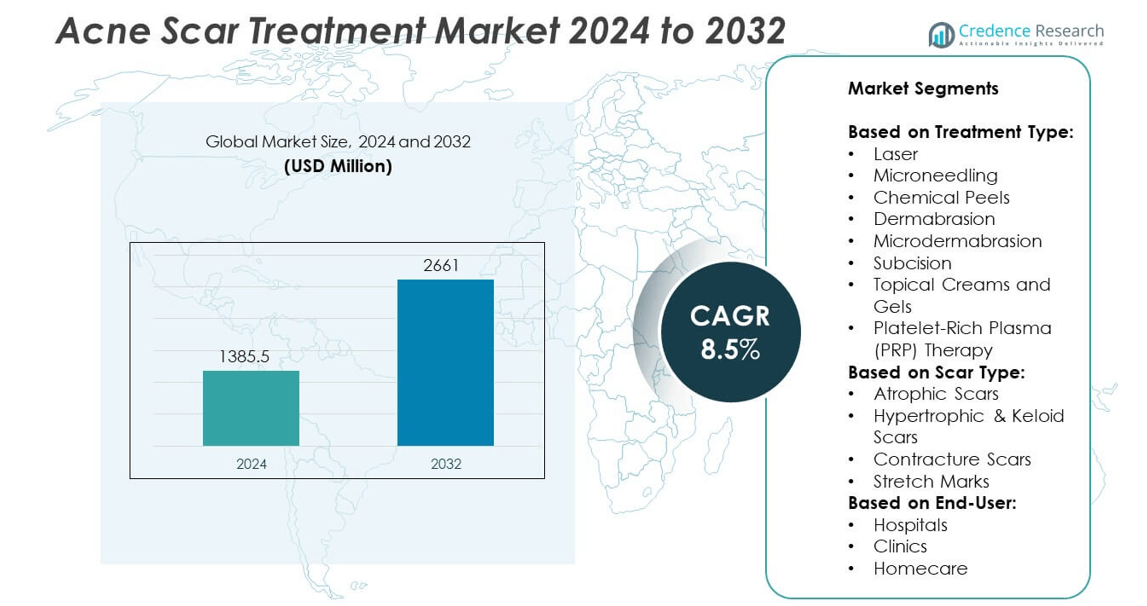

The Acne Scar Treatment Market size was valued at USD 1385.5 million in 2024 and is anticipated to reach USD 2661 million by 2032, registering a CAGR of 8.5% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Acne Scar Treatment Market Size 2024 |

USD 1385.5 million |

| Acne Scar Treatment Market, CAGR |

8.5% |

| Acne Scar Treatment Market Size 2032 |

USD 2661 million |

The Acne Scar Treatment market grows through rising global acne prevalence, increasing demand for advanced scar reduction solutions, and greater consumer willingness to invest in aesthetic care. Technological advancements in laser systems, microneedling devices, and regenerative therapies enhance treatment precision and outcomes. Expanding access to dermatology services in emerging markets broadens the patient base. Trends include the rising popularity of minimally invasive procedures, adoption of combination therapies for improved results, and demand for natural, biologically active ingredients in topical products.

North America leads the Acne Scar Treatment market due to advanced healthcare infrastructure, high patient awareness, and strong adoption of innovative procedures. Europe follows with a focus on safety, efficacy, and clean-label formulations, while Asia-Pacific shows rapid growth driven by a large population base and rising disposable incomes. Latin America and the Middle East & Africa are expanding with increasing access to dermatology services and medical tourism. Key players shaping the market include Smith & Nephew PLC.

Market Insights

- The Acne Scar Treatment market was valued at USD 1,385.5 million in 2024 and is projected to reach USD 2,661 million by 2032, registering a CAGR of 8.5% during the forecast period.

- Rising global acne prevalence, coupled with increased consumer focus on aesthetic appearance, drives demand for advanced scar reduction solutions, including laser therapies, microneedling, and regenerative treatments.

- Technological advancements in dermatology, such as AI-driven skin assessment, high-precision laser devices, and combination treatment protocols, are shaping market growth and enhancing treatment outcomes.

- Leading players, including Smith & Nephew PLC, Lumenis, and Perrigo Company plc, compete through product innovation, strategic collaborations, and expansion into emerging markets, strengthening their global reach.

- High treatment costs and limited insurance coverage for aesthetic procedures restrain adoption in price-sensitive markets, while variability in treatment outcomes and potential side effects create patient hesitancy.

