Market Overview

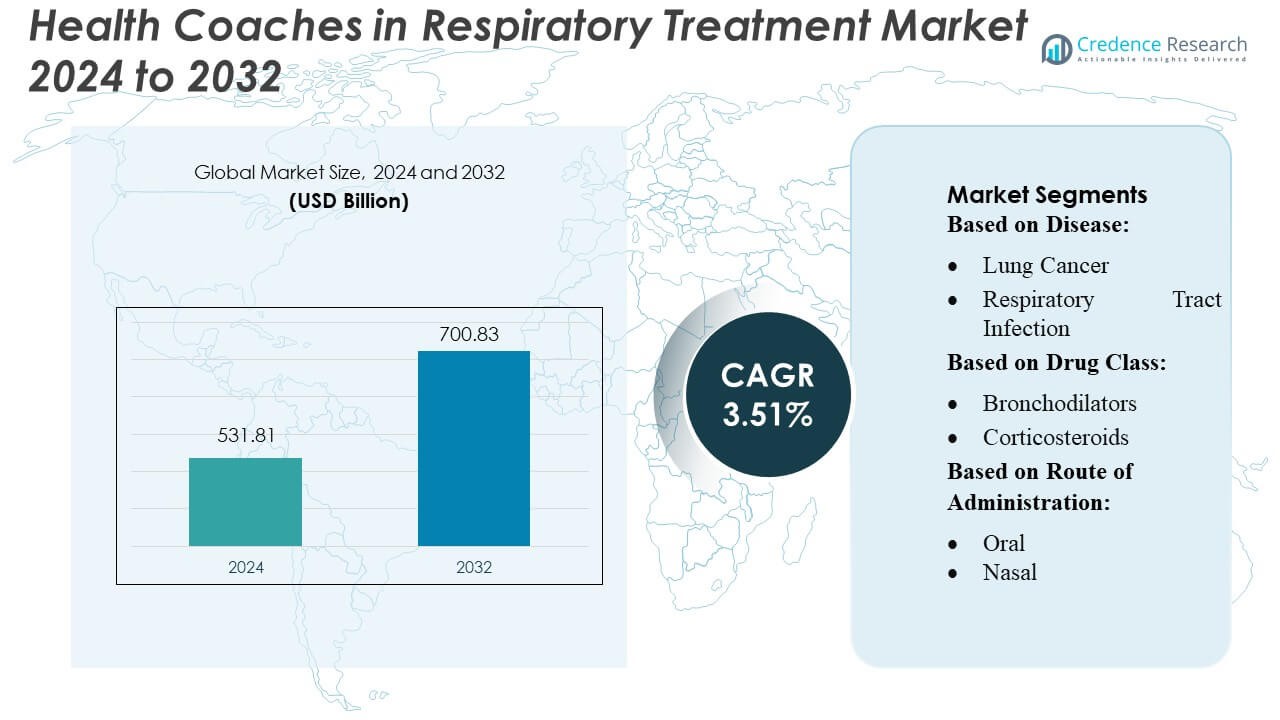

Health Coaches in Respiratory Treatment Market size was valued USD 531.81 billion in 2024 and is anticipated to reach USD 700.83 billion by 2032, at a CAGR of 3.51% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Health Coaches in Respiratory Treatment Market Size 2024 |

USD 531.81 Billion |

| Health Coaches in Respiratory Treatment Market, CAGR |

3.51% |

| Health Coaches in Respiratory Treatment Market Size 2032 |

USD 700.83 Billion |

The Health Coaches in Respiratory Treatment Market features a competitive environment driven by digital health innovation, expanding coaching programs, and strong integration of remote monitoring tools. Companies in this space focus on enhancing patient engagement, improving treatment adherence, and supporting long-term management of asthma, COPD, and related conditions through data-driven coaching models. The market benefits from increasing adoption of telehealth platforms and AI-enabled respiratory support systems that strengthen personalized care delivery. North America leads the market with approximately 38% share, supported by advanced healthcare infrastructure, widespread chronic respiratory disease prevalence, and strong payer adoption of preventive care solutions.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Health Coaches in Respiratory Treatment Market reached USD 531.81 billion in 2024 and is projected to hit USD 700.83 billion by 2032, growing at a CAGR of 3.51%, driven by expanding digital coaching adoption and rising chronic respiratory disease prevalence.

