Biopsy Devices Market Overview:

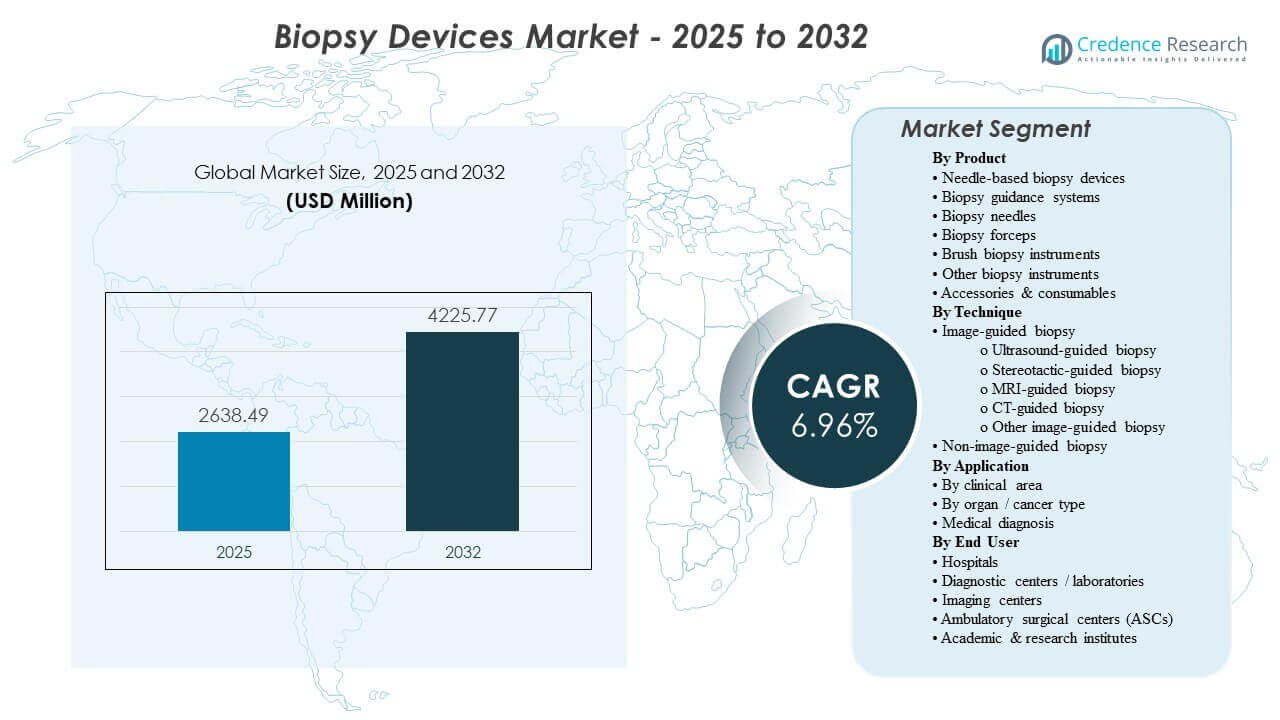

The global Biopsy Devices Market size was estimated at USD 2638.49 million in 2025 and is expected to reach USD 4225.77 million by 2032, growing at a CAGR of 6.96% from 2025 to 2032. Demand is primarily driven by sustained growth in diagnostic biopsy volumes across oncology and organ-specific pathways, where earlier detection and confirmation testing increase procedure throughput in hospitals and imaging-led settings. Adoption of image-guided workflows and single-use consumables further supports recurring purchasing, while Asia Pacific’s expanding diagnostic infrastructure is increasingly shaping global volume growth.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Biopsy Devices Market Size 2025 |

USD 2638.49 million |

| Biopsy Devices Market, CAGR |

6.96% |

| Biopsy Devices Market Size 2032 |

USD 4225.77 million |

Key Market Trends & Insights

- The market is projected to expand at a CAGR of 96% during 2025–2032, reflecting steady growth in diagnostic procedure volumes and device replacement cycles.

