Green Food Market Overview:

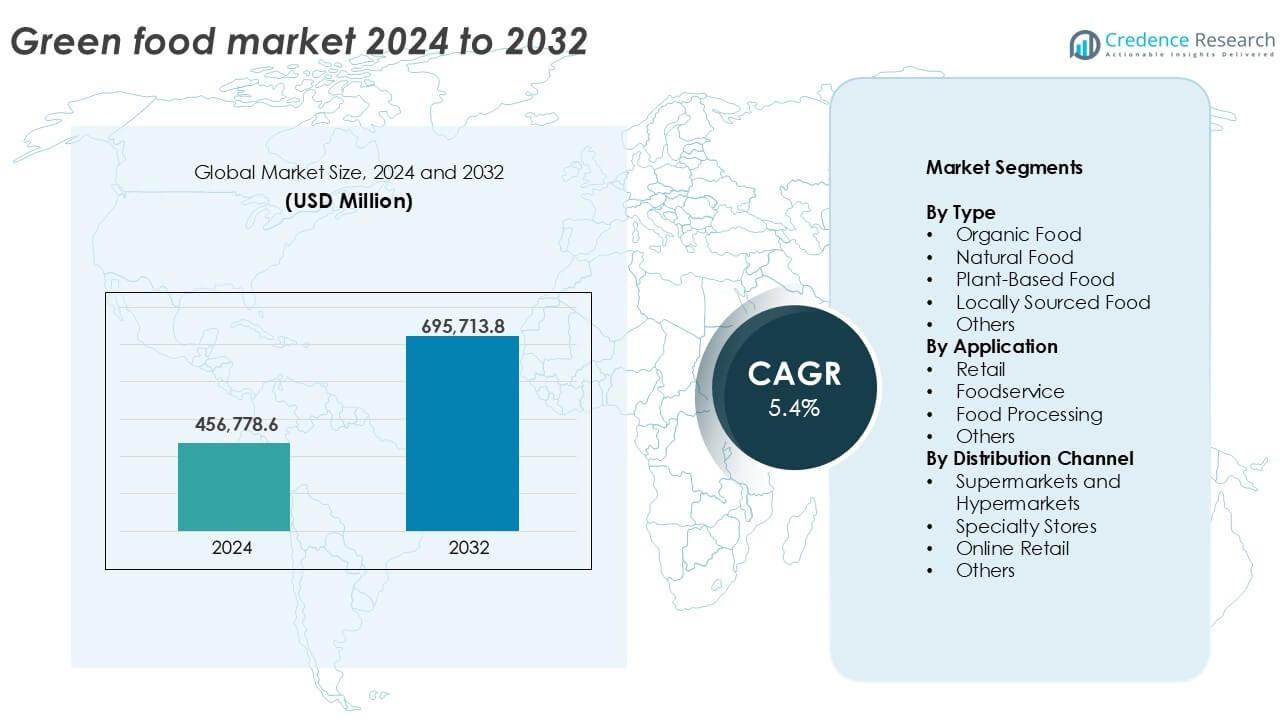

The Green Food Market size was valued at USD 456,778.6 million in 2024 and is anticipated to reach USD 695,713.8 million by 2032, at a CAGR of 5.4% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Green Food Market Size 2024 |

USD 456,778.6 million |

| Green Food Market, CAGR |

5.4% |

| Green Food Market Size 2032 |

USD 695,713.8 million |

Green Food Market Insights

- Rising consumer demand for organic, plant-based, and natural foods is driving growth across retail and foodservice channels.

- Key trends include increased adoption of clean-label, non-GMO, and alternative protein products across developed and emerging economies.

- Leading players such as Danone, General Mills, and The Hain Celestial Group dominate through product innovation and acquisitions, while smaller brands grow via online retail.

- North America leads the market with a 30.2% share, followed by Europe at 28%, while organic food holds the highest share by type at over 35%.

