Industrial Filtration Market Overview:

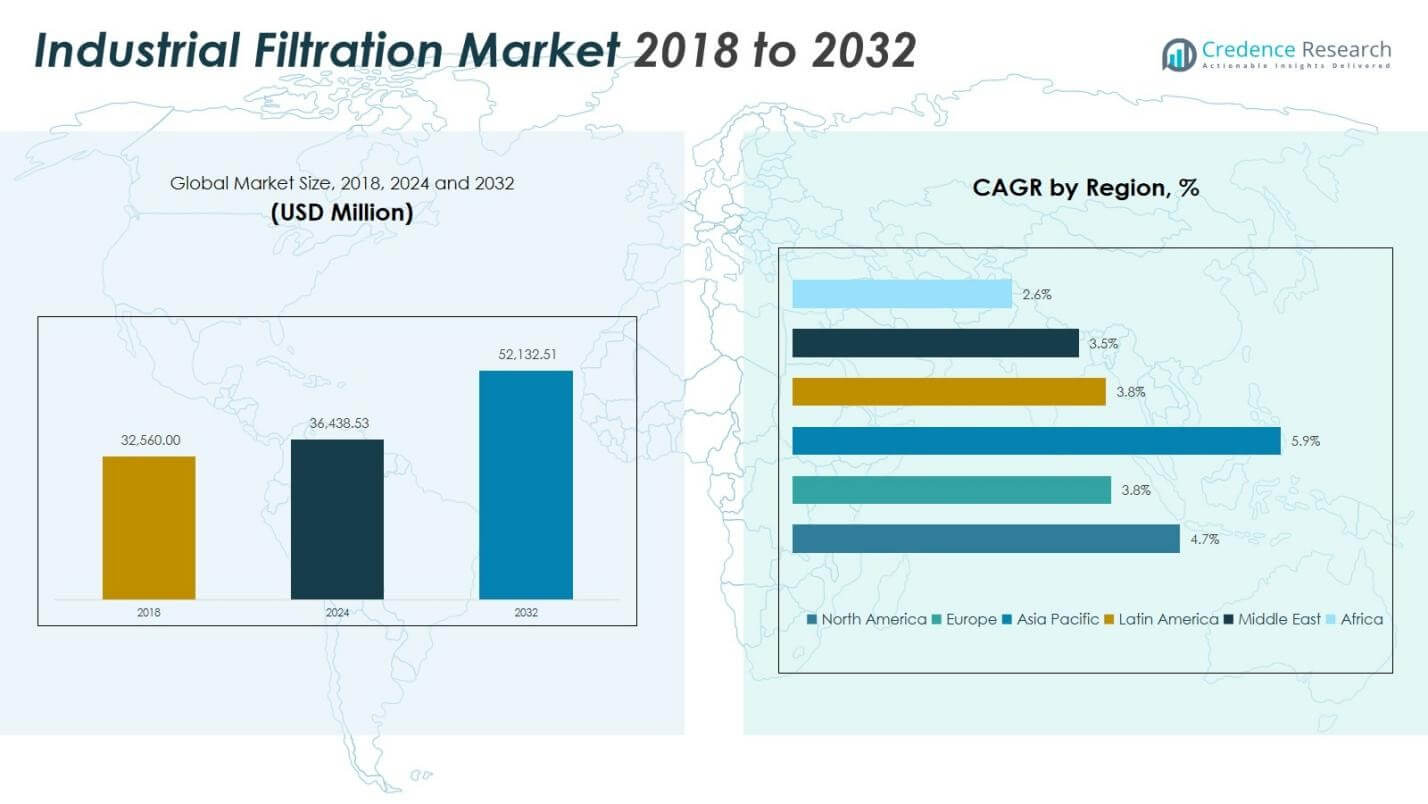

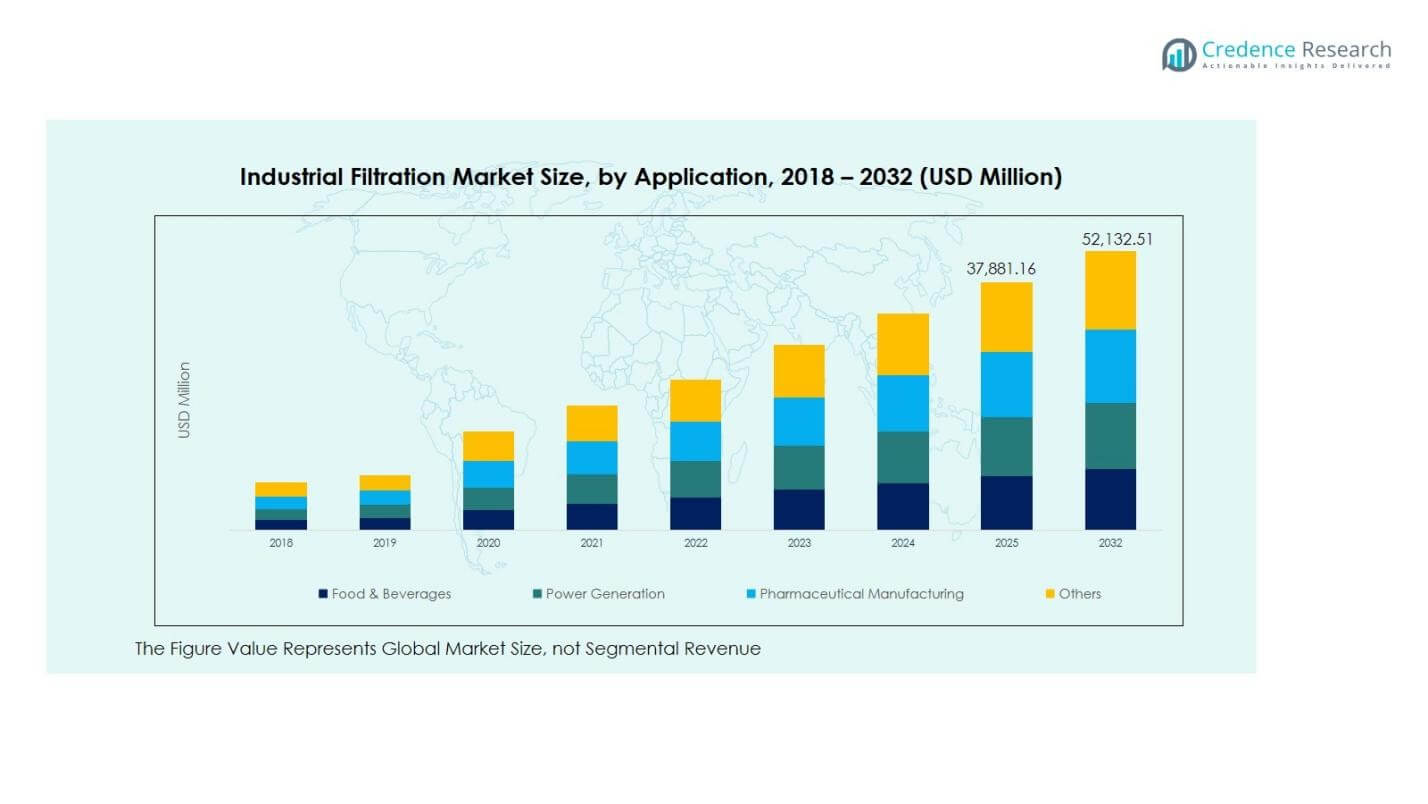

Industrial Filtration Market size was valued at USD 32,560.00 Million in 2018, increased to USD 36,438.53 Million in 2024, and is anticipated to reach USD 52,132.51 Million by 2032, growing at a CAGR of 4.67% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Industrial Filtration Market Size 2024 |

USD 36,438.53 million |

| Industrial Filtration Market, CAGR |

4.67% |

| Industrial Filtration Market Size 2032 |

USD 52,132.51 million |

Industrial Filtration Market Insights

- Markets overview highlights rising adoption of high-efficiency air and liquid filtration across process industries, with Air Filtration holding a 54.28% share in 2024 and strong demand driven by regulatory compliance, workplace safety, and product-quality assurance across critical manufacturing environments.

