Market Overview

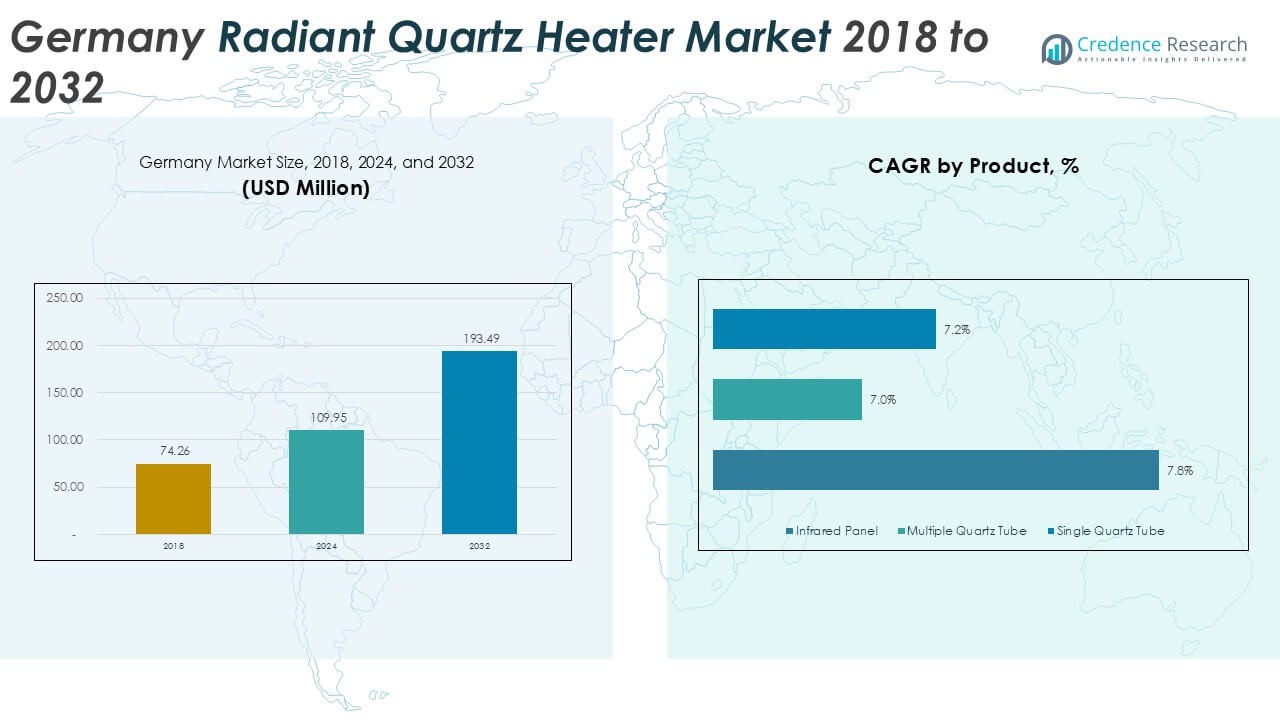

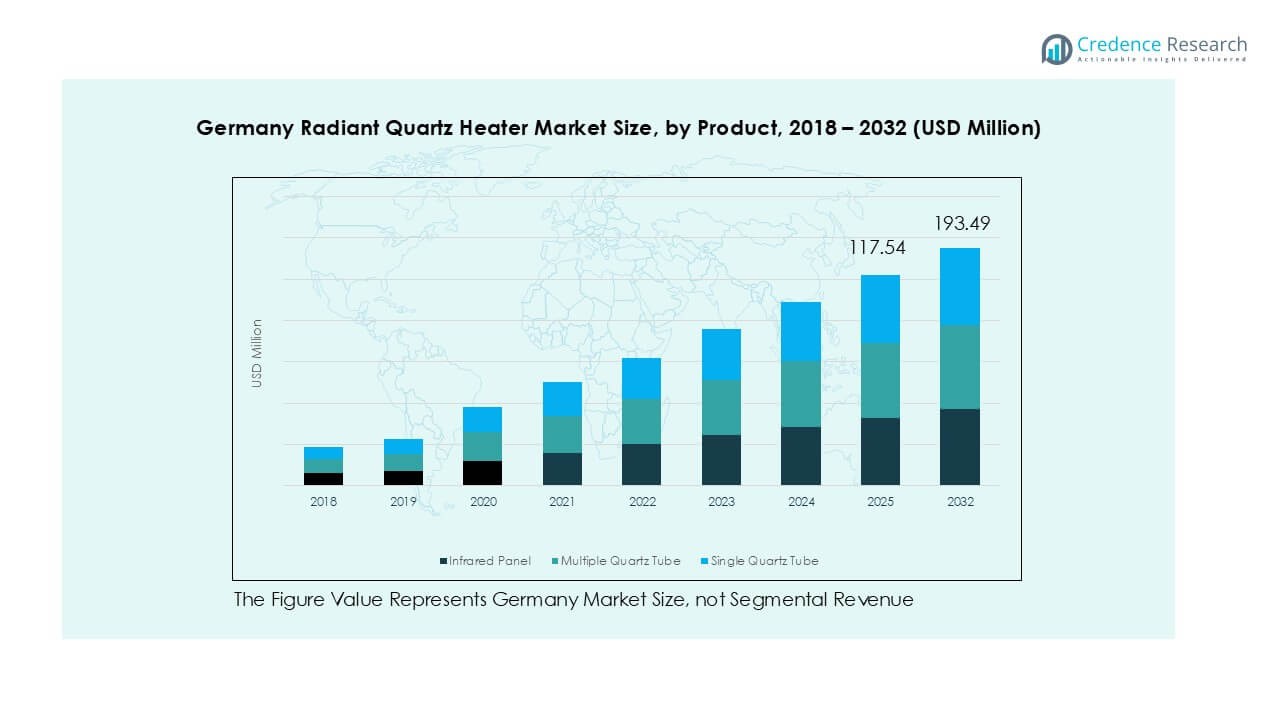

Germany Radiant Quartz Heater market size was valued at USD 74.26 million in 2018 to USD 109.95 million in 2024 and is anticipated to reach USD 193.49 million by 2032, at a CAGR of 7.3% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Germany Radiant Quartz Heater Market Size 2024 |

USD 109.95 Million |

| Germany Radiant Quartz Heater Market, CAGR |

7.3% |

| Germany Radiant Quartz Heater Market Size 2032 |

USD 193.49 Million |

The Germany radiant quartz heater market features a mix of global manufacturers and European specialists competing on safety, performance, and pricing. Leading players focus on mid-wattage and multi-quartz tube models to meet residential demand. Strong brand presence, certified safety features, and wide retail distribution support competitive positioning. Southern Germany leads the market with about 32% share, driven by colder winters, higher household incomes, and strong renovation activity. Northern Germany follows with nearly 27% share, supported by coastal climate conditions and demand for fast supplemental heating. Western Germany accounts for around 25%, reflecting dense urban housing, while Eastern Germany holds roughly 16%, driven by affordability-focused demand and replacement sales.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Germany radiant quartz heater market grew from USD 109.95 million in 2024 and is projected to reach USD 193.49 million by 2032, expanding at about 7.3% CAGR during the forecast period.

- Rising demand for energy-efficient and zone-based space heating drives market growth, as households seek quick warmth with controlled electricity use, especially in apartments and rental homes.

- Product trends favor multiple quartz tube heaters, which hold around 42% segment share due to higher heat output, while the 1000–1500-watt segment leads with nearly 47% share because of balanced efficiency and coverage.

- Competition remains moderate, with global and European brands focusing on safety features, mid-wattage models, offline retail strength, and growing online price competition.

- Southern Germany leads regionally with about 32% market share, followed by Northern Germany at 27%, Western Germany at 25%, and Eastern Germany at 16%, reflecting climate, income, and housing differences.

Market Segmentation Analysis:

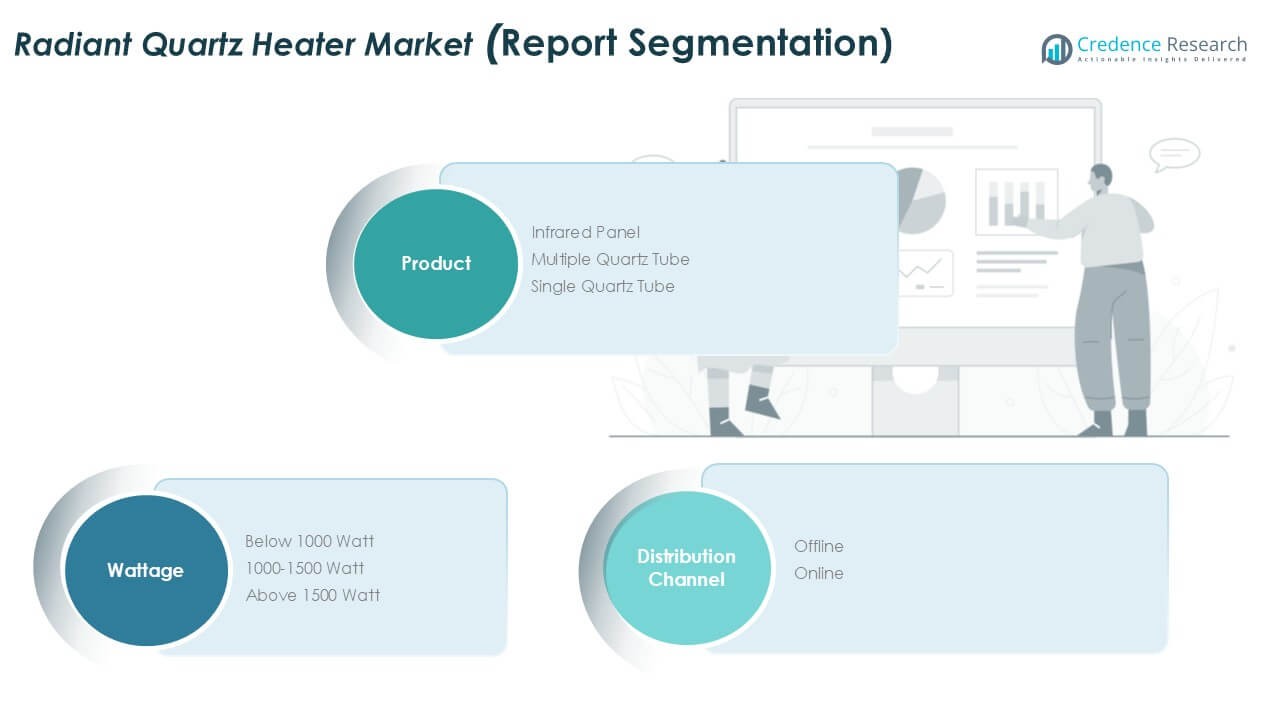

By Product

The product segment shows clear demand differences across heater designs in Germany. Multiple quartz tube heaters lead the segment, holding about 42% market share. Strong heat output and faster warm-up drive adoption in larger rooms. Commercial and semi-outdoor users prefer this design for stable performance. Infrared panel heaters follow, supported by slim designs and wall-mount options. Single quartz tube models serve cost-sensitive buyers seeking basic heating. Energy efficiency rules and space-heating needs continue to favor multi-tube systems across homes and workplaces.

- For instance, a typical portable electric infrared quartz heater may use four quartz heating tubes and operate at 1,500 watts, delivering effective radiant spot heating for areas generally up to 15 square meters (approximately 160 square feet), depending on room insulation and ambient conditions.

By Wattage Segment

The 1000–1500-watt segment dominates the wattage category with nearly 47% market share. Balanced power use and effective room coverage support strong demand. German households favor this range for bedrooms and living spaces. These models meet heating needs without high electricity strain. Below 1000-watt units serve personal and spot heating uses. Above 1500-watt heaters attract garages and workshops. Rising energy costs push consumers toward mid-wattage products that balance comfort, safety, and operating expenses.

- For instance, the Stiebel Eltron IW 120 infrared quartz heater operates at 1,200 watts (at max setting), provides immediate heat (within seconds), and is rated for small rooms up to approximately 8 to 10 square meters, aligning with residential safety limits and standards for domestic use.

By Distribution Channel

Offline channels remain dominant, accounting for about 61% of total sales. Consumers prefer in-store evaluation for safety-certified heating products. Specialist appliance stores and DIY chains support strong visibility. Staff guidance and installation advice strengthen buyer trust. Online sales grow steadily through e-commerce platforms and brand websites. Price comparison tools and seasonal discounts support online adoption. Urban buyers show faster online shift. However, offline retail remains critical due to regulatory awareness and preference for physical inspection before purchase.

Key Growth Drivers

Rising Demand for Energy-Efficient Space Heating

Energy efficiency remains a primary growth driver in Germany’s radiant quartz heater market. Households face rising electricity tariffs and tighter energy budgets. Quartz heaters deliver rapid heat with lower warm-up losses. This feature supports efficient short-duration heating. Many German homes prefer zone heating over central systems. Radiant quartz technology fits this preference well. Users heat occupied areas only. This approach lowers overall energy use. Government efficiency awareness programs reinforce this shift. Consumers increasingly compare wattage output to heat performance. Compact quartz heaters score well on this metric. Improved reflector designs enhance heat direction. Reduced standby losses also improve appeal. Together, these factors sustain strong demand across residential and small commercial spaces.

