Mono Ethanolamine Market Overview:

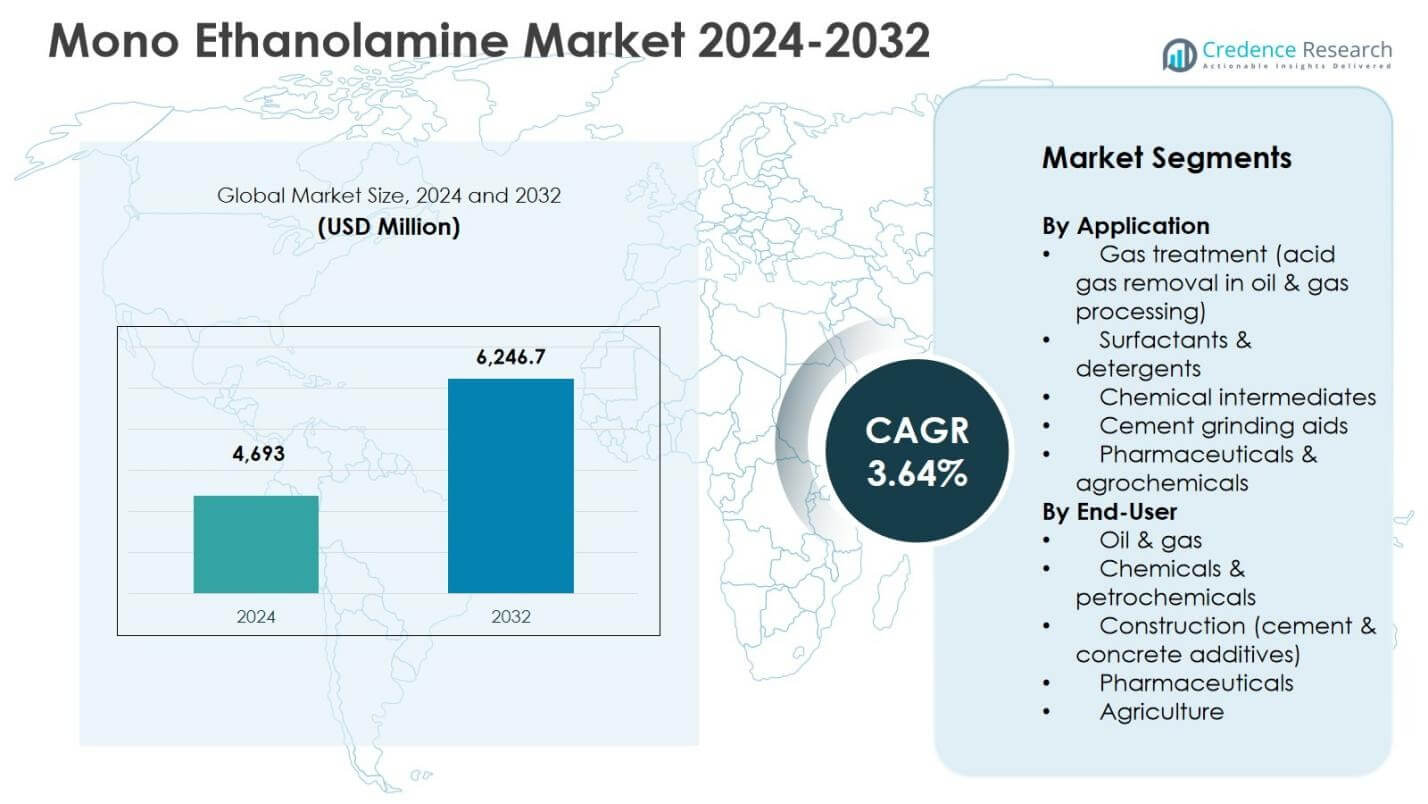

Mono Ethanolamine Market size was valued at USD 4,693 million in 2024 and is anticipated to reach USD 6,246.7 million by 2032, expanding at a CAGR of 3.64% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Mono Ethanolamine Market Size 2024 |

USD 4,693 million |

| Mono Ethanolamine Market, CAGR |

3.64% |

| Mono Ethanolamine Market Size 2032 |

USD 6,246.7 million |

Mono Ethanolamine Market Insights

- Market growth is primarily driven by strong demand from gas treatment applications, which accounted for 6% segment share in 2024, supported by rising natural gas processing, refinery upgrades, and stringent emission control requirements.

