Market Overview:

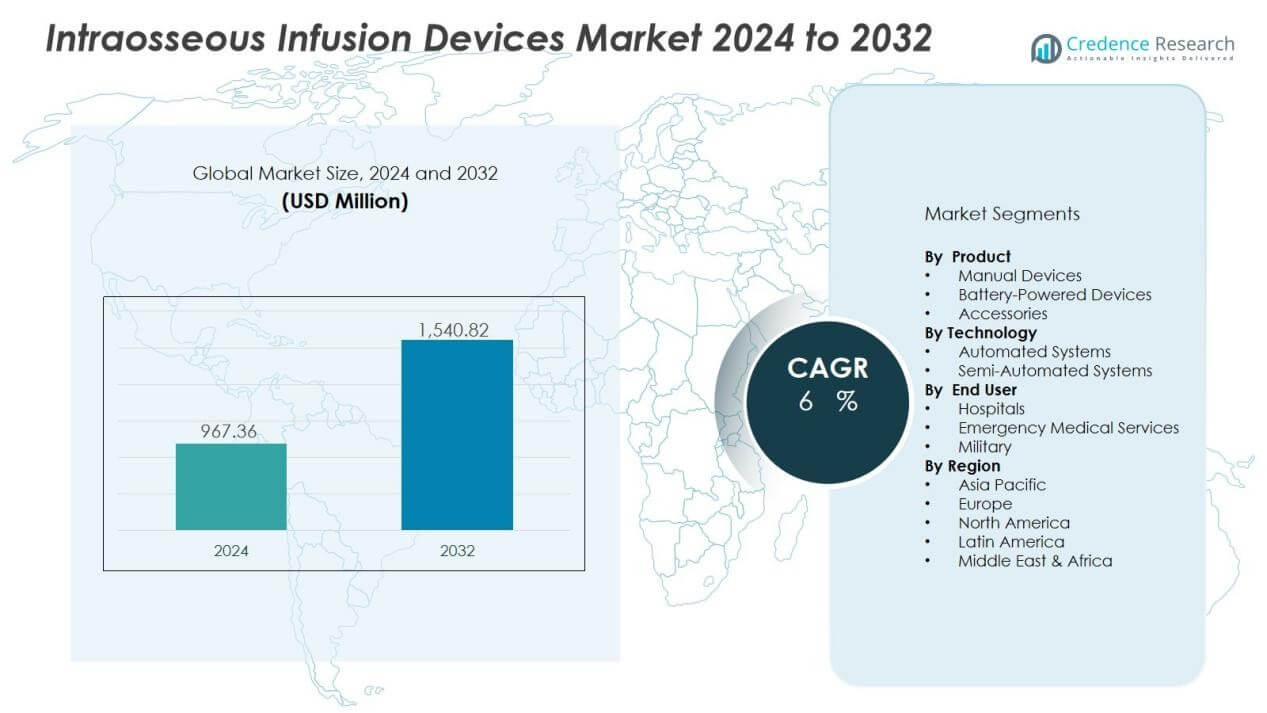

The intraosseous infusion devices market size was valued at USD 967.36 million in 2024 and is anticipated to reach USD 1,540.82 million by 2032, at a CAGR of 6% during the forecast period (2024-2032).

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Intraosseous Infusion Devices Market Size 2024 |

USD 967.36 Million |

| Intraosseous Infusion Devices Market, CAGR |

6% |

| Intraosseous Infusion Devices Market Size 2032 |

USD 1,540.82 Million |

Key market drivers include the growing prevalence of emergency conditions such as cardiac arrest, shock, and severe injuries, where fast fluid and medication delivery is essential. Advancements in device design, ease of use, and training programs for healthcare professionals have further improved adoption. Rising investments in emergency care infrastructure and military medical systems also boost the uptake of intraosseous infusion devices across regions.

Regionally, North America holds the largest share due to advanced healthcare facilities, widespread device availability, and strong focus on trauma care. Europe follows with significant adoption supported by established emergency response systems and government healthcare initiatives. Asia-Pacific is projected to record the fastest growth, driven by increasing healthcare spending, rising accident rates, and growing adoption of modern emergency care practices. Latin America and the Middle East & Africa show gradual progress as investments in critical care infrastructure expand.