- North America dominates the market due to advanced healthcare infrastructure and high treatment adoption rates, followed by Europe with a focus on regulated, high-quality solutions, and Asia-Pacific showing rapid growth from rising disposable incomes and expanding clinic networks.

- Growing penetration in Latin America and the Middle East & Africa is supported by medical tourism, increasing access to dermatology services, and targeted marketing strategies by both multinational and regional brands.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising Global Acne Prevalence and Demand for Advanced Scar Reduction Solutions

The growing incidence of acne among adolescents and adults fuels demand for targeted scar treatment solutions. Rising urban pollution, hormonal imbalances, and changing dietary patterns contribute to higher acne occurrence. Consumers seek treatments that deliver visible and long-lasting results, prompting the development of advanced formulations. The Acne Scar Treatment market benefits from the shift toward combination therapies, including topical agents and minimally invasive procedures. Dermatologists increasingly recommend customized regimens based on scar type and skin profile. This trend drives adoption of high-efficacy products and boosts innovation across multiple treatment categories.

- For instance, Perrigo’s Dermacosmetics branded business generated approximately 125 million in net sales.

Technological Advancements in Dermatological Devices and Procedures

Innovation in dermatological technologies expands treatment possibilities for acne scars. Laser-based systems, microneedling devices, and radiofrequency platforms provide improved efficacy and reduced downtime. It offers patients more precise targeting of scar tissue, leading to enhanced aesthetic outcomes. Clinics and med-spas invest in advanced devices to meet growing patient expectations. The integration of imaging technologies supports better diagnosis and treatment planning. Such progress encourages wider acceptance of professional-grade treatments, particularly in urban markets with higher disposable incomes.

- For instance, Cynosure’s PicoSure Pro system operates at 755 nanometers with pulse durations under 500 picoseconds, enabling effective pigment and scar treatment with minimal damage to surrounding tissue.

Growing Consumer Awareness and Willingness to Invest in Aesthetic Care

Heightened awareness of skin health and aesthetics encourages more individuals to seek scar treatment. Social media exposure and influencer-led skincare campaigns highlight available options and their benefits. It prompts consumers to invest in professional services and premium products that promise visible improvement. Younger demographics show greater openness to early intervention to prevent long-term scarring. Marketing strategies by key players emphasize scientific credibility and real-world results. These dynamics contribute to sustained growth in demand for both in-clinic and at-home solutions.

Expanding Access to Dermatology Services in Emerging Markets

Improved healthcare infrastructure in emerging economies broadens access to advanced acne scar treatments. Expansion of dermatology clinics in urban and semi-urban areas brings professional care closer to underserved populations. It supports market penetration by multinational and local brands. Economic growth in these regions increases affordability of aesthetic procedures. Training programs for dermatologists enhance service quality and patient trust. The combination of greater accessibility and rising income levels accelerates adoption of innovative treatment options.

Market Trends

Increasing Popularity of Minimally Invasive and Non-Invasive Treatment Options

Patient preference is shifting toward procedures that deliver results with minimal discomfort and downtime. Laser resurfacing, microneedling, and chemical peels are gaining traction for their ability to improve skin texture without extensive recovery. The Acne Scar Treatment market benefits from the adoption of these methods across both clinical and med-spa settings. It allows practitioners to cater to a broader demographic, including working professionals seeking discreet treatments. Manufacturers are enhancing device portability and user-friendliness to increase accessibility. This trend supports higher treatment frequency and greater patient satisfaction.

- For instance, RF microneedling platforms in the professional segment can deliver energy at depths up to 3.5 millimeters, improving collagen stimulation in deeper dermal layers.

Integration of Combination Therapies for Enhanced Clinical Outcomes

Dermatologists increasingly combine multiple treatment modalities to target different aspects of scar formation. Pairing laser therapy with topical agents or dermal fillers optimizes collagen remodeling and skin smoothness. It addresses the limitations of single-treatment approaches and delivers more comprehensive results. Clinics adopt protocols tailored to scar type, skin tone, and patient expectations. Research supports the efficacy of combination strategies in accelerating visible improvements. This practice strengthens patient loyalty and clinic reputation.

- For instance, Suneva Medical Bellafill dermal filler has received approval for acne scar treatment in more than 15 countries, expanding its availability in high-growth markets. Specifically, it’s indicated for the correction of nasolabial folds and moderate to severe, atrophic, distensible facial acne scars on the cheek in patients over 21 years old.

