Market Overview

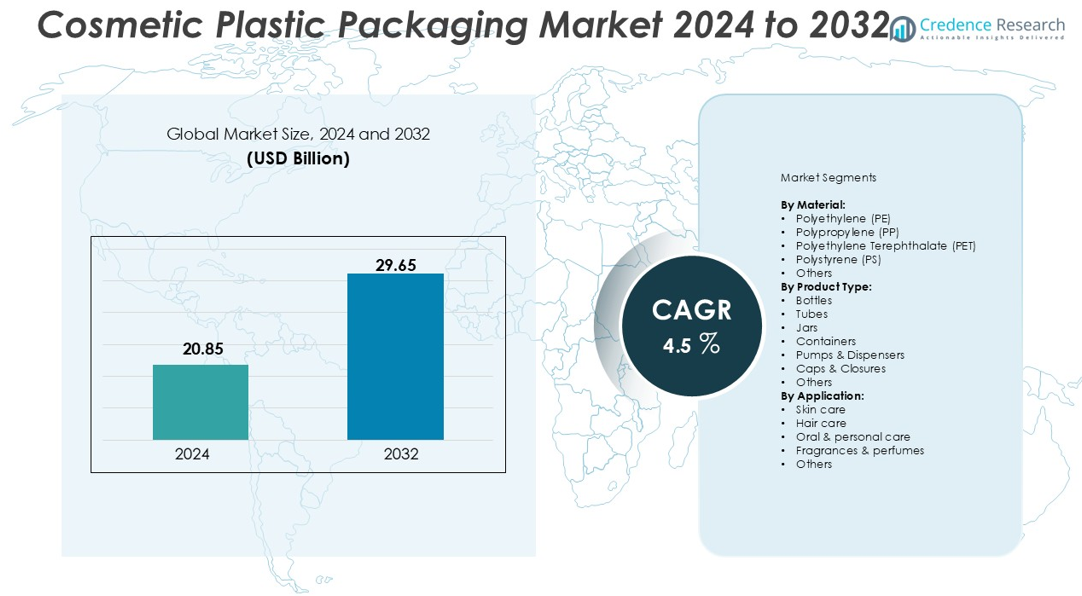

The cosmetic plastic packaging market size was valued at USD 20.85 billion in 2024 and is anticipated to reach USD 29.65 billion by 2032, at a CAGR of 4.5% during the forecast period

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Cosmetic Plastic Packaging Market Size 2024 |

USD 20.85 billion |

| Cosmetic Plastic Packaging Market, CAGR |

4.5% |

| Cosmetic Plastic Packaging Market Size 2032 |

USD 29.65 billion |

The cosmetic plastic packaging market is led by prominent players such as Amcor, Berry Global, Aptar Group, and Albea, which collectively account for a major share of global revenue through their strong product portfolios and global manufacturing networks. These companies focus on sustainable materials, innovative dispensing solutions, and premium packaging designs to meet the evolving needs of cosmetic brands. Other notable participants, including Gerresheimer, AG Poly Packs, Cosmopacks, and Green Earth Packaging, are expanding through customized and eco-friendly solutions. Regionally, Asia-Pacific dominates the market with an estimated 35% share in 2024, driven by high cosmetic consumption, growing e-commerce, and cost-effective production capabilities.

Market Insights

- The global cosmetic plastic packaging market was valued at USD 20.85 billion in 2024 and is projected to reach USD 29.65 billion by 2032, growing at a CAGR of 4.5% during the forecast period.

- Market growth is primarily driven by rising demand for sustainable, lightweight, and aesthetically appealing packaging solutions across skincare, hair care, and personal care segments, with PET material holding the largest share due to its recyclability and durability.

- Key trends include the adoption of refillable and recyclable packaging systems, digital printing for customization, and the growing influence of e-commerce and premium beauty products on packaging innovation.

- The market is moderately competitive, with major players such as Amcor, Berry Global, Aptar Group, and Albea focusing on eco-friendly designs, product innovation, and strategic collaborations to expand global presence.

