Market Overview

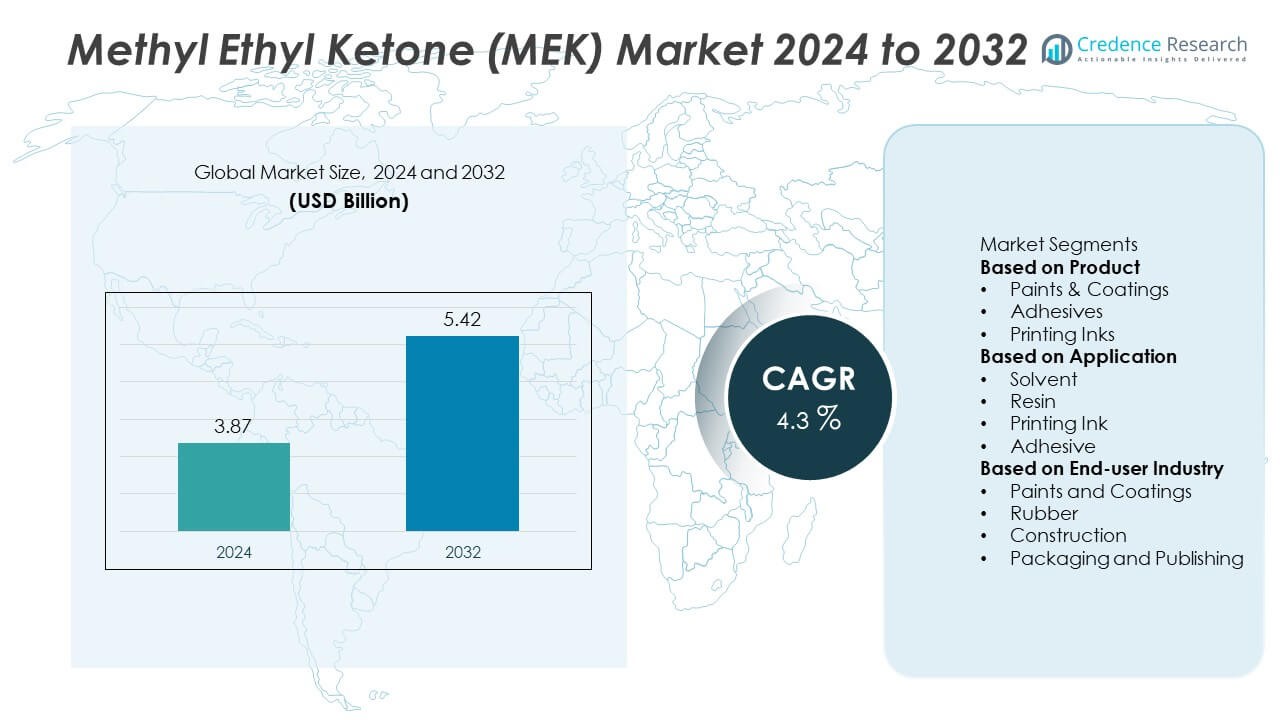

The Methyl Ethyl Ketone (MEK) Market was valued at USD 3.87 billion in 2024 and is anticipated to reach USD 5.42 billion by 2032, expanding at a CAGR of 4.3% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Methyl Ethyl Ketone (MEK) Market Size 2024 |

USD 3.87 Billion |

| Methyl Ethyl Ketone (MEK) Market, CAGR |

4.3% |

| Methyl Ethyl Ketone (MEK) Market Size 2032 |

USD 5.42 Billion |

The Methyl Ethyl Ketone (MEK) Market is driven by strong demand from paints, coatings, adhesives, and printing inks, where its fast evaporation rate and high solvency improve performance and efficiency. Growth in construction, automotive refinishing, and packaging industries supports wider adoption.