- For instance, Stiebel Eltron’s IW 120 infrared quartz heater operates at 1,200 watts, reaches full radiant output in under 2 seconds, and is designed to heat rooms up to 12 square meters, supporting efficient zone heating.

Growth in Renovation and Retrofit Activities

Germany’s aging building stock supports steady heater demand. Many older homes lack modern heating infrastructure. Radiant quartz heaters offer simple retrofit solutions. Installation does not require ducting or plumbing. Renters and landlords favor such flexibility. Urban apartments benefit from space-saving heater designs. Temporary heating needs also drive purchases. Renovation cycles often trigger appliance upgrades. Quartz heaters serve as supplemental heating options. Construction delays and phased renovations increase reliance on portable heaters. Builders use quartz units during interior finishing stages. These patterns support repeat and seasonal demand. Retrofit-friendly features remain a key purchase driver.

- For instance, AEG’s QH 1500 quartz heater operates at 1,500 watts, weighs 2.6 kilograms, and supports freestanding or wall-mounted use, making it suitable for renovation and temporary heating needs.

Expansion of E-Commerce and Product Availability

Wider product availability supports market growth. Online platforms list extensive heater models and specifications. Consumers access detailed wattage and safety information. Reviews influence buying decisions strongly. Seasonal promotions increase sales volumes. Brands reach customers beyond physical store limits. Smaller manufacturers gain national exposure online. Faster logistics improve delivery timelines. Urban buyers value doorstep delivery convenience. Online channels also support price-sensitive segments. Transparent pricing builds buyer confidence. Although offline remains strong, digital access expands the overall market base. This distribution expansion sustains long-term growth momentum.

Key Trends & Opportunities

Shift Toward Smart and Safety-Enhanced Heaters

Safety-focused innovation creates strong market opportunities. Consumers prioritize overheat protection and tip-over shutoff. Quartz heater brands integrate automatic cut-off systems. Improved grills reduce burn risk. Families and elderly users value these features. Some models add timers and remote controls. These features improve comfort and energy control. Smart plugs further extend usability. Regulatory focus on electrical safety supports adoption. Premium models command higher margins. Manufacturers use safety certification as a key differentiator. This trend supports product upgrades and value growth.

- For instance, Stiebel Eltron’s IW 120 infrared quartz heater operates at 1,200 watts with electrical protection rated to IPX4 (splashproof), making it suitable for indoor and covered outdoor installation, such as in bathrooms or on covered patios.

Demand for Compact and Aesthetic Heating Solutions

Design-driven demand presents new opportunities. Urban living spaces favor compact heaters. Slim infrared and quartz designs suit modern interiors. Consumers prefer neutral colors and minimal forms. Wall-mount options improve space efficiency. Retailers highlight design alongside performance. Hospitality and office spaces also demand discreet heating. Seasonal pop-up venues use portable units. These use cases expand beyond residential demand. Design-led innovation helps brands target premium buyers. Aesthetic appeal increasingly influences purchase decisions.

- For instance, Klarstein’s HeatPal Marble infrared heater delivers 1,300 watts of power, features dimensions (including the base) of approximately 25 cm in depth, and is a freestanding device not suitable for wall mounting. It has a modern design with brushed aluminum elements, marketed for use in living rooms and offices.

Key Challenges

High Electricity Prices and Operating Cost Concerns

Electricity costs present a major challenge. Germany maintains some of Europe’s highest power tariffs. Consumers closely track heater energy use. Extended heater operation raises monthly bills. This concern limits adoption in colder months. Buyers may restrict usage duration. Some households switch to alternative heating sources. Price sensitivity affects premium model sales. Manufacturers face pressure to prove efficiency claims. Clear energy labeling becomes essential. Without cost reassurance, buyers delay purchases. Operating cost anxiety remains a structural restraint.

Competition from Alternative Heating Technologies

The market faces strong competition from substitutes. Heat pumps gain popularity through subsidies. Oil-filled radiators attract cost-conscious users. Fan heaters offer lower upfront prices. Central heating upgrades reduce supplemental heater demand. Infrared panels also compete within the segment. Consumers compare lifetime costs carefully. Policy support favors long-term heating systems. Quartz heaters face perception as secondary solutions. Brands must position products clearly. Failure to differentiate reduces market traction. Competitive pressure limits pricing flexibility and margin expansion.