- Markets driver is supported by expansion in chemicals, petrochemicals, pharmaceuticals, power generation, and electronics manufacturing, where contamination control, equipment reliability, and process optimization continue to increase reliance on advanced filter media and membrane-based systems.

- Markets trends indicate growing investments in energy-efficient, automated, and sensor-enabled filtration solutions, along with technology upgrades by leading players focusing on product innovation, lifecycle-cost optimization, aftermarket services, and portfolio expansion across industrial applications.

- Regional analysis shows North America holding 36.66% share in 2024, Asia Pacific accounting for 26.87% with the fastest growth, Europe contributing 22.58%, while Latin America, the Middle East, and Africa collectively expand through gradual industrial modernization and infrastructure development.

Industrial Filtration Market Segmentation Analysis:

By Type

The By Type segment in the Industrial Filtration Market is dominated by Air Filtration with a 54.28% share in 2024, driven by stringent workplace safety regulations, rising particulate-emission control requirements, and increasing deployment of cleanroom environments across pharmaceuticals, food processing, and semiconductor facilities. Within this segment, HEPA and cartridge air filters form the leading sub-segment with a 61.34% share, supported by their high dust-holding capacity and ability to eliminate fine airborne contaminants. The Liquid Filtration segment holds 45.72% share, driven by wastewater treatment, process-fluid clarification, and industrial water-recycling initiatives across chemicals, metals, and petrochemicals sectors.

- For instance, Camfil supplies HEPA filters for pharmaceutical and biotechnology cleanrooms that are rated 99.97% efficient at 0.3 microns, enabling facilities to maintain ISO Class 5–7 conditions and comply with regulatory air-quality limits for sterile drug production.

By Application

The By Application segment is led by Chemicals & Petrochemicals with a 21.94% share in 2024, emerging as the dominant sub-segment due to intensive liquid- and gas-filtration needs in refining operations, catalyst protection, and hazardous-process contamination control. Growth is strengthened by capacity expansion projects and strict effluent-discharge and emission-compliance policies. The Food & Beverages segment accounts for 14.63% share, driven by sterile processing and product-purity standards, while Power Generation holds 12.84% share, supported by turbine-intake protection and equipment-reliability requirements across thermal and renewable-integrated power plants.

- For instance, Pall Corporation provides backwash filters in refineries to protect catalyst beds in fixed-bed reactors and remove catalyst fines from FCC slurry oil, delivering high returns on investment by extending catalyst life and minimizing fouling.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Industrial Filtration Market Overview

Rising Environmental Compliance and Industrial Emission Standards

Stringent global regulations on air quality, effluent discharge, and industrial emissions are driving large-scale adoption of advanced filtration systems across manufacturing, power, chemicals, and processing industries. Governments and regulatory bodies are enforcing tighter norms on particulate emissions, wastewater recycling, and hazardous-material handling, compelling industries to upgrade legacy filtration infrastructure. Companies are increasingly investing in high-efficiency particulate filters, membrane-based liquid filtration, and automated filtration units to ensure regulatory conformity while minimizing operational downtime. This regulatory push is also encouraging technology modernization, lifecycle-cost optimization, and sustainable filtration practices, positioning compliance-driven upgrades as a major growth driver in the Industrial Filtration Market.

- For instance, Alto Garda Power upgraded to Camfil’s 2-stage static filtration system for its LM6000 gas turbine to meet environmental standards. This change reduced pressure drop by 50%, extended final filter lifetime 4x, and prefilter lifetime 9x.