The Methyl Ethyl Ketone (MEK) Market demonstrates strong geographical presence across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, each region shaped by distinct industrial demands. North America shows steady adoption supported by advanced construction and automotive refinishing sectors. Europe emphasizes sustainability and regulatory compliance, driving interest in bio-based MEK formulations. Asia-Pacific remains the fastest-growing region with expanding infrastructure, high-volume automotive production, and strong packaging demand across China, India, and Southeast Asia. Latin America and the Middle East & Africa record gradual growth, supported by industrialization and construction projects. Leading companies actively shaping the market include ExxonMobil Corporation, which invests in large-scale petrochemical operations, Arkema S.A., known for specialty chemicals and eco-friendly solutions, INEOS Group, with a strong global supply network, and Shell Plc, which continues to strengthen solvent production capabilities worldwide. These players focus on innovation, capacity expansion, and sustainability-driven strategies to maintain competitiveness.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Methyl Ethyl Ketone (MEK) Market was valued at USD 3.87 billion in 2024 and is projected to reach USD 5.42 billion by 2032, expanding at a CAGR of 4.3% during the forecast period.

- Demand is strongly driven by its application in paints, coatings, adhesives, and printing inks, where fast evaporation and high solvency enhance efficiency and performance.

- Key trends include the shift toward bio-based and eco-friendly MEK formulations, expansion of specialty chemical applications, and rising use in electronics for high-purity cleaning.

- The market is competitive, with major companies such as ExxonMobil Corporation, Shell Plc, Arkema S.A., INEOS Group, Sasol Limited, and Idemitsu Kosan Co., Ltd. investing in production capacity, sustainability initiatives, and technological innovations.

- Constraints arise from strict environmental regulations on volatile organic compounds, fluctuating raw material prices, and supply chain disruptions that increase cost and reduce predictability.

- North America shows strong adoption in construction and automotive refinishing, Europe emphasizes sustainable solvent solutions, Asia-Pacific records the fastest growth with high demand from infrastructure and packaging, while Latin America and the Middle East & Africa show steady expansion supported by industrialization.

- The sector continues to evolve as industries adopt MEK for industrial coatings, adhesives, lubricants, and specialty chemicals, creating opportunities for producers to expand into high-value and sustainable markets.

Market Drivers

Expanding Demand from Paints and Coatings Industry

The Methyl Ethyl Ketone (MEK) Market grows steadily with rising consumption in the paints and coatings sector. MEK is widely used as a solvent due to its fast evaporation rate and ability to dissolve resins effectively. It enhances the performance of coatings by improving drying time, gloss, and film quality. Demand for high-performance coatings in construction and automotive industries supports consistent growth. It also plays an essential role in protective coatings applied in industrial equipment and infrastructure. The strong link between MEK and coatings demand strengthens its position in global markets.

- For instance, Sherwin-Williams reported in 2023 that it produced more than 1.57 billion gallons of paints and coatings globally, much of which relied on solvents like MEK to ensure fast-drying and high-performance finishes across construction and automotive sectors.

Growing Use in Adhesives and Printing Inks Applications

The Methyl Ethyl Ketone (MEK) Market benefits from its increasing application in adhesives and printing inks. It enables better bonding strength and flexibility, making it suitable for packaging, footwear, and automotive industries. MEK’s role in formulating quick-drying inks also supports the expansion of commercial printing and labeling. It contributes to the performance of adhesives used in high-stress environments, where durability and reliability are critical. Growth in packaging driven by e-commerce and consumer goods reinforces the demand for MEK-based adhesives. Its versatility across different formulations ensures steady adoption across industrial sectors.

- For instance, Henkel AG & Co. KGaA reported in 2023 that its Adhesive Technologies division generated sales exceeding €11.2 billion, with a significant share coming from MEK-based adhesive systems used in packaging, automotive assembly, and flexible labeling solutions.

Rising Consumption in Chemical Intermediates and Extraction Processes

The Methyl Ethyl Ketone (MEK) Market gains momentum from its use as an intermediate in chemical manufacturing and extraction processes. MEK is widely applied in dewaxing lubricating oils, improving performance in automotive and machinery applications. It also serves as a precursor in the production of specialty chemicals, resins, and coatings. It provides effective extraction capabilities in processes requiring high selectivity and efficiency. The demand for high-quality lubricants and specialty chemicals enhances MEK consumption in this segment. Its importance in downstream chemical applications ensures sustainable demand over time.

