Market Overview

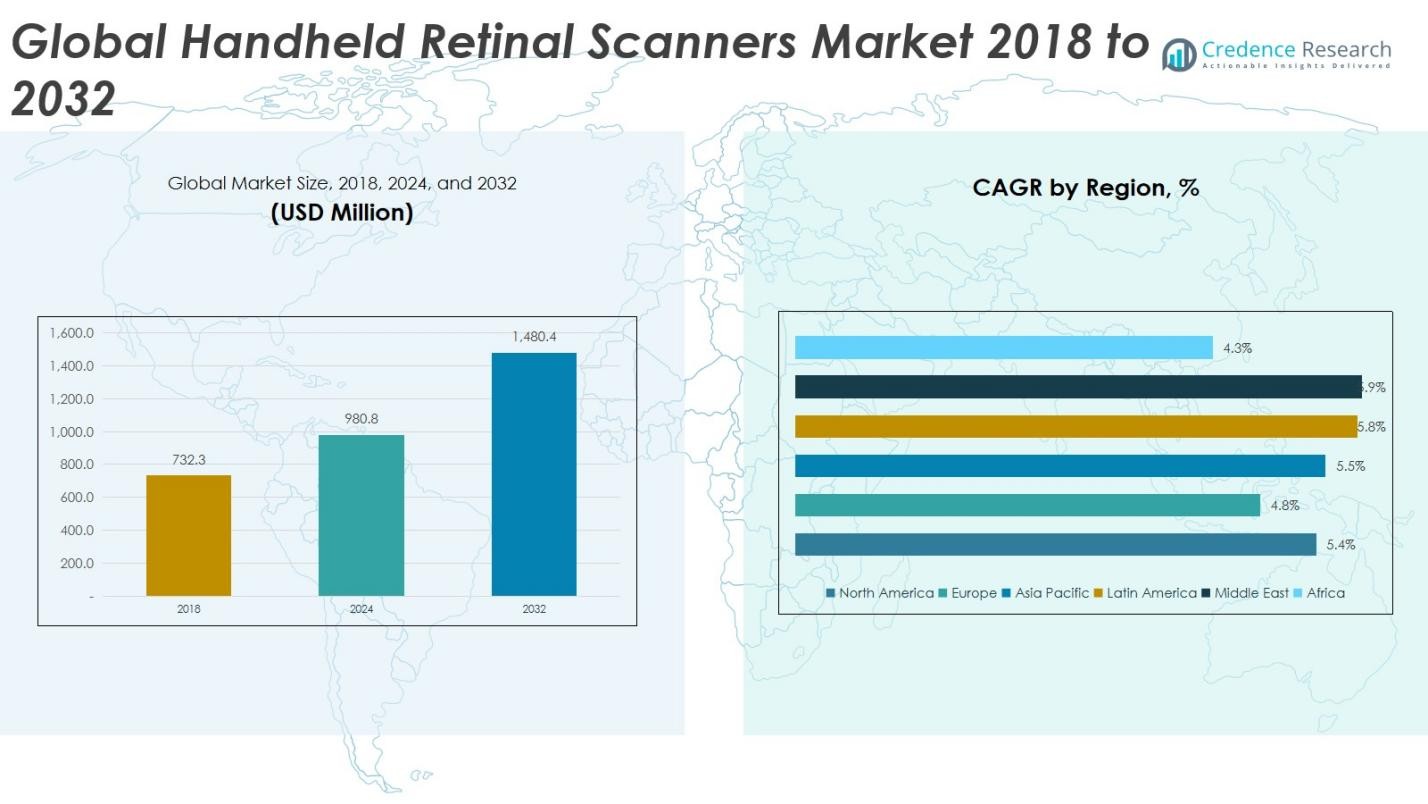

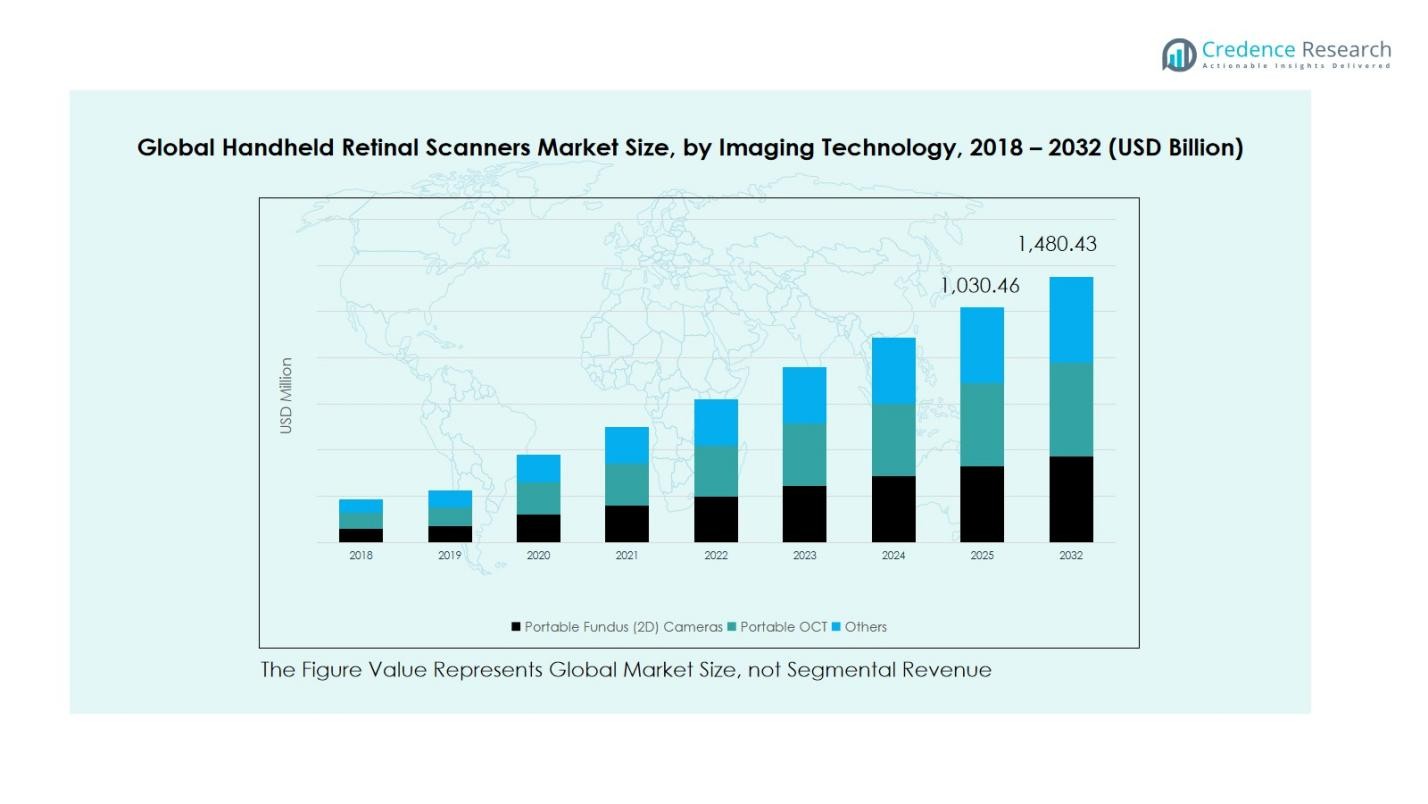

Global Handheld Retinal Scanners Market size was valued at USD 732.3 Million in 2018, growing to USD 980.8 Million in 2024, and is anticipated to reach USD 1,480.4 Million by 2032, at a CAGR of 5.31% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Handheld Retinal Scanners Market Size 2024 |

USD 980.8 Million |

| Handheld Retinal Scanners Market, CAGR |

5.31% |

| Handheld Retinal Scanners Market Size 2032 |

USD 1,480.4 Million |

The Global Handheld Retinal Scanners Market is highly competitive, with key players including Remidio, Topcon Healthcare, Eyenuk, Inc., Optomed, Volk Optical, Hillroom, Marco Lombart, and Zeiss. These companies are focusing on product innovation, AI-enabled imaging, and strategic partnerships to strengthen their market positions. Remidio and Topcon Healthcare lead in portable Fundus and OCT devices, while Optomed and Eyenuk, Inc. emphasize teleophthalmology integration. The market is regionally dominated by Asia Pacific, which holds a 34% share in 2024, driven by increasing adoption of retinal scanners in China, Japan, and India, rising prevalence of diabetes-related retinal disorders, and expanding healthcare infrastructure. The combination of technological advancement, government initiatives promoting early diagnosis, and affordability of portable devices positions Asia Pacific as the leading region, setting the pace for growth across the global handheld retinal scanners market.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Global Handheld Retinal Scanners Market was valued at USD 980.8 Million in 2024 and is projected to reach USD 1,480.4 Million by 2032, growing at a CAGR of 5.31%.

- Rising prevalence of retinal disorders, increasing demand for early diagnosis, and adoption of portable Fundus (2D) cameras and OCT devices are driving market growth globally.

- Market trends include integration of AI-enabled diagnostic tools, teleophthalmology adoption, and the expansion of handheld scanners into biometric authentication for banking, defense, and security applications.

- Competitive landscape is dominated by players such as Remidio, Topcon Healthcare, Eyenuk, Inc., Optomed, Volk Optical, Hillroom, Marco Lombart, and Zeiss, focusing on product innovation, strategic partnerships, and geographic expansion.

- Asia Pacific leads with a 34% market share, followed by North America and Europe, driven by adoption in China, Japan, and India, while Latin America, the Middle East, and Africa are gradually expanding with increasing healthcare infrastructure and technology penetration.

Market Segmentation Analysis:

By Imaging Technology:

The Portable Fundus (2D) Cameras segment dominates the handheld retinal scanners market, accounting for 52% of the global market share in 2024. Its popularity is driven by affordability, compact design, and ease of use in routine eye screenings and remote diagnostics. The Portable OCT segment follows, benefiting from high-resolution imaging for detailed retinal analysis, particularly in advanced medical centers. The Others category, including hybrid and emerging imaging technologies, holds a smaller share but is gaining traction due to innovations in non-invasive retinal diagnostics and telemedicine applications.

For instance, Remidio’s Fundus on Phone hybrid device integrates smartphone-based imaging and teleconsultation capabilities, advancing non-invasive retinal diagnostics in underserved regions.

By Application:

Within applications, Medical Diagnosis is the leading sub-segment, capturing 61% of the market share in 2024. Growth is fueled by the rising prevalence of retinal disorders, increasing awareness of early detection, and integration of handheld scanners in ophthalmology and optometry practices. The Banking & Finance segment leverages retinal scanners for secure biometric authentication, while Defense & Security adopts them for identity verification and border control. The Others category, including research and veterinary applications, remains niche but is gradually expanding with technological adoption.

For instance, Optomed Oyj’s handheld retinal camera is widely used by clinics in Europe and the U.S. for diabetic retinopathy screening, while Zeiss’s CLARUS 700 enables ultra-widefield retinal imaging to assist in glaucoma detection.

Key Growth Drivers

Rising Prevalence of Retinal Disorders

The increasing incidence of retinal diseases such as diabetic retinopathy, glaucoma, and macular degeneration is driving the demand for handheld retinal scanners. Early detection is critical for preventing vision loss, and portable devices allow ophthalmologists to conduct screenings efficiently across clinics and remote locations. Growing awareness among patients about preventive eye care further boosts adoption. This trend is particularly strong in aging populations and regions with limited access to advanced healthcare infrastructure, supporting sustained market growth during the forecast period.

For instance, Remidio’s Fundus on Phone (FOP) portable camera has enabled imaging of over ten million patients in five years, with offline AI software supporting large-scale screening for diabetic retinopathy and glaucoma across resource-limited settings.

Technological Advancements in Imaging Devices

Advances in imaging technology, including high-resolution Portable OCT and compact Fundus cameras, are enhancing diagnostic capabilities and ease of use. Improved portability, faster processing, and integration with telemedicine platforms make handheld scanners more attractive for healthcare providers. Innovations such as AI-enabled image analysis and cloud-based storage allow quicker, more accurate assessments, reducing reliance on traditional bulky equipment. These technological improvements are encouraging healthcare institutions to adopt handheld devices for routine screenings and specialized diagnostics, expanding market penetration globally.

For instance, Butterfly Network’s handheld ultrasound device combines AI-enabled image analysis with cloud storage, enabling clinicians to perform rapid, accurate assessments while reducing dependence on traditional bulky ultrasound machines.

Growing Demand for Biometric Security Applications

The adoption of handheld retinal scanners for secure biometric authentication is a significant growth driver. Sectors such as banking, finance, defense, and border control increasingly rely on retinal patterns for high-security identity verification due to their uniqueness and accuracy. The growing need for robust security solutions, combined with portable and user-friendly scanners, is fueling market expansion beyond healthcare. Integration with digital access systems and mobile verification platforms further strengthens adoption across enterprise and governmental applications.

Key Trends & Opportunities

Integration with Teleophthalmology and Remote Diagnostics

Handheld retinal scanners are increasingly integrated with teleophthalmology platforms, enabling remote consultations and screenings. This trend supports early diagnosis in underserved regions and rural areas, where access to ophthalmologists is limited. Portable devices paired with cloud-based data sharing allow real-time image transmission, enhancing patient care and treatment outcomes. The convergence of mobile healthcare solutions and handheld imaging presents a lucrative opportunity for market expansion, particularly in emerging economies with growing healthcare digitization initiatives.

For instance, the Stanford University Network for Diagnosis of ROP (SUNDROP) initiative in California utilized the RetCam II/III handheld retinal camera to screen 608 preterm infants across six neonatal intensive care units.

Rising Adoption of AI-Enabled Diagnostic Tools

Artificial intelligence is transforming retinal imaging by enabling automated detection of anomalies such as diabetic retinopathy and glaucoma. Handheld scanners equipped with AI algorithms reduce diagnostic errors, improve efficiency, and support large-scale screening programs. This trend opens opportunities for partnerships between device manufacturers and software developers, enhancing device capabilities. As healthcare providers increasingly adopt AI-powered solutions, the integration of AI with portable retinal scanners is expected to drive adoption and create new revenue streams across clinical and non-clinical applications.

For instance, RetmarkerDR, an AI-driven tool, aids in diabetic retinopathy screening by sorting out non-DR images and tracking disease progression over time, supporting ongoing patient management.

Key Challenges

High Device Costs and Limited Reimbursement

Despite growing demand, the high cost of handheld retinal scanners remains a barrier, particularly for small clinics and healthcare providers in developing regions. Limited reimbursement policies and budget constraints in public healthcare systems slow adoption. The initial investment and maintenance costs, coupled with the need for trained personnel, restrict widespread deployment. Manufacturers must address affordability and create flexible pricing models or leasing options to overcome this challenge and expand market penetration.

Data Privacy and Regulatory Concerns

The use of handheld retinal scanners for medical and biometric applications raises concerns about data privacy and compliance with stringent regulations. Handling sensitive patient or biometric data requires adherence to local and international privacy laws, which can be complex and vary across regions. Ensuring secure storage, transmission, and analysis of retinal images adds operational challenges for manufacturers and end-users. These regulatory and privacy concerns may slow adoption, requiring robust security protocols and clear compliance strategies to mitigate risks.

Regional Analysis

North America

North America held a significant share of the handheld retinal scanners market, with a valuation of USD 167.63 million in 2018, growing to USD 225.39 million in 2024 and projected to reach USD 341.98 million by 2032 at a CAGR of 5.4%. The region’s growth is driven by widespread adoption of advanced imaging technologies, rising prevalence of retinal disorders, and strong healthcare infrastructure. The U.S. leads market demand due to early adoption of portable diagnostic tools in ophthalmology and integration of telemedicine services. Canada and Mexico contribute steadily, with increased investment in eye care diagnostics.

Europe

Europe accounted for a market value of USD 195.76 million in 2018, expanding to USD 254.90 million in 2024 and expected to reach USD 370.11 million by 2032, with a CAGR of 4.8%. Germany, the UK, and France dominate due to advanced healthcare systems and growing geriatric populations. The demand for portable Fundus cameras and OCT devices is high, supported by preventive eye care initiatives. Investment in AI-assisted imaging and increased awareness of retinal health further fuels regional growth. Emerging economies in Eastern Europe are gradually contributing to market expansion.

Asia Pacific

Asia Pacific emerged as the largest market in 2018, valued at USD 250.68 million, and is projected to grow to USD 518.30 million by 2032 at a CAGR of 5.5%, reaching USD 339.01 million by 2024. Growth is fueled by rising prevalence of diabetes-related retinal disorders, expanding healthcare infrastructure, and increasing adoption of portable retinal scanners in China, Japan, and India. Government initiatives promoting early diagnosis and rural healthcare penetration enhance market potential. Technological adoption, coupled with affordable devices, positions the region for sustained growth throughout the forecast period.

Latin America

Latin America recorded a market size of USD 70.82 million in 2018, expected to grow to USD 97.66 million in 2024 and USD 153.08 million by 2032 at a CAGR of 5.8%. Brazil and Argentina lead the regional demand due to rising awareness of retinal health and growing use of portable diagnostic devices in medical and biometric applications. Increasing investment in ophthalmic healthcare infrastructure and the integration of handheld scanners in hospitals and clinics are major growth drivers. Emerging markets across the region are gradually expanding, contributing to overall market growth.

Middle East

The Middle East handheld retinal scanners market was valued at USD 31.78 million in 2018, projected to reach USD 43.95 million in 2024 and USD 69.14 million by 2032, at a CAGR of 5.9%. Growth is driven by investments in advanced healthcare facilities, rising demand for secure biometric systems, and increased adoption of portable Fundus and OCT devices. GCC countries, Israel, and Turkey dominate the market, leveraging technology for both medical diagnostics and security applications. Government initiatives supporting early retinal disease detection further strengthen market prospects across the region.

Africa

Africa held a smaller market share with USD 15.67 million in 2018, growing to USD 19.90 million in 2024 and expected to reach USD 27.83 million by 2032 at a CAGR of 4.3%. South Africa and Egypt lead adoption due to expanding healthcare access and growing awareness of retinal disorders. Portable retinal scanners are increasingly used in rural areas and mobile clinics for early detection programs. Limited infrastructure and high device costs restrict broader adoption, but increasing investment in teleophthalmology and healthcare digitization presents opportunities for market growth.

