Market Overview:

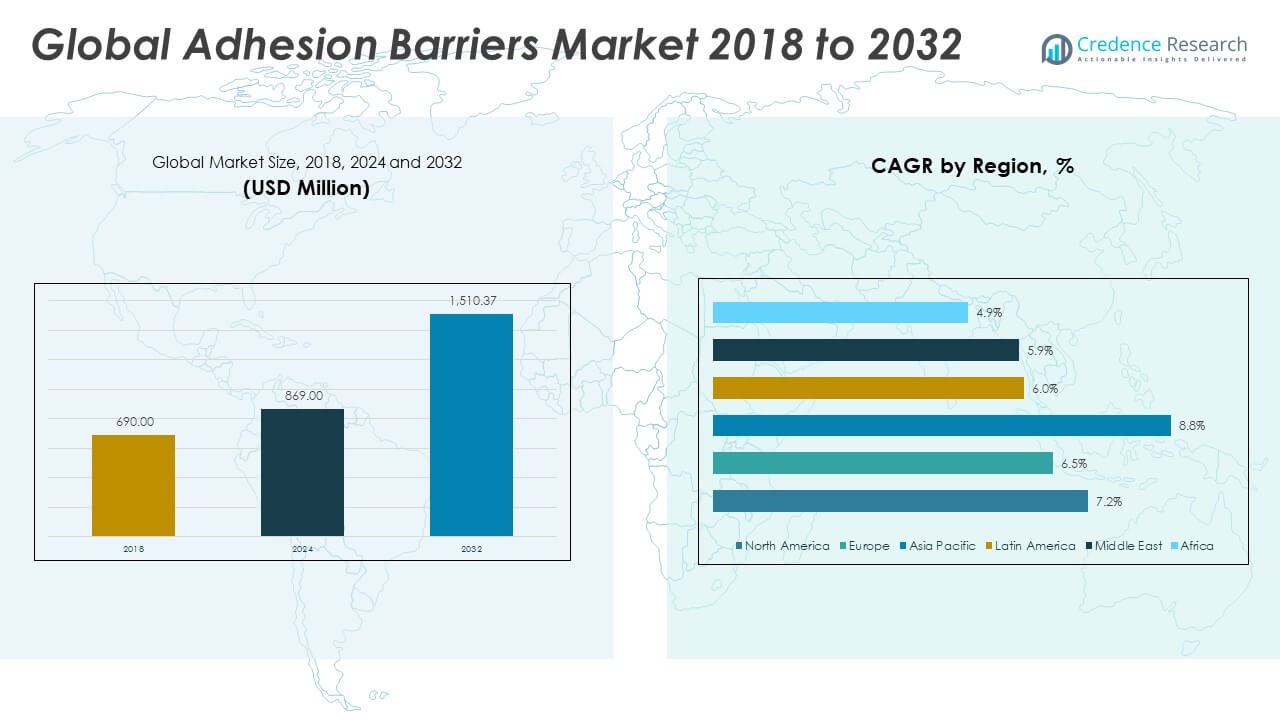

The Adhesion Barriers Market size was valued at USD 690.00 million in 2018 to USD 869.00 million in 2024 and is anticipated to reach USD 1,510.37 million by 2032, at a CAGR of 7.20% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2019-2022 |

| Base Year |

2023 |

| Forecast Period |

2024-2032 |

| Adhesion Barriers Market Size 2023 |

USD 869.00 million |

| Adhesion Barriers Market, CAGR |

7.20% |

| Adhesion Barriers Market Size 2032 |

USD 1,510.37 million |

The growth of the adhesion barriers market is primarily driven by the rising number of surgical procedures across various medical disciplines, including gynecology, orthopedics, and general surgery. As awareness increases regarding postoperative complications such as internal scarring and tissue adhesions, healthcare providers are placing greater emphasis on preventive solutions to enhance patient outcomes. Surgeons are progressively adopting adhesion barriers to reduce recovery times, lower the risk of reoperations, and improve long-term surgical success rates. Furthermore, advancements in biomaterials such as bioresorbable films and gels are offering more effective and safer solutions that are easier to apply and compatible with diverse surgical techniques. Increasing focus on patient safety and the demand for minimally invasive surgeries are also propelling product adoption. Additionally, support from regulatory agencies and growing investment by manufacturers in clinical research and development are expanding product portfolios, thereby accelerating market penetration and strengthening confidence among healthcare professionals.