Industrial Growth and Expanding End-Use Sectors

The Methyl Ethyl Ketone (MEK) Market is supported by broad industrial expansion and diverse end-use applications. Growth in construction, automotive, packaging, and electronics industries sustains strong demand for MEK as a critical solvent. It plays a vital role in ensuring process efficiency, quality performance, and durability of finished products. Industrialization in emerging economies creates new opportunities for MEK adoption in various applications. Rising demand for maintenance coatings and adhesive solutions further reinforces its market value. Its adaptability across multiple industries secures its long-term relevance in global supply chains.

Market Trends

Shift Toward Eco-Friendly and Sustainable Solvent Solutions

The Methyl Ethyl Ketone (MEK) Market reflects a clear trend toward sustainability, with manufacturers developing greener alternatives and blends. Regulatory pressures on volatile organic compounds encourage companies to innovate low-emission solvent systems. It creates opportunities for bio-based MEK derived from renewable feedstocks. Companies also invest in advanced production technologies to reduce environmental impact and meet global compliance standards. The transition aligns with broader sustainability initiatives in coatings, adhesives, and chemical industries. It positions MEK as part of a long-term shift toward environmentally responsible practices.

- For instance, Arkema announced in December 2024 that it completed the acquisition of Dow’s flexible packaging laminating adhesives unit, expanding production of sustainable adhesives with a portfolio capable of reducing VOC emissions by up to 40,000 tonnes annually in solvent-intensive industries.

Rising Demand from Construction and Infrastructure Projects

The Methyl Ethyl Ketone (MEK) Market benefits from increasing construction and infrastructure activities worldwide. MEK’s role in high-performance paints and coatings strengthens its relevance in projects requiring durability and quick drying. It supports large-scale applications such as bridges, commercial complexes, and industrial facilities. Growing investments in smart city developments and renovation projects further reinforce demand. The requirement for protective coatings that resist harsh environments sustains the use of MEK-based formulations. It highlights the close link between industrial expansion and MEK consumption.

- For instance, Nippon Paint Holdings reported in 2023 that it supplied over 1.6 billion liters of coatings globally, with a significant proportion applied in construction and infrastructure projects where solvents like MEK enhance protective performance and durability.

Integration of MEK in Automotive Refinishing and Coatings

The Methyl Ethyl Ketone (MEK) Market records steady growth through its use in automotive refinishing and coatings. MEK enhances coating properties by improving gloss, finish, and drying performance in automotive applications. It ensures consistent results in large-scale production as well as aftermarket refinishing. The rising preference for lightweight and high-durability coatings in vehicles supports this trend. Automotive OEMs and refinishing workshops adopt MEK-based formulations to meet performance and appearance standards. It reinforces MEK’s importance in sustaining innovation within the automotive coatings segment.

Expansion of MEK Applications in Electronics and Specialty Chemicals

The Methyl Ethyl Ketone (MEK) Market continues to expand with growing applications in electronics and specialty chemicals. MEK’s strong solvency supports precision cleaning of electronic components and circuit boards. It also plays a role in the formulation of specialty resins and high-performance polymers. Electronics manufacturers adopt MEK for processes requiring purity and reliability. The demand for specialty chemicals in advanced manufacturing drives further opportunities for MEK suppliers. It underscores the diversification of MEK applications beyond traditional coatings and adhesives.

Market Challenges Analysis

Regulatory Pressure and Environmental Concerns

The Methyl Ethyl Ketone (MEK) Market faces challenges due to strict environmental regulations and rising concerns over volatile organic compound emissions. Regulatory bodies impose limits on solvent usage in paints, coatings, and adhesives to reduce air pollution and safeguard worker safety. It creates compliance burdens for manufacturers who must invest in cleaner technologies and reformulated products. Companies that fail to adapt encounter restrictions on market access and growing competition from eco-friendly alternatives. The need to balance performance with sustainability complicates product development. It places continuous pressure on producers to innovate while keeping costs manageable.

Volatility in Raw Material Prices and Supply Constraints

The Methyl Ethyl Ketone (MEK) Market also struggles with fluctuating raw material prices and disruptions in supply chains. MEK production depends heavily on petrochemical feedstocks such as 2-butanol, which are subject to oil price volatility. It impacts overall production costs and creates uncertainty for both manufacturers and end users. Supply disruptions caused by geopolitical tensions or refinery outages further strain availability. Industries reliant on MEK must contend with unstable sourcing conditions that limit planning and efficiency. It raises risks for companies dependent on consistent quality and supply in large-scale operations.

Market Opportunities

Expansion of Demand in Emerging Economies and Industrial Growth

The Methyl Ethyl Ketone (MEK) Market presents strong opportunities in emerging economies where construction, automotive, and manufacturing industries are expanding rapidly. Rising infrastructure projects and urbanization create consistent demand for high-performance paints, adhesives, and coatings that rely on MEK as a solvent. It supports large-scale industrial applications where durability, quick drying, and process efficiency are critical. Growth in automotive refinishing markets across Asia-Pacific and Latin America further enhances consumption potential. Governments promoting industrial development strengthen the adoption of MEK across diverse end-use industries. It positions MEK as a key enabler of industrial progress in fast-developing regions.

Advancements in Eco-Friendly Formulations and Specialty Applications

The Methyl Ethyl Ketone (MEK) Market creates opportunities through the development of eco-friendly formulations and specialized applications. Companies are investing in bio-based MEK derived from renewable feedstocks to meet regulatory standards and consumer preferences for sustainable products. It also finds growing use in electronics and specialty chemicals where high solvency and purity are required. Demand for advanced polymers, specialty resins, and precision cleaning solutions expands the role of MEK in high-value industries. Adoption of green technologies and high-performance materials further increases its application scope. It enables producers to diversify offerings while aligning with evolving global sustainability trends.

Market Segmentation Analysis:

By Product

The Methyl Ethyl Ketone (MEK) Market is segmented by product into synthetic MEK and bio-based MEK. Synthetic MEK dominates the market due to its established use in coatings, adhesives, and chemical processing. It offers consistent quality and availability, making it the preferred choice for large-scale industrial operations. Bio-based MEK, although still emerging, is gaining attention as industries move toward sustainable solutions. It is produced from renewable feedstocks and provides lower environmental impact compared to traditional petrochemical-derived MEK. Growing environmental regulations and consumer demand for eco-friendly products encourage investments in bio-based alternatives. This balance between established synthetic dominance and future growth in bio-based products shapes the market trajectory.

- For instance, Shell reported in 2023 that it invested over $1.6 billion in developing renewable and low-carbon fuel and solvent technologies, including pathways for bio-based ketone production, aligning with stricter environmental standards.

By Application

The Methyl Ethyl Ketone (MEK) Market is segmented by application into paints and coatings, adhesives, printing inks, chemical intermediates, and others. Paints and coatings represent the largest application segment, supported by demand in automotive, construction, and industrial maintenance. It enhances coating performance by improving drying speed, gloss, and durability. Adhesives form another critical segment where MEK strengthens bonding capacity and flexibility in packaging, footwear, and automotive applications. Printing inks rely on MEK for quick drying and high-quality finishes, supporting commercial printing and labeling industries. Chemical intermediates also represent an important application, with MEK being used in dewaxing lubricants and specialty chemical production. This wide application base underpins its importance across multiple sectors.

- For instance, PPG Industries reported that it sold over 1.3 billion liters of coatings and adhesives globally, much of which depended on solvent systems such as MEK to achieve durability, fast drying, and consistent quality in construction and automotive applications.

By End-User Industry

The Methyl Ethyl Ketone (MEK) Market is segmented by end-user industry into construction, automotive, packaging, electronics, and others. Construction leads demand due to its extensive use in protective coatings and adhesives for infrastructure projects. It supports long-lasting performance in structures exposed to harsh conditions. The automotive industry consumes MEK through refinishing and high-performance coatings, ensuring durability and aesthetic appeal. Packaging industries use MEK in adhesives and inks that support consumer goods and e-commerce growth. Electronics adopt MEK for cleaning components and as a solvent in specialty polymers. Other industrial users, including textiles and chemicals, rely on MEK for various production processes. Its versatility across end-use industries confirms its central role in global industrial supply chains.

Segments:

Based on Product

- Paints & Coatings

- Adhesives

- Printing Inks

Based on Application

- Solvent

- Resin

- Printing Ink

- Adhesive

Based on End-user Industry

- Paints and Coatings

- Rubber

- Construction

- Packaging and Publishing

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America accounts for 29.4% of the Methyl Ethyl Ketone (MEK) Market in 2024, supported by its established industrial base and advanced end-user sectors. The region benefits from strong demand in paints and coatings, driven by infrastructure upgrades, housing projects, and automotive refinishing. It also records consistent consumption in packaging and adhesives, especially in the United States where e-commerce continues to expand rapidly. MEK plays an essential role in ensuring high-quality finishes for industrial coatings and protective applications across construction and oilfield equipment. Canada adds further demand through construction activities and specialty chemical use. The presence of leading chemical manufacturers strengthens the region’s supply capabilities, making North America a steady consumer as well as an exporter of MEK-based solutions.

Europe

Europe represents 27.1% of the Methyl Ethyl Ketone (MEK) Market in 2024, driven by automotive manufacturing, construction activity, and regulatory standards for high-performance coatings. Germany, France, and the United Kingdom remain key hubs for MEK adoption in paints, adhesives, and specialty chemical industries. It is widely used to meet the needs of industrial coatings that require durability and compliance with EU sustainability directives. Demand also comes from packaging and printing applications, where MEK-based adhesives and inks are used in large-scale labeling and consumer goods production. The European market experiences pressure to reduce VOC emissions, prompting gradual investment in bio-based MEK and reformulated solvent systems. This transition is reshaping long-term growth opportunities in the region while maintaining a high consumption base across traditional applications.

Asia-Pacific

Asia-Pacific holds 33.8% of the Methyl Ethyl Ketone (MEK) Market in 2024, making it the largest regional contributor. The region is fueled by rapid industrialization, infrastructure development, and high-volume automotive production in countries such as China, India, Japan, and South Korea. Construction growth across emerging economies drives significant demand for protective coatings and adhesives that depend on MEK’s solvency and quick-drying properties. The region also witnesses rising adoption in packaging and printing inks, supported by expanding consumer markets and strong e-commerce penetration. Electronics manufacturing in South Korea, Japan, and China further boosts MEK use in cleaning and specialty chemical processes. The dominance of Asia-Pacific is reinforced by competitive production costs and availability of petrochemical feedstocks, making it both a major producer and consumer in the global market.

Latin America

Latin America accounts for 5.7% of the Methyl Ethyl Ketone (MEK) Market in 2024, with Brazil and Mexico as leading consumers. Growth in this region is tied to increasing construction activity, automotive refinishing, and packaging applications. It benefits from expanding industrial operations and infrastructure projects that demand durable coatings and adhesives. E-commerce growth fuels packaging sector demand, where MEK-based adhesives support flexible packaging production. Supply chain challenges and dependence on imports influence availability, but regional manufacturers are gradually strengthening capacity. The shift toward industrial modernization positions Latin America as a market with moderate but steady growth potential for MEK suppliers.

Middle East & Africa

The Middle East & Africa contributes 4.0% of the Methyl Ethyl Ketone (MEK) Market in 2024, supported by infrastructure projects, oil and gas operations, and construction activities. The Gulf countries, led by Saudi Arabia and the UAE, generate strong demand for protective coatings in industrial and commercial projects. MEK finds consistent applications in adhesives and coatings used in large-scale urban development and maintenance activities. Africa contributes through gradual growth in construction and consumer goods packaging, particularly in Nigeria, South Africa, and Egypt. It benefits from ongoing industrialization and government-led infrastructure investments. While the overall market share is relatively small, the region offers long-term opportunities for MEK adoption in construction, packaging, and specialty chemical applications.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- ExxonMobil Corporation

- Sasol Limited

- Maruzen Petrochemical Co., Ltd.

- Arkema S.A.

- ENEOS Corporation

- Nova Molecular Technologies

- Shell Plc

- Idemitsu Kosan Co., Ltd.