- Asia-Pacific dominates the market with a 35% share, followed by North America (28%) and Europe (25%), reflecting strong regional cosmetic consumption and manufacturing capacities.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Material:

The cosmetic plastic packaging market by material is dominated by Polyethylene Terephthalate (PET), accounting for the largest market share in 2024. PET’s superior transparency, durability, and recyclability make it the preferred choice for premium cosmetic packaging. Its lightweight nature and resistance to impact enhance portability and product safety, driving demand across skincare and personal care products. Polypropylene (PP) and Polyethylene (PE) follow closely, owing to their flexibility and cost-effectiveness. Increasing consumer preference for sustainable and recyclable materials continues to boost the adoption of PET-based packaging solutions.

- For instance, Amcor’s new in-line operation in Paris, Texas, is expected to produce approximately 50 million hot-fillable PET bottles each year, enhancing operational efficiencies and sustainability.

By Product Type:

Among product types, bottles hold the dominant share in the cosmetic plastic packaging market, supported by their widespread use in skincare, hair care, and fragrance applications. Bottles offer excellent shelf appeal, ease of use, and design versatility, which attract major cosmetic brands. Growing innovation in lightweight and eco-friendly bottle designs also contributes to their dominance. Meanwhile, tubes and jars are gaining traction for compact and travel-friendly cosmetic products. Rising consumer awareness about product hygiene and controlled dispensing further drives demand for pumps, dispensers, and closures.

- For instance, Aptar’s Future Airless PET® is the first high-capacity, e-commerce-capable, and recyclable PET airless packaging solution for beauty brands, offering a sustainable alternative to traditional packaging.

By Application:

The skincare segment leads the cosmetic plastic packaging market by application, capturing the largest market share in 2024. The surge in global skincare consumption, driven by increasing awareness of personal grooming and anti-aging trends, has accelerated demand for aesthetic and functional packaging. Plastic packaging in skincare ensures product protection from contamination and UV exposure, enhancing shelf life. The hair care and personal care segments also show strong growth potential due to rising disposable incomes and urbanization. Customization, portability, and sustainable packaging innovations remain key growth drivers across all applications.

Key Growth Drivers

Rising Demand for Sustainable and Eco-Friendly Packaging

Growing environmental awareness among consumers and regulatory pressures on reducing plastic waste are driving the adoption of sustainable packaging materials in the cosmetic plastic packaging market. Manufacturers are increasingly shifting toward recyclable, biodegradable, and refillable plastic options such as bio-based PET and post-consumer recycled (PCR) plastics. Major cosmetic brands are investing in circular economy initiatives and green packaging innovations to meet sustainability goals and appeal to eco-conscious buyers. This shift not only enhances brand image but also encourages the development of innovative material technologies that reduce environmental impact while maintaining product quality and aesthetics.

- For instance, L’Oréal used 73,707 tonnes of recycled materials in 2021 in its packaging lines, including 43,373 tonnes in primary and secondary packaging, thereby replacing equivalent virgin plastic volumes.

Expanding Cosmetic and Personal Care Industry

The rapid expansion of the global cosmetic and personal care industry is a primary growth driver for the cosmetic plastic packaging market. Rising disposable incomes, urbanization, and evolving beauty standards have significantly boosted the consumption of skincare, hair care, and fragrance products. Plastic packaging remains the material of choice for its lightweight, durability, cost-effectiveness, and design flexibility. The surge in e-commerce beauty product sales also amplifies the demand for protective and visually appealing packaging. Additionally, the proliferation of men’s grooming and organic beauty products continues to broaden market opportunities, reinforcing steady demand across diverse cosmetic categories.

- For instance, Unilever reported that in 2023, 22 percent of its global plastic packaging was made from recycled content, up from 21 percent in 2022 (i.e. if its total plastic portfolio is 1,000,000 tonnes, then 220,000 tonnes used recycled content).

Innovation in Design and Functional Packaging Solutions

Technological advancements and design innovation are reshaping the cosmetic plastic packaging landscape. Brands are investing in smart, functional, and aesthetically appealing packaging that enhances user experience and strengthens brand identity. Features such as airless pumps, precision dispensers, and tamper-evident closures are gaining popularity for improving hygiene and product longevity. Furthermore, digital printing and customization capabilities enable personalized branding and limited-edition packaging, appealing to the premium and luxury cosmetic segments. These innovations not only drive differentiation in a competitive market but also encourage greater consumer engagement and brand loyalty, thereby fostering long-term growth.