Rising Demand for Natural and Biologically Active Ingredients in Topical Solutions

Consumers are seeking products that combine efficacy with clean and sustainable formulations. Botanical extracts, peptides, and growth factors are being incorporated into scar creams and serums to promote skin regeneration. It reflects a wider shift toward conscious beauty and ingredient transparency. Brands highlight scientific validation of natural actives to build trust and differentiate offerings. The expansion of online retail platforms accelerates availability of these products globally. This aligns with consumer demand for safer, at-home solutions.

Expansion of Teledermatology and Digital Skin Assessment Platforms

Remote consultation platforms are transforming patient access to acne scar treatments. High-resolution imaging tools and AI-driven analysis help dermatologists recommend targeted regimens without in-person visits. It expands reach to rural and underserved markets where specialist access is limited. Patients benefit from convenient follow-ups and ongoing treatment monitoring. Integration with e-commerce platforms enables direct purchase of prescribed products. This digital transformation enhances both patient engagement and treatment adherence.

Market Challenges Analysis

High Treatment Costs and Limited Insurance Coverage for Aesthetic Procedures

The cost of advanced acne scar treatments remains a barrier for a significant portion of potential patients. Laser resurfacing, dermal fillers, and other professional procedures often require multiple sessions, driving expenses beyond what many can afford. The Acne Scar Treatment market faces slow adoption in regions where aesthetic services are not covered by health insurance. It restricts access to premium technologies and limits market penetration among middle- and lower-income groups. Clinics must balance pricing strategies with profitability while addressing patient affordability concerns. This challenge sustains demand for lower-cost, at-home alternatives that may offer less effective results.

Variability in Treatment Outcomes and Risk of Adverse Effects

Differences in scar type, skin tone, and patient health contribute to inconsistent results from the same treatment protocol. Some patients experience incomplete scar reduction or recurrence, affecting satisfaction and trust in available solutions. It creates reputational challenges for clinics and product brands in the Acne Scar Treatment market. The risk of side effects such as hyperpigmentation, irritation, or infection discourages certain demographics from pursuing professional care. Regulatory scrutiny over safety and efficacy claims adds further pressure on manufacturers and service providers. Continuous training of practitioners and patient education remain essential to overcoming these limitations.

Market Opportunities

Emerging Demand in Untapped Regional Markets and Expanding Middle-Class Demographics

Rapid urbanization and rising disposable incomes in Asia-Pacific, Latin America, and parts of the Middle East create strong potential for advanced scar treatments. The Acne Scar Treatment market can leverage growing interest in aesthetic enhancement among younger populations. It benefits from improved access to dermatology clinics and greater exposure to global beauty trends through digital media. Local distributors and international brands have an opportunity to establish early market presence with affordable yet high-quality offerings. Government-led healthcare infrastructure upgrades further support the availability of advanced devices and procedures. Strategic partnerships with regional clinics can accelerate adoption and brand recognition.

Innovation in Personalized Treatment Protocols and Product Formulations

Advancements in AI-driven skin analysis, 3D imaging, and biomarker-based diagnostics enable highly customized acne scar treatments. Clinics can use these tools to design protocols that maximize efficacy while minimizing side effects for each patient. It aligns with consumer demand for tailored solutions and premium experiences. Topical product innovation incorporating growth factors, stem cell derivatives, and peptide complexes presents opportunities for differentiation in competitive markets. E-commerce integration allows brands to offer personalized product bundles based on digital consultations. Expanding into hybrid care models that combine in-clinic treatments with home-based maintenance solutions can strengthen long-term patient engagement.

Market Segmentation Analysis:

By Treatment Type:

The Acne Scar Treatment market covers a broad spectrum of procedures and products addressing varying scar severity and patient preferences. Laser treatments dominate in clinical settings due to their precision, shorter recovery times, and proven efficacy in collagen remodeling. Microneedling maintains strong adoption for its ability to improve texture across multiple scar types with minimal downtime. Chemical peels are valued for their cost-effectiveness and suitability for superficial scars, while dermabrasion and microdermabrasion cater to patients seeking mechanical exfoliation. Subcision remains a specialized approach for deep atrophic scars, often used in combination with other modalities. Topical creams and gels, including retinoids and growth factor-based formulations, continue to serve as first-line or maintenance therapy. Platelet-Rich Plasma (PRP) therapy is gaining momentum for its regenerative properties and minimal side-effect profile.