- Market growth is supported by strong drivers such as increasing demand for personalized respiratory management, smart inhaler integration, and continuous patient monitoring that improves treatment adherence across asthma and COPD segments, with asthma coaching contributing the largest segment share.

- Key trends include accelerated use of AI-enabled coaching tools, connected devices, and data-driven platforms that enhance patient engagement while enabling scalable virtual care delivery models across diverse populations.

- Competitive activity intensifies as companies invest in digital therapeutics, remote coaching ecosystems, and behavioral health integration, though challenges remain due to reimbursement gaps and variations in digital access across regions.

- North America dominates with 38% regional share, followed by Europe and Asia-Pacific, supported by advanced infrastructure and rising adoption of preventive care solutions.

Market Segmentation Analysis:

By Disease

Asthma represents the dominant disease segment, accounting for the largest share of the Health Coaches in Respiratory Treatment Market due to its high global prevalence and the increasing adoption of personalized digital coaching for symptom monitoring. Health coaches play a pivotal role in guiding patients on inhaler use, trigger avoidance, and lifestyle adjustments, which strengthens engagement and long-term disease control. COPD follows closely, driven by the growing elderly population and the need for continuous behavioral support. Rising demand for remote monitoring tools further boosts adoption across other segments, including allergic rhinitis and cystic fibrosis.

- For instance, Teva has deployed its ProAir Digihaler—a smart inhaler with built-in flow sensors—and in a CONNECT1 study involving 333 asthma patients, 61% of users in the Digihaler arm achieved well-controlled asthma or meaningful ACT-score improvement at 12 weeks versus 55% in the standard inhaler group.

By Drug Class

Bronchodilators hold the leading share in this segment, supported by their frequent prescription for asthma and COPD and the need for patient education on dosage timing and adherence. Health coaches enhance therapeutic effectiveness by improving self-management behaviors and monitoring medication responses. Corticosteroids and combination drugs also gain traction as coaches help patients understand step-therapy models and manage side effects. Antibiotics, targeted therapies, immunotherapies, and CFTR modulators expand steadily, driven by growing preference for guided treatment pathways and personalized coaching interventions for complex respiratory conditions.

- For instance, Astellas co-promotes the fixed-dose combination of budesonide and formoterol (Symbicort), in which each inhalation delivers 4.8 µg of formoterol fumarate and 160 µg of budesonide—refers to one specific formulation of the Symbicort pMDI (pressurized metered-dose inhaler) available in markets like the United States, which is a different product from the one Astellas co-promoted in Japan.

By Route of Administration

The inhalation route—including nasal and oral inhalers—dominates the market as most respiratory treatments require precise inhalation techniques, which health coaches help patients master through guided training and adherence tracking. Nasal administration grows consistently due to increasing diagnoses of allergic rhinitis. Injectable therapies expand moderately, primarily in severe asthma and targeted biologic treatments where coaching supports dosing schedules and post-injection monitoring. Oral therapies remain relevant for infections and long-term management, with coaches reinforcing compliance. Overall, rising demand for remote inhaler-use coaching sustains the leadership of inhalation-based treatments.

Key Growth Drivers

1. Rising Prevalence of Chronic Respiratory Diseases

The rapid increase in chronic respiratory diseases—including asthma, COPD, and allergic disorders—significantly drives the need for structured patient support through health coaching. Patients require continuous monitoring, behavioral guidance, and treatment adherence reinforcement to manage symptoms effectively. Health coaches bridge gaps between clinical visits by offering personalized care plans, inhaler-use training, and lifestyle modifications. The growing global burden of air pollution and smoking further expands the population needing long-term support, positioning health coaching as a cost-effective complement to medical treatment and improving overall disease management outcomes.