- Market trends indicate increasing use of mono ethanolamine in detergents, surfactants, and cement grinding aids, with detergents holding 3% share, while chemical intermediates, cement additives, and pharmaceuticals & agrochemicals together contributed 37.1% in 2024.

- Market restraints include volatility in ethylene oxide and ammonia prices and tightening environmental regulations, which impact production costs and compliance requirements across price-sensitive end-use industries.

- Regional analysis shows Asia Pacific leading with 6% share in 2024, followed by North America at 28.4% and Europe at 23.1%, while Latin America and Middle East & Africa collectively accounted for 13.9%, supported by energy and infrastructure development.

Mono Ethanolamine Market Segmentation Analysis:

By Application:

By application, gas treatment dominates the Mono Ethanolamine market, accounting for 38.6% market share in 2024, driven by its critical role in acid gas removal processes such as CO₂ and H₂S scrubbing in oil and gas operations. Mono ethanolamine’s high reactivity, absorption efficiency, and cost-effectiveness make it a preferred solvent in natural gas processing and refinery units. Surfactants and detergents follow with 24.3% share, supported by rising demand for household and industrial cleaning products, while chemical intermediates, cement grinding aids, and pharmaceuticals & agrochemicals collectively contribute 37.1%, supported by expanding construction, chemical synthesis, and specialty formulation activities.

- For instance, Dow offers Monoethanolamine 100% GT Grade, a formulated amine solvent specifically for gas treating to remove H₂S and CO₂, particularly where deep CO₂ removal is required in natural gas streams.

By End-User:

By end-user, the oil & gas sector leads the Mono Ethanolamine market with a 41.2% share in 2024, supported by sustained investments in natural gas processing, refinery upgrades, and stringent emission control requirements. Mono ethanolamine remains a core chemical in gas sweetening units due to its proven performance and operational reliability. Chemicals & petrochemicals hold a 27.5% share, driven by its use as an intermediate in multiple formulations. Construction accounts for 16.4%, supported by cement additive demand, while pharmaceuticals and agriculture jointly represent 14.9%, driven by increasing specialty chemical and agrochemical production.

- For instance, SABIC supplies Monoethanolamine 99% as a raw material for manufacturing ethylene diamine and other chemical intermediates in petrochemical processes.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Key Growth Drivers

Rising Demand from Gas Treatment Applications

The Mono Ethanolamine market is strongly driven by rising demand from gas treatment applications, particularly in natural gas processing and refinery operations. Increasing global consumption of natural gas, supported by energy transition initiatives and stricter emission regulations, has accelerated investments in gas sweetening units. Mono ethanolamine remains a preferred solvent for CO₂ and H₂S removal due to its high absorption efficiency, operational simplicity, and cost advantages. Expansion of LNG infrastructure, refinery modernization, and upstream gas projects across Asia Pacific, the Middle East, and North America continue to support sustained consumption growth.

Expansion of Surfactants and Detergents Industry

Growth in the surfactants and detergents industry significantly supports the Mono Ethanolamine market. Rising urbanization, higher hygiene awareness, and increased use of household, industrial, and institutional cleaning products are boosting demand. Mono ethanolamine plays a critical role in formulation stability, pH control, and emulsification in detergent and personal care products. Strong demand from emerging economies, combined with consistent consumption in developed markets, ensures stable volume growth. Additionally, the expansion of industrial cleaning solutions across manufacturing and healthcare facilities further reinforces long-term demand.

- For instance, Dow’s Monoethanolamine (MEA) is incorporated into heavy-duty detergents for reserve alkalinity, effective oil removal, and anti-redeposition properties during laundry processes, preventing soil from resettling on fabrics.

Increasing Use in Cement and Chemical Manufacturing

The increasing application of mono ethanolamine in cement grinding aids and chemical intermediates is a key growth driver. Rapid infrastructure development and urban construction activities are boosting cement production volumes, particularly in Asia Pacific, the Middle East, and Africa. Mono ethanolamine improves grinding efficiency, enhances cement performance, and reduces energy consumption, making it a preferred additive. Simultaneously, its role as a versatile chemical intermediate supports demand from agrochemicals, pharmaceuticals, and specialty chemicals, strengthening its multi-industry growth potential.