Regionally, the adhesion barriers market exhibits varied levels of adoption influenced by healthcare infrastructure, regulatory policies, and awareness. North America leads due to well-established healthcare systems, widespread adoption of advanced surgical techniques, and strong reimbursement frameworks that encourage use of adhesion prevention products. Europe follows closely, supported by robust surgical volumes and increasing focus on patient recovery outcomes. The Asia Pacific region is emerging as the fastest-growing market, driven by rising medical tourism, increasing healthcare expenditures, and growing demand for modern surgical interventions in densely populated countries like China and India. This region also benefits from rapid urbanization and expansion of private healthcare facilities. Meanwhile, Latin America, the Middle East, and Africa are witnessing gradual market expansion, supported by improving healthcare access and rising awareness of postoperative care. While these regions currently represent smaller market shares, they hold significant growth potential as governments and private sectors invest in modernizing their healthcare delivery systems.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights:

- The Adhesion Barriers Market is projected to grow from USD 869.00 million in 2024 to USD 1,510.37 million by 2032, driven by a strong CAGR of 7.20%.

- Rising surgical procedures in gynecology, orthopedics, and general surgery are accelerating demand for adhesion prevention solutions.

- Technological advancements in biomaterials, including bioresorbable gels and films, are enhancing safety, usability, and surgeon preference.

- Hospitals are integrating adhesion barriers into surgical protocols to reduce complications, reoperations, and long-term patient care costs.

- Regulatory support and growing clinical evidence are encouraging faster approvals and broader product acceptance across regions.

- North America holds the largest market share due to advanced healthcare systems and strong reimbursement frameworks, while Asia Pacific is the fastest-growing region.

- Limited surgeon adoption, high product cost, and reimbursement challenges remain key obstacles to widespread global implementation.

Market Drivers:

Surge in Surgical Procedures Across Medical Specialties is Fueling Demand for Adhesion Prevention

The increasing number of surgical interventions globally is one of the most significant drivers in the Adhesion Barriers Market. General, gynecological, orthopedic, and cardiovascular surgeries often lead to internal scarring and postoperative adhesions, creating a high demand for adhesion-preventive solutions. Hospitals and surgical centers are focusing on reducing complications and improving patient outcomes by incorporating advanced barriers. It is becoming standard practice to use adhesion barriers during procedures that carry high adhesion risk. Growing access to elective surgeries in developing regions is expanding the addressable market. It continues to gain traction across multiple disciplines as awareness about adhesion-related risks increases among surgeons and healthcare providers.

- For instance, Baxter’s Seprafilm Adhesion Barrier has been used in over 4 million abdominal and pelvic procedures worldwide, with clinical trials across 2,133 patients showing significantly fewer adhesions—51% in treated patients were adhesion-free at 8–12 weeks versus just 6% in controls (p < 0.0001).

Technological Advancements in Barrier Materials Are Enhancing Product Efficiency and Application

Product development in the adhesion barriers space has shifted toward advanced biomaterials that ensure biocompatibility and ease of use. Manufacturers are introducing film, gel, and spray formats that can be easily applied during laparoscopic and open surgeries. These innovations support precision and safety, reducing surgical time and improving usability in various settings. It supports clinical outcomes by offering temporary protection and complete resorption without causing adverse reactions. The availability of multiple formulations allows healthcare providers to choose the most suitable option for each procedure. The market benefits from continuous research investments aimed at optimizing performance and improving shelf-life.

Rising Focus on Postoperative Care and Long-Term Patient Outcomes Is Encouraging Adoption

Hospitals and healthcare systems are under growing pressure to minimize postoperative complications and readmission rates. Adhesion-related problems, including infertility, bowel obstruction, and chronic pain, often require costly and complex follow-up procedures. The Adhesion Barriers Market addresses this issue by enabling preventive care strategies that align with modern surgical standards. It plays a critical role in reducing healthcare costs over time and improving quality-of-life metrics. Health systems and insurance providers are increasingly supporting the use of adhesion barriers as part of standard surgical protocols. This focus on preventive healthcare continues to create favorable conditions for product acceptance.

- For instance, FzioMed’s Oxiplex/SP Gel, applied in lumbar discectomy, led to a 35% greater reduction in leg pain and 28% greater reduction in back pain at 6 months compared to surgery alone. Additionally, the treated group had only 1 reoperation versus 6 in controls over the same period.

Expanding Clinical Evidence and Regulatory Support Is Strengthening Market Confidence

Growing clinical data demonstrating the effectiveness of adhesion barriers is helping build trust among surgeons and regulatory bodies. Published studies and successful trials are reinforcing the role of these products in enhancing surgical safety. It is prompting regulators to issue clearer guidelines and approvals, enabling faster market access for new products. Regulatory clarity also encourages manufacturers to expand product lines and invest in specialized formulations. The presence of established quality standards assures clinicians of product reliability during critical procedures. These regulatory and clinical developments are positioning the market for sustained adoption and innovation.

Market Trends:

Growing Preference for Biodegradable and Natural Polymer-Based Adhesion Barriers Is Gaining Momentum

There is a rising interest in adhesion barriers derived from natural polymers such as hyaluronic acid, collagen, and carboxymethylcellulose. These materials offer improved safety profiles and are perceived to be more biocompatible than synthetic alternatives. Researchers and manufacturers are exploring plant-based and bioengineered materials to meet the increasing demand for sustainable medical solutions. The Adhesion Barriers Market is witnessing a shift toward formulations that degrade naturally in the body without triggering immune responses. It supports the healthcare industry’s move toward eco-friendly, patient-centered product development. This trend aligns with broader regulatory emphasis on clean-label medical products and non-toxic surgical aids.

- For example, the ABT13107 thermosensitive HA–poloxamer gel, developed by A.BioTech, transitions from liquid to gel at body temperature. In a 2024 randomized clinical trial with 192 women undergoing hysteroscopic surgery, ABT13107 demonstrated non-inferiority to Hyalobarrier (the industry reference gel) in reducing intrauterine adhesions, with zero serious adverse events reported and a user-reported application time of less than 60 seconds per procedure.

Adoption of Combination Barrier Products with Antimicrobial or Anti-Inflammatory Properties Is Expanding

Manufacturers are developing multifunctional adhesion barriers that combine anti-adhesion capabilities with antimicrobial or anti-inflammatory effects. These hybrid solutions are designed to lower the risk of postoperative infections while preventing tissue adhesions. Hospitals and surgical centers are increasingly favoring such dual-purpose products to simplify procedural workflows and improve patient outcomes. The Adhesion Barriers Market is seeing greater investment in integrated solutions that provide both protection and therapeutic benefits. It reflects a trend toward innovation-driven differentiation in a competitive landscape. Regulatory bodies are supporting such advancements when safety and efficacy profiles are well-documented through clinical trials.

- For instance, a sprayable hydrogel developed by a leading biotechnology firm uses sulfated hyaluronic acid (sHA) blended with chitosan, delivered via a dual-syringe system. This hydrogel forms a conformal gel film in situ and actively modulates local inflammation by promoting an M2 macrophage phenotype, which is anti-inflammatory.

Increased Use of Adhesion Barriers in Robotic and Minimally Invasive Surgeries Is Accelerating

The rapid growth of robotic-assisted and minimally invasive surgical procedures is influencing the development and deployment of specialized adhesion barriers. These surgeries require highly adaptable barrier materials that can be delivered through small incisions and perform reliably under constrained visibility. The Adhesion Barriers Market is responding with thinner, more pliable films and sprayable gels that meet the precision needs of these procedures. It enables surgeons to apply adhesion barriers more effectively without compromising procedural efficiency. As hospitals invest in advanced surgical platforms, the demand for compatible adjunctive materials continues to rise. This trend is reshaping product design and formulation strategies across the market.

Rising Integration of Adhesion Barrier Use into Clinical Protocols and Surgical Training Programs

Medical institutions are incorporating the use of adhesion barriers into their standard operating procedures and training curricula. This move ensures that new surgeons and residents become familiar with the indications, applications, and benefits of adhesion prevention early in their careers. The Adhesion Barriers Market is benefiting from this institutional alignment, which supports wider and more consistent product adoption. It also reflects the growing importance of evidence-based practices in surgical education. Training hospitals and academic centers are collaborating with manufacturers to evaluate and refine the use of these barriers in real-world settings. This integration strengthens long-term usage trends and encourages continuous product improvement.

Market Challenges Analysis:

Limited Surgeon Adoption and Procedural Compatibility Are Hindering Broader Market Penetration

Despite proven clinical benefits, many surgeons remain hesitant to incorporate adhesion barriers into routine procedures. Concerns regarding additional steps during surgery, variability in product performance, and limited hands-on training contribute to inconsistent usage. Some procedures, especially in emergency settings, do not allow time for careful application of adhesion barriers. The Adhesion Barriers Market faces resistance from surgical teams that prioritize speed and familiarity over preventive interventions. It struggles with integration in workflows where standardization is not enforced or where product selection varies by institution. To overcome this challenge, greater emphasis is needed on surgeon education and streamlined product design.

High Product Cost and Reimbursement Limitations Are Restricting Adoption in Cost-Sensitive Markets

The relatively high cost of adhesion barriers presents a challenge in healthcare systems with strict budget controls or limited reimbursement frameworks. Hospitals in developing regions often prioritize essential surgical tools over adjunctive products like adhesion barriers. The Adhesion Barriers Market encounters difficulties in regions where insurance does not cover non-mandatory surgical materials. It also faces pricing pressure from procurement departments that seek to reduce overall procedural costs. Manufacturers must demonstrate clear cost-benefit value to justify routine use. Addressing economic barriers remains essential for expanding adoption across public and private healthcare settings.

Market Opportunities:

Expansion into Emerging Healthcare Markets Can Unlock Untapped Growth Potential

Healthcare systems in emerging economies are rapidly investing in surgical infrastructure and advanced medical technologies. This shift presents a strong opportunity for the Adhesion Barriers Market to expand its footprint in regions such as Asia Pacific, Latin America, and the Middle East. Rising surgical volumes, coupled with improving healthcare access, create a favorable environment for adoption. It can leverage partnerships with local distributors and hospitals to introduce cost-effective products tailored to regional needs. Educational initiatives and government-backed quality care programs can support awareness and usage. These markets hold significant long-term potential for manufacturers willing to adapt to local conditions.

Product Innovation for Niche Applications Can Broaden Clinical Adoption Across Specialties

There is growing demand for adhesion barriers specifically designed for niche surgical applications such as pediatric procedures, neurological surgeries, and trauma cases. The Adhesion Barriers Market can benefit by developing targeted solutions that meet the unique requirements of these high-risk areas. It can also explore opportunities in outpatient surgical centers and ambulatory care settings where minimally invasive procedures are gaining popularity. Customizable formulations and delivery systems can enhance product appeal. Expanding indications through regulatory approvals will further strengthen market position. These innovation-driven strategies can open new revenue channels and deepen penetration across clinical environments.

Market Segmentation Analysis:

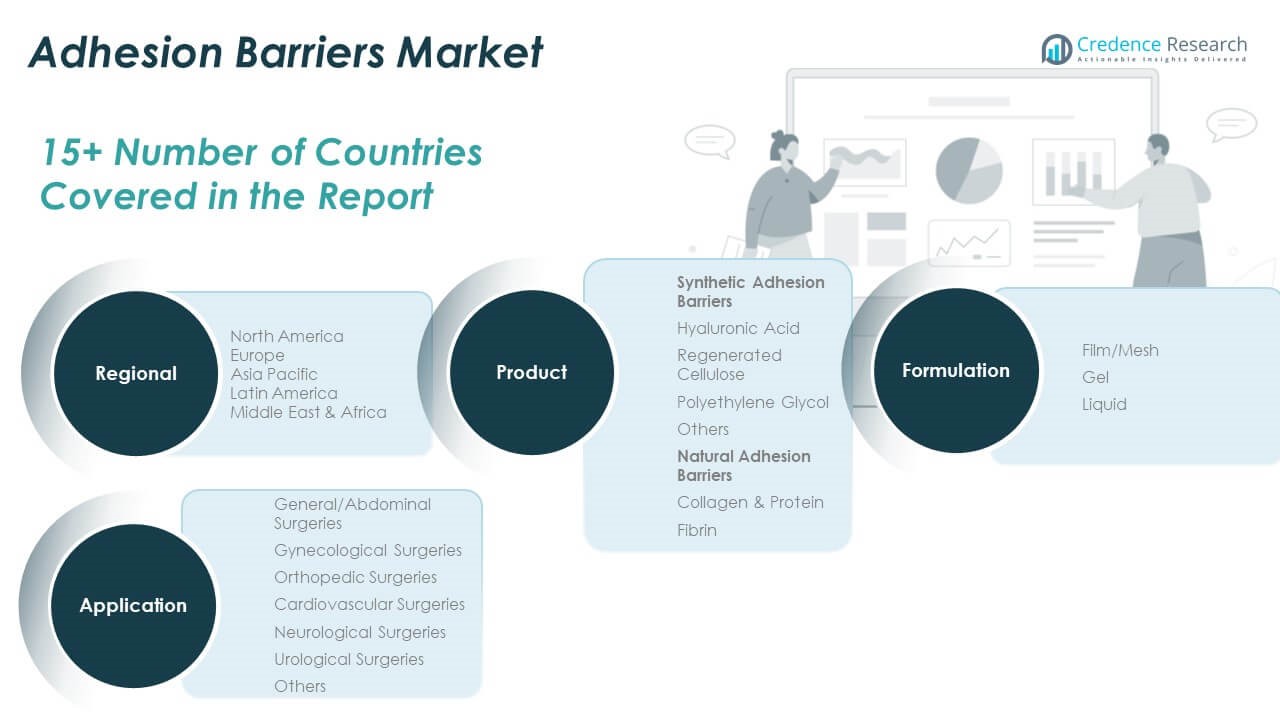

The Adhesion Barriers Market is segmented by product, formulation, and application, each contributing uniquely to its overall expansion.

By product, synthetic adhesion barriers dominate the market due to their widespread use and favorable properties. Hyaluronic acid, regenerated cellulose, and polyethylene glycol lead the synthetic category, offering effective adhesion prevention across various surgical procedures. Natural adhesion barriers, including collagen & protein and fibrin, are gaining traction for their biocompatibility and minimal adverse reactions.

- For instance, Seprafilm®, made from chemically modified hyaluronic acid and carboxymethylcellulose (a regenerated cellulose derivative), has been used in over 4 million abdominal and pelvic procedures. It significantly reduced reoperations for small bowel obstruction by 47% compared to controls

By formulation, film/mesh products hold a strong position due to their precision in open surgeries, while gels are favored in laparoscopic and minimally invasive settings for their ease of application. Liquid formulations are also being adopted for complex or irregular anatomical areas.

By application, general and abdominal surgeries account for the largest market share, driven by the high volume of procedures and risk of adhesions. Gynecological and orthopedic surgeries follow closely. The Adhesion Barriers Market also sees steady demand from cardiovascular, neurological, and urological surgeries, reflecting its expanding utility across specialties.

- For instance, PEG liquid spray during gynecological laparoscopy reduced new adhesions: 0% incidence in treated vs. 67% in controls, with mean adhesion scores significantly improved (–2.6 vs –0.06).

Segmentation:

By Product

- Synthetic Adhesion Barriers

- Hyaluronic Acid

- Regenerated Cellulose

- Polyethylene Glycol

- Others

- Natural Adhesion Barriers

- Collagen & Protein

- Fibrin

By Formulation

By Application

- General/Abdominal Surgeries

- Gynecological Surgeries

- Orthopedic Surgeries

- Cardiovascular Surgeries

- Neurological Surgeries

- Urological Surgeries

- Others

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America

The North America Adhesion Barriers Market size was valued at USD 273.93 million in 2018 to USD 341.16 million in 2024 and is anticipated to reach USD 592.22 million by 2032, at a CAGR of 7.2% during the forecast period. North America holds the largest share in the global adhesion barriers market, accounting for nearly 34% of the total market. The region’s dominance stems from advanced surgical infrastructure, widespread adoption of preventive surgical solutions, and well-defined reimbursement policies. It benefits from the presence of key market players and consistent innovation in product formulations and delivery systems. Increasing demand for minimally invasive surgeries and high awareness of post-surgical complications drive product utilization across hospitals and specialty centers. Regulatory support and integration of adhesion barriers into clinical protocols further strengthen the market position across the U.S. and Canada.

Europe

The Europe Adhesion Barriers Market size was valued at USD 203.55 million in 2018 to USD 247.47 million in 2024 and is anticipated to reach USD 408.94 million by 2032, at a CAGR of 6.5% during the forecast period. Europe captures a 25% share of the global adhesion barriers market, supported by a strong focus on patient safety and surgical quality standards. High adoption of laparoscopic procedures and growing elderly population contribute to market growth. It benefits from established healthcare systems and regulatory frameworks that encourage innovation while ensuring patient safety. The region also witnesses active collaboration between hospitals, academic institutions, and manufacturers to validate new applications and formulations. Germany, France, and the U.K. lead in terms of market penetration due to their surgical volume and advanced medical infrastructure.

Asia Pacific

The Asia Pacific Adhesion Barriers Market size was valued at USD 134.55 million in 2018 to USD 178.88 million in 2024 and is anticipated to reach USD 350.86 million by 2032, at a CAGR of 8.8% during the forecast period. Asia Pacific holds a 21% share and is the fastest-growing regional market due to increasing healthcare investments, rising surgical volumes, and expanding access to quality care. It is driven by population growth, a surge in chronic disease prevalence, and modernization of surgical practices across China, India, Japan, and South Korea. Government initiatives to upgrade hospital infrastructure and promote clinical training boost market prospects. Local manufacturing and distributor partnerships support regional supply and cost efficiency. The demand for affordable and minimally invasive adhesion barriers continues to expand, especially in urban centers.

Latin America

The Latin America Adhesion Barriers Market size was valued at USD 35.19 million in 2018 to USD 43.79 million in 2024 and is anticipated to reach USD 69.28 million by 2032, at a CAGR of 6.0% during the forecast period. Latin America represents a smaller yet steadily expanding share of 5% in the global adhesion barriers market. Rising surgical volumes, coupled with improvements in hospital infrastructure, are driving gradual growth. It is supported by increasing awareness among healthcare professionals about post-surgical complications and benefits of barrier use. Countries like Brazil, Mexico, and Argentina are key contributors, with public and private healthcare institutions adopting advanced surgical protocols. Cost sensitivity remains a barrier, but local partnerships and targeted education programs are improving product access and acceptance.

Middle East

The Middle East Adhesion Barriers Market size was valued at USD 26.84 million in 2018 to USD 31.71 million in 2024 and is anticipated to reach USD 49.85 million by 2032, at a CAGR of 5.9% during the forecast period. The Middle East accounts for a 3% share in the global adhesion barriers market, supported by growing investments in healthcare modernization. It is gaining traction in surgical centers that focus on minimally invasive and high-precision procedures. The UAE and Saudi Arabia lead regional adoption through advanced infrastructure and surgical expertise. Increasing collaboration with international manufacturers and improved regulatory clarity contribute to market growth. While cost remains a constraint in public healthcare, private facilities are showing higher usage of adhesion barriers.

Africa

The Africa Adhesion Barriers Market size was valued at USD 15.94 million in 2018 to USD 25.99 million in 2024 and is anticipated to reach USD 39.22 million by 2032, at a CAGR of 4.9% during the forecast period. Africa holds a 2% share and represents the least penetrated region in the adhesion barriers market. Limited access to surgical care, low awareness, and constrained budgets restrict broader adoption. It is in the early stages of development, with few hospitals integrating adhesion barriers into standard practices. South Africa and Egypt are emerging as focal points for market entry, supported by medical tourism and regional partnerships. Local training initiatives and government-led health reforms are expected to improve long-term adoption. The market remains dependent on donor support and public-private collaborations for expansion.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Sanofi S.A.

- Becton Dickinson and Company

- Baxter International, Inc.

- Johnson & Johnson

- Anika Therapeutics, Inc.

- FzioMed, Inc.

- Mast Biosurgery, Inc.

- Innocoll Holdings PLC

- Atrium Medical Corporation (a part of Getinge Group)

- Conifer Health Solutions, LLC

Competitive Analysis:

The Adhesion Barriers Market features a moderately consolidated competitive landscape, led by established players with strong portfolios and global distribution networks. Key companies focus on product innovation, regulatory approvals, and strategic partnerships to strengthen market presence. It includes firms offering film, gel, and spray formulations designed for use across various surgical procedures. Competition intensifies as manufacturers invest in expanding indications and securing clinical validation to differentiate their offerings. Emerging players are entering with specialized solutions tailored to minimally invasive surgeries and niche applications. The market also sees growing collaboration between medical institutions and suppliers to develop customized, procedure-specific products. It remains dynamic, driven by technological advancement, surgeon preferences, and regional expansion strategies that aim to balance performance with affordability.

Recent Developments:

- In June 2025, Sanofi announced the acquisition of Blueprint Medicines, a biopharmaceutical company specializing in rare immunological diseases. This strategic move expands Sanofi’s portfolio in rare disease treatments and adds promising early-stage immunology assets to its pipeline. The acquisition notably brings Ayvakit/Ayvakyt, the only approved medicine for advanced and indolent systemic mastocytosis, further strengthening Sanofi’s position in the immunology sector.

- In October 2024, Baxter International extended its strategic partnership with Oneview Healthcare, a provider of patient experience solutions. The partnership, initially focused on the U.S., has now expanded to include Canada. This collaboration aims to improve patient engagement and operational efficiency in healthcare facilities through advanced technology integration and a joint product roadmap.

- In September 2024, Becton Dickinson and Company (BD) revealed its acquisition of Edwards Lifesciences’ Critical Care product group for $4.2 billion. This acquisition is designed to enhance BD’s smart connected care solutions and further its presence in the monitoring technology market, particularly benefiting operating rooms and intensive care units. The transaction is expected to close by the end of 2025, pending regulatory approvals.

Market Concentration & Characteristics:

The Adhesion Barriers Market exhibits moderate to high market concentration, with a few multinational companies controlling a significant share through established brands and patented technologies. It is characterized by strong regulatory oversight, high entry barriers, and product differentiation based on material composition, ease of application, and clinical efficacy. The market favors companies with extensive R&D capabilities and a track record of successful clinical trials. Product adoption depends heavily on surgical compatibility and practitioner familiarity, influencing competitive positioning. It shows a strong preference for bioresorbable and biocompatible materials, reflecting a broader shift toward patient-centric surgical solutions. Demand patterns vary across regions, shaped by healthcare infrastructure, reimbursement frameworks, and surgeon training levels.

Report Coverage:

The research report offers an in-depth analysis based on product, formulation, and application. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Rising demand for minimally invasive surgeries will drive the need for compatible adhesion barrier solutions.

- Ongoing product innovation will enhance material safety, ease of use, and resorption rates.

- Expanding surgical volumes in Asia Pacific will position the region as a key growth engine.

- Increased clinical awareness will promote earlier integration of adhesion barriers into standard surgical protocols.

- Strategic partnerships between hospitals and manufacturers will boost product customization and access.

- Advancements in biodegradable polymers will improve market appeal among eco-conscious healthcare systems.

- Wider insurance coverage and reimbursement support will enable adoption in cost-sensitive markets.

- Regulatory clarity across developing regions will streamline product approvals and market entry.

- Surge in outpatient procedures and ambulatory surgical centers will expand use cases.

- Growing investment in healthcare infrastructure across emerging economies will sustain long-term growth.