- For instance, Linzagolix is an oral GnRH antagonist that has completed Phase 3 PRIMROSE trials for uterine fibroids. Across both studies, a total of 1,012 patients were enrolled: 511 women in the PRIMROSE 1 trial and 501 women in the PRIMROSE 2 trial.

2. Expansion of Digital Health Platforms and Remote Monitoring

The rapid scale-up of digital health solutions strengthens the adoption of respiratory health coaching programs. Mobile health applications, teleconsultation platforms, and remote monitoring tools enable coaches to track symptoms, medication adherence, peak-flow readings, and lifestyle metrics in real time. These technologies increase accessibility, reduce follow-up burden on hospitals, and offer scalable coaching models for large patient groups. Integration of AI-driven alerts and personalized recommendations enhances patient engagement and treatment optimization. As governments and insurers support virtual care, digital ecosystems continue to drive growth in structured respiratory coaching.

- For instance, Pfizer ran a 12-month pilot in collaboration with Catalia Health using the Mabu® AI robot, which engaged chronically ill patients through voice-based conversations and fed real-time medication-adherence and symptom-management data into a clinician insights platform.

3. Shift Toward Preventive and Patient-Centric Care Models

Health systems increasingly prioritize preventive care to reduce hospitalizations associated with respiratory conditions, which drives strong demand for coaching services. Health coaches help patients develop long-term self-management habits, minimizing exacerbations and supporting early identification of symptom deterioration. Providers adopt patient-centric models that emphasize behavioral change, education, and personalized guidance, aligning directly with the coaching framework. Payers and employers also recognize the cost benefits of reducing emergency visits through continuous coaching support. This shift positions respiratory health coaches as a key component of integrated and value-based care pathways.

Key Trends & Opportunities

1. Integration of AI and Predictive Analytics in Coaching

AI-enabled tools present a major opportunity to enhance respiratory coaching through personalized insights and real-time risk prediction. Predictive analytics assess symptom patterns, inhaler usage, and environmental triggers to help coaches intervene early and optimize treatment plans. Wearables and smart inhalers generate continuous data streams that enable customized behavioral strategies. This trend improves treatment adherence, reduces exacerbation risks, and enhances patient satisfaction. Health providers increasingly adopt AI-driven platforms to deliver scalable coaching programs, presenting strong commercial potential for technology-enabled respiratory management solutions.

- For instance, ARCH (AbbVie R&D Convergence Hub) is a platform that integrates over 200 internal and external data sources. It accumulates more than 2 billion points of knowledge (or connections) within its knowledge graph, enabling machine-learning models to surface hidden disease-relevant relationships.

2. Growing Adoption of Smart Inhalers and Connected Devices

The market benefits from the rising penetration of connected inhalers, digital spirometers, and home-based respiratory monitors. These devices capture objective usage data and allow coaches to provide targeted guidance on inhalation technique, dosing frequency, and symptom trends. Smart inhalers, in particular, streamline data sharing between patients, coaches, and physicians, supporting coordinated care. As device accuracy improves and costs decline, adoption expands across asthma and COPD populations. This creates strong opportunities for integrating coaching services into device ecosystems and subscription-based digital therapeutics models.

- For instance, AstraZeneca is working with Honeywell to transition its triple-combination inhaler, Breztri Aerosphere, to a new platform using a near-zero global-warming-potential propellant, reducing greenhouse gas emissions by up to 99.9% compared to current pMDI propellants.