- For instance, Cynosure’s PicoSure Pro system supports customizable treatments through a Zoom handpiece with spot sizes ranging from 2 to 6 mm and fixed handpieces at 5, 6, 8, and 10 mm, which enhances precision in treating acne scars.

By Scar Type:

Atrophic scars represent the largest segment due to their high prevalence among post-acne patients. These depressions in the skin often require combination approaches, including laser resurfacing and microneedling. Hypertrophic and keloid scars present a smaller but complex segment, with treatment focusing on reducing excess collagen through steroid injections, laser therapy, or surgical revision. Contracture scars, though less common in acne, demand advanced intervention due to their impact on skin mobility and function. Stretch marks, while not traditional acne scars, are addressed within the same treatment portfolio in many clinics, creating cross-selling opportunities for providers. It enables practitioners to diversify services and appeal to broader patient needs.

- For instance, Lumenis’ ResurFX fractional laser system operates at a wavelength of 1565 nanometers and allows treatment of up to 500 microspots per scan, enabling precise collagen stimulation for acne scar reduction.

By End-User:

Hospitals account for a significant share due to their access to advanced equipment, multidisciplinary expertise, and capacity for complex procedures. Clinics, including dermatology centers and med-spas, hold a competitive position by offering specialized treatments in accessible locations with shorter appointment lead times. Homecare forms a rapidly expanding segment driven by over-the-counter creams, serums, and at-home microneedling devices. It caters to patients seeking convenience, privacy, and lower costs while maintaining skin improvement between professional sessions. The growing availability of teledermatology further supports the homecare segment by enabling remote consultations and personalized product recommendations.

Segments:

Based on Treatment Type:

- Laser

- Microneedling

- Chemical Peels

- Dermabrasion

- Microdermabrasion

- Subcision

- Topical Creams and Gels

- Platelet-Rich Plasma (PRP) Therapy

Based on Scar Type:

- Atrophic Scars

- Hypertrophic & Keloid Scars

- Contracture Scars

- Stretch Marks

Based on End-User:

- Hospitals

- Clinics

- Homecare

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America holds 38.2% of the global Acne Scar Treatment market share, driven by high awareness of aesthetic dermatology and strong purchasing power among consumers. The United States leads regional demand with a well-established network of dermatology clinics, med-spas, and advanced hospitals offering a wide range of scar treatments. It benefits from rapid adoption of laser-based systems, microneedling, and PRP therapy supported by favorable clinical outcomes. Canada follows with growing investments in dermatology services and a preference for minimally invasive procedures. Direct-to-consumer marketing by leading brands increases adoption of premium topical formulations. The presence of major industry players and favorable reimbursement policies for certain reconstructive procedures further strengthen the market position.

Europe

Europe accounts for 27.4% of the market, supported by advanced healthcare infrastructure and stringent regulatory standards for dermatology equipment and products. Germany, France, and the United Kingdom lead in procedure volume, with high demand for combination therapies and non-invasive solutions. It reflects a patient base that prioritizes both clinical efficacy and safety. Scandinavian countries show strong adoption of clean-label topical products aligned with natural ingredient trends. The region benefits from active research collaborations between universities, clinics, and manufacturers, enhancing treatment innovation. Medical tourism in countries such as Poland and Hungary also supports growth by offering competitive pricing for advanced procedures.

Asia-Pacific

Asia-Pacific represents 22.8% of the global share, with rapid growth driven by a large population base and rising disposable incomes. Countries like China, Japan, South Korea, and India are key markets, with South Korea recognized as a global hub for cosmetic dermatology innovation. It benefits from increasing consumer awareness and social media influence on beauty standards. Local manufacturers introduce competitively priced devices and products, accelerating accessibility. The younger demographic actively invests in early treatment to prevent long-term scarring, fueling demand across clinics and homecare solutions. Expanding private healthcare infrastructure supports penetration into tier-2 and tier-3 cities.

Latin America

Latin America holds 6.9% of the Acne Scar Treatment market, with Brazil and Mexico accounting for the majority of regional revenue. Brazil’s well-developed aesthetic medicine industry and growing middle class create favorable conditions for advanced treatment adoption. It reflects a consumer base that values appearance and actively seeks professional dermatology services. Mexico benefits from cross-border medical tourism, attracting patients from the United States for cost-effective procedures. Increasing availability of non-invasive technologies and rising retail distribution of topical products broaden access. Regulatory improvements in medical device approvals further support market expansion.