Green Food Market Segmentation Analysis:

By Type

Organic Food dominates the green food market by type, accounting for over 35% of the total market share in 2024. Its growth is driven by rising consumer awareness of chemical-free farming and health benefits associated with organic produce. Regulatory support and certifications also enhance consumer trust. Plant-Based Food follows closely, fueled by vegan lifestyle trends and increasing lactose intolerance cases. Natural and locally sourced food segments show strong regional traction due to freshness, low carbon footprint, and community support. The “Others” category captures niche categories like eco-labeled and fair-trade food.

- For instance, Whole Foods Market operates over 500 stores in North America and the UK selling certified organic food products.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Application

Retail leads the market by application, contributing more than 45% of revenue share in 2024. It benefits from the growing number of organic and health-focused aisles in supermarkets and convenience stores. Shoppers actively seek eco-friendly options for daily consumption. Foodservice is gaining momentum, supported by plant-based menu integration in restaurants and cafés. Food Processing sees stable demand as manufacturers introduce clean-label packaged goods. The “Others” segment includes institutional buyers like schools and hospitals incorporating green food into nutrition programs.

- For instance, Panera Bread removed more than 150 artificial ingredients from its U.S. menu to meet clean‑food demand.

By Distribution Channel

Supermarkets and Hypermarkets dominate the distribution channel segment with over 40% share in 2024. These stores offer wide assortments, visibility, and easy access to certified green food products. Specialty Stores follow due to their curated, health-focused selections catering to niche buyers. Online Retail shows the fastest growth, driven by e-commerce expansion, doorstep delivery convenience, and digital marketing of organic products. The “Others” segment includes direct farm sales and cooperative models that appeal to locally conscious buyers seeking traceable sources.

Key Growth Drivers

Rising Consumer Awareness of Health and Sustainability

The green food market is primarily driven by a surge in consumer awareness regarding health, nutrition, and environmental impact. Shoppers increasingly choose food products that are free from harmful pesticides, preservatives, and GMOs. This shift in preference supports organic, plant-based, and locally sourced food. Sustainability-focused campaigns and growing concerns about climate change encourage the adoption of eco-friendly diets. Regulatory frameworks mandating clean labeling and sustainable sourcing further reinforce trust in green food. As lifestyle diseases rise, health-conscious consumers now view food as a preventive tool, promoting consistent demand growth across both developed and emerging markets.

- For instance, Sprouts Farmers Market offers around 200 varieties of organic produce across approximately 478 stores in 24 U.S. states, promoting diet choices tied to sustainability and nutrition.

Expansion of Retail Infrastructure and E-Commerce Platforms

The growth of modern retail formats and digital marketplaces is a strong enabler for the green food sector. Supermarkets and hypermarkets have expanded their organic and health-food sections, while specialty stores cater to niche preferences with curated selections. Online platforms enable small producers to reach wider audiences without large capital investment. E-commerce giants increasingly promote eco-friendly product lines with targeted campaigns and subscriptions. Mobile apps, contactless delivery, and transparent traceability boost consumer confidence and ease of purchase. This omnichannel availability supports the scale-up of green food brands, especially in urban and semi-urban areas where convenience and speed influence buyer behavior.

- For instance, Thrive Market serves over 1.6 million members online with health‑oriented food delivery nationwide.

Supportive Government Policies and Certifications

Government regulations and initiatives globally have created a favorable environment for green food expansion. Programs that incentivize organic farming, subsidies for sustainable agriculture, and tax benefits for eco-label compliance boost supply chain participation. Certification standards such as USDA Organic, EU Organic, and India Organic help validate product claims and increase market credibility. Public-private partnerships and awareness drives also educate farmers and consumers about the benefits of sustainable production and consumption. Schools and public institutions increasingly adopt green food in nutrition programs. These structural efforts reduce barriers for producers and instill long-term confidence in green food supply chains.