Regional Analysis

Northern Germany

Northern Germany accounts for about 27% of the Germany radiant quartz heater market. Colder coastal climates and high humidity drive steady demand for fast-acting heating solutions. Households favor radiant quartz heaters for quick warmth during short heating cycles. Apartments and rental housing dominate urban areas like Hamburg and Bremen. These conditions support demand for portable and mid-wattage heaters. Energy efficiency awareness remains strong across the region. Seasonal weather variability increases supplemental heating needs. Commercial spaces, including warehouses and small workshops, also adopt quartz heaters. Stable residential demand anchors regional market performance.

Southern Germany

Southern Germany represents the largest regional market, holding nearly 32% market share. Colder winters and higher household income levels support strong adoption. Bavaria and Baden-Württemberg show high penetration of premium and multi-quartz tube models. Consumers emphasize performance, safety, and design quality. Detached homes and larger living spaces drive demand for higher wattage units. Renovation activity remains strong in suburban areas. Energy-conscious buyers still prefer zone heating solutions. Retail appliance chains maintain high sales volumes. The region benefits from strong purchasing power and consistent winter demand patterns.

Western Germany

Western Germany captures around 25% of the national market. Dense urban populations in North Rhine–Westphalia drive steady heater sales. Apartments and mixed-use buildings favor compact quartz heaters. Short heating durations suit radiant technology well. Consumers often use heaters as supplementary solutions. Retail presence remains strong through DIY and appliance stores. Commercial demand arises from offices and small retail spaces. Price sensitivity influences buying decisions in this region. Mid-range wattage products see high turnover. Stable population density supports consistent year-round demand.

Eastern Germany

Eastern Germany holds roughly 16% of the Germany radiant quartz heater market. Lower average household income affects purchasing behavior. Consumers focus on affordability and basic functionality. Single quartz tube and lower wattage models dominate sales. Older housing stock increases reliance on supplemental heating. Rental apartments drive portable heater demand. Winters remain cold, supporting seasonal sales spikes. Offline retail remains important for price comparison. Government energy awareness programs influence buyer choices. While smaller in size, the region shows steady replacement-driven demand growth.

Market Segmentations:

By Product

- Infrared Panel

- Multiple Quartz Tube

- Single Quartz Tube

By Wattage Segment

- Below 1000 Watt

- 1000–1500 Watt

- Above 1500 Watt

By Distribution Channel

By Geography

- Northern Germany

- Southern Germany

- Western Germany

- Eastern Germany

Competitive Landscape

The Germany radiant quartz heater market shows moderate competition with a mix of global brands and regional manufacturers. International players such as Lasko, TPI Corporation, and Pelonis Technologies compete on scale, pricing, and broad product portfolios. European and domestic companies focus on compliance, build quality, and safety standards. Product differentiation centers on wattage range, safety features, and design. Offline retail remains the main battleground, supported by seasonal promotions. Online platforms intensify price competition and visibility. Companies invest in energy-efficient components and compact designs. Private-label offerings from retailers add pricing pressure. Brand trust and certification influence buyer choice. Strategic focus remains on mid-wattage models and reliable performance.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Red Rad

- Convectronics

- Tempco Electric Heater Corporation

- Döbeln Elektrowärme GmbH

- Lasko Products, LLC

- TPI Corporation

- Pelonis Technologies, Inc.

- Duraflame, Inc.

- SPACE-RAY

- CLARKE INTERNATIONAL

Recent Developments

- In June 2023, The European Union revised its overarching Energy Efficiency Directive, and new, stricter Ecodesign standards for local space heaters, including radiant heaters, were adopted in April 2024 and will apply from July 1, 2025.

- In January 2023, Honeywell announced a new line of smart radiant quartz heaters with integrated Wi-Fi capabilities.

Report Coverage

The research report offers an in-depth analysis based on Product, Wattage Segment, Distribution Channel and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand will grow as households prefer zone heating over full central systems.

- Energy efficiency concerns will shape product design and buyer decisions.

- Mid-wattage heaters will remain the most preferred category.

- Safety-certified and auto shut-off features will gain stronger importance.

- Compact and wall-mounted designs will see wider adoption.

- Online sales will expand faster than offline channels.

- Seasonal weather variation will continue to drive replacement demand.

- Urban apartments will remain the core end-use segment.

- Competition will intensify around pricing and feature differentiation.

- Manufacturers will focus on durable, low-maintenance heating solutions.