- Asia Pacific led regional demand with a 8% share in 2025, supported by expanding imaging capacity and rising cancer diagnostic penetration.

- Needle-based biopsy devices accounted for the largest product share of 6% in 2025, underpinned by routine use in core and fine-needle sampling workflows.

- Breast applications represented 4% share in 2025, sustained by high screening follow-ups and standardized image-guided biopsy pathways.

- Hospitals held a 3% share in 2025, reflecting concentration of complex cases and integrated imaging–pathology infrastructure.

Segment Analysis

Demand is increasingly shaped by the need for reliable tissue acquisition that supports precision diagnostics, including broader use of image guidance to improve targeting confidence and reduce repeat sampling. Providers are also tightening infection-control standards, reinforcing the shift toward single-use needles and compatible disposables that standardize workflow and reduce reprocessing burden. As procedure volumes rise, organizations prioritize devices that shorten setup time, improve sampling consistency, and integrate smoothly with imaging modalities used in breast, lung, and gastrointestinal pathways.

Technology adoption is also influenced by workflow standardization across multi-site networks, where consistent device platforms simplify training, quality assurance, and reporting comparability. Growth in outpatient and distributed care settings supports demand for compact, efficient systems and consumables that fit high-throughput procedural environments. Over the forecast period, vendors that pair device performance with training, service, and modality compatibility are better positioned to capture recurring purchasing tied to consumables and refresh cycles.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Product Insights

Needle-based biopsy devices accounted for the largest share of 43.6% in 2025. This leadership is supported by their routine use across core sampling and fine-needle procedures in multiple clinical pathways, including breast, lung, and gastrointestinal diagnostics. Broad modality compatibility and predictable sampling performance strengthen adoption in both high-volume hospital settings and imaging-led centers. Ongoing product refinement focused on ergonomics, tip geometry, and tissue yield consistency further reinforces purchasing preference.

By Technique Insights

Image-guided biopsy leads technique adoption because guidance improves targeting precision in small, deep, or anatomically complex lesions and supports minimally invasive care pathways. Ultrasound and CT guidance expand applicability across soft-tissue and thoracic procedures, enabling wider use in both hospital and outpatient environments. Workflow tools that reduce procedure-time variability and improve targeting confidence increase utilization in high-throughput settings. Non-image-guided approaches remain relevant where lesion accessibility is straightforward or where imaging resources are limited, supporting continued baseline demand.

By Clinical Area Insights

Oncology-driven biopsy demand remains structurally strong because tissue confirmation and biomarker testing are increasingly embedded in diagnosis, staging, and therapy selection. Gastroenterology sampling continues to expand as endoscopic ultrasound and advanced endoscopy workflows increase targeted tissue acquisition for submucosal and pancreatic lesions. Bone and bone marrow biopsy volumes stay supported by hematologic diagnostics, monitoring, and treatment-response assessment. Together, these clinical pathways sustain steady utilization across devices and recurring consumables.

By Organ / Cancer Type Insights

Breast accounted for the largest share of 30.4% in 2025. This is supported by high screening participation, frequent diagnostic follow-ups, and established image-guided biopsy protocols that standardize care across provider networks. The breadth of compatible devices for stereotactic, ultrasound, and MR-guided workflows supports consistent procurement patterns. Continued emphasis on minimizing repeat procedures and improving tissue adequacy sustains demand for devices that deliver reliable sampling performance.

By End User Insights

Hospitals accounted for the largest share of 67.3% in 2025. Hospitals concentrate complex diagnostic pathways, integrated imaging resources, and pathology capabilities that support end-to-end biopsy workflows. They also manage higher-acuity cases that require multi-modality guidance and robust complication management infrastructure. Standardization across departments and sites reinforces demand for consistent device platforms and dependable service support.