Key Trends & Opportunities

Shift Toward Plant-Based and Alternative Proteins

A prominent trend in the green food market is the accelerated shift toward plant-based diets and meat alternatives. Rising concerns over animal welfare, greenhouse gas emissions, and cholesterol-related health issues have encouraged consumers to opt for soy, pea, and lentil-based protein products. Startups and food tech firms continue to innovate with plant-derived alternatives that closely mimic meat, eggs, and dairy. Partnerships between global fast-food chains and plant-based brands have further normalized alternative proteins. This trend presents major opportunities for product diversification, especially in functional foods, ready meals, and sports nutrition categories targeting health-conscious and flexitarian consumers.

- For instance, McDonald’s offers the McPlant burger, developed with Beyond Meat, featuring a plant‑based patty using potatoes, peas and rice.

Premiumization and Clean Label Preferences

Consumers are showing growing preference for premium green food offerings that emphasize clean labels, functional benefits, and traceable sourcing. Ingredients with minimal processing, clear provenance, and added health value—such as antioxidants or probiotics—are gaining traction. Brands that highlight transparency and ethical practices, such as regenerative agriculture or fair trade sourcing, earn stronger customer loyalty. Premiumization allows players to command higher margins while aligning with consumer demand for value-added wellness. This trend opens opportunities for differentiation, especially in categories like snacks, beverages, and dairy alternatives where taste and nutrition both drive repeat purchase behavior.

Key Challenges

High Price Points and Affordability Issues

One of the major challenges in the green food market is the high cost of production and pricing, making products less accessible to middle- and low-income consumers. Organic and sustainably sourced ingredients require more labor-intensive practices, higher compliance costs, and often limited yields, resulting in premium prices. Retailers also factor in inventory risks and certification expenses. In price-sensitive markets, consumers may still opt for conventional alternatives despite awareness of health benefits. Bridging this affordability gap remains a key hurdle for green food brands aiming for mass-market penetration. Scaling operations and optimizing supply chains could gradually reduce cost barriers.

Supply Chain Complexity and Limited Producer Base

The green food supply chain is highly fragmented and dependent on a limited number of certified producers and sustainable farms. This creates bottlenecks in procurement, especially during seasonal fluctuations or when demand spikes. Logistics are further complicated by the need for separate handling, storage, and transportation to preserve organic or perishable quality. Cross-border trade of certified green food also faces regulatory hurdles and inconsistent standards. Delays in certification processes and a lack of trained labor for sustainable practices add to the challenge. Market players must invest in capacity building, digitization, and farmer outreach to secure long-term supply chain stability.

Regional Analysis

North America

North America holds a dominant position in the green food market with a market share of over 30% in 2024. Strong consumer demand for organic and plant-based foods, backed by high purchasing power and health awareness, drives growth in the U.S. and Canada. Retail giants actively expand their organic ranges, while foodservice outlets increasingly offer sustainable options. Government support for organic farming and clean labeling boosts market confidence. Rising concerns over lifestyle-related illnesses further promote green food consumption. The region benefits from a well-developed supply chain and advanced food processing technologies that enhance product availability and shelf-life.

Europe

Europe accounts for approximately 28% of the global green food market share in 2024. Consumer preferences lean heavily toward organic, clean-label, and locally sourced products due to strong environmental consciousness. Countries like Germany, France, and the UK lead in organic consumption. Strict EU regulations and sustainability targets push producers toward greener practices. Retailers and specialty stores emphasize eco-certified foods, while plant-based innovation gains momentum across multiple categories. The region’s mature infrastructure and efficient distribution networks support growth. Institutional demand from schools and healthcare sectors further strengthens Europe’s position in the global green food market.

Asia Pacific

Asia Pacific holds around 22% of the green food market in 2024 and is the fastest-growing region. Rising health awareness, urbanization, and a growing middle class fuel demand across China, India, Japan, and Southeast Asia. Governments promote organic farming through subsidies and certification schemes, especially in India and China. Increasing e-commerce penetration allows wider access to eco-friendly products in urban and rural markets. Younger consumers adopt plant-based diets influenced by social media trends. Retail chains and food delivery platforms expand their green food offerings. Despite infrastructure gaps in some areas, rapid digitalization accelerates market reach across the region.