3. Expansion of Employer Wellness and Insurance-Based Programs

Employers and insurers increasingly integrate respiratory health coaching into wellness programs as they seek to reduce absenteeism and long-term treatment costs. These initiatives offer structured coaching for employees with asthma, allergies, or smoking-related respiratory issues, improving workforce productivity and lowering claim rates. Insurance companies bundle coaching with reimbursement models for chronic disease management, creating new commercial channels for coaching providers. The trend encourages scalable, subscription-based coaching solutions that extend beyond clinical settings into corporate health ecosystems.

Key Challenges

1. Limited Reimbursement and Standardization

Despite rising demand, limited reimbursement frameworks hinder broader adoption of respiratory health coaching. Many regions lack standardized guidelines that define coaching as a billable clinical service, causing inconsistent integration within healthcare systems. Providers face challenges in securing coverage for digital coaching platforms, reducing scalability. The absence of unified certification standards also results in variability in coach competency and program quality. Without structured reimbursement and regulatory clarity, the market faces barriers in achieving full clinical and commercial integration.

2. Data Privacy Concerns and Digital Access Gaps

The increasing reliance on digital tools for respiratory coaching raises significant concerns around data security and patient privacy. Sensitive health data from smart devices and mobile apps requires robust protection, and inadequate safeguards can reduce patient trust. Additionally, digital access gaps—particularly in rural and low-income populations—limit the reach of virtual coaching services. Limited internet connectivity and low digital literacy create adoption barriers. These challenges restrict equitable access and may slow market expansion unless addressed through secure platforms and inclusive infrastructure development.

Regional Analysis

North America

North America leads the Health Coaches in Respiratory Treatment Market with approximately 38% share, supported by high adoption of digital health platforms, structured chronic disease management programs, and strong insurance reimbursement for coaching services. The United States drives regional dominance due to its large asthma and COPD patient base and increasing use of smart inhalers and remote monitoring devices. Health systems integrate coaching into value-based care models to reduce hospitalizations and improve adherence. Growing employer wellness programs and collaborations between digital therapeutics companies and healthcare providers further strengthen regional market expansion.

Europe

Europe holds around 28% of the market, driven by well-established chronic disease management frameworks and strong government emphasis on preventive respiratory care. Countries such as Germany, the U.K., and the Netherlands show high digital health adoption, enabling health coaches to support asthma, COPD, and allergy management through virtual platforms. The region benefits from advanced reimbursement structures, rising pollution-linked respiratory disorders, and increasing integration of smart devices in clinical pathways. Efforts to reduce healthcare system burdens through remote coaching and patient education further reinforce Europe’s position in the market.

Asia-Pacific

The Asia-Pacific region accounts for nearly 22% of the global market and is the fastest-growing segment, propelled by high prevalence of asthma, respiratory infections, and pollution-driven conditions. Rapid digitalization in healthcare, increasing smartphone penetration, and growing acceptance of telehealth encourage the expansion of respiratory health coaching services. China, India, Japan, and South Korea lead adoption as governments promote digital health reforms and preventive care models. Rising awareness of long-term disease management and partnerships between hospitals and digital health platforms accelerate market growth across diverse population groups.

Latin America

Latin America holds approximately 7% of the market, with growth driven by increasing diagnosis of respiratory diseases and rising demand for patient education and follow-up care. Brazil and Mexico lead adoption due to expanding telehealth ecosystems and government initiatives aimed at improving chronic disease management. Although digital infrastructure varies across countries, mobile-based coaching programs are gaining traction due to affordability and accessibility. The region sees growing interest from private clinics and employers seeking to reduce respiratory-related absenteeism. However, reimbursement limitations continue to slow broader adoption.

Middle East & Africa

The Middle East & Africa region captures around 5% of the market, supported by rising awareness of respiratory health risks, increasing pollution levels, and a growing burden of asthma and COPD. Gulf countries, particularly the UAE and Saudi Arabia, lead adoption through strong investments in digital health and preventive care programs. Mobile-based respiratory coaching is expanding as hospitals integrate remote monitoring for chronic disease patients. However, limited healthcare access in parts of Africa and low digital literacy restrict widespread penetration. Gradual improvements in telehealth infrastructure will enhance future market growth.