Biopsy Devices Market Drivers

Rising cancer detection and biopsy confirmation volumes

Cancer detection pathways increasingly rely on tissue confirmation and characterization, sustaining biopsy procedure volumes across multiple organs. Growing adoption of biomarker-driven therapy selection increases the need for adequate, high-quality sampling. Higher diagnostic throughput also supports replacement and upgrade cycles for devices that improve sampling reliability. As clinical protocols standardize, providers prioritize platforms that reduce repeat sampling and streamline workflow.

- For instance, Hologic states that its Brevera Breast Biopsy System can provide specimen information in as little as 8 seconds per core, deliver an average time saving of 12 minutes per procedure, and reduce time spent per procedure by 25%, supporting faster throughput while maintaining biopsy workflow efficiency.

Expansion of image-guided and minimally invasive procedural workflows

Image guidance improves lesion targeting confidence and supports minimally invasive approaches that reduce recovery time and procedural variability. Wider availability of ultrasound and CT capacity expands the addressable base of guided biopsy procedures. Imaging-led workflows also reinforce demand for device portfolios designed for modality compatibility and procedural efficiency. This driver supports both capital equipment-linked purchasing and recurring demand for compatible consumables.

- For instance, XACT Robotics reported a lung biopsy case in which its ACE robotic system achieved 0.8 mm tip-to-target accuracy, reached the lesion within 3 minutes, and navigated a 33.6 mm trajectory to sample an 8 x 16 mm target, highlighting the precision gains possible in image-guided minimally invasive biopsy workflows.

Shift toward single-use devices and recurring consumables demand

Infection-control priorities and reprocessing burdens are accelerating the preference for single-use needles and associated consumables. Disposable formats support consistent performance and reduce turnaround time between cases, improving throughput. This increases the recurring revenue component of the market, particularly in high-volume centers. Vendors that provide broad consumables coverage and reliable supply continuity gain purchasing preference.

Growth of outpatient diagnostics and distributed care delivery

A rising share of diagnostic activity is shifting toward ambulatory and imaging center environments for suitable biopsy workflows. Distributed care delivery increases demand for compact, standardized systems that can be deployed across multiple sites. Operational constraints favor devices that shorten setup time and simplify training requirements. This driver broadens the customer base beyond large tertiary hospitals and supports steady unit demand.

Biopsy Devices Market Challenges

Procurement can be constrained by budget pressure, especially where diagnostic reimbursement levels do not fully support frequent technology refresh cycles. Facilities often balance performance improvements against lifecycle service costs, training requirements, and consumables pricing, which can slow standardization decisions. In lower-resource settings, limited access to imaging guidance infrastructure can restrict the adoption of advanced biopsy workflows. Variability in clinical practice patterns also influences device preference and complicates vendor efforts to drive uniform adoption.

Procedure-related risk management and quality expectations create additional hurdles, particularly for complex organ sampling where targeting accuracy and tissue adequacy are critical. Providers demand evidence of consistent performance across operators and settings, raising the bar for product validation, training, and support. Workflow integration challenges can emerge when devices must align with multiple imaging modalities and reporting systems. Supply continuity for disposables and accessories can also become a decision factor for large networks seeking predictable throughput.

- For instance, Intuitive reports that in a multicenter study of 155 subjects with small pulmonary nodules of median 14 mm, its Ion shape-sensing robotic-assisted bronchoscopy platform used with Siemens Healthineers’ Cios Spin mobile cone-beam CT achieved a 91% diagnostic yield, 91.5% sensitivity for malignancy, and 0% pneumothorax incidence, demonstrating the kind of quantified performance and multimodality compatibility that providers increasingly expect in advanced biopsy workflows.

