Structural Insulated Panels Market Overview:

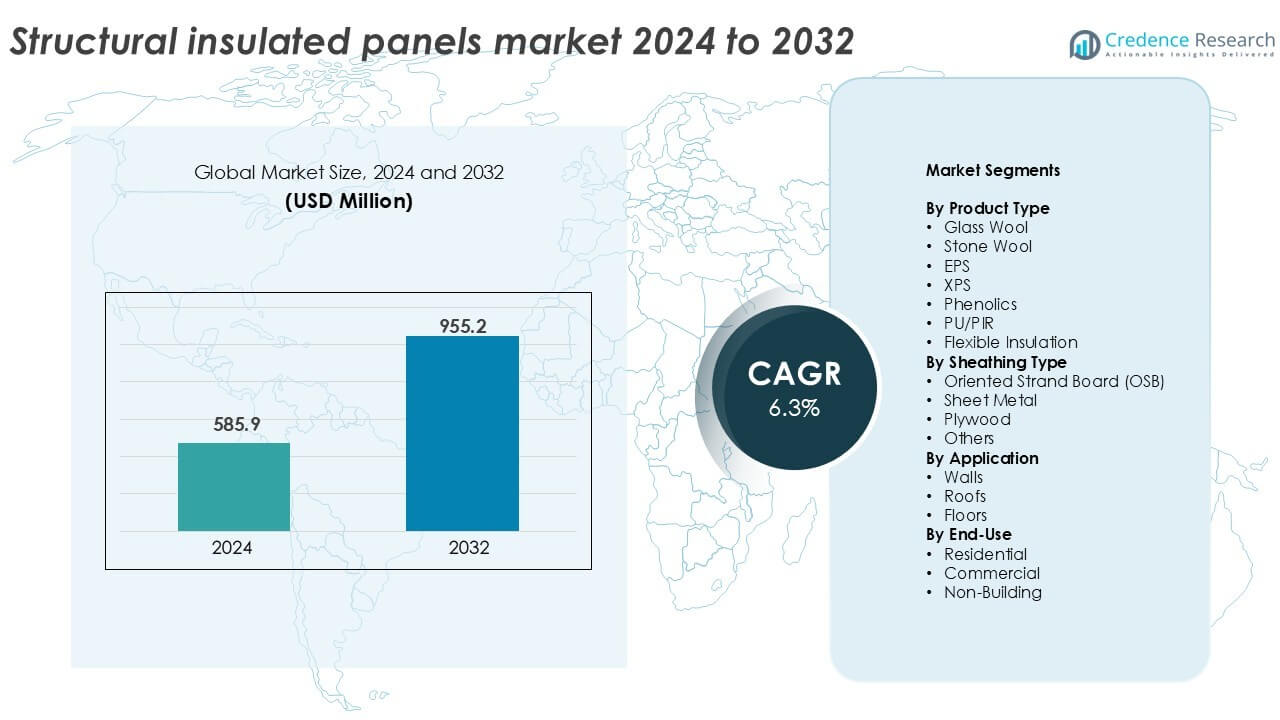

The Structural Insulated Panels Market size was valued at USD 585.9 million in 2024 and is anticipated to reach USD 955.2 million by 2032, at a CAGR of 6.3% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Structural Insulated Panels Market Size 2024 |

USD 585.9 million |

| Structural Insulated Panels Market, CAGR |

6.3% |

| Structural Insulated Panels Market Size 2032 |

USD 955.2 million |

Structural Insulated Panels Market Insights

- Rising demand for energy-efficient and fast construction drives market growth, supported by stricter building codes, green certifications, and increasing adoption of prefabricated and modular construction methods across residential and light commercial projects.

- Growing use of PU/PIR panels leads product segmentation with over 35% share due to high thermal performance, while wall applications dominate usage with nearly 45% share, supported by large surface coverage and insulation efficiency needs.

- The competitive landscape includes global leaders like Kingspan Group, Owens Corning, and METECNO, focusing on product innovation, capacity expansion, and sustainable materials to strengthen market positioning and address evolving construction standards.

- North America leads the market with around 35% share, followed by Europe at 28% and Asia-Pacific at about 22%, driven by energy regulations, urbanization, and rising adoption of modular housing solutions.

Structural Insulated Panels Market Segmentation Analysis:

By Product Type

PU/PIR panels dominate the structural insulated panels market, accounting for over 35% of the revenue share in 2024. Their strong thermal insulation properties, fire resistance, and lightweight design support widespread adoption across commercial and residential projects. These panels also offer long-term energy efficiency, reducing building operational costs. EPS panels follow due to cost advantages and easy handling. Glass wool and stone wool hold niche applications in fire-rated constructions. XPS and phenolics gain traction in cold storage and high-humidity zones. Flexible insulation remains limited to custom applications requiring adaptable forms.