Market Segmentations:

By Disease:

- Lung Cancer

- Respiratory Tract Infection

By Drug Class:

- Bronchodilators

- Corticosteroids

By Route of Administration:

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The competitive landscape of the Health Coaches in Respiratory Treatment Market features a diverse mix of global pharmaceutical and healthcare innovators, including Teva Pharmaceutical Industries Ltd., Astellas Pharma, Inc., Zydus Healthcare Limited, ObsEva SA, Pfizer, Inc., AbbVie, Inc., Takeda Pharmaceutical Company Limited, AstraZeneca, Gedeon Richter Plc., and Bayer AG. The Health Coaches in Respiratory Treatment Market is evolving rapidly as companies strengthen their focus on integrating behavioral support with clinical respiratory care. Market participants prioritize digital health platforms, remote monitoring solutions, and data-driven coaching models to enhance patient adherence and reduce exacerbation risks. Innovations in smart inhalers, AI-enabled symptom tracking, and personalized care pathways are shaping competitive differentiation. Organizations increasingly collaborate with hospitals, insurers, and digital therapeutics firms to expand service reach and deliver scalable coaching programs. As demand for preventive care grows, competition intensifies around platform usability, clinical accuracy, outcome-based performance, and long-term patient engagement capabilities.

Key Player Analysis

- Teva Pharmaceutical Industries Ltd.

- Astellas Pharma, Inc.

- Zydus Healthcare Limited

- ObsEva SA

- Pfizer, Inc.

- AbbVie, Inc.

- Takeda Pharmaceutical Company Limited

- AstraZeneca

- Gedeon Richter Plc.

- Bayer AG

Recent Developments

- In January 2025, Numan launched an AI Health Assistant to offer personalized health coaching as part of its weight management strategy. This AI is designed to provide tailored advice on nutrition and exercise, support patient-centered goals, and enhance Numan’s existing weight management program.

- In January 2025, Elyria, a UK-based health tech startup, introduced a digital health coaching platform developed especially for people with fibromyalgia. The app aims to offer personalized support through human coaching and digital tools.

- In January 2024, Hera Biotech, Inc., a Texas-based biotechnology company specializing in tissue-based diagnostics for endometriosis, announced its agreement to acquire the endometriosis diagnostic assets and associated intellectual property of Scailyte AG. Scailyte AG, a Swiss firm known for its expertise in single-cell omics and AI-driven biomarker discovery, continues to operate independently, focusing its proprietary AI platform and remaining assets on other therapeutic areas, such as immuno-oncology and autoimmunity.

- In March 2023, Affibody AB and Chiesi Farmaceutici S.p.A have announced a collaboration and licensing agreement to develop and commercialize innovative treatments for respiratory diseases using Affibody’s proprietary technology.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Report Coverage

The research report offers an in-depth analysis based on Disease, Drug Class, Route of Administration and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will increasingly integrate AI-driven coaching tools to deliver personalized respiratory management and early risk detection.

- Smart inhalers and connected devices will strengthen real-time monitoring and enhance coach–patient engagement.

- Digital therapeutics partnerships will expand, enabling scalable coaching programs across chronic respiratory conditions.

- Remote care adoption will rise as healthcare systems prioritize preventive and continuous management models.

- Employers and insurers will broaden coaching coverage to reduce respiratory-related absenteeism and long-term treatment costs.

- Coaching programs will become more standardized with clearer certification frameworks and evidence-based protocols.

- Behavioral health integration will grow as emotional and lifestyle factors gain importance in respiratory care outcomes.

- Coaching platforms will adopt multilingual and culturally adaptive interfaces to address diverse patient groups.

- Predictive analytics will help coaches tailor interventions and reduce acute exacerbations.

- Overall market adoption will accelerate as respiratory disease prevalence rises and digital health infrastructure expands.