Biopsy Devices Market Trends and Opportunities

Workflow standardization is becoming a central purchasing criterion as multi-site networks aim for consistent procedure protocols and comparable diagnostic quality. This supports demand for device families that integrate well with imaging workflows and reduce operator-to-operator variability. Opportunities increase for vendors that complement hardware with training, procedural guidance tools, and service models tailored to high-throughput environments. Standardization also encourages multi-year purchasing agreements that stabilize recurring consumables demand.

An additional opportunity lies in expanding precision diagnostics requirements, which increases the importance of tissue adequacy and sampling quality. Devices that deliver consistent core samples and reduce repeat procedures gain traction in oncology and organ-specific pathways. Growing adoption of imaging-led diagnostics in emerging markets supports increased penetration of image-guided biopsy workflows. Vendors that align portfolios to modality compatibility and supply reliability are better positioned to capture both capital and consumables-led growth.

- For instance, in a study published in Archives of Medical Science covering 802 patients, Devicor’s Mammotome vacuum-assisted biopsy system achieved a 99.6% diagnostic concordance rate and a 1.6% pathological underestimation rate, compared with 94.7% and 37.3%, respectively, for core needle biopsy, underscoring the clinical value of stronger tissue acquisition performance.

Regional Insights

North America

North America accounted for 31.4% share in 2025, supported by high diagnostic procedure volumes, established screening pathways, and broad access to imaging-guided interventions. Providers emphasize sampling quality, workflow efficiency, and consistent outcomes, reinforcing demand for advanced needle-based systems and compatible consumables. Hospital networks and large imaging providers also drive platform standardization and multi-site procurement. Ongoing replacement and upgrade cycles sustain demand alongside recurring consumables purchasing.

Europe

Europe held a 23.9% share in 2025, reflecting mature diagnostic infrastructure and steady utilization across hospital and imaging-led settings. Standardized care pathways and strong clinical governance support adoption of devices that improve consistency and reduce repeat procedures. Procurement often weighs lifecycle cost, service support, and consumables continuity, shaping vendor competition. Demand remains stable with incremental growth linked to workflow upgrades and efficiency improvements.

Asia Pacific

Asia Pacific led with a 31.8% share in 2025, driven by expanding imaging capacity, rising diagnostic penetration, and growing procedure volumes in major markets. Increased access to guided interventions supports adoption of modality-compatible biopsy devices and standardized consumables. Providers prioritize scalable workflows that can be deployed across growing networks of hospitals and diagnostic centers. The region’s volume expansion creates strong opportunities for both device placement and recurring consumables.

Latin America

Latin America represented 7.2% share in 2025, with growth shaped by uneven infrastructure and reimbursement variability across countries. Demand is supported by expanding private-sector diagnostics and gradual modernization of imaging-led biopsy workflows in major urban centers. Procurement often emphasizes affordability, service availability, and supply stability for disposables. Continued growth is likely to be concentrated in higher-capacity hospital systems and leading diagnostic networks.

Middle East & Africa

Middle East & Africa accounted for 5.7% share in 2025, with demand concentrated in higher-capacity markets and private hospital groups. Investments in diagnostic infrastructure and specialist services support adoption of guided biopsy workflows in key hubs. However, variability in access and coverage limits broader penetration across the region. Vendors that provide robust training and reliable consumables supply can capture growth in expanding centers.

Competitive Landscape

Competition is driven by portfolio breadth across biopsy devices and consumables, with differentiation centered on sampling consistency, modality compatibility, and workflow efficiency in high-throughput settings. Vendors compete on procedure reliability, ease of use, and the ability to support standardized protocols across multi-site provider networks. Service models, training support, and supply continuity for disposables influence long-term contracts and preferred-vendor status. Innovation focus increasingly targets workflow simplification, improved tissue yield, and compatibility across imaging-guided pathways.