Latin America

Latin America captures close to 10% of the green food market share in 2024. Brazil, Argentina, and Mexico are key contributors, with growing awareness around clean eating and organic farming practices. The region benefits from abundant arable land, enabling strong potential for local green food production. Consumer interest in natural and locally sourced foods grows steadily, especially in urban centers. However, affordability remains a challenge, limiting broader adoption. Government programs supporting agroecological practices help promote organic farming. Retail and online platforms play a growing role in market expansion, making green food more visible and accessible to health-conscious consumers.

Middle East & Africa (MEA)

The Middle East & Africa hold a modest 5% share in the global green food market in 2024 but show emerging potential. High-income countries like the UAE and Saudi Arabia lead demand through premium organic and plant-based food offerings. Health-focused urban consumers drive this trend, supported by clean eating campaigns. Regional agriculture faces challenges such as limited arable land and water scarcity, prompting reliance on imports. In Africa, awareness is growing slowly, with governments and NGOs promoting sustainable farming and local nutrition. Expansion of modern retail formats and growing digital penetration will play a key role in future growth.

Green Food Market Segmentations:

By Type

- Organic Food

- Natural Food

- Plant-Based Food

- Locally Sourced Food

- Others

By Application

- Retail

- Foodservice

- Food Processing

- Others

By Distribution Channel

- Supermarkets and Hypermarkets

- Specialty Stores

- Online Retail

- Others

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The competitive landscape of the green food market is moderately fragmented, with a mix of multinational corporations and niche players competing across categories. Companies focus on product innovation, clean labeling, and sustainable sourcing to differentiate their offerings. Major players such as Danone, General Mills Inc., and The Hain Celestial Group expand their organic and plant-based portfolios through acquisitions and partnerships. Brands like Nature’s Path Food, Amy’s Kitchen, and Clif Bar & Company cater to health-conscious consumers with specialized, non-GMO, and vegan product lines. Retailers such as Whole Food Market Inc. and United Natural Food Inc. strengthen market presence through private labels and wide distribution networks. Continuous investment in supply chain transparency, eco-friendly packaging, and certifications remains key to gaining consumer trust. E-commerce growth enables smaller brands like SunOpta Inc. and Eden Food to scale quickly. The market sees rising M&A activity as firms aim to expand reach, enhance capacity, and enter emerging green food segments.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Naturex

- United Natural Food Inc.

- Clif Bar & Company

- Amy’s Kitchen

- General Mills Inc.

- Nature’s Path Food

- Hain Celestial

- SunOpta Inc.

- Organic Valley

- Danone

- Whole Food Market Inc.

- WhiteWave Food Company

- Eden Food

- Earth’s Best

- The Hain Celestial Group

Recent Developments

- In 2022, Organic India, a renowned organic tea and wellness brand, introduced Tulsi Detox Kahwa and Peppermint Refresh teas. These certified organic and vegan teas come in loose-leaf and teabag options, aligning with the brand’s commitment to providing healthy and sustainable wellness products.

- In 2022, Amul, an Indian dairy company, diversified into the organic food market with a range of products, including organic rice, flour, honey, chocolates, and potato items. They also initiated plans to establish a “green college” to educate young farmers about natural and organic farming practices and create “organic haats” for selling organic products.

Report Coverage

The research report offers an in-depth analysis based on Type, Application, Distribution Channel and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Consumer demand for healthier and sustainable food choices will continue to strengthen market expansion.

- Plant-based and organic food adoption will rise across mainstream and mass-market consumer groups.

- Retailers will expand private-label green food products to improve affordability and margins.

- Online and direct-to-consumer channels will gain importance for product access and brand visibility.

- Foodservice operators will increase green food offerings to meet changing dining preferences.

- Innovation in clean-label and functional ingredients will support product differentiation.

- Sustainable packaging adoption will accelerate to align with environmental expectations.

- Emerging economies will see faster adoption due to urbanization and income growth.

- Strategic partnerships and acquisitions will reshape competitive positioning among key players.

- Supply chain transparency and certification compliance will remain critical for long-term growth.