Expansion of Process-Intensive Industries and Manufacturing Output

Rapid industrialization, capacity expansion in chemicals and petrochemicals, growth in pharmaceuticals and semiconductor fabrication, and increased production activity in metals and mining are strengthening filtration demand across global industrial ecosystems. These industries rely on precise contamination control to protect equipment, maintain product quality, and ensure uninterrupted operations in critical production environments. Rising automation, continuous-processing systems, and deployment of high-purity production lines are further increasing dependence on specialized air, liquid, and gas filtration solutions. The expansion of industrial manufacturing clusters in Asia-Pacific, North America, and the Middle East reinforces market growth, supported by capital investments in new plants and process-efficiency enhancement projects.

- For instance, in the semiconductor sector, TSMC’s new Fab 21 facility in Arizona employs high-efficiency particulate filters (HEPA and ULPA) across cleanroom environments, maintaining sub‑micron air purity standards critical for chip fabrication.

Increasing Focus on Workplace Safety, Reliability, and Product Quality

Industrial organizations are prioritizing worker safety, asset protection, and defect-free production, which is significantly accelerating adoption of high-performance filtration systems. Effective filtration prevents particulate exposure, airborne contaminants, and process-fluid impurities that can damage sensitive components, reduce equipment life, or compromise final product integrity. Industries such as food and beverages, pharmaceuticals, electronics manufacturing, and precision engineering are investing in sterile, microfiltration, and cleanroom-grade filtration technologies to meet quality-assurance standards and customer expectations. The growing emphasis on operational reliability, risk mitigation, and preventive maintenance continues to position filtration as a mission-critical enabler in modern industrial environments.

Key Trends & Opportunities

Adoption of Smart, Energy-Efficient, and Automated Filtration Systems

A major trend shaping the Industrial Filtration Market is the transition toward smart, digitally monitored, and energy-efficient filtration solutions. Industries are adopting IoT-enabled filtration units equipped with condition-monitoring sensors, differential-pressure analytics, and predictive-maintenance capabilities to improve system uptime and reduce unplanned downtime. Energy-optimized filter media, self-cleaning filters, and automated backwashing systems are helping companies lower operating costs and extend filter life cycles. This shift creates strong opportunities for manufacturers offering integrated filtration platforms, remote monitoring services, and intelligent asset-management solutions, particularly in high-duty environments such as refineries, power plants, pharmaceutical production, and semiconductor cleanrooms.

- For instance, Donaldson Company’s iCue connected filtration service uses IoT sensors to monitor dust collector vital signs like differential pressure in real time.

Growing Investment in Water Reuse, Wastewater Treatment, and Sustainability Programs

Sustainability-driven industrial transformation is creating significant opportunities for advanced liquid filtration technologies, particularly in wastewater treatment, process-water recycling, and zero-liquid-discharge initiatives. Industries facing water scarcity, rising utility costs, and environmental-footprint reduction targets are increasingly deploying membrane-based filtration, ultrafiltration, and microfiltration solutions to improve water recovery efficiency and minimize resource losses. Circular-economy policies and ESG-focused manufacturing strategies are accelerating investments in eco-efficient filtration systems with lower waste generation and improved recyclability. This sustainability-centric filtration adoption trend is expanding across sectors including chemicals, food processing, textiles, and metalworking, strengthening long-term market growth potential.

- For instance, R. Simplot’s potato plant achieved ZLD with CDM Smith’s membrane bioreactor and reverse osmosis system, recycling process water to EPA drinking standards without discharge

Key Challenges

High Capital Investment and Maintenance Costs for Advanced Filtration Technologies

One of the major challenges in the Industrial Filtration Market is the high initial investment associated with advanced filtration systems, specialized membranes, and automated monitoring technologies. Many small and mid-scale industrial operators face budget constraints, delaying modernization programs or opting for low-cost alternatives with shorter lifecycles. Ongoing maintenance, periodic media replacement, and system retrofitting further increase ownership costs, especially in heavy-duty and corrosive operating environments. While advanced filtration improves reliability and compliance, the financial burden on users can limit adoption rates, requiring vendors to emphasize value-driven pricing, lifecycle optimization, and service-based support models.