BD’s positioning is strengthened by its emphasis on integrated biopsy workflows, combining device performance with procedural standardization and compatibility across imaging environments. The company’s approach typically aligns product updates with clinical workflow needs, aiming to improve sampling reliability and reduce repeat procedures in high-volume settings. Portfolio breadth across needles and related consumables supports recurring demand and procurement continuity for large provider networks. This combination of workflow alignment and consumables coverage supports competitiveness in hospital-led purchasing.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- BD (Becton, Dickinson and Company)

- Hologic, Inc.

- Medtronic plc

- Boston Scientific Corporation

- Cardinal Health, Inc.

- Cook Medical / Cook Group

- Argon Medical Devices, Inc.

- Olympus Corporation

- FUJIFILM Corporation / FUJIFILM Holdings

- B. Braun SE / B. Braun Melsungen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focus

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In February 2026, Virchow Medical entered a partnership with the Project Santa Fe Foundation to expand the use of Virchow’s Crow’s Nest Biopsy Catchment System and Virchow Vault biorepository, with the aim of improving the capture and use of biopsy-derived biospecimens for oncology analytics.

- In January 2026, Olympus announced the U.S. launch of its SecureFlex single-use fine needle biopsy device, designed for endoscopic ultrasound-guided tissue sampling and intended to help clinicians reach difficult lesions such as those in the pancreatic head and uncinate process.

- In May 2025, BiBB Instruments signed a letter of intent with TaeWoong Medical USA for the U.S. commercialization of the EndoDrill GI powered biopsy instrument, following FDA clearance and the company’s first U.S. sales earlier in 2025.

- In November 2024, Mammotome launched the Mammotome AutoCore Single Insertion Core Biopsy System, which the company described as the first automated spring-loaded core needle device on the market, with U.S. FDA clearance already in place.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 2638.49 million |

| Revenue forecast in 2032 |

USD 4225.77 million |

| Growth rate (CAGR) |

6.96% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026–2032 |

| Quantitative units |

USD million |

| Segments covered |

By Product Outlook: Needle-based biopsy devices, Biopsy guidance systems, Biopsy needles, Biopsy forceps, Brush biopsy instruments, Other biopsy instruments, Accessories & consumables;

By Technique Outlook: Image-guided biopsy (Ultrasound-guided biopsy, Stereotactic-guided biopsy, MRI-guided biopsy, CT-guided biopsy, Other image-guided biopsy approaches), Non-image-guided biopsy;

By Application Outlook: By clinical area (Oncology, Gastroenterology, Bone / bone marrow biopsy),

By organ / cancer type (Breast, Lung, Colorectal, Prostate, Kidney, Bone marrow), Medical diagnosis & related diagnostic use cases;

By End User Outlook: Hospitals, Diagnostic centers / laboratories, Imaging centers, Ambulatory surgical centers (ASCs), Academic & research institutes |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

BD (Becton, Dickinson and Company), Hologic, Inc., Medtronic plc, Boston Scientific Corporation, Cardinal Health, Inc., Cook Medical / Cook Group, Argon Medical Devices, Inc., Olympus Corporation, FUJIFILM Corporation / FUJIFILM Holdings, B. Braun SE / B. Braun Melsungen AG |

| No. of Pages |

325 |

Segmentation

By Product

- Needle-based biopsy devices

- Biopsy guidance systems

- Biopsy needles

- Biopsy forceps

- Brush biopsy instruments

- Other biopsy instruments

- Accessories & consumables

By Technique

- Image-guided biopsy [Ultrasound-guided biopsy, Stereotactic-guided biopsy, MRI-guided biopsy, CT-guided biopsy, Other image-guided biopsy approaches]

- Non-image-guided biopsy

By Application

- By clinical area [Oncology, Gastroenterology, Bone / bone marrow biopsy]

- By organ / cancer type [Breast, Lung, Colorectal, Prostate, Kidney, Bone marrow]

- Medical diagnosis & related diagnostic use cases

By End User

- Hospitals

- Diagnostic centers / laboratories

- Imaging centers

- Ambulatory surgical centers (ASCs)

- Academic & research institutes

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa