Market Overview

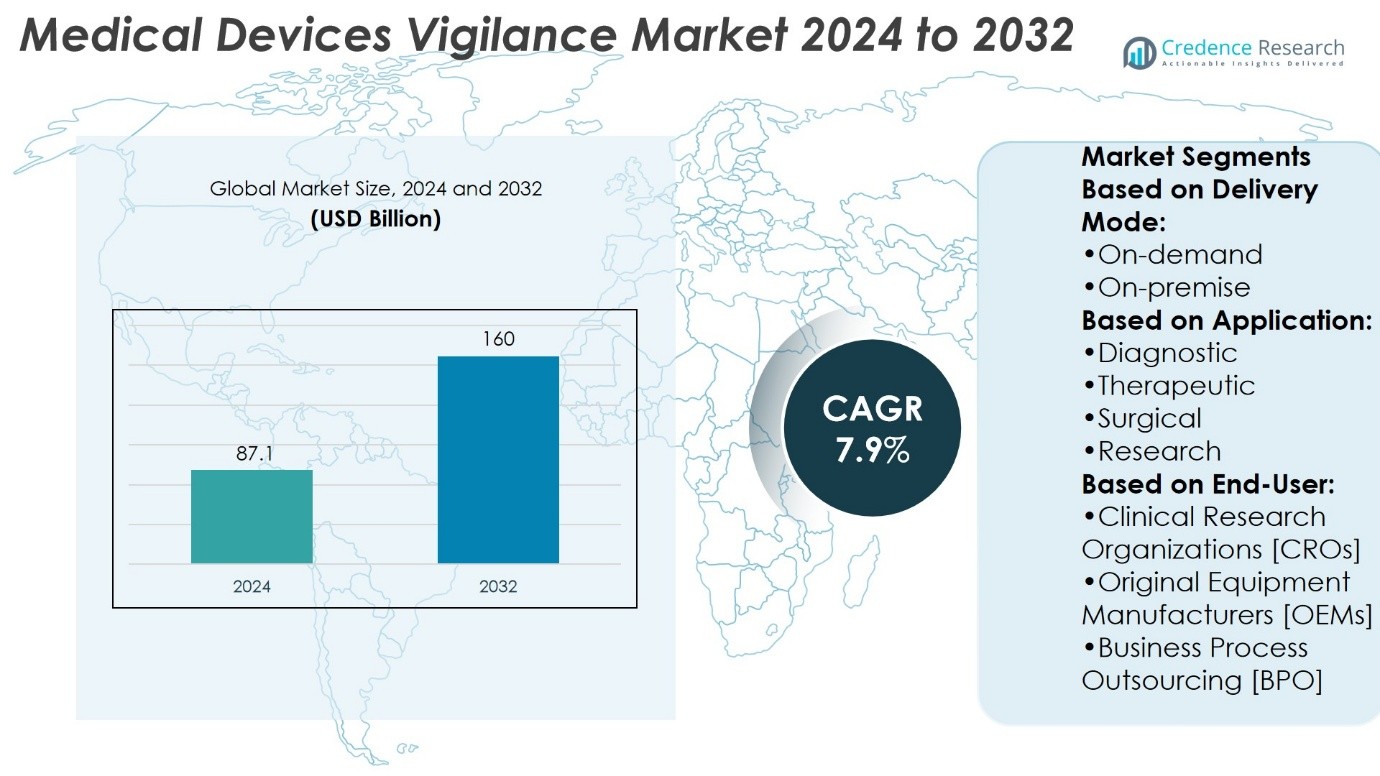

Medical Devices Vigilance Market size was valued at USD 87.1 billion in 2024 and is anticipated to reach USD 160 billion by 2032, at a CAGR of 7.9% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Medical Device Vigilance Market Size 2024 |

USD 87.1 Billion |

| Medical Device Vigilance Market, CAGR |

7.9% |

| Medical Device Vigilance Market Size 2032 |

USD 160 Billion |

The Medical Devices Vigilance Market is driven by increasing regulatory requirements and rising focus on patient safety across healthcare systems. It benefits from growing adoption of advanced post-market surveillance solutions that enable real-time monitoring, automated adverse event reporting, and predictive analytics. Digital transformation in healthcare, including cloud-based platforms and integration with hospital information systems, strengthens market growth. Demand rises from hospitals, clinical research organizations, and device manufacturers seeking compliance with FDA, EU MDR, and ISO standards. The market trends toward automation, interoperability, and scalable solutions, while emerging regions offer new opportunities for expansion and technological adoption.

North America leads the Medical Devices Vigilance Market due to advanced healthcare infrastructure and stringent regulatory frameworks, followed by Europe with strong compliance standards and digital adoption. Asia-Pacific shows rapid growth driven by expanding healthcare facilities and rising device usage, while Latin America and the Middle East & Africa maintain steady demand through gradual adoption and regulatory awareness. Key players driving market innovation and adoption include ZEINCRO, AssurX Inc., Sparta System, Oracle Corporation, Xybion Corporation, Sarjen Systems Pvt. Ltd., MDI Consultants, AB-Cube, Laerdal Medical, and Omnify Software, Inc.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- Medical Devices Vigilance Market size was valued at USD 87.1 billion in 2024 and is anticipated to reach USD 160 billion by 2032, at a CAGR of 7.9% during the forecast period.

- Increasing regulatory requirements and growing focus on patient safety drive market demand globally.

- Adoption of advanced post-market surveillance solutions with real-time monitoring, automated adverse event reporting, and predictive analytics strengthens growth.

- Digital transformation, including cloud-based platforms and integration with hospital information systems, enhances operational efficiency.

- Competition intensifies through automation, interoperability, customizable solutions, and strategic innovation.

- Market restraints include high implementation costs, complexity of regulatory compliance, and limited skilled workforce in emerging regions.

- North America leads due to advanced infrastructure and strict regulations, Europe follows with strong compliance standards, Asia-Pacific grows rapidly with expanding healthcare facilities, and Latin America and the Middle East & Africa show steady adoption.

Market Drivers

Rising Regulatory Stringency and Emphasis on Patient Safety

The Medical Devices Vigilance Market experiences strong growth due to increasing regulatory requirements and stringent safety standards. Governments and health authorities mandate timely reporting of adverse events, recalls, and device-related complications. Compliance with these regulations drives healthcare providers and manufacturers to adopt comprehensive vigilance systems. It ensures real-time monitoring of device performance and improves traceability across supply chains. Vigilance systems also support internal audits and regulatory inspections, reducing the risk of penalties. The focus on patient safety encourages proactive identification and mitigation of potential device-related risks. This regulatory pressure strengthens market adoption of advanced surveillance solutions.

- For instance, as of March 2025, there were 6,308 Medicare-certified Ambulatory Surgical Centers (ASCs) in the United States, based on 2023 data reported by the Medicare Payment Advisory Commission (MedPAC).

Technological Advancements in Monitoring and Reporting Systems

Advancements in digital tools, data analytics, and cloud-based platforms fuel the adoption of medical device vigilance solutions. It allows organizations to collect, store, and analyze large volumes of adverse event data efficiently. Automated reporting systems accelerate submission to regulatory authorities, enhancing compliance and reducing manual errors. Integration with electronic health records and hospital management systems improves accuracy and completeness of data. Real-time alerts and predictive analytics enable early identification of device-related risks. These capabilities support informed decision-making and enhance overall operational efficiency. Continuous innovation in software solutions ensures that vigilance systems keep pace with evolving regulatory and clinical requirements.

- For instance, Xybion Corporation’s eQCM-XD platform enabled a pharmaceutical client to significantly reduce average case resolution time by streamlining workflows and improving data management.

Increasing Adoption Across Healthcare Facilities and Medical Device Manufacturers

Healthcare institutions and device manufacturers recognize the importance of robust vigilance programs to safeguard patients and maintain credibility. It helps reduce product recalls and associated costs, while fostering trust among healthcare providers and patients. Hospitals and diagnostic centers implement surveillance systems to monitor in-use devices and respond promptly to incidents. Device manufacturers deploy vigilance software to track post-market performance and generate regulatory-compliant reports. Growing awareness of the benefits of proactive risk management drives investments in specialized platforms. Standardized processes for reporting, analysis, and corrective actions strengthen operational workflows. This widespread adoption directly contributes to market expansion globally.

Expansion of Global Medical Device Market and Complex Device Portfolio

The growing variety and complexity of medical devices create a need for efficient vigilance mechanisms. It ensures that innovative devices, such as implantables, diagnostic tools, and surgical instruments, maintain safety and performance standards. The surge in device approvals and product launches increases the volume of post-market surveillance activities. Vigilance systems provide structured frameworks for capturing, analyzing, and reporting adverse events effectively. The demand for risk management and quality assurance further encourages implementation of these platforms. Global expansion of healthcare infrastructure supports integration of vigilance solutions across regions. It enables manufacturers and providers to manage multi-market compliance efficiently while reducing patient safety risks.

Market Trends

Integration of Advanced Analytics and Artificial Intelligence in Vigilance Systems

The Medical Devices Vigilance Market increasingly incorporates artificial intelligence and advanced analytics to enhance data interpretation. It enables predictive insights from adverse event reports, improving early detection of potential device failures. Analytics-driven dashboards allow regulatory teams to visualize trends and identify high-risk devices effectively. Automated algorithms reduce human error in signal detection and reporting. Integration with electronic health records ensures seamless data flow and enhances post-market surveillance accuracy. Organizations adopt these technologies to strengthen compliance and improve operational efficiency. Real-time monitoring capabilities further support proactive risk management strategies.

- For instance, a December 2021 study analyzing data from January 2019 to January 2021 found a 48.0% decrease in surgical procedures in the U.S. during the initial shutdown period from March to May 2020, compared to the same period in 2019.

Expansion of Cloud-Based and Mobile Reporting Solutions

Cloud computing and mobile platforms emerge as a major trend in the Medical Devices Vigilance Market. It allows healthcare providers and manufacturers to access vigilance systems remotely and update reports instantly. Centralized cloud solutions reduce infrastructure costs while enhancing data security and accessibility. Mobile reporting applications facilitate on-site incident logging, improving timeliness and accuracy of submissions. Cloud platforms support scalability, enabling organizations to manage growing volumes of post-market data. They also offer automated backup and audit capabilities, increasing regulatory compliance confidence. The trend promotes collaboration between multiple stakeholders across different locations efficiently.

- For instance, according to the 2023 report of the MedTech Dive, breakthrough designations were awarded to 167 devices in 2023, as compared to 135 in 2022.

Focus on Global Standardization and Interoperability Across Regions

Organizations in the Medical Devices Vigilance Market emphasize harmonized reporting standards and interoperable systems across international markets. It ensures consistent adverse event reporting and simplifies submissions to multiple regulatory authorities. Standardized data formats improve transparency and enable benchmarking across regions. Interoperable platforms reduce duplication of effort, saving time and operational resources. Global harmonization allows manufacturers to implement a unified vigilance framework for diverse product portfolios. Stakeholders increasingly adopt solutions compatible with international standards, strengthening regulatory confidence. This trend encourages global adoption and continuous improvement of vigilance processes.

Shift Toward Proactive Risk Management and Predictive Safety Measures

The Medical Devices Vigilance Market shows a shift toward proactive risk management rather than reactive reporting. It emphasizes early identification of device-related issues to prevent adverse outcomes. Predictive safety measures leverage historical data to anticipate potential risks and implement corrective actions. Integration of surveillance systems with manufacturing and clinical workflows ensures comprehensive monitoring throughout the product lifecycle. Organizations prioritize solutions that offer actionable insights and rapid response mechanisms. The trend enhances patient safety, strengthens regulatory compliance, and optimizes operational efficiency. Vigilance platforms evolve to support continuous improvement in device performance and risk mitigation.

Market Challenges Analysis

Complex Regulatory Compliance and Diverse Reporting Requirements Across Regions

The Medical Devices Vigilance Market faces significant challenges due to varying regulatory frameworks and reporting standards in different regions. It requires manufacturers and healthcare providers to maintain multiple compliance protocols simultaneously. Differences in adverse event definitions, submission timelines, and documentation standards increase operational complexity. Organizations must invest in specialized personnel and training to ensure adherence to evolving regulations. Discrepancies between regional authorities can delay reporting and complicate post-market surveillance processes. Maintaining consistent quality and accuracy in data collection across borders remains a persistent challenge. Regulatory uncertainty may also affect strategic planning and technology adoption decisions.

Integration Difficulties and High Implementation Costs of Vigilance Systems

Healthcare institutions and device manufacturers encounter obstacles in implementing robust vigilance platforms. It involves integrating new systems with existing electronic health records, hospital management, and manufacturing workflows. High initial investment and ongoing maintenance costs deter some organizations from adopting comprehensive solutions. Data privacy and cybersecurity concerns further complicate implementation and system interoperability. Limited standardization across legacy systems can lead to fragmented reporting and reduced efficiency. Ensuring staff proficiency and continuous monitoring demands additional resources and time. These challenges slow widespread adoption and may impact the overall effectiveness of vigilance programs in detecting and mitigating device-related risks.

Market Opportunities

Growing Demand for Real-Time Post-Market Surveillance and Predictive Risk Management

The Medical Devices Vigilance Market offers significant opportunities through real-time post-market surveillance and predictive risk management solutions. It enables manufacturers and healthcare providers to identify potential device failures before they impact patients. Integration of cloud-based platforms and advanced analytics supports faster detection and reporting of adverse events. Organizations can leverage predictive models to anticipate device-related risks and implement preventive measures. Expansion of remote monitoring capabilities allows continuous oversight of high-risk devices across healthcare facilities. These advancements improve patient safety while enhancing operational efficiency. The trend encourages investment in scalable and technologically advanced vigilance systems.

Expansion into Emerging Markets and Support for Complex Medical Devices

Emerging markets present strong growth potential for the Medical Devices Vigilance Market due to expanding healthcare infrastructure and rising adoption of advanced medical technologies. It provides opportunities for manufacturers to deploy standardized vigilance solutions across diverse regions. Increasing introduction of complex devices such as implantables, diagnostic tools, and wearable health technologies creates demand for comprehensive monitoring systems. Organizations can capitalize on gaps in regulatory compliance support and reporting efficiency in these markets. Integration with hospital information systems and electronic health records enhances adoption potential. Focused strategies targeting emerging regions and technologically sophisticated devices strengthen market reach. Vigilance solutions that combine regulatory compliance, predictive analytics, and interoperability gain competitive advantage.

Market Segmentation Analysis:

By Delivery Mode

The Medical Devices Vigilance Market offers solutions through on-demand and on-premise delivery models to meet diverse organizational needs. On-demand platforms provide remote access, flexibility, and scalability, enabling healthcare providers and manufacturers to manage adverse event reporting without heavy infrastructure investment. It supports cloud-based data storage and real-time monitoring, improving regulatory compliance and operational efficiency. On-premise solutions appeal to organizations requiring full control over data security, internal workflows, and system customization. These platforms integrate with hospital management systems and enterprise IT networks to ensure comprehensive surveillance. Both delivery modes continue to evolve with enhanced automation, analytics, and interoperability features, expanding adoption across different healthcare environments.

- For instance, according to the data provided by the National Center for Biotechnology Information (NCBI) in August 2023, nearly 422 million people across the world are diagnosed with diabetes, with the majority living in low-and middle-income countries, and 1.5 million deaths are directly attributed to diabetes every year.

By Application

The Medical Devices Vigilance Market segments applications into diagnostic, therapeutic, surgical, and research devices to address unique monitoring needs. Diagnostic devices, including imaging and laboratory equipment, require continuous performance tracking to prevent reporting errors and ensure patient safety. Therapeutic devices such as infusion pumps and respiratory systems depend on vigilance systems for early detection of malfunctions or adverse events. Surgical instruments and implantables benefit from structured post-market surveillance, supporting traceability and corrective actions. Research devices, particularly those used in clinical trials, rely on accurate adverse event reporting to maintain regulatory compliance. It enhances safety monitoring and supports informed decision-making across all device categories.

- For instance, Centers for Disease Control and Prevention (CDC), the prevalence of type 2 diabetes among U.S. youth could increase by as much as 673% by 2060 if current trends continue. Under this same scenario, the total number of young people with diabetes including both type 1 and type 2—is projected to be approximately 526,000 by 2060.

By End-User

Clinical Research Organizations (CROs) represent a significant end-user segment within the Medical Devices Vigilance Market. It enables CROs to manage post-market surveillance and adverse event reporting for multiple clients efficiently. Vigilance systems streamline data collection, analysis, and submission processes, ensuring adherence to global regulatory standards. CROs leverage these platforms to improve trial quality, maintain data integrity, and minimize operational risks. Integration with sponsor systems and hospital records enhances real-time visibility of device performance. The increasing complexity of medical devices and global clinical trials strengthens demand for specialized vigilance solutions among CROs.

Segments:

Based on Delivery Mode:

Based on Application:

- Diagnostic

- Therapeutic

- Surgical

- Research

Based on End-User:

- Clinical Research Organizations [CROs]

- Original Equipment Manufacturers [OEMs]

- Business Process Outsourcing [BPO]

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America holds the largest market share in the Medical Devices Vigilance Market, accounting for approximately 35% of global adoption. The region benefits from advanced healthcare infrastructure, stringent regulatory frameworks, and high awareness of patient safety. It drives the adoption of sophisticated post-market surveillance solutions across hospitals, diagnostic centers, and device manufacturers. Vigilance platforms support compliance with the U.S. Food and Drug Administration (FDA) regulations and Health Canada requirements. It enables real-time monitoring of medical devices, automated adverse event reporting, and predictive analytics for risk management. The presence of major medical device manufacturers and clinical research organizations further strengthens market demand. Continuous investments in digital healthcare technologies and integration with electronic health records maintain North America’s leading position.

Europe

Europe contributes around 25% of the global Medical Devices Vigilance Market, reflecting steady growth driven by regulatory compliance and patient safety initiatives. The European Union Medical Device Regulation (EU MDR) mandates rigorous post-market surveillance, which increases demand for comprehensive vigilance systems. It allows manufacturers and healthcare providers to monitor device performance, manage recalls, and ensure reporting accuracy. Key countries, including Germany, France, and the United Kingdom, implement standardized reporting frameworks that encourage adoption of advanced surveillance platforms. Integration with hospital IT systems and local regulatory databases improves operational efficiency. Europe’s emphasis on quality assurance, coupled with growing adoption of digital tools, sustains the market’s expansion in the region.

Asia-Pacific

The Asia-Pacific region accounts for approximately 20% of the global Medical Devices Vigilance Market and demonstrates the fastest growth rate. Rising healthcare infrastructure, increased regulatory awareness, and growing adoption of advanced medical devices fuel market expansion. It enables hospitals and manufacturers in China, Japan, India, and Australia to deploy vigilant systems for monitoring diagnostic, therapeutic, and surgical devices. Cloud-based and mobile solutions gain traction due to their scalability and cost-effectiveness in diverse healthcare settings. Emerging economies invest in compliance training and technology integration to meet international safety standards. The region’s focus on improving patient outcomes and expanding medical device usage drives sustained market growth.

Latin America

Latin America holds an estimated 12% of the global market, driven by increased adoption of medical devices in countries such as Brazil, Mexico, and Argentina. It enables hospitals and clinical research organizations to manage adverse events efficiently and comply with local regulatory frameworks. Vigilance platforms support accurate reporting, recalls, and risk mitigation for diagnostic, therapeutic, and surgical devices. Implementation of cloud-based solutions improves data accessibility and reporting timelines across multiple facilities. It also facilitates training programs and capacity-building initiatives for healthcare personnel. Growing awareness of patient safety and compliance requirements supports steady market expansion in the region.