- For instance, Kingspan manufactures PIR panels with certified thermal conductivity of 0.022 W/m·K for commercial wall and roof systems.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Sheathing Type

Oriented Strand Board (OSB) is the leading sheathing material, holding more than 40% market share in 2024. OSB panels offer high mechanical strength, dimensional stability, and compatibility with various insulation cores. Their cost-effectiveness and easy availability make them the preferred choice in residential construction. Sheet metal sheathing finds favor in industrial structures demanding moisture and pest resistance. Plywood sheathing is used in projects requiring improved load-bearing strength. Other materials like fiber cement and composites see selective adoption in projects emphasizing sustainability and durability.

- For instance, West Fraser produces structural OSB panels compliant with EN 300 and APA standards for load-bearing SIP applications. Sheet metal sheathing suits industrial buildings needing moisture resistance.

By Application

Wall applications remain the dominant segment, contributing over 45% to the structural insulated panels market share in 2024. Walls require large panel surface areas and benefit most from the insulation, strength, and speed offered by SIPs. Rapid urbanization, energy-efficient building codes, and the need for fast construction drive this growth. Roof applications follow, supported by demand in low-energy housing and retrofitting. Floor applications hold a smaller share but are growing steadily, particularly in modular buildings and eco-friendly home designs where thermal bridging reduction is a priority.

Key Growth Drivers

Rising Demand for Energy-Efficient Construction

The global shift toward energy-efficient buildings significantly drives the adoption of structural insulated panels (SIPs). Governments and regulatory bodies are mandating stricter building codes that emphasize thermal performance and reduced carbon emissions. SIPs offer superior insulation compared to conventional materials, helping builders meet energy certification standards like LEED and BREEAM. Their use contributes to lower heating and cooling loads, cutting long-term energy expenses for homeowners and developers. This is especially critical in cold climates and high-performance building projects. As awareness grows regarding net-zero energy buildings and passive house standards, SIPs are increasingly selected for their ability to reduce energy leakage, shorten construction timelines, and improve indoor comfort. Energy cost inflation also pushes both commercial and residential sectors to invest in high-insulation solutions, boosting market momentum. The demand is further supported by subsidies and incentives promoting green construction.

- For instance, the Passive House Institute specifies wall assemblies achieving U-values of 0.15 W/m²K or lower, which SIP systems can meet in certified projects.

Growth in Prefabricated and Modular Construction

The global construction sector is undergoing a transformation with the increasing adoption of prefabrication and modular techniques. Structural insulated panels fit seamlessly into this shift, offering factory-built precision, faster installation, and reduced labor requirements. These panels enhance the structural integrity of modular units while supporting consistent thermal performance. Builders prefer SIPs for modular housing, schools, and disaster-relief shelters due to their lightweight nature and ease of transport. Shorter project timelines, minimal waste, and cost savings strengthen their value proposition in modular projects. As urban housing shortages rise and governments push for faster infrastructure development, the prefabrication trend accelerates. SIPs also reduce the dependency on skilled on-site labor, which is becoming scarce in several countries. This structural evolution in construction methods reinforces the long-term demand for SIPs in both developed and emerging markets.

- For instance, Enercept reports SIP installation timelines that cut structural shell erection to fewer than 5 days for standard residential units.

Increasing Residential Construction Activities

Rising residential construction across North America, Europe, and Asia-Pacific is a major growth catalyst for the SIPs market. The ongoing demand for single-family homes, affordable housing, and low-rise apartments increases material demand with high insulation performance. SIPs reduce construction time and support cost-effective development, making them ideal for residential builders operating under tight budgets and deadlines. In the U.S. and Canada, green building programs and homeowner preferences for energy-efficient materials accelerate SIP usage. In Asia-Pacific, population growth and rapid urbanization stimulate large-scale housing development, especially in China and India. Residential builders increasingly choose SIPs for their load-bearing capabilities and compatibility with modern design layouts. The pandemic also influenced consumer preferences for high-performance homes with better insulation and air quality, further boosting SIP integration in residential projects.

Key Trends & Opportunities

Adoption of Sustainable Building Materials

Sustainability is becoming a core focus in the construction sector, creating a significant opportunity for structural insulated panels. SIPs contribute to greener construction by minimizing material wastage, reducing job-site emissions, and improving energy efficiency. Manufacturers are now using recycled content, bio-based resins, and eco-friendly adhesives to produce more sustainable panels. Green certifications and Environmental Product Declarations (EPDs) add value to SIPs in environmentally sensitive projects. Builders targeting carbon-neutral goals prefer SIPs for their closed-building envelope, which limits thermal bridging. Moreover, the recyclability of panel components aligns with circular economy goals. This trend is especially prominent in Europe, where the Green Deal and other climate regulations favor sustainable construction solutions. As corporate real estate and public infrastructure move toward ESG-aligned building strategies, SIPs offer a scalable and sustainable material alternative.