- For instance, Dow supplies MEA specifically for cement grinding aids, where it reduces particle agglomeration and optimizes energy use during milling.

Key Trends & Opportunities

Shift Toward Natural Gas and Cleaner Energy Systems

A major trend shaping the Mono Ethanolamine market is the global shift toward natural gas and cleaner energy systems. Governments and energy producers are prioritizing lower-emission fuels, resulting in increased investments in gas processing facilities and LNG terminals. Gas sweetening remains an essential step in natural gas value chains, creating sustained demand for mono ethanolamine. Expansion of cross-border gas trade and LNG capacity in Asia and Europe further strengthens growth opportunities, positioning mono ethanolamine as a critical component of the global energy transition.

- For instance, INEOS offers Gas/Spec CS-1, outperforming monoethanolamine in gas removal capacity per circulating volume for natural gas and LPG treatment. This formulation lowers operating costs in existing gas processing equipment.

Industrial Growth in Emerging Economies

Emerging economies present strong opportunities for the Mono Ethanolamine market due to rapid industrialization and expanding domestic chemical production. Countries across Asia Pacific, Latin America, and the Middle East are investing heavily in petrochemicals, construction materials, and agriculture-related chemicals. Rising local manufacturing capacity and supportive government policies are encouraging increased consumption of mono ethanolamine. This trend supports supply chain localization, reduces import dependence, and creates long-term growth opportunities for both regional and global manufacturers.

- For instance, Petronas Chemicals Group Berhad produces monoethanolamine (MEA 90%) at its Malaysian facilities using Dow-licensed technology, supporting petrochemical applications in Southeast Asia.

Key Challenges

Volatility in Raw Material Prices

Volatility in raw material prices remains a major challenge for the Mono Ethanolamine market. Production depends heavily on ethylene oxide and ammonia, which are influenced by fluctuations in crude oil and natural gas prices. Supply disruptions, geopolitical uncertainties, and feedstock availability issues can significantly impact production costs. Manufacturers often face difficulty passing cost increases to end users, particularly in price-sensitive segments such as cement additives and bulk chemicals, which can pressure margins and affect overall market stability.

Environmental and Regulatory Constraints

Environmental and regulatory constraints pose ongoing challenges for the Mono Ethanolamine market. Increasing scrutiny related to occupational safety, wastewater discharge, and chemical handling is raising compliance costs for manufacturers and end users. Regulatory frameworks governing ethanolamine exposure and disposal are becoming more stringent across developed regions. Additionally, growing interest in alternative amine blends and advanced gas treatment technologies may limit mono ethanolamine adoption in specific applications, requiring continuous product innovation and regulatory alignment to maintain competitiveness.

Regional Analysis

North America

North America accounted for 28.4% of the Mono Ethanolamine market share in 2024, supported by strong demand from the oil & gas, chemicals, and detergents industries. The region benefits from a well-established natural gas processing infrastructure, where mono ethanolamine is widely used for acid gas removal. Stringent environmental regulations related to emissions control further support sustained consumption. The presence of major chemical manufacturers, advanced refining capacity, and steady demand from cement additives and specialty chemicals continues to strengthen regional growth. Ongoing investments in LNG terminals and refinery upgrades reinforce North America’s stable demand outlook.

Europe

Europe held a 23.1% share of the Mono Ethanolamine market in 2024, driven by regulatory compliance requirements and mature industrial applications. The region’s focus on emission reduction and clean fuel usage sustains demand for gas treatment chemicals in refineries and natural gas facilities. Mono ethanolamine is also widely consumed in surfactants, detergents, and chemical intermediates due to strong manufacturing standards. Growth is further supported by steady construction activity and cement additive usage across Western and Central Europe. The presence of leading chemical producers and strong R&D capabilities enhances product optimization and long-term market stability.

Asia Pacific

Asia Pacific dominated the Mono Ethanolamine market with a 34.6% share in 2024, driven by rapid industrialization, expanding petrochemical capacity, and large-scale infrastructure development. Strong growth in natural gas processing, cement manufacturing, and agrochemicals across China, India, and Southeast Asia fuels high consumption levels. Rising urbanization and increasing demand for detergents and cleaning products further support market expansion. Government-led investments in energy infrastructure and domestic chemical manufacturing enhance regional demand. The availability of cost-effective production and growing downstream industries positions Asia Pacific as the fastest-growing regional market.