Middle East & Africa

The Middle East & Africa contributes approximately 8% of the global Medical Devices Vigilance Market, reflecting gradual adoption of advanced surveillance systems. It enables healthcare providers and device manufacturers to monitor post-market device performance and ensure compliance with evolving regulations. Countries such as Saudi Arabia, the United Arab Emirates, South Africa, and Egypt invest in digital healthcare infrastructure and regulatory enforcement. Vigilance platforms enhance operational efficiency and improve patient safety monitoring across hospitals and clinical research organizations. It supports training, technology integration, and multi-site reporting capabilities. The region offers opportunities for growth as governments prioritize modernization, risk management, and adoption of standardized surveillance practices.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Laerdal Medical

- AssurX Inc.

- AB-Cube

- Omnify Software, Inc.

- Sarjen Systems Pvt. Ltd.

- MDI Consultants, Inc.

- Sparta System

- Oracle Corporation

- ZEINCRO

- Xybion Corporation

Competitive Analysis

The Medical Devices Vigilance Market include ZEINCRO, AssurX Inc., Sparta System, Oracle Corporation, Xybion Corporation, Sarjen Systems Pvt. Ltd., MDI Consultants, Inc., AB-Cube, Laerdal Medical, and Omnify Software, Inc. The Medical Devices Vigilance Market is highly competitive, driven by the increasing demand for robust post-market surveillance solutions and regulatory compliance. Companies focus on delivering platforms that streamline adverse event reporting, enhance patient safety, and support global regulatory standards. Advanced features such as cloud-based access, real-time monitoring, predictive analytics, and integration with hospital information systems strengthen market offerings. Vendors differentiate themselves through customizable solutions, seamless interoperability, and specialized applications for diagnostic, therapeutic, surgical, and research devices. Investment in research and development enhances automation, data accuracy, and reporting efficiency. Competition also centers on pricing strategies, implementation support, and customer training to improve adoption. Continuous updates to comply with evolving regulations, including FDA, EU MDR, and ISO standards, drive innovation and ensure reliability. The market emphasizes operational efficiency, risk management, and technological advancement, creating an environment where companies compete on the quality, scalability, and regulatory alignment of their vigilance solutions.

Recent Developments

- In July 2025, Pharmacovigilance Automation (PV) landscape enforcement and technological advancements like AI-driven pharmacovigilance offers numerous advantages over outdated methods, including enhanced drug safety through faster detection, immediate.

- In January 2024, Medtronic received the U.S. FDA approval for the Percept RC Deep Brain Stimulation (DBS) system. This system helped physicians to personalize treatment for patients with brain-related disorders.

- In May 2023, Royal Philips showcased its cardiology devices portfolio, including diagnostic imaging devices, software, and services, at the European Association of Percutaneous Cardiovascular Interventions 2023.

- In May 2023, Cardinal Health expanded its distribution footprint by opening a new distribution center in Canada with the aim of catering to the rising demand for medical and surgical products in the country.

Report Coverage

The research report offers an in-depth analysis based on Delivery Mode, Application, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will expand with increasing adoption of advanced post-market surveillance systems.

- Integration of artificial intelligence and predictive analytics will improve adverse event detection.

- Cloud-based platforms will gain traction for their scalability and remote accessibility.

- Regulatory compliance requirements will continue to drive demand for comprehensive vigilance solutions.

- Expansion in emerging regions will create new opportunities for market growth.

- Hospitals and clinical research organizations will prioritize real-time monitoring and reporting efficiency.

- Investment in automation will reduce manual errors and enhance data accuracy.

- Demand for solutions supporting diagnostic, therapeutic, surgical, and research devices will rise.

- Collaboration between technology providers and healthcare institutions will strengthen market penetration.

- Continuous updates to align with evolving global standards will sustain innovation and market relevance.