Operational Complexity and Performance Limitations in Harsh Industrial Conditions

Industrial filtration systems face performance challenges when operating in extreme temperatures, chemically aggressive environments, or high-particulate process conditions. Filter clogging, pressure-drop fluctuations, membrane fouling, and reduced service life can impact operational stability and increase system downtime. Selecting appropriate filtration media and configuration requires technical expertise, and incorrect system design may result in inefficiencies or contamination risk. Additionally, integrating new filtration technologies into legacy industrial infrastructure can be complex and resource-intensive. These technical and operational barriers create implementation challenges for end-users, reinforcing the need for application-specific solutions, skilled engineering support, and continuous performance optimization.

Regional Analysis

North America

North America accounts for 36.66% of the Industrial Filtration Market in 2024, with revenue increasing from USD 12,079.76 Million in 2018 to USD 13,358.15 Million in 2024, and projected to reach USD 19,085.81 Million by 2032, growing at a CAGR of 4.7%. Growth is driven by strict environmental compliance mandates, modernization of industrial facilities, and high demand for filtration in power generation, chemicals, and pharmaceuticals. Investments in process-safety systems and clean manufacturing continue to strengthen adoption of advanced air and liquid filtration technologies across the U.S., Canada, and Mexico.

Europe

Europe represents 22.58% of the Industrial Filtration Market in 2024, rising from USD 7,684.16 Million in 2018 to USD 8,226.82 Million in 2024, and expected to reach USD 11,039.20 Million by 2032, expanding at a CAGR of 3.8%. Market growth is supported by strong regulatory oversight on workplace safety, industrial emissions, and wastewater discharge across manufacturing and process industries. The region benefits from increased adoption of energy-efficient filtration systems in food processing, pharmaceuticals, and automotive production, while technological upgrades in industrial plants across Germany, France, Italy, and the UK further sustain filtration demand.

Asia Pacific

Asia Pacific holds 26.87% of the Industrial Filtration Market in 2024, increasing from USD 8,397.22 Million in 2018 to USD 9,792.70 Million in 2024, and projected to reach USD 15,389.56 Million by 2032, registering the highest CAGR of 5.9%. Rapid industrialization, expansion of chemical and petrochemical production, and growth in semiconductor, electronics, and pharmaceutical manufacturing are major growth drivers. Strong investments in wastewater treatment, clean manufacturing environments, and worker-safety standards across China, India, Japan, and Southeast Asia further accelerate the adoption of advanced air and liquid filtration technologies in high-volume production environments.

Latin America

Latin America accounts for 6.74% of the Industrial Filtration Market in 2024, increasing from USD 2,214.08 Million in 2018 to USD 2,455.59 Million in 2024, and anticipated to reach USD 3,277.57 Million by 2032, expanding at a CAGR of 3.8%. Market growth is supported by rising industrial activity in oil and gas, mining, food processing, and metal fabrication. Strengthening regulatory reforms related to environmental compliance and plant-safety standards is encouraging investments in liquid and dust-filtration systems, particularly across Brazil, Mexico, Argentina, and Chile, where industrial modernization and process-reliability requirements are steadily increasing.

Middle East

The Middle East represents 3.86% of the Industrial Filtration Market in 2024, with revenue rising from USD 1,334.96 Million in 2018 to USD 1,406.29 Million in 2024, and forecast to reach USD 1,830.14 Million by 2032, growing at a CAGR of 3.5%. Growth is driven by extensive filtration demand across oil refining, petrochemicals, power generation, and desalination operations. Ongoing industrial-infrastructure development, modernization of process plants, and increasing environmental-safety standards across GCC economies support adoption of high-performance filtration systems for equipment protection, emission control, and process-fluid purity.