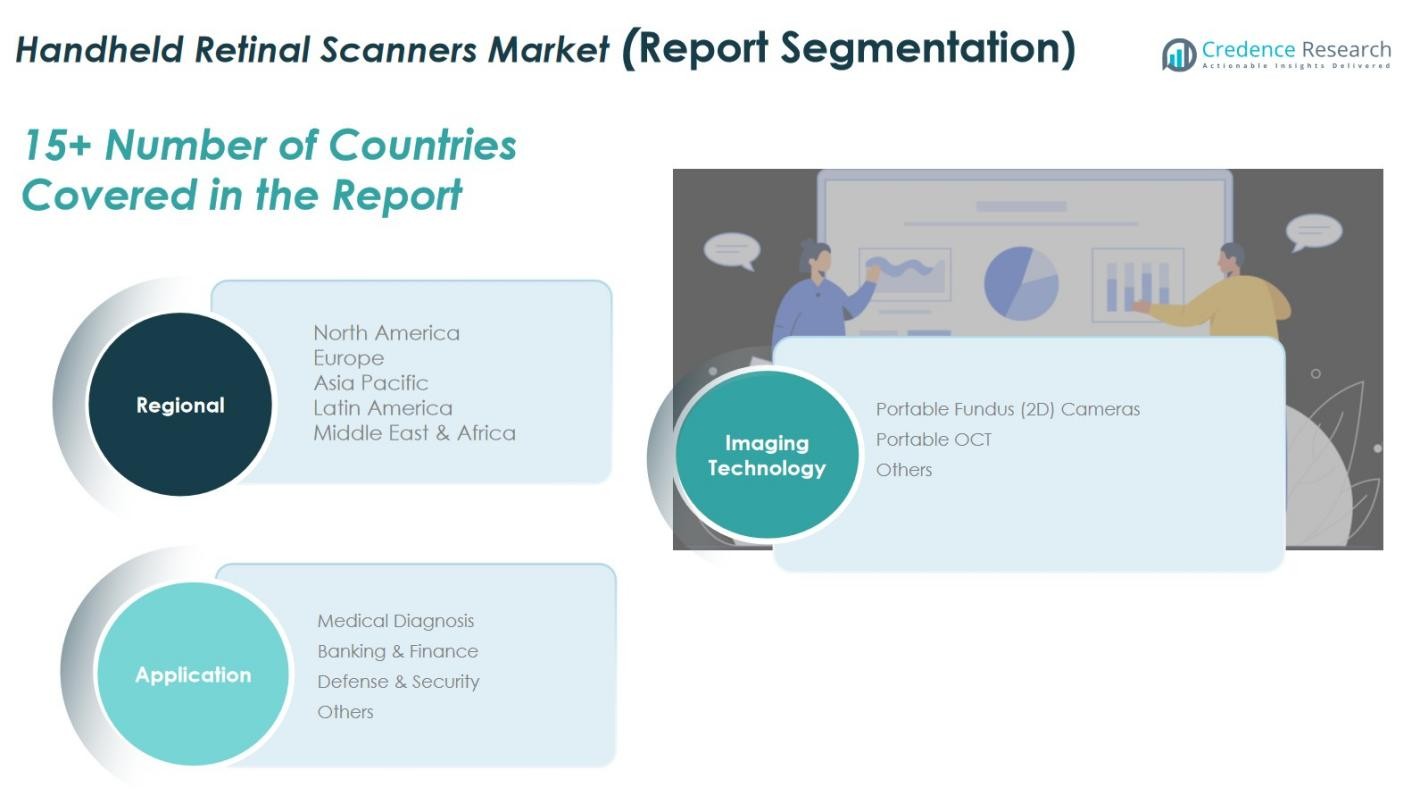

Market Segmentations:

By Imaging Technology:

- Portable Fundus (2D) Cameras

- Portable OCT

- Others

By Application:

- Medical Diagnosis

- Banking & Finance

- Defense & Security

- Others

By Region:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The competitive landscape of the Global Handheld Retinal Scanners Market is characterized by the presence of key players such as Remidio, Topcon Healthcare, Eyenuk, Inc., Optomed, Volk Optical, Hillroom, Marco Lombart, and Zeiss. These companies are actively focusing on product innovation, strategic partnerships, and geographical expansion to strengthen their market position. Manufacturers are investing in advanced imaging technologies, including high-resolution Portable OCT and Fundus cameras, while integrating AI-enabled diagnostic tools to enhance accuracy and efficiency. Companies are also exploring teleophthalmology solutions to expand into emerging markets. Competitive strategies include mergers, acquisitions, and collaborations to diversify product portfolios and capture a larger share of the growing healthcare and biometric applications. Continuous R&D, coupled with strong distribution networks and customer support services, allows leading players to maintain a competitive edge, meet evolving regulatory requirements, and address rising demand for portable, efficient retinal imaging solutions globally.

Key Player Analysis

- Remidio

- Topcon Healthcare

- Eyenuk, Inc.

- Optomed

- Volk Optical

- Hillroom

- Marco Lombart

- Zeiss

- Other Key Players

Recent Developments

- In May 2024, Optomed Oyj and AEYE Health received U.S. FDA 510(k) clearance for the handheld fundus camera “Aurora AEYE”, enabling portable retinal AI screening.

- In April 2023, Phelcom Technologies launched its handheld fundus camera “Eyer” in Japan, expanding commercialization to five countries.

- In July 2025, Topcon Healthcare, Inc. acquired Intelligent Retinal Imaging Systems (IRIS), a U.S.-based cloud-based AI-assisted retinal screening company, to enhance its “Healthcare from the Eye” strategy.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Report Coverage

The research report offers an in-depth analysis based on Imaging Technology, Application and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market is expected to witness steady growth driven by rising prevalence of retinal disorders.

- Increasing adoption of portable Fundus and OCT scanners in clinics and hospitals will fuel demand.

- Integration of AI-powered diagnostic tools will enhance efficiency and accuracy in retinal imaging.

- Teleophthalmology and remote diagnostic solutions will expand market reach in underserved regions.

- Growing use of retinal scanners for biometric authentication in banking, defense, and security sectors will boost adoption.

- Continuous technological innovations will lead to smaller, faster, and more affordable handheld devices.

- Expansion in emerging markets across Asia Pacific, Latin America, and the Middle East will drive growth.

- Strategic partnerships, mergers, and acquisitions among key players will strengthen competitive positioning.

- Rising awareness of preventive eye care will encourage early adoption of handheld scanners.

- Increasing investment in healthcare infrastructure and digital health solutions will support long-term market growth.