Market Insights:

- The intraosseous infusion devices market was valued at USD 967.36 million in 2024 and is projected to reach USD 1,540.82 million by 2032, growing at a CAGR of 6%.

- Rising emergency cases such as cardiac arrest, trauma, and shock drive strong adoption of intraosseous devices for rapid vascular access.

- Battery-powered and automated devices are gaining preference due to ease of use, safety, and efficiency in critical care.

- Military operations and disaster response continue to create demand for portable intraosseous systems suited for field conditions.

- High product costs and lack of reimbursement policies in developing regions limit accessibility and adoption rates.

- North America held 42% share in 2024, supported by advanced healthcare infrastructure, high spending, and strong trauma care protocols.

- Asia-Pacific secured 21% share in 2024 and is expected to grow fastest due to rising healthcare investments, accident rates, and expanding emergency systems.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Rising Demand for Rapid Vascular Access in Emergency Care:

The intraosseous infusion devices market is driven by the urgent need for reliable vascular access in life-threatening situations. Emergency cases such as cardiac arrest, trauma, and shock often require immediate administration of fluids and drugs. Intravenous access can be difficult in critical conditions, making intraosseous devices a preferred option. It ensures fast, safe, and effective delivery, which strengthens its adoption in hospitals and emergency medical services.

- For instance, PAVmed Inc.’s PortIO™ Intraosseous Infusion System demonstrated a maintenance-free implant duration of over six months in a pre-clinical animal study, underscoring its reliability for long-term infusion applications.

Increasing Adoption in Military and Disaster Response Settings:

The demand for intraosseous infusion devices is expanding due to their role in military and disaster response. Combat injuries and natural disasters often involve conditions where rapid access is essential. Portable and easy-to-use designs make these devices suitable for field operations. It supports soldiers and emergency responders in delivering immediate care in resource-limited or high-stress environments.

- For instance, the FAST1™ Intraosseous Infusion System used by U.S. military medics provides rapid sternal access with flow rates of up to 80 mL/min and has a compact weight of 5 oz, making it highly suitable for battlefield conditions.

Technological Advancements and Ease of Use Driving Clinical Preference:

Continuous innovation in device technology supports the growth of the intraosseous infusion devices market. Modern systems are designed for simple operation, reducing the skill level required for effective use. Automated devices with safety features improve efficiency and reduce the risk of complications. It drives higher preference among healthcare professionals in both advanced and developing healthcare systems.

Expanding Healthcare Infrastructure and Emergency Preparedness Initiatives:

The global focus on strengthening emergency care systems positively influences market growth. Governments and healthcare organizations are investing in training programs, emergency equipment, and trauma centers. Growing awareness of the importance of preparedness for emergencies further drives adoption. It positions intraosseous infusion devices as a vital tool for improving patient outcomes and survival rates worldwide.

Market Trends:

Growing Integration of Intraosseous Devices into Emergency and Critical Care Protocols:

The intraosseous infusion devices market is witnessing stronger integration into emergency medical protocols worldwide. Hospitals, trauma centers, and emergency response units increasingly adopt these devices for rapid vascular access when intravenous routes fail. Clinical guidelines now recommend intraosseous access as a standard procedure in critical cases, which improves acceptance among practitioners. The growing role of pre-hospital care services, including ambulances and air medical teams, further accelerates demand. It reflects the shift toward ensuring reliable and immediate solutions in life-threatening situations. With continuous training programs, more healthcare professionals gain confidence in using these devices, strengthening overall adoption.

- For instance, Cardiff and Vale University Health Board in the UK has standardized emergency intraosseous cannulation using the EZ-IO device, with thorough training programs ensuring proficient use among clinical staff since 2015.

Technological Innovations and Focus on User-Friendly Automated Systems:

Innovation is shaping the intraosseous infusion devices market, with manufacturers introducing advanced features to improve safety and usability. Automated and battery-powered devices reduce the complexity of manual insertion, minimizing risks and ensuring consistent outcomes. Lightweight, portable systems are increasingly designed for use in field emergencies, disaster zones, and military operations. It allows practitioners to perform procedures quickly with minimal error, even under challenging conditions. Growing collaboration between manufacturers and healthcare institutions supports the development of next-generation products tailored for diverse settings. The emphasis on reducing training time and enhancing procedural efficiency makes these devices more attractive to both developed and emerging healthcare markets.