Africa

Africa holds 3.29% of the Industrial Filtration Market in 2024, rising from USD 849.82 Million in 2018 to USD 1,198.98 Million in 2024, and projected to reach USD 1,510.24 Million by 2032, advancing at a CAGR of 2.6%. Growth is influenced by industrial expansion in mining, cement, food processing, and power sectors, where dust control, worker-safety regulations, and process-reliability needs are increasing. Gradual investments in manufacturing infrastructure, water-treatment facilities, and resource-processing industries across South Africa, Egypt, and emerging African economies are strengthening long-term opportunities for filtration-system deployment.

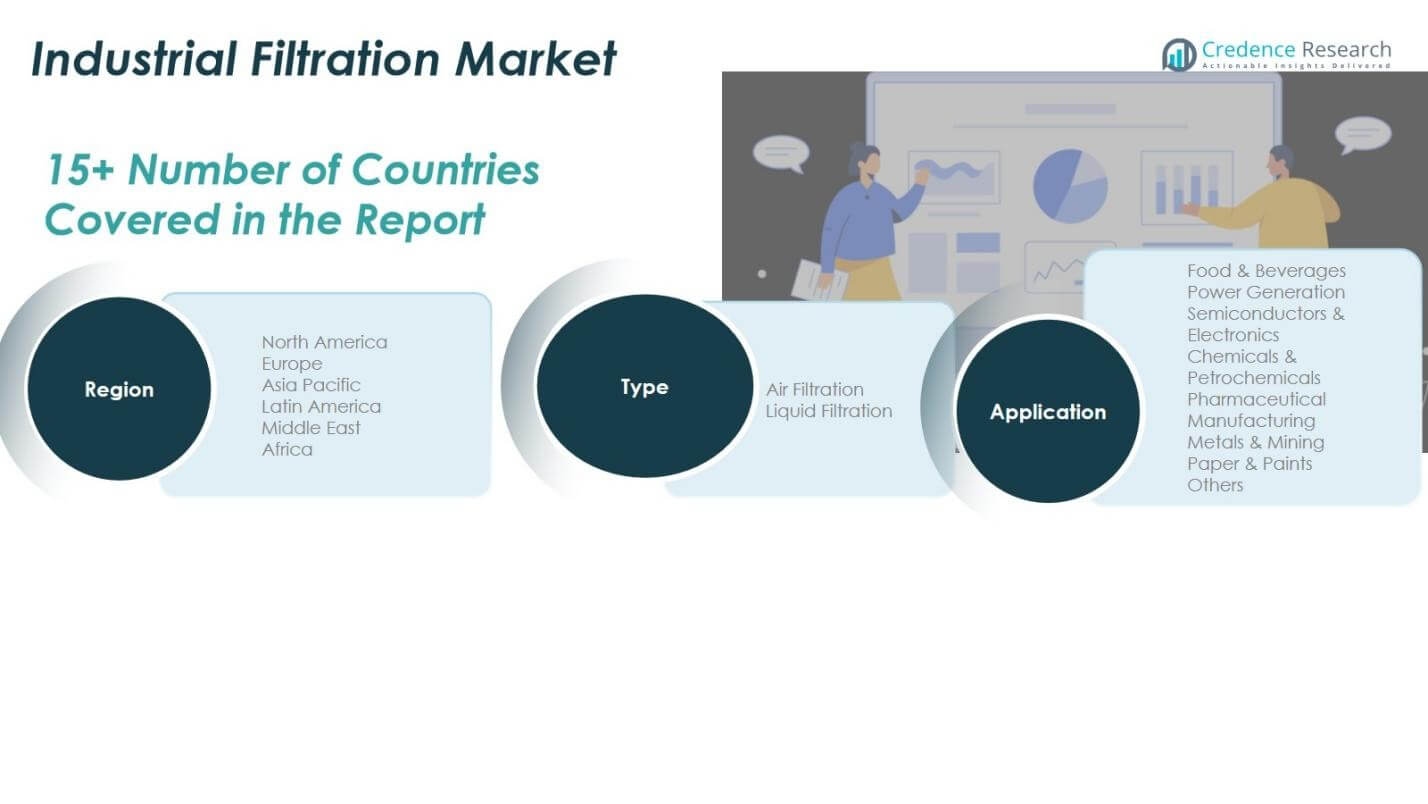

Industrial Filtration Market Segmentations:

By Type

- Air Filtration

- Liquid Filtration

By Application

- Food & Beverages

- Power Generation

- Semiconductors & Electronics

- Chemicals & Petrochemicals

- Pharmaceutical Manufacturing

- Metals & Mining

- Paper & Paints

- Others

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

Competitive landscape analysis in the Industrial Filtration Market is shaped by leading players such as 3M Company, Alfa Laval Inc., Donaldson Company, Filtration Group, Freudenberg Filtration Technologies, Mann+Hummel, Pall Corporation, Parker Hannifin Corp., Ahlstrom-Munksjö, and Hollingsworth & Vose Company. The market remains moderately consolidated, with large multinational manufacturers focusing on product innovation, advanced filter-media technologies, and expansion into high-growth end-use sectors such as chemicals, pharmaceuticals, electronics, and power generation. Companies are increasingly investing in membrane-based systems, energy-efficient air filtration units, and automated smart-filtration solutions to enhance performance, operational reliability, and lifecycle efficiency. Strategic initiatives such as mergers, acquisitions, and capacity expansion are strengthening global manufacturing footprints and portfolio diversification, while partnerships with industrial OEMs and EPC firms support integration into critical process environments. Growing emphasis on regulatory compliance, sustainability, and clean-manufacturing standards continues to intensify competition, encouraging technology upgrades and value-added service offerings across both mature and emerging regional markets.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- 3M Company

- Alfa Laval Inc.

- Donaldson Company, Inc.

- Filtration Group

- Freudenberg Filtration Technologies SE & Co. KG

- Mann+Hummel

- Pall Corporation

- Parker Hannifin Corp.

- Ahlstrom-Munksjö

- Hollingsworth & Vose Company

Recent Developments

- In December 2025, FloWorks International acquired Slater Controls LLC, reinforcing its distribution capabilities for critical flow control and filtration products.

- In November 2025, Parker Hannifin Corporation announced its acquisition of Filtration Group Corporation for $9.25 billion, creating one of the largest global industrial filtration businesses with expanded aftermarket and proprietary technologies.

- In March 2025, Cleanova completed the acquisition of Micronics Engineered Filtration Group, strengthening its portfolio of industrial filtration systems and engineered solutions for air and liquid applications.

- In September 2025, Thermo Fisher Scientific completed the acquisition of Solventum’s Purification & Filtration business, expanding its industrial filtration and membrane technology footprint.

Report Coverage

The research report offers an in-depth analysis based on Type, Application and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The Industrial Filtration Market will experience steady growth as industries prioritize cleaner production environments and stricter regulatory compliance.

- Demand for advanced air and liquid filtration systems will rise across chemicals, pharmaceuticals, food processing, and semiconductor manufacturing.

- Adoption of smart, sensor-enabled, and automated filtration technologies will increase to improve efficiency, monitoring accuracy, and predictive maintenance.

- Sustainability initiatives will drive higher investment in water reuse, wastewater treatment, and energy-efficient filtration solutions.

- Expansion of industrial manufacturing bases in Asia Pacific and the Middle East will strengthen regional demand for high-capacity filtration systems.

- Companies will increasingly shift toward high-performance filter media and membrane-based technologies to enhance process reliability and purity levels.

- Replacement and upgrade cycles for legacy filtration equipment will accelerate across mature industrial economies.

- Partnerships between filtration manufacturers and industrial automation providers will expand integrated system deployment.

- Growth in mining, power generation, and petrochemicals will support ongoing adoption of dust, gas, and process-fluid filtration solutions.

- Continuous innovation in modular, compact, and low-maintenance filtration designs will enhance operational flexibility for end-users.