- For instance, Kingspan uses recycled PET content in insulation boards, diverting over 1 billion PET bottles annually from landfill across its insulation products.

Expansion of Cold Chain Infrastructure and Offsite Buildings

Structural insulated panels are increasingly used in cold chain infrastructure such as refrigerated warehouses, food processing units, and pharmaceutical storage due to their excellent thermal performance. The rising demand for temperature-controlled logistics, driven by e-commerce, perishable goods trade, and vaccine distribution, creates significant growth opportunities. SIPs help maintain interior temperature consistency and reduce energy consumption in cold storage facilities. Simultaneously, offsite buildings including mobile medical units, temporary shelters, and military housing also adopt SIPs for their ease of assembly and low weight. These applications require rapid setup, strong thermal insulation, and resistance to moisture all strengths of SIPs. As global logistics networks and emergency response infrastructure continue to expand, SIPs emerge as a material of choice for speed, efficiency, and thermal integrity in these specialized buildings.

Key Challenges

High Initial Costs Compared to Traditional Materials

One of the major challenges in the structural insulated panels market is the relatively high upfront cost compared to conventional wood framing and insulation systems. SIPs involve manufacturing precision and controlled production environments, which increase material and transportation costs. Builders unfamiliar with SIPs may face added expenses for specialized training or installation services. Although long-term energy savings offset some of the initial investment, the higher purchase price can deter budget-conscious developers, especially in cost-sensitive markets. Residential contractors often hesitate to adopt SIPs due to tight margins, preferring traditional methods they are already skilled in. For price-sensitive geographies or low-income housing projects, the upfront expense limits mass adoption. Overcoming this challenge requires stronger cost awareness campaigns, better installation training, and scalable production models that can lower the per-unit price through economies of scale.

Limited Skilled Workforce and Installation Challenges

Although SIPs simplify construction in theory, improper installation can undermine their benefits, making the availability of trained installers a critical issue. In many regions, the construction workforce lacks exposure to SIP systems, leading to errors like poor joint sealing, incorrect fastening, or thermal bridging. These mistakes compromise insulation performance and cause long-term structural issues. The need for accurate panel cutting, tight tolerances, and weatherproof sealing increases reliance on skilled labor or precision equipment. Without sufficient training programs and certified installers, developers may avoid SIPs despite their advantages. Labor shortages in construction further intensify this problem, particularly in rural or developing areas. Addressing this challenge demands industry-wide investment in education, certification, and technical support to ensure SIPs are correctly integrated into diverse project types.

Regional Analysis

North America

North America leads the structural insulated panels market with over 35% revenue share in 2024. The region benefits from high demand for energy-efficient buildings, government-backed green construction codes, and widespread use of prefabricated housing. The United States dominates due to residential construction and strong SIP adoption in passive house designs. Canada supports market growth through cold climate applications and government incentives for sustainable building materials. SIP manufacturers in North America also benefit from advanced production facilities and favorable labor productivity. Growing interest in modular housing further boosts the region’s share in both residential and light commercial sectors.

Europe

Europe holds approximately 28% share of the structural insulated panels market in 2024, supported by stringent environmental regulations and the EU Green Deal targets. Countries like Germany, the UK, and the Netherlands lead adoption due to their commitment to zero-emission buildings and energy codes. SIPs are widely used in residential retrofits, public housing, and modular educational facilities. Demand is reinforced by increasing raw material innovations and recyclability standards. The trend toward prefabricated, low-energy buildings aligns with SIP strengths. The region also emphasizes circular economy principles, encouraging sustainable insulation materials with strong thermal performance and minimal site disruption.

Asia-Pacific

Asia-Pacific accounts for nearly 22% of the market share, with rapid growth led by China, Japan, Australia, and India. Rising urbanization, infrastructure development, and increasing awareness of energy conservation drive SIP adoption in this region. China leads in volume due to its aggressive housing and green building policies. Japan’s focus on disaster-resilient structures favors SIPs for modular and fast-deploy buildings. Australia promotes SIP use in remote housing and sustainable construction. Although India’s adoption remains nascent, growing demand for prefabricated and thermally efficient materials positions SIPs for long-term growth in urban housing and smart city projects.