- INEOS Group

- Nouryon

Competitive Analysis

The competitive landscape of the Methyl Ethyl Ketone (MEK) Market is shaped by leading global chemical manufacturers that focus on production capacity expansion, sustainable innovation, and diversification of applications to strengthen their market presence. Key players include Shell Plc, ExxonMobil Corporation, Arkema S.A., Sasol Limited, INEOS Group, Maruzen Petrochemical Co., Ltd., Idemitsu Kosan Co., Ltd., Nouryon, ENEOS Corporation, and Nova Molecular Technologies. These companies leverage integrated petrochemical operations and global supply chains to ensure steady availability of MEK across regions. ExxonMobil and Shell emphasize large-scale petrochemical production and investment in process efficiency, while Arkema and INEOS focus on specialty chemical innovations and sustainable solvent alternatives. Sasol and Idemitsu Kosan contribute through diversified product portfolios and regional supply strengths, particularly in Asia-Pacific. Nouryon and ENEOS strengthen competitiveness by investing in advanced manufacturing and eco-friendly formulations. Nova Molecular Technologies differentiates itself by offering high-purity MEK solutions for niche applications, including electronics and specialty chemicals. The market remains moderately consolidated, with these players competing through technology upgrades, environmental compliance initiatives, and long-term partnerships with end-user industries such as paints, coatings, adhesives, packaging, and automotive.

Recent Developments

- In April 2025, ExxonMobil increased its MEK pricing by $0.08 per pound, reflecting supply chain recalibrations and cost pressures in raw materials.

- In December 2024, Arkema acquired Dow’s flexible packaging laminating adhesives business, strengthening its position in MEK-related adhesive solutions.

- In November 2024, Nouryon completed a capacity expansion for organic peroxides at its Ningbo, China facility, doubling production capacity to 6,000 tonnes each for Perkadox® 14 and Trigonox® 101, enhancing supply reliability for polymer applications

- In August 2024, Sasol Chemicals today introduced SASOLWAX LC100, an industrial wax grade with a 35% lower carbon footprint, further expanding its growing sustainable product.

Market Concentration & Characteristics

The Methyl Ethyl Ketone (MEK) Market reflects a moderately consolidated structure with dominance by a few multinational chemical producers that control significant portions of global supply. Key players such as ExxonMobil, Shell, INEOS, Arkema, Sasol, and Idemitsu Kosan operate large-scale facilities with integrated petrochemical feedstocks, ensuring stable production and competitive pricing. It is characterized by strong reliance on paints, coatings, adhesives, and printing inks as primary demand drivers, while applications in lubricants, specialty chemicals, and electronics expand its scope. Regional concentration is evident, with Asia-Pacific serving as both the largest consumer and a major production hub, supported by cost-efficient feedstock availability. It demonstrates high entry barriers due to capital-intensive infrastructure, regulatory requirements, and complex supply chains. The market evolves with trends toward sustainable and bio-based alternatives, shaping competition through innovation and compliance with environmental standards. It maintains steady growth potential while remaining exposed to fluctuations in petrochemical raw material prices and global trade dynamics.

Report Coverage

The research report offers an in-depth analysis based on Product, Application, End-User Industry and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Asia-Pacific will continue to drive demand growth, supported by industrial expansion and infrastructure development in emerging economies.

- Printing inks application will gain rapid market share, fueled by high-speed packaging requirements in food, pharma, and consumer goods sectors.

- Emerging markets will invest more in bio-based and eco-friendly MEK alternatives to comply with tightening VOC regulations and circular economy goals.

- Manufacturers will focus on improving production efficiency and reducing environmental impact through enhanced refining and purification technologies.

- Electronics sector will expand its use of MEK in precision cleaning of components, driven by rising demand for high-purity solvents.

- Leaner and flexible supply chains will become critical as raw material volatility and geopolitical shifts pressure MEK producers to ensure steady availability.

- Integrated chemical firms will push for geographic expansion, particularly in Asia-Pacific, to benefit from cheaper feedstocks and scale production.

- Demand for MEK in construction-related protective coatings will strengthen with ongoing infrastructure projects and renovation trends in urban centers.

- Regulatory emphasis on VOC reduction will stimulate reformulation of MEK-based products with improved environmental profiles.

- Supply-demand dynamics will become more regionalized, with local production and distribution optimizing responsiveness to end-user needs.