For example, the FAST1™ Intraosseous Infusion System designed for sternal insertion is compact and lightweight at just 5 ounces and supports fluid flow rates up to 80 mL/min via gravity drip.

Market Challenges Analysis:

High Costs and Limited Accessibility in Emerging Healthcare Systems:

The intraosseous infusion devices market faces challenges due to high product costs and limited accessibility in developing regions. Advanced automated systems are often priced beyond the budgets of smaller hospitals and rural clinics. Lack of reimbursement policies in certain countries further discourages adoption. It creates a gap between demand for rapid vascular access and the ability to supply these devices widely. Limited awareness among healthcare providers in low-resource settings also restricts growth. Without targeted investment and cost-reduction strategies, the market struggles to achieve broader penetration.

Risk of Complications and Dependence on Specialized Training:

The use of intraosseous devices requires proper training, which poses another barrier to growth. Inadequate skills can increase risks such as infection, bone fracture, or incorrect placement. Concerns about patient safety sometimes discourage clinicians from adopting intraosseous access as a first-line option. It highlights the need for continuous training and awareness programs. Despite advancements in user-friendly designs, resistance remains in facilities where traditional intravenous methods dominate. Overcoming this challenge requires stronger emphasis on education and clinical confidence to expand adoption globally.

Market Opportunities:

Expanding Applications Across Pre-Hospital and Emergency Response Systems:

The intraosseous infusion devices market offers strong opportunities through wider use in pre-hospital and emergency response systems. Growing investments in ambulance fleets, air medical services, and disaster preparedness programs support higher demand. Adoption is expanding in both civilian and military healthcare sectors, where rapid vascular access is critical. It positions these devices as a standard tool for frontline responders. Increasing awareness of their role in saving lives during cardiac arrest, trauma, and shock enhances future growth potential. Emerging markets with expanding emergency medical services represent a significant untapped opportunity.

Innovation in Device Design and Growing Penetration in Developing Regions:

Innovation presents another growth path for the intraosseous infusion devices market, with manufacturers focusing on user-friendly, automated systems. Devices designed for portability, safety, and ease of use are gaining traction across diverse care settings. It creates opportunities for broader adoption in resource-limited regions where advanced training may be less available. Partnerships between healthcare organizations and device makers can accelerate technology transfer and training initiatives. Rising healthcare spending in Asia-Pacific, Latin America, and Africa strengthens the scope for market penetration. These factors collectively create an environment where intraosseous devices can achieve higher acceptance and global reach.

Market Segmentation Analysis:

By Product:

The intraosseous infusion devices market by product is divided into manual devices, battery-powered devices, and accessories. Battery-powered devices hold a significant position due to their ease of use and ability to provide consistent insertion. Manual devices continue to find use in settings with limited resources, supported by lower costs and portability. Accessories, including needles and stabilizers, support recurring demand as essential components in clinical practice. It reflects a balance between advanced automated systems and affordable manual solutions.

- For instance, Teleflex Incorporated’s Arrow EZ-IO system offers quick insertion with a lithium battery-powered driver, ensuring rapid vascular access in emergency care. The driver has a useful life of approximately 500 insertions, which may vary depending on actual usage

By Technology:

Market segmentation by technology includes automated and semi-automated systems. Automated devices dominate due to their ability to reduce user error and ensure rapid access in emergencies. Semi-automated options maintain relevance in regions with budget constraints or limited training availability. It highlights growing preference for technologies that simplify procedures and minimize complications. Continuous innovation in this segment strengthens device efficiency and expands adoption in both civilian and military care.

- For instance, the Autonomous Portable Refrigeration Unit (APRU 6L) developed by Delta Development Team maintains blood temperatures for days on a single battery charge.

By End User:

The intraosseous infusion devices market by end user covers hospitals, emergency medical services, and military. Hospitals remain the leading segment due to advanced infrastructure and routine integration of intraosseous access in critical care. Emergency medical services adopt these devices to ensure reliable pre-hospital interventions in trauma and cardiac cases. Military organizations represent a strong growth area, supported by the need for rapid care in battlefield conditions. It demonstrates broad usage across diverse healthcare and emergency environments.