Key Trends & Opportunities

Growth of Refillable and Recyclable Packaging Systems

A significant market trend is the growing adoption of refillable and recyclable cosmetic packaging solutions. Leading brands are launching refill pods, modular packaging, and returnable systems to minimize waste and reduce carbon footprints. This trend aligns with sustainability regulations and shifting consumer expectations toward responsible consumption. Companies leveraging advanced recycling technologies, such as chemical recycling, are gaining a competitive edge by producing high-quality recycled resins suitable for cosmetic-grade applications. The opportunity lies in developing cost-effective, scalable, and attractive refillable systems that maintain both functionality and luxury appeal, meeting the dual goals of sustainability and customer satisfaction.

- For instance, L’Oréal Groupe expanded the number of refillable packaging options by a factor of 17 over five years across its brands.

Rising Influence of E-commerce and Digital Branding

The global rise of e-commerce platforms has transformed packaging requirements in the cosmetic industry. Online retail demands durable, lightweight, and visually appealing packaging capable of withstanding transportation while preserving product integrity. Plastic packaging meets these needs effectively and allows brands to experiment with eye-catching digital printing and design innovation for virtual shelf appeal. Furthermore, unboxing experiences and influencer-driven marketing have made packaging a critical brand touchpoint. Companies that integrate smart labeling, QR codes, and augmented reality (AR) elements into their packaging designs can enhance digital engagement and consumer loyalty, creating new opportunities for growth.

Key Challenges

Environmental Concerns and Regulatory Pressures

One of the foremost challenges in the cosmetic plastic packaging market is addressing environmental concerns and meeting stringent regulatory requirements. Governments and international agencies are imposing restrictions on single-use plastics and mandating higher recycling rates. Compliance with these evolving standards increases production costs and operational complexities for manufacturers. In addition, consumer backlash against excessive plastic use has intensified, pressuring companies to adopt sustainable alternatives without compromising aesthetics or affordability. Balancing innovation, cost-efficiency, and environmental responsibility remains a critical challenge that requires ongoing R&D investment

Fluctuating Raw Material Prices and Supply Chain Constraints

The volatility in crude oil prices, which directly affects the cost of plastic resins like PET, PE, and PP, poses a significant challenge to market stability. Unpredictable price fluctuations disrupt manufacturing margins and affect overall profitability. Moreover, global supply chain disruptions—driven by geopolitical tensions, trade restrictions, or logistical bottlenecks—have impacted the timely availability of raw materials and packaging components. These issues compel manufacturers to diversify suppliers, explore alternative materials, and invest in localized production. Building supply chain resilience and cost-effective sourcing strategies is essential to maintaining competitive advantage in a dynamic market environment

Regional Analysis

North America:

North America holds a significant share of the global cosmetic plastic packaging market, accounting for around 28% in 2024. The region’s strong demand stems from the high consumption of premium skincare, hair care, and personal grooming products. The presence of established cosmetic brands and growing adoption of sustainable and recyclable plastic materials drive market growth. Consumers’ preference for convenient, travel-friendly, and aesthetically designed packaging further supports product innovation. Additionally, stringent environmental regulations and increasing investment in eco-friendly packaging technologies are expected to sustain steady growth in the North American market over the forecast period.

Europe:

Europe captures approximately 25% of the global cosmetic plastic packaging market, driven by strong environmental awareness and regulatory mandates promoting sustainability. Countries such as Germany, France, and the U.K. are key contributors, emphasizing recyclable and bio-based plastic packaging solutions. The rising popularity of luxury cosmetics and the shift toward minimalist, refillable packaging designs enhance regional demand. European manufacturers are also leading innovations in circular economy practices, including post-consumer recycled (PCR) materials and closed-loop systems. The market continues to benefit from the region’s mature cosmetic industry and growing preference for eco-conscious, high-quality packaging alternatives.

Asia-Pacific:

Asia-Pacific dominates the cosmetic plastic packaging market with the largest share of around 35% in 2024. Rapid urbanization, rising disposable incomes, and expanding middle-class populations in countries like China, India, Japan, and South Korea are fueling market growth. The booming e-commerce and beauty retail sectors drive high consumption of lightweight and durable packaging. Additionally, increasing awareness of personal grooming and Western beauty trends supports continuous demand. Local manufacturers are investing in cost-effective and innovative packaging designs, while sustainability initiatives are gaining traction, positioning Asia-Pacific as the fastest-growing regional market through 2032.

Latin America:

Latin America accounts for nearly 7% of the global cosmetic plastic packaging market, with Brazil and Mexico emerging as key contributors. The region’s market growth is supported by a thriving beauty and personal care industry, particularly in skincare and hair care categories. Affordable plastic packaging options remain in high demand due to the region’s price-sensitive consumer base. Increasing adoption of modern packaging formats such as pumps, dispensers, and recyclable plastics is enhancing product appeal. While sustainability awareness is still evolving, global cosmetic brands’ regional expansions are expected to drive long-term growth in Latin America.

Middle East & Africa:

The Middle East & Africa region holds about 5% of the global cosmetic plastic packaging market in 2024. Market growth is driven by increasing demand for premium cosmetics, rising disposable incomes, and expanding retail infrastructure. Countries like the UAE, Saudi Arabia, and South Africa are witnessing a surge in personal care consumption influenced by urbanization and lifestyle changes. The adoption of durable and lightweight packaging materials supports growth across skincare and fragrance segments. Although sustainability initiatives are emerging gradually, the region presents strong opportunities for international brands and packaging manufacturers to expand their footprint

Market Segmentations:

By Material:

- Polyethylene (PE)

- Polypropylene (PP)

- Polyethylene Terephthalate (PET)

- Polystyrene (PS)

- Others

By Product Type:

- Bottles

- Tubes

- Jars

- Containers

- Pumps & Dispensers

- Caps & Closures

- Others

By Application:

- Skin care

- Hair care

- Oral & personal care

- Fragrances & perfumes

- Others

By Geography:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The competitive landscape of the cosmetic plastic packaging market is characterized by the presence of several global and regional players focusing on innovation, sustainability, and strategic expansion. Key companies such as Amcor, Berry Global, Aptar Group, and Albea dominate the market through advanced product designs, eco-friendly materials, and smart packaging solutions. These players invest heavily in R&D to develop recyclable, lightweight, and aesthetically appealing packaging that meets evolving consumer preferences and regulatory standards. Emerging participants like AG Poly Packs, Cosmopacks, and Green Earth Packaging are strengthening their positions through customized solutions and cost-effective manufacturing. Strategic partnerships, mergers, and acquisitions are common, enabling companies to enhance their product portfolios and expand geographic reach. The growing focus on circular economy practices and sustainable innovation continues to reshape competition, compelling both established and new entrants to balance functionality, design, and environmental responsibility in their packaging offerings.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Amcor

- Berry Global

- Aptar Group

- Albea

- Gerresheimer

- AG Poly Packs

- Cosmopacks

- APackaging Group

- Blakelin Plastics

- Green Earth Packaging

- Harman Packaging

- Guangzhou Keyuan Plasticware

- Jarsking

Recent Developments

- In March 2024, GEKA introduced the post-consumer-recycled (PCR) polypropylene (PP) material which is suitable for primary cosmetic packaging. It helps in reducing Co2 emissions by 75% and offers high quality colors to increase the visual appeal of the product.

- In June 2023, Respectueuse, known for its eco-friendly cosmetics, launched a product line which utilizes Sonoco’s rigid paper, EnviroStick Packaging. The company has launched this specifically for its deodorant products across the market.

- In February 2023, WWP Beauty, a company with strong focus on eco-conscious packaging and turnkey solutions for the beauty industry, announced the launch of its sustainable and eco-smart collections and refillable packaging solutions.

Report Coverage

The research report offers an in-depth analysis based on Material, Product Type, Application, and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The cosmetic plastic packaging market is expected to witness steady growth driven by increasing global demand for personal care and beauty products.

- Manufacturers will continue to focus on sustainable and recyclable packaging materials to meet environmental regulations.

- Innovation in refillable and reusable packaging formats will gain strong momentum among premium and mass-market brands.

- Smart packaging technologies, including QR codes and digital labeling, will enhance consumer engagement and brand transparency.

- Lightweight, durable, and travel-friendly packaging designs will remain a top priority for cosmetic brands.

- The rise of e-commerce and direct-to-consumer beauty sales will boost demand for protective and visually appealing packaging.

- Asia-Pacific will continue to lead the market, supported by strong manufacturing bases and expanding beauty industries.

- Collaborations between packaging producers and cosmetic brands will accelerate innovation and design efficiency.

- Bioplastics and post-consumer recycled materials will see increased adoption across product lines.

- Customization and aesthetic differentiation will remain key strategies for maintaining brand competitiveness.