Market Overview:

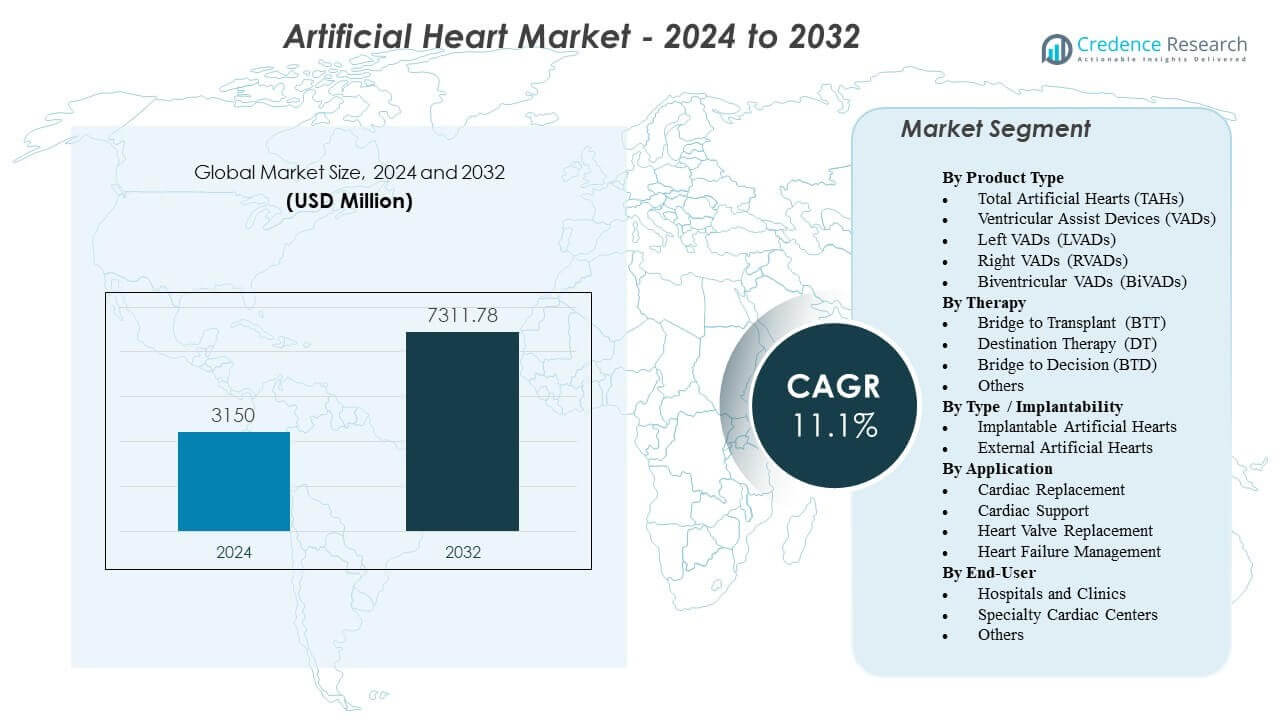

The Artificial Heart Market is projected to grow from USD 3,150 million in 2024 to an estimated USD 7,311.78 million by 2032, with a CAGR of 11.1% from 2024 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Artificial Heart Market Size 2024 |

USD 3,150 million |

| Artificial Heart Market, CAGR |

11.1% |

| Artificial Heart Market Size 2032 |

USD 7,311.78 million |

Rapid technological advancements fuel market expansion, supported by innovations in biomaterials, pump engineering, and energy transfer systems. Manufacturers enhance device durability, reduce thrombus risk, and improve physiological responsiveness through magnetically levitated rotors, adaptive flow algorithms, and better hemodynamic sensors. Growing heart failure prevalence and limited donor organ availability increase reliance on mechanical circulatory support in high-risk patients. Hospitals adopt advanced platforms to stabilize complex cases and support patients who cannot undergo immediate transplantation. These drivers strengthen overall acceptance across specialized cardiac centers.

North America leads the Artificial Heart Market due to advanced cardiac surgery infrastructure, high procedural volumes, and strong clinical training programs. Europe follows with broad adoption supported by structured regulatory frameworks and strong transplant networks across Germany, France, and the UK. Asia-Pacific is emerging rapidly, driven by rising heart failure incidence, expanding hospital capacity, and growing investment in cardiac care technology in countries such as Japan, China, and India. Improvements in surgeon training, hospital capability, and access to high-end implants accelerate regional uptake across developing economies.

Market Insights:

- The Artificial Heart Market is projected to grow from USD 3,150 million in 2024 to USD 7,311.78 million by 2032, expanding at a CAGR of 11.1% during the forecast period.

- Market growth is driven by rising end-stage heart failure cases, limited donor organ availability, and stronger clinical outcomes delivered by advanced artificial heart and ventricular assist technologies.

- Restraints emerge from high device costs, complex surgical requirements, and the need for specialized post-implant care, which limits adoption in resource-constrained healthcare systems.

- North America leads the market due to advanced cardiac centers and high procedural capacity, while Europe maintains strong uptake supported by structured regulatory pathways.

- Asia-Pacific shows the fastest growth because of expanding cardiac surgery infrastructure, rising disease burden, and increasing investment in mechanical circulatory support technologies.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising Heart Failure Prevalence And Declining Donor Organ Availability

The Artificial Heart Market gains momentum due to the growing number of patients living with severe heart failure across major healthcare regions. Donor shortages restrict transplant options, which pushes hospitals to adopt long-term mechanical support. High-risk patients benefit from improved survival rates supported by newer devices. Healthcare professionals rely on these systems to stabilize complex cases when surgery delays occur. Device performance improves through better flow control and durable internal components. Patients with limited treatment choices receive support that improves daily activity levels. Clinical teams trust modern systems due to strong reliability metrics. The technology strengthens cardiac care programs worldwide.

- For instance, the SynCardia TAH from SynCardia Systems delivers up to 9.5 L/min total cardiac output with a 70-cc pumping chamber, supporting complete circulatory replacement when transplant wait times exceed months

Advancements In Pump Design, Biomaterials, And Power Delivery Systems

Engineering upgrades reshape the Artificial Heart Market with better hemodynamic performance and reduced device wear. Manufacturers develop smoother internal surfaces to cut friction and improve compatibility. Stronger polymers extend device life under demanding conditions. Compact energy units reduce the need for frequent external adjustments. Engineers integrate smarter controllers that respond to rapid physiological changes. Power modules support stable output that protects patient safety. Next-generation materials help reduce clotting risks. Hospitals prefer devices that lower complications for critical patients.

Growing Clinical Validation And Stronger Regulatory Support Across Regions

Regulators increase approvals for next-generation systems, which strengthens confidence in the Artificial Heart Market. Trials show improved therapy outcomes for patients with limited treatment choices. Hospitals expand their adoption when supported by clear clinical guidelines. Surgeons value data showing reduced pump failures across extended timelines. Government programs support research teams to introduce safer circulatory support devices. Strong review frameworks help shorten approval timelines without reducing safety standards. Clinical adoption rises when payers recognize improved patient stabilization. This shift supports stronger long-term market growth.

Expansion Of Specialized Cardiac Centers And Improved Surgical Expertise

Advanced cardiac centers invest in experienced teams that support the Artificial Heart Market through successful implant procedures. Surgeons gain exposure to advanced training models that improve decision-making. Hospitals integrate simulation systems to reduce operative risks. Skilled staff manage post-implant care with higher accuracy. Better patient monitoring enhances outcomes during recovery. Healthcare networks coordinate long-term follow-up programs to maintain patient safety. Clinical infrastructure upgrades reduce failure rates after implantation. Adoption improves when hospitals invest in dedicated cardiovascular units.

- For example, high-volume U.S. transplant centers performing more than 50 VAD implants per year report improved success rates due to standardized HeartMate 3 surgical protocols and integrated hemodynamic monitoring tools.

Market Trends

Shift Toward Miniaturized And Fully Implantable Device Architectures

Emerging designs reshape the Artificial Heart Market with compact structures that support broader patient groups. Manufacturers develop systems that reduce external hardware dependency. Surgeons prefer devices that simplify operative workflows without raising risks. Compact pumps improve comfort for mobile patients. Miniaturization helps clinicians treat younger patients with smaller thoracic cavities. Engineers improve internal components to reduce heat buildup during extended use. Battery innovation supports longer device performance between charges. This shift helps expand device feasibility across diverse clinical profiles.

- For example, the HeartMate 3 LVAD by Abbott Laboratories uses a magnetically levitated rotor operating at speeds between 3,000–9,000 RPM, which lowers friction and device heat generation while maintaining up to 10 L/min flow.

Integration Of Smart Monitoring, AI-Based Control, And Predictive Analytics

Innovative control software enables real-time device adjustments within the Artificial Heart Market. Hospitals integrate predictive analytics to support rapid intervention decisions. AI modules study flow patterns to detect irregularities before complications occur. Remote monitoring tools allow specialists to evaluate patient progress outside hospitals. Surgeons rely on automated data dashboards that reduce manual tracking. Engineers design sensors that measure pressure shifts with greater precision. Monitoring platforms improve patient comfort by reducing unnecessary hospital visits. The digital shift supports safer long-term therapy.

- For instance, the Aeson TAH uses an embedded sensor-driven algorithm that adjusts beat rate automatically between 35–180 beats per minute to match physiological demand, based on continuous pressure and flow monitoring.

Growing Use Of Hybrid Mechanical Circulatory Support Platforms

Clinical teams explore hybrid platforms within the Artificial Heart Market that combine short-term and long-term support features. This approach helps treat patients with shifting hemodynamic needs. Hybrid systems bridge gaps between temporary stabilization and durable mechanical pumps. Surgeons gain flexibility in tailoring therapy precisely. Stronger transition pathways reduce the need for repeat operations. Engineers develop modular components that fit multiple patient scenarios. Programs support safer upgrades when patient conditions evolve. Hospitals value platforms that improve treatment continuity.

Increasing Adoption In Emerging Economies With Expanding Cardiac Care Infrastructure

Expanding healthcare networks give the Artificial Heart Market stronger penetration across developing regions. Governments support new cardiac units in major hospitals. Patient awareness improves through national heart failure programs. More training centers prepare surgeons for complex implant procedures. Import pathways become smoother when supported by clearer regulations. Hospitals expand advanced surgery budgets to include circulatory support systems. Local distributors increase supply chain strength for life-support devices. Demand rises as cardiac disease rates climb in urban populations.

Market Challenges Analysis

High Procedure Costs, Limited Reimbursement, And Intensive Maintenance Needs

Cost barriers limit growth within the Artificial Heart Market due to expensive devices and extended hospital care requirements. Reimbursement gaps reduce access for patients in regions with weaker healthcare funding. Maintenance protocols demand specialized staff and routine evaluations. Some hospitals struggle to manage training needs for complex systems. Power units and accessories increase lifetime therapy expenses for families. Device failure risks require strict monitoring procedures. Regulatory reviews extend development timelines for new versions. These hurdles reduce adoption in cost-sensitive markets.

Clinical Complications, Surgical Complexity, And Long-Term Durability Concerns

Complications create major concerns for the Artificial Heart Market as clinicians work to reduce clotting and infection risks. Some patients face recovery challenges after extended surgeries. Long procedures raise strain on surgical teams without adequate support systems. Internal pump wear still impacts device reliability in certain cases. Durability questions slow approval in regions that require extensive validation data. Follow-up care demands strong coordination between hospitals and home-care teams. Surgeons often face learning curve challenges for advanced implant models. These issues limit broad-scale deployment.

Market Opportunities

Growing Scope For Next-Generation Devices With Better Durability And Expanded Patient Eligibility

Technological progress expands opportunities in the Artificial Heart Market through pumps with longer life cycles and reduced complication profiles. Better biomaterials help support wider patient groups who previously lacked treatment options. Miniaturized pumps increase suitability for smaller adults and younger patients. Engineers refine surface coatings to reduce thrombus formation. Improved implant techniques reduce post-operative recovery strain. Hospitals value devices that lower readmission rates. Manufacturers gain new entry points in regions upgrading cardiac units. Stronger designs improve therapy confidence among clinicians.

Rapid Expansion Of Global Heart Failure Burden And Focus On Strengthened Cardiac Infrastructure

Healthcare networks expand opportunities for the Artificial Heart Market while responding to rising heart failure cases in urban and aging populations. Investment in cardiac centers increases surgical capacity. Governments support advanced therapy programs to reduce mortality. Hospitals adopt diagnostic tools that improve patient selection for implants. Training programs help surgeons master complex procedures with better accuracy. Organizations promote awareness campaigns that highlight long-term survival improvements. These developments support long-term device uptake. Demand strengthens as access improves across emerging regions.

Market Segmentation Analysis:

By Product Type

The Artificial Heart Market expands through strong demand for Total Artificial Hearts and advanced Ventricular Assist Devices. TAHs support patients with end-stage cardiac failure who require full replacement therapy. VADs gain wider acceptance due to their durability and lower surgical burden. LVADs lead usage because they stabilize left ventricular dysfunction in a broad patient pool. RVADs remain important for right-sided support in critical cases. BiVADs assist patients with complex biventricular failure who need balanced flow control. Hospitals choose devices based on severity and long-term treatment goals. Product diversity strengthens therapy flexibility across cardiac programs.

- For example, CARMAT’s Aeson TAH uses bioprosthetic surfaces and an adaptive pumping algorithm that adjusts flows up to 7 L/min for physiologic response.

By Therapy

Therapy segmentation shapes the Artificial Heart Market through expanding roles of BTT, DT, and BTD pathways. BTT dominates due to rising transplant wait times and urgent stabilization needs. DT supports patients who cannot undergo transplant due to age or medical limitations. BTD helps clinicians evaluate long-term care plans for unstable patients. Other therapies include temporary support for post-operative recovery. Each pathway aligns device choice with patient condition. Hospitals favor structured therapy protocols to improve survival. Clinical teams rely on clear treatment categories to improve decision-making.

By Type / Implantability

Implantability categories influence the Artificial Heart Market by separating fully implantable and external systems. Implantable devices support patient mobility and reduce dependence on external controllers. These systems offer stronger long-term comfort. External devices assist patients needing short-term stabilization before advanced surgery. Hospitals use external platforms for rapid deployment in emergency cases. Implantable systems remain preferred for extended therapy. Engineers refine both types to reduce complications. Clear implant categories help physicians match therapy needs with device complexity.

By Application

Applications guide development priorities in the Artificial Heart Market through cardiac replacement and support needs. Cardiac replacement devices support patients with irreversible heart damage. Cardiac support systems stabilize patients with partial ventricular dysfunction. Heart valve replacement integration expands device use in multi-condition cases. Heart failure management remains the broadest category due to rising global disease incidence. Each application serves defined clinical goals. Hospitals prioritize systems with proven survival benefits. Application diversity strengthens adoption across various patient profiles.

- For instance, Total Artificial Hearts maintain systemic pressures within a controlled 90–140 mmHg range and deliver consistent biventricular output that supports organ perfusion even in severe circulatory collapse. Clinical evaluations show that these devices sustain full cardiac replacement for months to years with stable flow dynamics and low mechanical fatigue rates.

By End-User

End-user segmentation directs adoption patterns in the Artificial Heart Market through hospitals, specialty cardiac centers, and other care settings. Hospitals and clinics lead due to strong surgical infrastructure and post-operative support capabilities. Specialty cardiac centers deliver care for complex heart failure cases requiring advanced devices. These centers invest in skilled surgical teams and monitoring units. Other settings include emergency care units that stabilize high-risk patients before referral. End-user preference depends on availability of trained staff. Strong infrastructure supports reliable treatment outcomes. Steady upgrades in care facilities improve long-term adoption.

Segmentation:

By Product Type

- Total Artificial Hearts (TAHs)

- Ventricular Assist Devices (VADs)

- Left VADs (LVADs)

- Right VADs (RVADs)

- Biventricular VADs (BiVADs)

By Therapy

- Bridge to Transplant (BTT)

- Destination Therapy (DT)

- Bridge to Decision (BTD)

- Others

By Type / Implantability

- Implantable Artificial Hearts

- External Artificial Hearts

By Application

- Cardiac Replacement

- Cardiac Support

- Heart Valve Replacement

- Heart Failure Management

By End-User

- Hospitals and Clinics

- Specialty Cardiac Centers

- Others

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America holds the largest share of the Artificial Heart Market with a strong lead supported by advanced cardiac care infrastructure and broad reimbursement coverage. Hospitals in the region adopt high-end circulatory support systems due to rising prevalence of end-stage heart failure. The U.S. drives demand with a high concentration of trained cardiac surgeons and transplant centers. Canada strengthens adoption through structured national heart failure programs. The region benefits from ongoing clinical trials that validate device performance. It keeps the highest market share due to strong innovation pipelines and rapid regulatory approvals.

Europe maintains the second-largest share supported by expanding adoption in Germany, France, and the UK. The Artificial Heart Market gains traction through well-established transplant programs and strong collaboration between cardiac institutions. Hospitals focus on advanced ventricular assist devices to manage growing heart failure cases. Regulatory bodies support safer device introduction through clear evaluation pathways. It demonstrates solid uptake in countries with strong investment in surgical training. Southern and Eastern Europe show emerging demand as cardiac centers upgrade their infrastructure. Increased awareness improves therapy acceptance across multiple care settings.

Asia-Pacific records the fastest growth and holds an expanding share driven by high cardiac disease prevalence and rapid healthcare modernization. Key countries such as Japan, China, and India expand cardiac surgery programs to meet rising patient loads. The Artificial Heart Market benefits from government-backed hospital expansions in urban centers. It gains further traction through improving access to advanced implant procedures. Training initiatives help build local expertise for complex device implantation. Strong investment in domestic med-tech manufacturing also supports supply chain strength. Growing middle-class populations accelerate long-term demand.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- SynCardia Systems, LLC

- CARMAT

- Abbott Laboratories

- Abiomed (Johnson & Johnson)

- BiVACOR Inc.

- Jarvik Heart, Inc.

- Medtronic plc

- Berlin Heart GmbH

- CryoLife, Inc.

- ReliantHeart, Inc.

- Terumo Corporation

- LivaNova PLC

- Getinge AB

Competitive Analysis:

Competition within the Artificial Heart Market intensifies as global and emerging companies expand their device portfolios and clinical evidence. Leading companies strengthen their advantage with durable pump designs, enhanced biocompatible materials, and improved control systems. It gains further momentum through strategic mergers, technology licensing, and multi-center clinical studies. Companies focus on long-term reliability to support both transplant-eligible and transplant-ineligible patients. New entrants introduce compact, fully implantable platforms that improve patient comfort and mobility. Established players maintain leadership through strong surgeon training programs and global distribution networks. Continuous innovation shapes product differentiation and strengthens industry competitiveness.

Recent Developments:

- In January 2026, SynCardia Systems entered into a development collaboration with Hydrix to advance the Emperor, their next-generation fully implantable Total Artificial Heart.

Report Coverage:

The research report offers an in-depth analysis based on Product Type, Therapy, Type / Implantability, Application, and End-User. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Growth accelerates with expanding adoption of advanced implantable systems that support patients with complex heart failure conditions.

- Rising transplant wait times increase reliance on long-term mechanical circulatory support across major cardiac centers worldwide.

- Strong innovation in biomaterials improves durability and lowers complication risk for next-generation devices.

- AI-enabled flow control enhances device responses to rapid physiological changes and improves treatment precision.

- Smaller, lighter pumps expand eligibility for younger patients and individuals with limited anatomical space.

- Hybrid platforms gain attention for supporting patients transitioning between temporary and permanent therapy pathways.

- Regulatory environments strengthen clinical evidence requirements, improving overall device safety outcomes.

- Training investments build specialized cardiac teams capable of managing advanced implant procedures.

- Emerging economies expand infrastructure, widening access to high-end mechanical support therapies.

- Strategic partnerships between manufacturers and research institutions drive faster development of fully implantable designs.