Segmentations:

By Product:

- Manual Devices

- Battery-Powered Devices

- Accessories

By Technology:

- Automated Systems

- Semi-Automated Systems

By End User:

- Hospitals

- Emergency Medical Services

- Military

By Region

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis:

Strong Presence of North America Supported by Advanced Emergency Care:

North America held 42% market share of the intraosseous infusion devices market in 2024, maintaining its leadership position. The region benefits from well-established emergency medical services and strong adoption of advanced technologies. Hospitals and trauma centers integrate intraosseous access into standard emergency protocols, supporting steady demand. It is further strengthened by ongoing training programs and government initiatives to improve patient survival rates. High healthcare spending and availability of automated devices accelerate adoption in both urban and rural systems. Military medical units in the U.S. also represent a key driver of regional growth.

Steady Growth in Europe with Emphasis on Healthcare Standards:

Europe accounted for 29% market share in 2024, supported by strict medical standards and organized healthcare systems. The region benefits from favorable government policies that prioritize emergency preparedness and training. Countries such as Germany, France, and the U.K. lead in adoption due to advanced trauma care infrastructure. It is also supported by increasing collaboration between device manufacturers and healthcare providers to improve technology access. Demand in Southern and Eastern Europe is rising as healthcare facilities invest in modern emergency tools. Continuous professional education across the region strengthens practitioner confidence and drives long-term growth.

Asia-Pacific Emerging as Fastest Growing Regional Market:

Asia-Pacific secured 21% market share in 2024, positioning itself as the fastest-growing region. Rising investments in healthcare infrastructure and growing focus on emergency care drive adoption. High accident rates and an expanding middle-class population increase demand for life-saving medical technologies. It benefits from government-led initiatives to improve pre-hospital and hospital-based trauma care. Manufacturers target the region with portable and user-friendly devices, meeting diverse healthcare needs. Expanding emergency response systems in India, China, and Southeast Asia are expected to further accelerate market expansion.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Pyng Medical Corp.

- Cook Medical Incorporated

- Biopsybell

- PAVmed

- Aero Healthcare

- PerSys Medical

- Teleflex, Inc.

- SAM Medical

- Becton Dickinson and Company

- Cardinal Health, Inc.

Competitive Analysis:

The intraosseous infusion devices market is defined by strong competition among global and regional players. Leading companies such as Pyng Medical Corp., Cook Medical Incorporated, Biopsybell, PAVmed, Aero Healthcare, PerSys Medical, and Teleflex, Inc. focus on advancing product performance and expanding clinical adoption. Innovation remains central, with emphasis on automated and battery-powered systems that reduce procedural risks and improve efficiency. It is supported by ongoing investments in R&D and collaborations with healthcare providers to enhance training and awareness. Strategic expansion into emerging markets and military healthcare further strengthens the growth opportunities for these players. Competitive differentiation is often based on product reliability, user-friendly features, and the ability to meet diverse emergency care needs worldwide.

Recent Developments:

- In August 2025 Cook Medical launched a new division focused on intraoperative MRI (iMRI) technology, aiming to drive wider adoption of innovative procedures in medical imaging.

- In August 2025, Veris Health, a PAVmed subsidiary, finalized a strategic partnership with The Ohio State’s James Cancer Hospital for commercial deployment of its Cancer Care Platform and integration with the hospital’s EHR system.

Report Coverage:

The research report offers an in-depth analysis based on Product, Technology, End User and Region. It details leading Market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current Market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven Market expansion in recent years. The report also explores Market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on Market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the Market.

Future Outlook:

- Growing integration of intraosseous infusion devices into emergency and trauma protocols will strengthen adoption across hospitals and EMS units.

- Expansion of pre-hospital applications, including ambulances, air medical services, and military operations, will drive sustained demand.

- Technological innovations in automated and portable systems will improve usability and safety, reducing risks for patients.

- Rising investments in emergency healthcare infrastructure will create opportunities for wider market penetration in developing regions.

- Training initiatives and education programs will continue to enhance clinical confidence and expand practitioner adoption.

- Strategic collaborations between manufacturers and healthcare providers will accelerate product innovation and expand global reach.

- Growing awareness of the life-saving potential of intraosseous access will increase acceptance among healthcare professionals.

- Regulatory approvals and streamlined distribution will help improve accessibility of advanced devices in underserved regions.

- Focus on cost-effective solutions will open the market for smaller hospitals and rural healthcare facilities.

- Sustained demand from military and disaster response systems will ensure long-term growth for intraosseous infusion devices.