Latin America

Latin America holds a smaller but emerging share of around 7% in the structural insulated panels market. Brazil and Mexico lead regional demand due to government housing programs, expanding commercial real estate, and growing awareness of sustainable building practices. Prefabricated structures using SIPs are gaining ground in disaster-prone and rural areas where quick assembly and thermal comfort are key. However, high upfront costs and limited local manufacturing pose challenges. With rising energy prices and a need for affordable housing, the region is expected to adopt SIPs more widely as cost barriers reduce and training improves.

Middle East & Africa

The Middle East & Africa region accounts for roughly 5% of the structural insulated panels market in 2024. Market expansion is driven by growing investments in smart cities, modular construction, and green buildings, particularly in the UAE and Saudi Arabia. Harsh climatic conditions increase the appeal of SIPs for thermal insulation and energy efficiency. Africa’s urban housing demand also supports future market growth, especially in South Africa and Nigeria. Limited awareness and infrastructure currently restrain broader adoption. However, with regional initiatives focusing on sustainable development, the market is poised for gradual expansion over the forecast period.

Structural Insulated Panels Market Segmentations:

By Product Type

- Glass Wool

- Stone Wool

- EPS

- XPS

- Phenolics

- PU/PIR

- Flexible Insulation

By Sheathing Type

- Oriented Strand Board (OSB)

- Sheet Metal

- Plywood

- Others

By Application

By End-Use

- Residential

- Commercial

- Non-Building

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The structural insulated panels market features a competitive landscape shaped by both global manufacturers and regional suppliers focused on energy-efficient building solutions. Key players such as Kingspan Group, Owens Corning, and METECNO maintain strong positions through extensive product portfolios, global distribution networks, and continuous innovation in insulation technologies. These companies invest in advanced manufacturing techniques and sustainable materials to meet evolving building codes and customer demands.

Mid-sized players like Enercept Inc., Foard Panel Inc., and The Murus Company compete by offering customized panel systems and technical support for residential and commercial applications. Strategic initiatives such as capacity expansions, acquisitions, and partnerships help players strengthen market presence and meet rising prefabrication demands. Localized production facilities and responsive supply chains give regional firms a competitive edge in niche markets. As demand for modular, energy-efficient construction rises, competition intensifies around thermal performance, cost efficiency, and speed of installation driving continuous product development and differentiation across the market.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Future Building of America

- Rautaruukki Corporation

- METECNO

- T Clear Corporation

- ACME PANEL

- Kingspan Group

- The Murus Company

- Eagle Panel Systems, Inc.

- Owens Corning

- Lattonedil Spa Milano

- Cornerstone Building Brands

- PFB Corporation

- Foam Laminates

- Enercept Inc.

- Foard Panel Inc.

Recent Developments

- In December 2024, AWIP collaboratively launched FASSADE with Bellara to offer a versatile solution for a wide range of single skin metal panels. Bellara Steel Siding products can be integrated into the system and can be easily attached using hat channels fastened through the tongue and groove joint.

- In 2024, Mayor Steve Rotheram officially launched a press machine at Hemsec’s structural insulated panel manufacturing hub. This machine is a paradigm of state-of-the-art. This groundbreaking technology is positioned to drive crucial innovation in the construction sector and a fabric-first approach to achieving a net-zero built environment, particularly in the area of social and affordable housing.

- In June 2022, Owens Corning acquired WearDeck, a Florida-based manufacturer of composite decking and structural lumber. This acquisition aims to enhance Owens Corning’s portfolio of weather-resistant decking and lumber products while expanding its expertise in commercial and residential applications.

Report Coverage

The research report offers an in-depth analysis based on Product Type, Sheathing Type, Application, End-Use and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The structural insulated panels market is expected to grow steadily due to rising energy efficiency needs and sustainable construction trends.

- Energy-efficient building regulations and incentives are key drivers accelerating adoption across residential and commercial projects.

- Growing interest in prefabricated and modular construction boosts demand for fast-installing, thermally efficient panel systems.

- Major players like Kingspan Group, Owens Corning, and METECNO lead the market with innovations in insulation materials and product customization.

- High initial costs and limited awareness in emerging economies continue to restrain full-scale adoption of structural insulated panels.

- North America dominates with a 35% share, followed by Europe with 28%, driven by strict energy codes and prefab housing growth.

- Asia-Pacific is the fastest-growing region due to urban expansion and construction modernization, especially in China and Japan.

- PU/PIR panels lead product demand with over 35% market share due to superior thermal performance and durability.

- Wall applications hold nearly 45% share, supported by demand for airtight, load-bearing insulation in residential projects.

- Cold chain infrastructure and modular healthcare buildings present new growth opportunities for panel manufacturers globally.