Middle East & Africa

The Middle East & Africa region accounts for 4.7% of the market, with demand concentrated in urban centers such as Dubai, Riyadh, and Johannesburg. The Middle East benefits from a high-income population with strong interest in aesthetic enhancements, supported by luxury clinic infrastructure. It shows high uptake of laser resurfacing, PRP therapy, and premium skincare lines. In Africa, market growth is gradual due to limited specialist availability, but expanding private healthcare facilities are improving access. Governments in the Gulf Cooperation Council countries actively promote medical tourism, which supports dermatology service growth. Local distribution partnerships are essential to strengthen product reach in emerging areas.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Perrigo Company plc

- Lumenis

- Scar Heal Inc.

- Suneva Medical

- Sonoma Pharmaceuticals, Inc.

- Mölnlycke Health Care AB

- Pacific World Corporation

- Smith & Nephew PLC

- Enaltus LLC

- CCA Industries, Inc.

- Cynosure

- Merz Pharmaceuticals, LLC

- Newmedical Technology Inc.

Competitive Analysis

The leading players in the Acne Scar Treatment market include Smith & Nephew PLC, Lumenis, Perrigo Company plc, Merz Pharmaceuticals LLC, Sonoma Pharmaceuticals Inc., Cynosure, and Mölnlycke Health Care AB. These companies compete by leveraging product innovation, advanced technologies, and global distribution networks to capture diverse customer segments. They invest heavily in research and development to introduce solutions with improved efficacy, safety, and patient comfort. Strategic mergers, acquisitions, and partnerships with dermatology clinics and distributors expand their market footprint and enhance service accessibility. Strong branding and targeted marketing campaigns reinforce product positioning in both professional and consumer segments. Expansion into emerging markets remains a critical growth strategy, supported by localized manufacturing and tailored pricing models. The competitive environment is shaped by constant technological upgrades in devices, integration of biologically active ingredients in topical formulations, and adoption of hybrid treatment protocols combining in-clinic procedures with at-home maintenance products. Continuous training programs for healthcare professionals and patient education initiatives further strengthen brand credibility. Companies that successfully align innovation with affordability and accessibility are better positioned to gain long-term competitive advantages in this fast-evolving market.

Recent Developments

- In 2025, Perrigo Company plc also shared a press release outlining a strategic organizational update aimed at scaling and optimizing its global category-led growth model.

- In 2023, Sonoma Pharmaceuticals, Inc. launched two new office‑dispensed skincare products—Relifen Plus and Rejunex Plus to expand its dermatology professional line.

- In 2022, Cynosure introduced the PicoSure Pro system, an FDA‑cleared 755 nm picosecond laser designed to treat wrinkles, pigmentation, and acne scars.

Market Concentration & Characteristics

The Acne Scar Treatment market shows a moderately fragmented structure with a mix of global leaders and regional players competing across device-based solutions, topical products, and regenerative therapies. It is characterized by continuous technological innovation, strong brand positioning, and diverse distribution channels spanning hospitals, clinics, and homecare. Leading companies focus on product differentiation through advanced laser systems, microneedling technologies, and scientifically backed topical formulations. The market benefits from rising consumer awareness, expanding access to dermatology services, and growing demand for minimally invasive options. Pricing strategies vary significantly between premium clinical procedures and mass-market over-the-counter products, creating opportunities for multiple tiers of competition. Regulatory compliance and safety certifications remain critical for market entry and brand credibility, especially in developed regions. Competitive intensity is reinforced by marketing campaigns, strategic partnerships, and expansion into emerging economies with untapped growth potential.

Report Coverage

The research report offers an in-depth analysis based on Treatment Type, Scar Type, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will see stronger demand for minimally invasive and non-invasive procedures with shorter recovery times.

- Technological innovation in laser systems and regenerative therapies will enhance treatment precision and outcomes.

- Combination protocols integrating multiple modalities will gain wider clinical adoption for improved scar reduction.

- Consumer preference for natural and biologically active ingredients in topical products will continue to grow.

- AI-driven skin assessment tools will become a standard in personalized treatment planning.

- Teledermatology platforms will expand access to professional consultations and product recommendations.

- Emerging markets will experience higher adoption rates driven by expanding clinic networks and rising incomes.

- Strategic collaborations between manufacturers and dermatology service providers will strengthen market reach.

- Medical tourism will contribute to the uptake of advanced procedures in cost-competitive regions.

- Continuous education for practitioners and awareness campaigns will improve treatment acceptance and patient satisfaction.