Latin America

Latin America accounted for 7.6% of the Mono Ethanolamine market share in 2024, supported by moderate growth in oil & gas processing, construction, and agriculture. Countries such as Brazil and Mexico drive regional demand through refinery operations, fertilizer production, and cement manufacturing. Increasing investments in natural gas infrastructure and gradual industrial modernization contribute to steady consumption growth. Mono ethanolamine usage in agrochemicals and detergents also supports demand, particularly in expanding urban markets. While smaller in scale, the region offers long-term growth potential through infrastructure development and rising domestic chemical production.

Middle East & Africa

The Middle East & Africa region captured 6.3% of the Mono Ethanolamine market share in 2024, primarily driven by extensive oil & gas activities and refinery operations. Mono ethanolamine plays a critical role in gas sweetening across major hydrocarbon-producing countries. Growing investments in petrochemicals, LNG facilities, and downstream processing support consistent demand. The construction sector also contributes through cement grinding aid applications, particularly in infrastructure-driven economies. Although market size remains comparatively smaller, expanding energy projects and industrial diversification initiatives are expected to strengthen regional consumption over the forecast period.

Mono Ethanolamine Market Segmentations:

By Application

- Gas treatment (acid gas removal in oil & gas processing)

- Surfactants & detergents

- Chemical intermediates

- Cement grinding aids

- Pharmaceuticals & agrochemicals

By End-User

- Oil & gas

- Chemicals & petrochemicals

- Construction (cement & concrete additives)

- Pharmaceuticals

- Agriculture

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

Competitive landscape analysis of the Mono Ethanolamine market indicates a moderately consolidated structure dominated by BASF SE, Dow Inc., SABIC, INEOS Group, Nouryon, Huntsman Corporation, Nippon Shokubai Co., Ltd., Amines & Plasticizers Ltd., Indorama Ventures Public Company Limited, and Zhejiang Jianye Chemical Co., Ltd. These companies compete primarily on production capacity, product quality, supply reliability, and cost efficiency. Leading players leverage integrated feedstock access and global manufacturing footprints to ensure stable supply across key end-use industries such as oil & gas, chemicals, and construction. Strategic capacity expansions, long-term supply agreements, and regional footprint strengthening remain common competitive strategies. Companies are also focusing on process optimization, regulatory compliance, and sustainability initiatives to meet evolving environmental standards. In addition, partnerships with downstream users and investments in emerging markets enable players to capture growing demand, while smaller regional manufacturers compete by offering cost-competitive solutions and localized supply advantages.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- BASF SE

- Dow Inc.

- Nouryon

- SABIC

- INEOS Group

- Nippon Shokubai Co., Ltd.

- Huntsman Corporation

- Amines & Plasticizers Ltd.

- Indorama Ventures Public Company Limited

- Zhejiang Jianye Chemical Co., Ltd.

Recent Developments

- In February 2023, Nippon Shokubai acquired ISCC PLUS certification for mono-ethanolamine produced at its Himeji and Kawasaki plants, enabling sustainable biomass-derived production.

- In September 2024, BASF launched a new plant for alkyl ethanolamines at its Antwerp Verbund site, enhancing production capabilities relevant to the mono ethanolamine market.

Report Coverage

The research report offers an in-depth analysis based on Application, End User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand will remain stable due to sustained consumption in gas treatment and acid gas removal applications.

- Expansion of natural gas infrastructure will continue to support long-term market growth.

- Increasing detergent and surfactant production will strengthen recurring demand from consumer and industrial sectors.

- Cement grinding aid applications will gain traction alongside rising global infrastructure development.

- Growing chemical intermediate usage will support diversified end-use demand.

- Asia Pacific will continue to lead growth due to rapid industrialization and capacity expansion.

- Emerging economies will attract new investments in local ethanolamine production facilities.

- Process optimization and efficiency improvements will enhance production competitiveness.

- Regulatory compliance and environmental management will shape product formulation and handling practices.

- Competitive intensity will increase as regional players expand capacity and global suppliers strengthen supply chains.